@Raj7800 how did you assume 400 rs/kg? Did the management provide?

1 Like

yes, management had indicated on the concall

Feb 2024 concall(Mold tek packaging)

1 …Performance

=Q3 sales volumes are up by 14%. This is the first time this year that we could cross 10% – I mean,

double-digit volume growth.

=However, the EBITDA is up by only 5.23%

=Net profit due to increased depreciation and financial costs has come down by about 15%, because there’s almost 50% increase in the financial costs and 26% in depreciation due to the new machines being added in a big way.

===============================

2…Capex

=Current year, already INR105 crores of investments are made. And

in the remaining 2 months, we hope to reach our targeted investment of about INR120 crores in the financial year

A…Panipat plant

=Panipat is yet to start. They

have taken only trial samples and their lines are getting debugged. So I think on a middle of February or end of February, they have a formal inauguration of Panipat.

B…Cheyyar plant

= Cheyyar started already

in January. So we’ll be going along with them. So hopefully, in these 2 months, before March 31, both the plants will be up and running.

=And as I said, I can only comment upon the numbers and the capacity utilization only seeing few months of operations sometime in the month of June/July.

===============================

3…PAINT SEGMENT

=.Why flattish growth in paint segment

A…Asian paint@satara plant

=Last 4, 5 quarters, there is a drop in paint volumes due to Satara Plant, one of the major plans for Asian Paints was underutilized due to various maintenance and remodification work they have taken up there.

=And now it is back to normal,

B…Not chasing new paint players

I also mentioned in the last quarter that we are not chasing any more new Paint other than the new ABG, that is Aditya Birla Group, we are not going after the small and medium

players in this field because of the tight pricing norms they are following.

FUTURE GROWTH FROM PAINT SEG.

A…ABG(Aditya birla group)

=I am very glad now the commercial supplies to ABG have started in the middle of January and they are picking up pace in February, at least for Cheyyar plant for ABG, and indications are that in a month’s time probably supplies to Panipat Plant also will start.

=So by the time we close this financial year, there will be some numbers coming from ABG, and they will very strong improve the Paint numbers in the coming quarters, starting from Q1 of next financial year.

B…New products for asian paint

=And coming back to our major client, Asian Paints, they have given us the opportunity in 2 new product segments. I can’t reveal the details. And those 2, one of them started in

February, other one will start mid-March. So those 2 also will be contributing to reasonable

numbers to our growth in Paint segment.

C…Paint segment growth

=.So going forward, we’ll be back to double-digit Paint sales growth, which was a major miss in the last 4 to 5 quarters.

===============================

5…PHARMA

=.Pharma Packaging, we are coming out with small USPs in all the segments.

A)…For effervescent tubes,

=we are the first company to establish IML, in-mold labelling.

=There is a company which is not so successful in developing the IML solution.

= But our samples and our first lots of trial samples, what we supply to clients are well accepted. So our effervescent tubes would come not only in HTL, but also in IML for the first time in the country.

=And we definitely see a great advantage there because in Pharma, label quality and clarity

and its stickiness to the container is very important.

= In IML, we’ll be giving that as permanent skin like kind of decoration. So definitely, there is a good interest from the Pharma companies

whom we have approached so far.

B) Canisters

= we have come out with a single-piece canister as against 2-piece canisters that are prevalent in the country

=We are going for larger etching, which is the latest in the canister manufacturing in the world, which would give us an USP against the labelled canisters.

=So in Q1, we might see some numbers coming in from those 2 segments also

C)Iodex

=Iodex project, which has been long delayed, is now starting. Their assembly lines have been corrected and recent trials are approved. They’re ready to go for commercial impression from March. So if not

much, at least from Q1 definitely, Iodex will also be adding numbers.

D…Pharma segment growth

=Overall capacity of the plant, if it turns at of full capacity, which may not happen in the year 1, would be in the tune of around INR50 crores per

annum in terms of revenue.

= So going forward, the numbers can only go up rapidly from INR20 crores, INR25 crores in the year 1, that is '24, '25.

=They should at least cross the entire capacity of INR50 crores to INR60 crores within 2, 3 years can be better.

=But I can only comment once we see the market response from sometime in June, July.

=Probably in the year, '24, '25 itself, you will see progressively pharma

contributing to the bottom line in a handsome manner.But it might take a full year to really reflect on a substantial basis.

===============================

6…FOOD AND FMCG

=The main lever for Food and FMCG going beyond the current team level is our plant at North, that’s Panipat, -which is starting in February for ABG -March for thin wall containers

- 6 products to be introduced in the month of March, April, and

-another 4 in June, July.

=So these 10 products would be having numbers in the year '24, '25 at least for 8 to 9 months

=Probably at least half or more than half would be produced in North, that’s in Panipat. So going forward, again, we’ll be going into 20s for growth in Food and FMCG

=Customers

-HUL would be more than 10% alone. Maybe Hatsun, that is an ice cream major in South, Arun

Ice Creams. They also must be around 10%. Cadbury’s could be somewhere around 7%, 8%.

That is M2K Lickables chocolates. That one is around 7% to 8%.

=In Food and FMCG, by expanding our presence in North and widening our

product range, every year, we’re adding 3,4 new products. This year also, no Exception. These

things will continue to give us a 20% volume growth at least for the next 2, 3 years and that will be at a much better EBITDA of close to INR80 per kg.

===============================

7…Q pack

=We are aiming around 40%.growth in Q packs

=We are finding very good growth in

Qpack sales, that is our Square Pack and adoption option by Gemini and Patanjali for their edible

oil has also now increased the attraction in that segment.

=In fact, we grew by more than 100% in that segment this year. And we expect to grow at least 30% to 40% even on this – increase the

number for the next financial year.

=Reasons for good growth in Qpack

A…One is the big brands are now adopting our pails

B…We could push out patent rights on the Qpack and could take up kind of suspension of activities by some of our competitors, who have completely copied our concept and model.

=So that is also going to help

us in a big way, especially with the organized sector companies who don’t want to play with patents and IP rights

C…One of the reasons is we have widened our product ranges.

Currently, we have 2, 5, 10, 15

and 17-liter Square Packs.

D…Adoption by cashews and fertilizer and nutrients, which started a year ago, are really picking up pace. And they find this pack very useful and

very attractive also in the marketplace.

=So these are the reasons why there is a spurt in growth in Qpack sales.

Let’s see how it goes because now Gemini Oil, which is one of the

largest in South, in Hyderabad. They have adopted our 10-liter pack and they’ve also taken some

5-liter later packs. They are indicating interest in other packs also.

=Patanjali has started taking

for the last 2 months in decent volumes, but comparative to Gemini, it is much low. And we are

also having some Sunpure and other big brands inquiries for 10-liter pack

=Why Q pack has low ebidta

Qpack, though it is good growth driver, it is not a high contributor

towards EBITDA. It is similar to Paint segment or little better than that.

Less number of players adopt IML in that. Only edible oil, some of the nutrients and protein powder manufacturers, they go for IML. Majority of this cashew and other players go for plain containers.

So you all know that in IML, we have much better margins. Hence, Qpack growth will not contribute handsomely to the bottom line in terms of per kg. In terms of capacity utilization and

in terms of profitability, is still good, but not as good as Food and FMCG

===============================

8…EBIDTA

=Currently, this year, we might end up at around 37 kg only. But for the Q1 onwards, we will see a definite improvement in the EBITDA per kg also.

We have rough guess is like this

A…Paint, Lubes and Qpacks

=They have in the region of INR30 per kg to INR35 per kg.

=In case of some of the paint

companies, it is less than even INR30 per kg.

=Paints would improve because we have a good understanding with ABG and Asian Paints

where we are concentrating for our growth in the next financial year, where our EBITDAs are

protected definitely or even improved.

B…Food and fmcg

=In the case of Food and FMCG, it is in the range of INR80 per kg.

C…Pharma

=And going forward, in our pharma, we are aiming at INR120 per kg to

INR150 per kg

=Having said that, my main growth in EBITDA per kg would be coming from pharma in the next couple of years.

===============================

9…Future revenue growth and ebidta

A…EBIDTA

=EBITDA percentage wise, we are almost there, 18.91% is EBITDA

margin. Probably, we will attempt to cross the 20 percentile during '24, '25.

=If pharma goes as

per our plans, it should be in that region. Otherwise, it may take 1 more year, but we will be certainly there, is my guess in the 1 year or max 2 years. That is regarding EBITDA.

B…Revenue

=Raw material plays a vital role in our top line .- 18% to 20% drop in raw material price. It shows there is a 4% fall in the revenue. In fact, it is 6.6%

growth in the volume.

=We are aiming at, as I said in my previous commentary also, at least 15% or probably 20% volume growth for the next financial year.

= That is on the volume front, I can comment. How it will reflect on the revenue, it will depend upon the raw material price momentum.

A…Paint will continue to be a main growth factor next year because ABG growth will be considerable.

=And as I said, the Asian Paints

also given us a couple of opportunities which would take the Paint growth into double digit is my strong feeling for the next financial year.

B…Pharma Packaging, though it might not be a very big number next year, from the year 2 onwards, it will definitely be a considerable addition, at least 5% and above for the top line or

could be even a 7%, 8%.

C…Thin wall, that is Food and FMCG and Square pack, especially, will be shooting up at a pace

much better than Paint segment.

=So the numbers will be more favourable in Square Packs,

followed by Food and FMCG and then Paint. That is the order of growth percentage

=So it’s better to have Food and FMCG and Pharma growing. That will be adding better numbers to the bottom line. So that impact you will see in the next financial year partially, and from '25, '26, certainly in a significant manner.

===============================

10…Break down of 57,000 ton installed capacity by FY '24

=50% in Paint,

=Lubes maybe around 22%, 23%. And

=Food and FMCG should be in the region of 14%, 15%.

=Qpack also will be in the region of 15%,

===============================

11…Fungability

=The beauty of injection molding process is sometimes, let’s say, the paint industry does not grow

as per our anticipation, we can use the same molds and – sorry, same machines and robots also

for the Qpacks.

=Similarly, some of the smaller machines of the pail manufacturing can also be used for Food and FMCG.

= So that fungibility is there across the capacities. So there is no worry

that let’s say, if I aimed at 20% growth in Food and FMCG, but there’s a growth of 30%, we can

still handle it.

===============================

12…New clients

=In this quarter, we added Patanjali, SciTech Specialties, Swagath Hotels, Daspalla Hotels, SN Traders, Vijaykant Dairy & Food

===============================

13…Promoter holding

=Any long distance promoters are selling for their personal needs, but there’s no change in promoter

holding as far as I know.

Disc…invested since 3-4 yrs and added more recently

16 Likes

Nice Analysis. I am also holding in my portfolio, just curious about your opinion, of its going down the 40 month EMA? Its a crucial support…I am lil worried

3 Likes

I dont have any knowledge about technical analysis. I just hold on stocks until fundaments are severely impacted.

I dont sell for minor hiccups. I think mold tek has stagnant growth since 3 yrs. That meight be reason for this stock price.However ,i see this as opportunity to add.

As per book 100 baggers, we have to differentiate company’s SHORT TERM EARNING FLUCTUATIONS from LONG TERM EARNING POWER.

I meight be wrong about analysis of stock .As i want to stay invested in stock for 5-10 yrs or more, i always diversify in 15-20 stocks

I know, few stocks will not perform well in future, but 2-3 stocks out of 10 may give multibagger return.

When stock will rise?

Which stock (from my portfolio) will rise?

-I dont know.

So i just hold them and buy whenever they are in consolidation phase or their stock price falls.

9 Likes

I also dont know too much technical analysis and for long term investors , chart patterns and other intricacies are not much helpful. But what chart is made up of is, Price and volume action and it shows what other buyers and market players are doing with your stock. If their buying and selling is affecting the price of your stock and through that your wealth, then you need to give attention to it. So what part of technical is useful to us as investors ( and not traders) is…to see if our stock is in uptrend (as per stage analysis…in stage 2) , or downtrend (Stage 4) or in sideways that means neither moving up , neither down…

Why this is important …because of opportunity cost of your capital…As you dont want your promoter of Mold-Tek Packaging to mis-allocate capital into such avenues where return on capital is less, similarly you also dont want your own capital to get mis-allocated into such companies at such stages where they are not earning anything.

Few Examples

- Mold-Tek Packaging is a great company with great fundamentals but its price on January 2022 was 830 and after more than 2 years in march 2024, its at 796…During these 2 years, its between and around this price. 2 Years is a long period of time, where you could have invested your capital into some equally good and fundamentally strong company and price may have taken your capital into 60-70% up, considering the roaring bull market during these 2 years.

- Same is the case with equally superior Bajaj Finance with price at 7800 in october 2021 till today at 6910 , more than 2 and half years , price at that level…big opportunity loss for our small capital

- same is the case with SRF, PI industries , Divis labs, Tata Elxsi…all of these are A-grade blue chip companies but price has not moved over last 2 years and its a great mis-allocation of capital on our part in remaining invested in them during their down trend. We are not married to them or neither we have any personal interest in these promoters. Our sole goal is to enhance our capital at a decent rate of return , probably better than index. These are just instruments for us to increase our capital. They are not End point, they are just intermediaries to fulfill our financial goals, not goal in themselves…What say?

14 Likes

Rightly said, though as a small individual investor - I find it difficult. After investing 100s of hours going through concalls, presentations, reports, etc and continuous tracking, bias is hard to get rid of. Maybe for the likes of us, as far as we know that there is nothing significantly wrong with the company’s management or business per se, it is okay to stick to it? I am new at this even after 3+ years but hopeful of learning from the more efficient investors. The likes of Divis, Bajaj Finance and HDFC are going through difficult times, and untill I gather enough confidence or energy (part time investor with limited bandwidth so track less than 20 companies at a time) to invest in something better I find comfort sticking with them.

2 Likes

How can we know that perticular stock(e.g. mold tek pack, bajaj finance etc) will not go up in next two yrs? These examples are retrospective studies.

By the way, i try to follow 100 bagger book. As per book, one should not sell stock because it is not going anywhere. Rather one should add that stock during this consolidation phase.

One point from that book is as follow

"DONT GET BORED

=People often do dumb things with their portfolio just because they’re bored. They feel they have to do something

=Why do people buy and sell stocks so frequently? Why can’t they just buy a stock and hold it for at least a couple of years? (Most don’t.) Why

can’t people follow the more time-tested ways to wealth?

BECAUSE PEOPLE GET BORED

=People get bored holding the same stock for a long time—especially if it doesn’t do much.

…They see other shiny stocks zipping by them, and they can’t stand it. So they chase whatever is moving and get into trouble.

=Wanger used to say, investors tend to like to “buy more lobsters as the price goes up.” Weird, since you

probably don’t exhibit this behavior elsewhere. You usually look for a deal when it comes to gasoline or washing machines or cars. And you don’t sell your house or golf clubs or sneakers because someone offers less than what you paid

=Usually the market pays what you might call an entertainment tax, a premium, for stocks with an

exciting story.

=So boring stocks(stock going no where) sell at a discount. Buy enough of them"

6 Likes

Offcourse, bajaj finance or mold-tek may go up in next 2 years, but when they do so, we will be watching them and we can re-enter when we see them rising. Selling stocks doesnt mean totally abandon them, never to touch them again in life. Crux of the point is investing capital in those stocks who are in growing stage instead of investing in those who are not moving or going down. And I fully subscribe to hold for long period. If a stock is rising for next 3 years straight, without going into consolidation or downtrend, then definitely hold that stock for 3-5 years. Why interrupt the compounding? See Trent, from last 4 years in uptrend…u can hold it for last 4 years and you can keep holding for next 4 years too, if it doesnt go in downtrend…see APL apollo, you could have easily hold it during last 4 years, see varun beverages, u could have hold in last 4 years…KEI, Polycab same story…All these companies are fundamentally good as well as in uptrend. I have read 100 baggers and even Pulak prasad…I am all for long term holding, but those stocks which are increasing my capital, not those good companies whose price is going down or not moving… I dont want to become purely fundamental investor or purely technical investor…I wish to become fundamentally opportunistic investor.

7 Likes

Familiarity Bias is difficult to get over with. We tend to develop unfounded liking and affection towards company, its products and promoters when we study the company. Thats natural. For that very reason, you should have one eye on the price chart also, while studying fundamentals. I love Astral and use its products wherever possible and recommend too. In recent investors interaction, I remember , promoter saying that stay with Astral for next 10 years and then see the results. I was emotional about the company and couldnt sell it even though it was slipping below 40 week EMA, but somehow I managed to overcome the emotional bias and sold it recently. May be I can go wrong. But I know that company well, I can anytime buy it when it comes in stage 2.

Most important is, I am totally against trading frequently, but I want to invest in fundamentally good companies who are also good on charts, thats it. This is just another and very crucial dimension to check while entering or exiting in the company, just like we check ROCE, Promoter holding, Debt levels, Just check where the stock is headed. This will make us nimble-footed.

Also , always remember, as retail, we are the last people who gets the information on fundamentals. Before us, promoters know it, analysts know it, Fund managers know it, speculators know it, …We always get the information last and most times just to fool us. So these guys who have got the information early, take steps of buying and selling and that is reflected on chart. There is no other way of knowing any fundamental info earlier than these guys , than following what happens with the chart. Thats why it becomes important. Always remember what Warren Buffet says…When dumb money acknowledges its limitations, it ceases to be dumb

6 Likes

Thanks Mudit and Pragnesh for an illuminating discussion,

I have a slightly different point of view. At the end of the day individual stock CAGR is an useless metric for an investor as any PF will have lets say a median retail investor will have lets say 10-20 shares in the PF.

All that matters is PF CAGR. To expect that all shares will be at high points throught is impossible. What is the probability that the share you have swapped into will continue to go up and will not stagnate or drop below.

4 years of a mega bull run has conditioned us into thinking we can time a stock.

Hindsight is golden. The Future is uncertain.

This is my extremely limited non expert and maybe dumb 2-cent view.

6 Likes

Its probably difficult for individual investor to check both fundamental and technical analysis all time and divert the money based on the direction. Also we always don’t get correct interpretation from chart, so that mistake also can be costly. At the end of the day, it really depends on the individual to decide what they want.

1 Like

100 baggers is perhaps the worst book to follow. It is like saying 10 people jumped from a ledge and landed successfully so it is something that has good success. It doesn’t talk about potentially 1000 people who failed the jump. You cannot make learnings about success stories without looking into counter examples where the companies who did the same thing still failed. In that the case the trait might be harmless or worse.

3 Likes

The debate we are having is time in the market vs timing the market. I personally do not have the confidence to time the market.

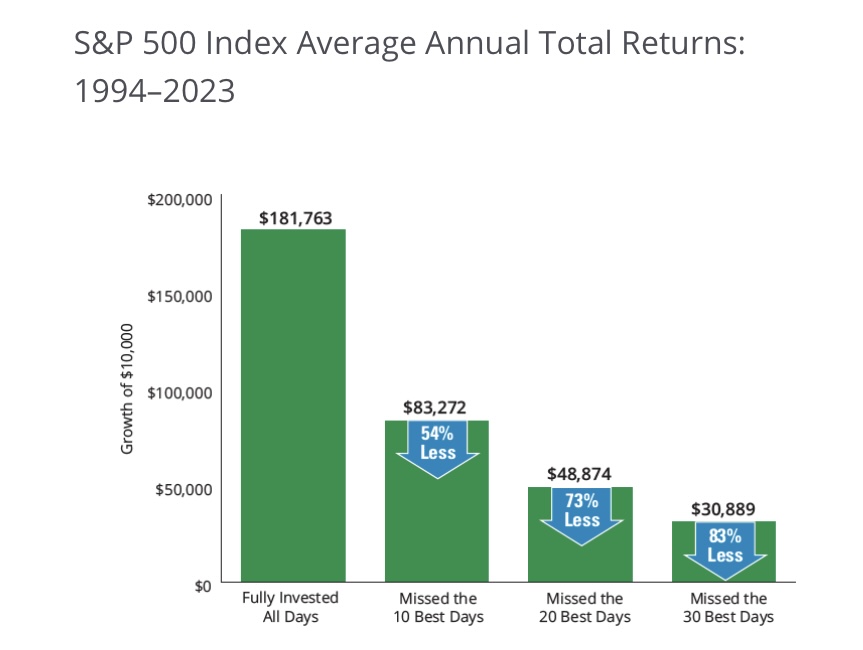

Missing just a few good days can have massive detrimental effects to long term returns. When stocks move they move very aggressively and we have seem the same with Mold Tek in the past, when gains have come they come super fast. Stock went from 200 to 1000 in less than 2 years time frame, during that journey there were weeks when stock price has doubled. Yes it is in consolidation now but fundamentals are quietly strengthening. Institutional investors have many advantages over retail investors. They have private meetings with promoters, they have access to industry reports worth 1000s of dollars etc. The only advantage we have is our ability to stay invested during hard times as we dont have the pressure to show gains to clients every month or quarter. We have to hold on dearly to that advantage if we wish to outperform.

8 Likes

While I agree with holding on, but if such an analysis is shared then the reverse of this which is avoiding the 10 worst days should also be shared. That gives a balanced perspective. ![]()

1 Like

The balanced approach will be to identify a universe of around 50 companies, whose business model is robust and sustainable with moat, from fundamental point of view and enter and exist in such companies based on technicals and stage analysis. This will ensure that you are always in your comfort zone companies and also in growth companies out of that selected 50. What say?

3 Likes

The company reported numbers. If I compare the full year FY24 and FY23 one thing to note is that company has maintained EBITDA levels despite revenue reducing as well as customer mix changing. This would likely imply that incremental business taken in other segments have been relatively margin accretive. The capex is behind them now and With Grasim ramping up paints maybe this a good time to enter this name? open to hear the communities thoughts.

7 Likes

Interview by the MD - positive on the pharma sector and guiding 15% volume growth for FY25

2 Likes

When all the packaging sector stocks like Uflex, Cosmo Films and Polyplex doing so well; why is there no momentum with MoldTek Packaging. Understand its in a bit different segment of products but its surprising to see no momentum.

The other shares either have huge debts or huge no of pledged shares (Uflex and Polyplex) which tells me its not safe for holding; wonder why the MoldTek while really good valuations, is still stagnant at CMP levels… any idea/inputs (starting to lose patience in this ![]() )

)

1 Like

The reason is that the spreads of polypropylene and BOPP are improving leading the above players to make better margins in the coming quarters however mold tek packaging is not in a similar business as other players

3 Likes