over ownership is the biggest reason , some MF holdings have beat the drums & spread it to the last mile, these kind of stock doesn’t move easily when there is no local buyer left,

4 Likes

My observation post analysis

Positive points

- Only integrated player who makes its own robots, labels and moulds

- When competition in IML increases to manufacture Pails (huge part of portfolio), a EBITDA per ton expansion is likely. Currently this is not possible as Moldtek is the only player in IML.

- Pharma packaging is a good segment to give a growth with higher EBITDA per ton

- There are many segments waiting to transition to Plastic packaging (for ex Plastic based hospital furniture). Being a leader in the segment Moldtek has all resources to venture into many other industries of plastic products where margins are high.

- Business succession seems to have been taken care of as the promoters son and Nephew seems to have a good hold over the business. The son has proved the same by adding pharma sector packaging to the kitty.

- Regulatory risk is low as they can make upto 25% use of recycled plastic in their products as per new EPR (extended producer responsibility) norms

- With expansion over different geographies, company is trying to build a moat by being the only player who is present closer to the clients all manufacturing facilities through out the country

Some Risks

- Largely a family business with many family members already working at several positions

- Currently they might not be able to use IML for Manufacturing Pails for Paint industry

- Majorly a domestic play, export will not be more than 10% as logistics cost make export unviable

Note: Invested

12 Likes

Concall@ Q1 -2025(Aug 2024)

As per management

=Growth triggers will be

A…Q pack

B…Pharma

C…ABG(paint)

=Descent numbers will be seen from 2026.

1…Expected growth

=Mid- to high-teens volume

growth for this year and possibly next year as well

2…New plants utilization

=All the projects have started

commencing their commercial production in the last few months, starting from our plant in

Cheyyar and Panipat for ABG and then the third plant is our pharma products at Sultanpur Hyderabad.

=Cheyyar and Panipat plants are

running around 15% to 25% capacity utilization.But now it is

around 40% in June. And we are seeing more than 50% utilization coming from July onwards.

=Pharma plant is hardly running at 10% capacity utilization. We are just doing a few EV tube sales have picked up. Various clients have taken our trial supplies, and filling line adoption and trial batches have been successfully completed. And now slowly, we expect the bulk orders to start coming in.

=Going forward, the good news is that both the pharma and ABG plants are indicated to do better in the coming quarters and hopefully will add better volumes from Q2 and Q3

2…F and F

=The Food & FMCG grew by about 4.5% compared to the previous Q1. But compared to Q4, it’s a healthy 24% growth.

A…Q pack

=It grew robustly at around 45% compared to the Q1 last year.

=Qpacks is where we are finding solid demand coming in, inquiries coming from major players for our edible and ghee and even other sectors. So I’m very confident of what we – last year, it did almost 60%, 70% growth in Qpack. Probably, it’s not that much, at least 40% to 50% volume

growth is possible in Qpacks.

=And in Qpack, our margins are not as good as thin walls. So that is why,

though, the 21% growth in the overall food and Qpack has come, it has not contributed handsomely to the bottom line improvement and EBITDA improvement

B…Ice cream

=Competition in some sectors of ice cream, especially in the interior sections in North and South, deep in the South, we are losing due to some competitors holding up with the standard ice cream packs

=There is some pressure. Once there is a competition increasing, you need to adjust your pricing

to retain your major players, so we could successfully do. But there are pockets of small players

and they, indeed, arise only in the season, due to which we also let go.

And they will be looking at – even at 3%, 4% price advantage and they’ll lap it. So that way, we

miss the growth burst in ice cream this season. And going forward also, that should be a reality,

because there will be players who will make standard products like ice cream cups and diary

cups also to some extent.

And they will be able to garner local demand,

=Bigger companies will look at, not only just the pricing, but they also look at the volume or ability to house several molds and several

robos, which will, in case of any breakdown, there won’t be any disruptions. So bigger players

won’t leave us.

=Like, same in the paint industry. Earlier, we used to supply to everybody. But today, we are only restricted to top 5, 6 companies.

=Similar to ice cream industry also, we are with all the top companies but let go some of these small companies who are far away and they’re periodic in their buying and they are very stingy about pricing.

=Do we plan to move beyond ice cream packs ?

Lakshmana Rao: Of course, this is the idea. We keep moving on with a new set of products for new applications.

And that – in this direction, we are – Qpacks are growing rapidly now because that is where we

are finding new adoption happening in various new product segments, so that is focus point now.

Even in North, we are starting our Qpacks at least 2 sizes, 10- and 15-liter will be starting in October and necessary equipment is being installed out

C…Growth in f and f

a)Q pack, ofcourse will have 40% to 50% volume growth

b)Our north plant, which will be starting in August, September, probably September, it will start some products and pick up by next season. It would be the way to grow again into double digits. That’s in Food & FMCG.

c)Couple of those projects got delayed, which has impacted the growth in this year. Once those clearances come, they will improve. It can happen from Diwali or even before Diwali.

d)Another reason some of the products which we have developed them molds, they have not yet taken off. Only Kissan Jam has taken off the past 2, 3 months. And other products, for HUL and others, are still in a different stage of adoption. So those numbers have not yet come to contribute

=But the numbers may not reach 20%, 25% growth levels, which we achieved in the last 5, 6 years. Such growth we will only see in pharma going forward.

=But Food & FMCG will continue to play an important contribution to our growth. I’ll be happy

even if we close only Food & FMCG thin wall at 10%, with Qpack around 40% to 45%. Therefore, together will be contributing around 20% to the volume growth.

4…Paint@ABG

= They are picking up faster now. The

pace of their production and the orders are increasing rapidly.

=And we hope hereafter, we can

even see around 8% to 10% growth coming in the paint sector.

=Coming to ABG, their indications are pretty strong. And our third plant, the Mahad, supplies will be starting from September on a trial basis. But by October, November, it will pick up pace. And those numbers will be added to improve our volumes further.

=We’ll be adding at least

60% to 75% capacities, which are currently for ABG

=ABG is certainly a torch bearer of growth for us for the next couple of years. And by then, pharma should be able to give us the impetus.

5…Pharma

=We are very excited about our entry into pharma because we notice, in pharma also, a lot of

players are not agile in terms of development of new products. It takes a long time in their

abilities to showcase to the pharma company about – by providing samples or 3D designs. Our

concepts, it seems to be, in our first few months of marketing, we noticed that the pharma industry is really looking for such a well player. So Mold-Tek can be run because of our product design, mold design and mold manufacturing facilities. So we’re really hopeful that our way to

pharma will be very successful in the coming years.

=Already in EV tubes IML, we have achieved a breakthrough, which many players could not do that

=And like that – in other products like canisters and various types of caps and bottles, we have

already submitted at least 5, 6 products newly developed within these 4 months to various clients.

=So that is the speed at which we are able to develop new products. I’m sure that is where I’m going to be, our USP in winning the clients

=Already, 4 major clients have audited and cleared our premises and accepted us as the vendors. Several

products, I would say, more than 4 to 5 products are under development. Most are at final stage now. Some samples have also been submitted. As I told you, the stability tests and approvals

take a long time in pharma. But some of them are on the anvil, which could even get cleared in September, and some of them in October and November.

=Almost 6 or 7 such players have already put us in the list. And some of the products have been already

offered to us for development and sample submission.

So this process takes maybe another 3 to 6 months to stabilize

=So for a company which is hardly 3 months old, getting 7 audits done and 3, 4 already

approved is definitely a good milestone

= I’m very positive the way our plant has been approved by various major pharma players and being given a clean chit to go ahead to their respective vendor development teams.

=So as I said, from Q3, we will see decent numbers coming from pharma. In this Q1, it’s hardly a

beginning with 80 lakhs worth of goods sold in pharma sector. But this number can swell in the

coming quarters, maybe second quarter, it could be INR2 crores to INR2.5 crores. But in the

third and fourth quarter, it can go up to INR5 crores to INR6 crores each. So our overall guidance

of around INR15 crores to INR20 crores, we are still confident in pharma, which will be coming

at a much higher EBITDA. So once those numbers come in from third quarter, we’ll be seeing

better growth in both in terms of volumes and even in EBITDA.

=If things go well in pharma, what we anticipate will be more stable from next year because this

year will be our introductory and then approvals and statutory clearances and various things,

which we almost crossed. But client approvals and stability tests will take a little longer time.

=. From Q3 onwards, we will be

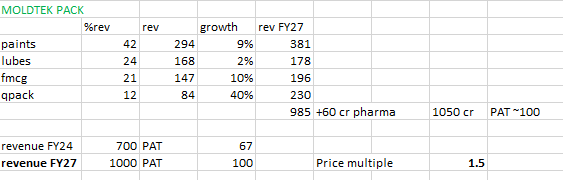

seeing decent numbers coming in. But the numbers, if you ask me, in the year '25/'26, they will be decent. And if things go well as per plan, '26/'27 would be a major year where pharma will be contributing handsomely, and that can shoot up our numbers beyond INR1,000 crores top line and even INR100-plus crores in the PAT.

6…Revenue

=In terms of revenue, paint is 42.5%, lubes is 23.8%, Food & FMCG is 21.17%, Qpack is 12.11%,

pharma is 0.4%.

7…Near future growth

Q=You mentioned you’re maintaining a mid-teen kind of a volume guidance for the year, so that there’s an extremely high 9-month run rate to catch up. So apart from the ABG, which is expected to operate at 50% utilization of around 1,000 tons, any

other green shoots you are seeing in the lubricants or the base paint customers that you’re adding

for such a high 9-month run rate?

Ans=

A…ABG, more than 1,000 tons per month will be the addition because Mahad plant also will start from September, .

B…Pharma

So along with that and pharma, we are still hopeful that we’ll be reaching

close to 15% volume growth.

=Q2, that is rain-impacted season, will be difficult to clock such a big number. But from Q3 onwards, we see a good ramp-up coming up in our capacities to ABG and also numbers from

pharma. Yes, it is a challenge, but we still keep 15% as our guidance. We try to achieve that.

8…Asian paint

Q=For the Asian Paints, like, we have not lost any kind of a market share?

Ans= No. I don’t think that is the case with Asian Paints. Probably, their developed 1 or 2 plants are

subdued due to various reasons, but they are not impacted as of now at least, certainly not.

=There is no conflict of interest for our business with ABG as we also supply other paint companies too.

Disc…invested

8 Likes

This stock has consolidated for more than 2 years.

But revenues haven’t seen a significant jump in last few years either.

There needs to be some reason for the stock to capture momentum

Recent quarter number did show sort of uptick in revenues, and if the sctor has bottomed out, we may see revenue growth in coming quarters.

2 Likes

If current valuations sustain, this has ~50% upside in 3 years. Possibly a buy on dips on kind of stock.

Company wise, I like the management. They are continuously working on improving the market size and have enough expertise and goodwill with their current customers.

1 Like

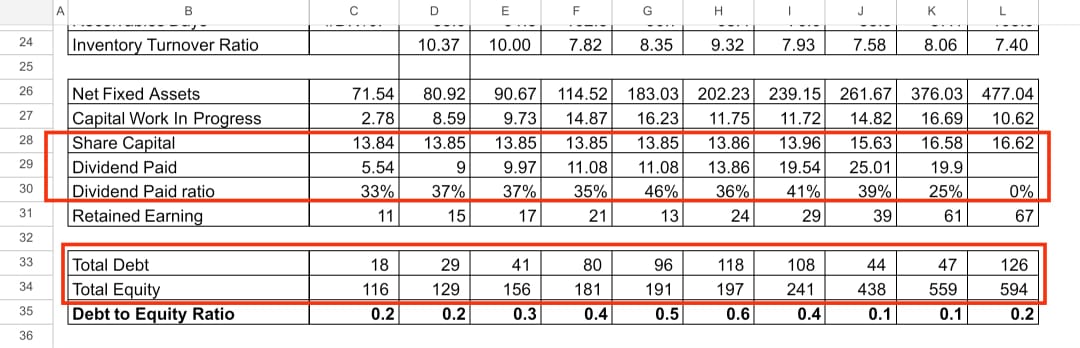

In the manufacturing industry, which is highly capital-intensive, it is generally advisable for a company to retain the majority of its profits. However, in the case of a mold packaging company, it is distributing 37% to 45% of its profits as dividends. Over the past 10 years, the company debt has been rising and in the last 3-4 years, it has also started raising funds through equity.

My question is: why is the company paying a 35% to 40% dividend while simultaneously raising external funds? Wouldn’t it be more prudent for the company to reduce its dividend payout and use those funds internally?

11 Likes

Good question, I wonder if someone has asked this question in the concall before.

Would love to hear from folks if any inputs.

When you analyse a small business, you need to understand, How is the promoter making his money? He needs that dividend & ESOPs or else he will have to steal which many promoters do. Additional equity share issue to QIP helps gain attention from investor community. Its similar to branding.

Note: Invested.

3 Likes

Hi Narendar, the company has a health balance sheet if you look at the Net Debt/EBITDA or interest coverage ratios. They can sustain 30%+ dividend payout without really hurting the balance sheet so by paying a dividend they send a positive signal into the market. Also, the capex need of the business has reduced relative to last few years and this a good cash conversion business. If they hoard this cash on their balance sheet the returns will get impacted so net net its a positive that they do pay dividend while keeping a relatively healthy balance sheet

4 Likes

Basically pkging industry itself is a pure play commodity business, now many other sector co’s are adding machines to make these stuffs but not QR coded one, in commodity space it’s very hard to push specialized product, like paint where every co is joining the band wagon like Astral, JSW etc & more will follow where costing to end user matters, so adopting a pkging which will increase cost is a matter of question, also co claiming to be mkt is accepting specialized product that too is a matter of speculation at this moment, costing minimization is the agenda of customers that may hurt Moldtk’s speculation,

It’s absolutely personal view, may differ with others

3 Likes

Another “Little Champions” stock that is 0 return since 2021. Looks like the sales and EBITDA are actually declining. Expected recovery is only from 2026 - so might decline much further

I am kind of stuck in this stock and will not average down to compound loss but maybe will average when it goes down to 550 in coming year

I am kind of stuck in this stock and looking to exit

2 Likes

This is my personal rant and accountability note for my future self, to unclutter my thought process and biases, especially the sunk cost fallacy

Simple Introduction:

- This is a rigid plastic packaging company.

Raw Material: Crude derivatives - (Reliance Industries for procurement)

End-user Industries:

- Paints

- Lubes

- FMCG

- Pharma

Mental Model

Value Added Business - Converter type, taking a commodity raw material and convert into something more valuable

Buy Rationale

45,000MTA to70,000MTA new capacity addition in 2 years

Bottom line margin expansion due to product mix change

Moat:

- Plants near by to customer, which reduces their freight cost and makes it sticky

- Low-cost producer, inhouse robots, adopting latest tech and new product development capability

- Successfully pushed to adopt new products - IML on paint industry

- Having Stable margin 18-20% indicates they are able to pass on the raw material fluctuations

Current State:

Lubes is a saturated industry so not much of volume growth: Low ebita per/kg (25-30 rs)

Paints industry facing headwinds and uncertainty (Birla , JSW) - However this is somewhat mitigated by supplying to all three big players - Asian, Berger and Birla . Still not much of growth expected for another 6-8 quarters ebita per/kg (30-40 rs)

Qpacks: Ebidta between lubes and paints , we can conclude it is in similar range (30rs)

FMCG slow down, economic slowdown - Higher Ebita per/kg (60-80rs)

Pharma expected to be around Ebita per kg 150rs

Most of the customers are currently facing headwinds, which I believe are transient in nature, However, currently almost 90% of the business cater to lower ebita per kg so overall avg ebita per kg as company is 36-38 now

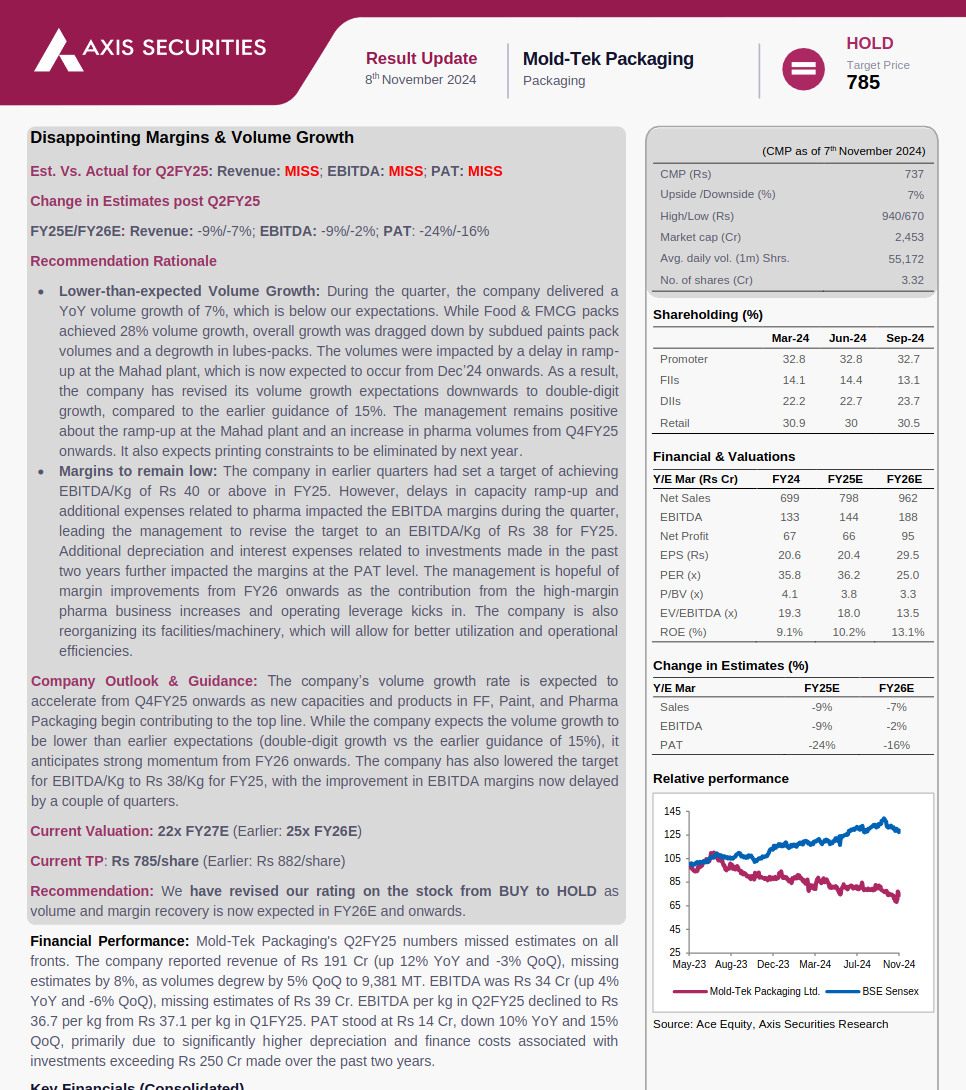

Source: Q2 Fy 25 concall

Last year it was 50.8% and it is now 50% paint. Last year lubes was 24.6%, it has now come

down to 21.9%. Food and FMCG 11.85% to 11.77% and Qpack from 12.72% to 16.12%, pharma

is 0.26% this year.

Mistake on my side

- Taking the guidance on the face value from the promoter and loading up.

- Over allocation and averaging down (overpaid), opportunity cost

- I bought this stock due to Marcellus’ addition (This was before VP, couple of years back and I needed them for forensic account fraud detection (still need others help) )

- This business had to utilise around 39000 out of 45000 , so until new capacity come to online which may take few quarters to a couple of years

- This is the business which was facing similar kind of situation in top line earlier too, however bottom line was aided by IML adoption

Here no volume growth

But this may be attributed to end user slowdown still I should have been more prudent

Personal Commentary on Management

I genuinely don’t think Promoter is an ill intensioned person, however so far past 3 years he has been over promising and under achieving or at least missing it barely.

He is quite optimistic guy of future

Still I should have to take 70-80% of what he guides

But has extensive experience in this industry and is tech-savvy in their domain, always pushing for innovation and winning new business

Future Prospects

Apart from the obvious utilising the newly added capacity and recovery of end-user industries , their growth solely hinges on pharma and FMCG adoption, Pharma takes typically 12-18 months after the initial audit to commercial production - Currently, IML is not needed in Pharma companies its for decoration only, however their moat here is that their quality and adoption & development of new products quickly then anyone else in the industry

Example:

In the canisters, ours is single piece canisters whereas the others are

majority of them are in two piece. So, this will give them lot of benefits in not only cost but also

in safety and non-breakage of the canisters during usage. So, these two benefits will go a long

way in being able to penetrate into the market. Already in EV tubes we are seeing that. In

canisters our supplies are being tested in what you call trial runs and hopefully bulk orders will

start coming in from December.

Refer q2Fy25 concall, I would suggest to read the whole transcript which is quite informative on pharma section

So far 100 crore invested in pharma - which may bring 80 -100 crore on pharma segment, from January they may have 15-25 crore top-line (Proabably)

so next financial year they may do somewhere between 25-50crore in pharma (conservative as per me)

Currently, they claim already they have 8-10 pharma companies are on the line and always in constant talks with all the players for the adoption

Managment claims pharma is 5000 crore industry both domestic and export, if they are able to be major player in the pharma then they can be one of best long term wealth creator

Anti thesis:

- Not able to scale up pharma-section and FMCG section

- Not able to win new customers - should be tracked every quarter

- Having some sort of quality issue their molds and packages which spoils the reputation in the pharma section

Sell Rationale

-

This is exactly the type of business should be accumulated through the mutated volume growth and sold near highest capacity utilisation

-

There is no scope for further PE expansion for this type of business at least not in the long term, best time to buy this stock would be around 200 levels (PE expansion) (right after covid )

-

Since their margins are stable and given the accreditve product mix, I think they should be able maintain this current band of PE

-

So unless they find a way to produce/ accommodate for pharma in existing capacities i.e: replacing dud lubes packaging to pharma and FMCG, (low ebita to high ebita products), I should sell it in the next up cycle once they reach the peak utilisation regardless of the overall market condition and look to re-enter again once they fell 25-35%

Disclaimer: Invested with 21% loss currently second highest allocation in my PF. and sell side rationale is for my reminder, reflects my current thought process, views are welcomed.

21 Likes

I have been tracking this company for more than 2 years. It’s in a stagnation/sideways mode. Unfortunately, most of their business comes from Paints & Lubes which had almost no growth for the last year. I believe the management has been trying to move to higher ebidta/kg segments like pharma, but for them to scale up they would need to make use of the current capacity and see if they can win contracts. I’m currently watching their pharma and FMCG segment which have the highest ebidta/kg and they’re slowly moving away from Paints & Lubes (low margin).

3 Likes

I have also taken a tracking position around 1 month earlier keeping the fact that Birla OPUS entering into paint segment. It is currently down around 10% from my buying price. I have an opinion that although sales are not growing and remains stagnant from last few years, but intrinsic value of company is increased due to capex in pharma packaging sector.

They are facing some challenges in supplying paint bucket to one of the Birla OPUS plant due to unavailability of IML printing machines, which is why they are supplying to Birla OPUS from their other plant.

Pharma packaging is a key sector to watch as it can command higher ebita/kg. Will continue to track results and concall to have pulse of the business.

3 Likes

Basically packaging segment is full commodity in nature Globally, what ever you try to establish as a premium it’s not, Moldtk main revenue is paint segment where many player has appeared & margin of profit may shrink as everyone will lure Dealer with that, so shifting to expensive packaging quickly is really doubtful, also policy change in USA in pharma segment may boost sentiment but actual demand tick may take time, that’s why it’s in a consolidation mode for long & will be, also some broking house pump it & over ownership has been created, but fundamentally a good stock with uncertainties

6 Likes

Nov 2024(Q2-2025) concall

1…Growth

=We are lagging behind our target of 15% volume growth for full year due to delay in projects execuation including printing

=Next year onwards we should be in the position to reach somewhere around 12% to 15% volume growth

=Going forward to 2025-26, I am positive about it because all these numbers because

A…Pharma will contribute handsomely.

B…ABG paints

C…Q pack

D…Printing capacity addition

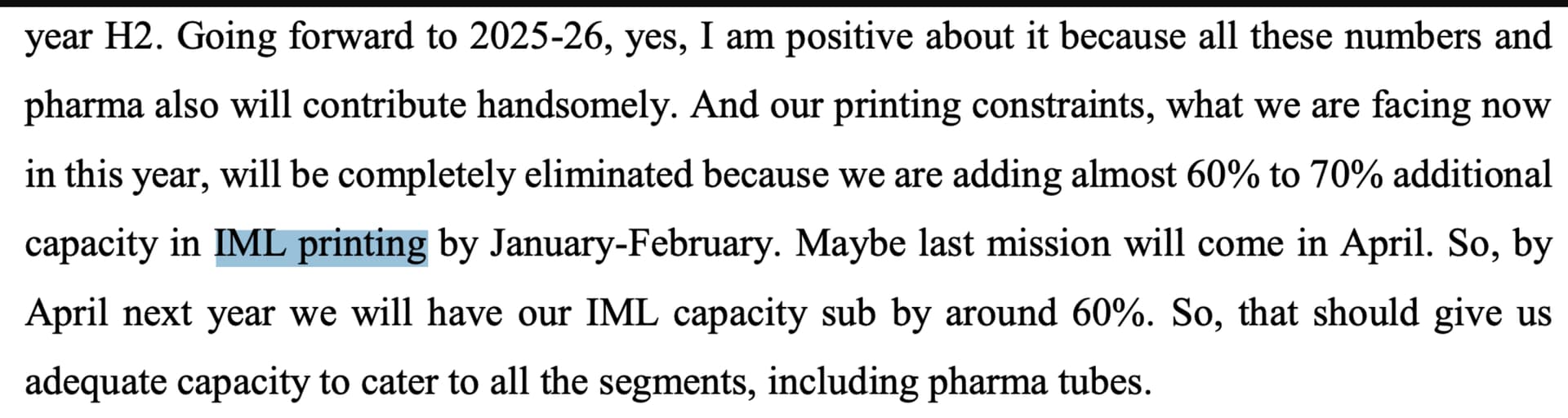

=Our printing constraints, what we are facing now in this year, will be completely eliminated because we are adding almost 60% to 70% additional

capacity in IML printing by January-February. Maybe last mission will come in April. So, by

April next year we will have our IML capacity sub by around 60%. So, that should give us

adequate capacity to cater to all the

2…EBITDA IMPROVEMENT

=We have increased staff cost, because for all these several projects across the country, especially

pharma, we have added a lot of staff who are yet to contribute.

=Pharma

=Increased capacity utilization

3…PHARMA

A…USP

-IML

-QUALITY OF TUBES

-SINGLE PIECE CANISTERS

-NEW PRODUCT DEVELOPMENT

The point what Mold-Tek is trying to drive to pharma companies is our ability to develop new products faster than anybody else. Even the leaders in pharma packaging, we are in a position to meet or exceed them in terms of new product development.

B…I am confident about pharma growth because almost 8- 10 companies have already approved

C…But it will take time because pharma companies go through a lot of testing and stability tests

before they will take volumes.

D…As an opportunity, pharma is a huge

opportunity, close to Rs. 5,000 crores opportunity, including both exports and the Indian market.

So, even if we reach 1% to 2% of the market share, it will be close to Rs. 100 crores.

E…COMPETITION

=Unlike huge competition in paint,

when it comes to pharma, you can hardly count on fingers, notable players like FIJI, Gopaldas, Doctor Pack like that there may be another 3-4 players. So, these are all catering

to the current pharma companies. We too also enter into the fray with them.

=But our USP will be new product development and faster mold development. Because of our strengths in injection molding, our ability to produce at low cycle times will also make us can be an economical player.

So, with all these strengths, we are trying to focus on pharma business.

4…F and F

=Food and FMCG side unless our north client comes, we may not able to see more than 10% growth because as I said last quarter there is quite a bit of competition in the small product

segment in the south and in the north we are completely absent

=In north, we will start in january

5…PAINT SEGMENT

-Grasim@good growth

-Asian paints@degrowth due to pricing pressure, capacity constrain

=Once we have capacities by Q4 onwards, we can also be competitive

= In the paint and FMCG, most of the products are well established, especially come to paint pails,

those paint pails standards have become normal. They are like commoditized. So, there are at

least 20, 30, 40 suppliers or even 50 suppliers who are able to produce paint buckets to a

reasonable quality and reasonable consistency. So, obviously there is a severe price war and also

supply option

=Competition will be always there in all segments. Even today paint, we are now 40th, almost

35th or 36th year of production of paint pails. So, even today we have our own value and even

today 47% of our sales come from the paint segment. So, there is a growing demand for the pails

and quality pails especially with IML. So, having IML advantage, which is not possible for all

and sundry to start, we will certainly have our own niche market for our products going forward.

6…LUBRICANT

=stagnant market

=Not losing any share

7…MOATS

=Even in such competitive era, we have stable ebidta due to in-house manufacturing of labels, robots and economies of scale .That’s how

we are able to stabilize our EBITDA.

Disc…invested

Mold tek has given 3 times return in initial 2 yrs and negative return since last 3 yrs.

Really frustrating experience since last 3 yrs

I will wait for more 2 yrs for expectant growth from

1…Pharma

2…ABG

3…IML. increased capacity

4…Q packs

5…F and F@ north expansion

6…Around 280 cr capex completed in last 2 yrs

7…Ebitda improvement

7 Likes

I would like to know views of Value Pickr community about IML Printing machine shortage.

Is it the major constraint going forward as they seem to suggest that, they are unable to fulfill demand from Birla Opus from new facility due to this.

All the earlier assumptions of secular growth has not played well in the past 3 years.

I have invested in this stock due to their in-house Robotic capabilities during 2020 and then gradually increased the position with moderate conviction but have reduced my expectations from future growth. Due to saturation in Sales, PAT has been declining and there are no immediate triggers which are visible for Sales and PAT improvement.

1 Like

From all the points, it is clear that, future growth will come mainly from Pharma and FMCG.

Paints and FMCG may continue to face headwinds for next 1-2 quarters and once inflation settles down, things will become clear. I am not expecting any major increases in Salaries or Tax cuts which can increase urban demand hence will remain less optimistic going forward about these sectors.

If they can get New business from Pharma, then that will add lot of value in the longer term.

some back of the envelope calculations.

| in Cr. | ||

|---|---|---|

| Fixed Assets | 500 | |

| Sales | 1125 | 2.25X of Assets |

| Net Profit | 106.875 | 9.5% of Sales |

| Median PE | 5 Year | 10 Years | from beginning | |

|---|---|---|---|---|

| from screener | Median PE | 37 | 30 | 22 |

| Net Profit * PE | Mcap | 3954.375 | 3206.25 | 2351.25 |

| Mcap/#shares | Price / Share | 1187.50 | 962.84 | 706.08 |