Concall may 2025(moldtek pack)

MOAT

A…Tool room and various molds

That is strong moat. Very difficult for other companies and strong entry barrier.

B…Pharma USP: Rapid mold and product development due to in-house tool room—“Mold-Tek could do it in 1.5 to 2 months vs. 4-5 months for competitors.

=The point what Mold-Tek is trying to drive to pharma companies is our ability to develop new products faster than anybody else. Even the leaders in pharma packaging, we are in a position to meet or exceed them in terms of new product development.

=======================

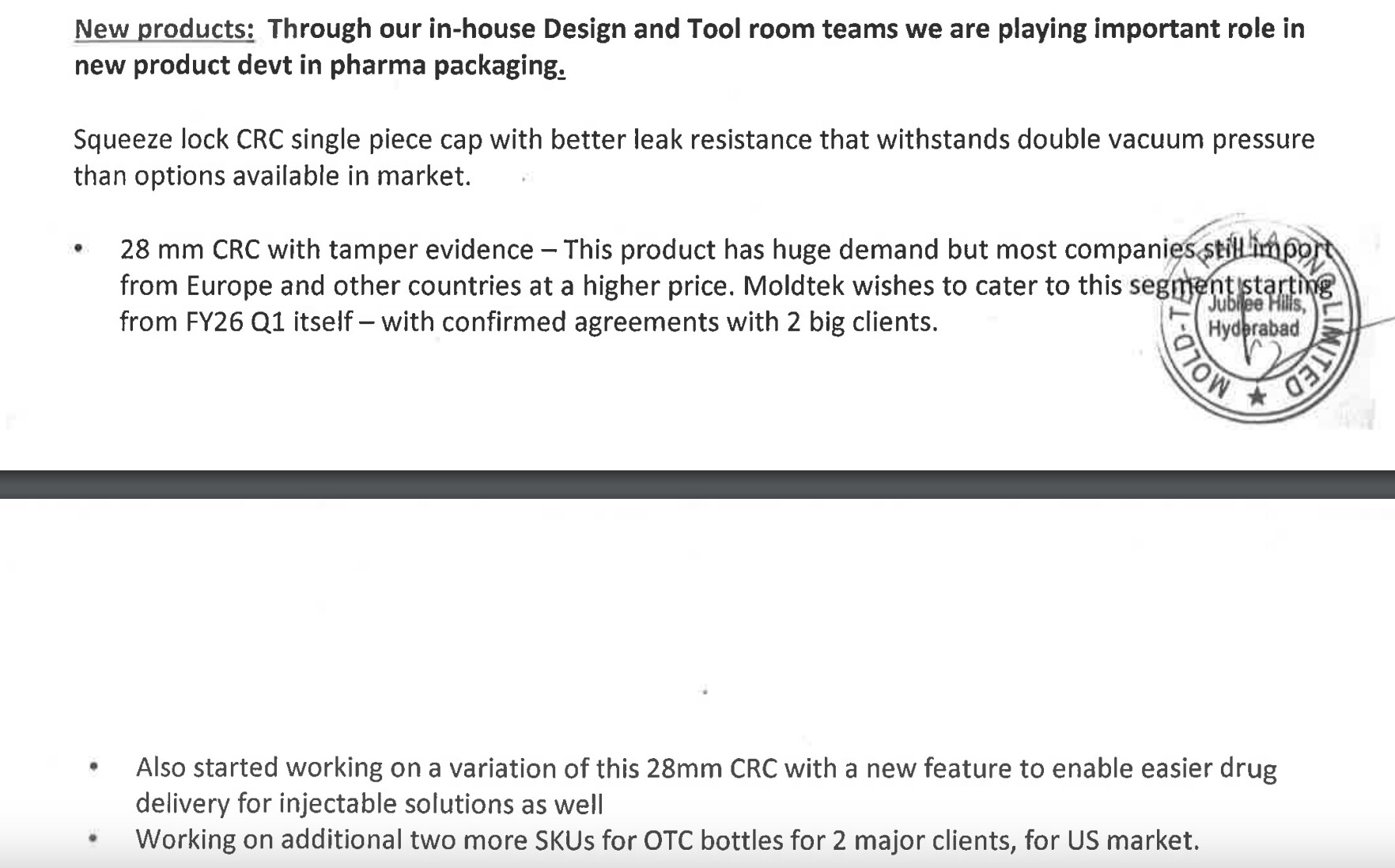

1…Pharma

=As an opportunity, pharma is a huge

opportunity, close to Rs. 5,000 crores opportunity, including both exports and the Indian market.

So, even if we reach 1% to 2% of the market share, it will be close to Rs. 100 crores.

=By end of 1st year itself, company

achieved over 50% capacity

utilization to reach Breakeven level.

Further capacity expansion across

product mix planned by Q1/Q2.

=Out of 20+ pharma clients who cleared audits, only 4-5 have started commercial buying; more expected to ramp up.Huge opportunity ahead.

2…FMCG

A…Printing capacity

enhancement for handling

seasonal demand

FY 25 F&F growth of 11.76% as the new printing capacities started improving quarterly numbers

B…Square pack

FY 25 growth of 17.34% fueled by detergent segment and cashews

3…Paint

A…Aditya Birla steady growth

Aditya Birla Group (ABG): Capacity enhancement (brownfield) at Cheyyar and Panipat, operational from March/April.

B…Asian paints

IML adoption

Increased IML adoption; all four plants (Hyderabad, Satara, Vizag, Mysore) now equipped for IML production.

4…Lubricants

=Long term contracts to safe-guard volume share from industry leaders like Gulf, Shell, Castrol

5…Capex

A…pharma

-Capacity Expansion:

Current: 1,500 TPA; ramping up to 3,000 TPA by March 2026.

-Capex: Adding 5 new injection molding machines; molds arriving by June.

-Land: Applied for 2.5 acres adjacent to existing Sultanpur facility for future pharma expansion.

B…Printing Capex: @ Rs. 25 crore printing capacity up >70%.

=FY25 Capex: ~Rs. 140 crore (higher than earlier guidance of Rs. 70-80 crore), split between pharma, printing, and incremental paint capacity.

FY26 Capex Guidance: Rs. 70-80 crore.