Hi all,

Look to these Snippets from the company con call, The Company is taking the competition seriously and clearly sharing why they have subdued growth and all. At the end of the end transparency of management and taking every small competition seriously help in the long term to protect market share and all.

I’m not sure if people stopped eating ice creams in summer or ice cream makers are not using mold tek products? Is this one summer phenomenon? Anyone tracking this for long time can comment?

Hi, yess this only for this summer because of two reasons 1st uneven rainy season, 2nd the consequence of first one which leads to huge drop in sales of ice cream. So this temporary and will have to track on next year rainy season.

Agreed completely.

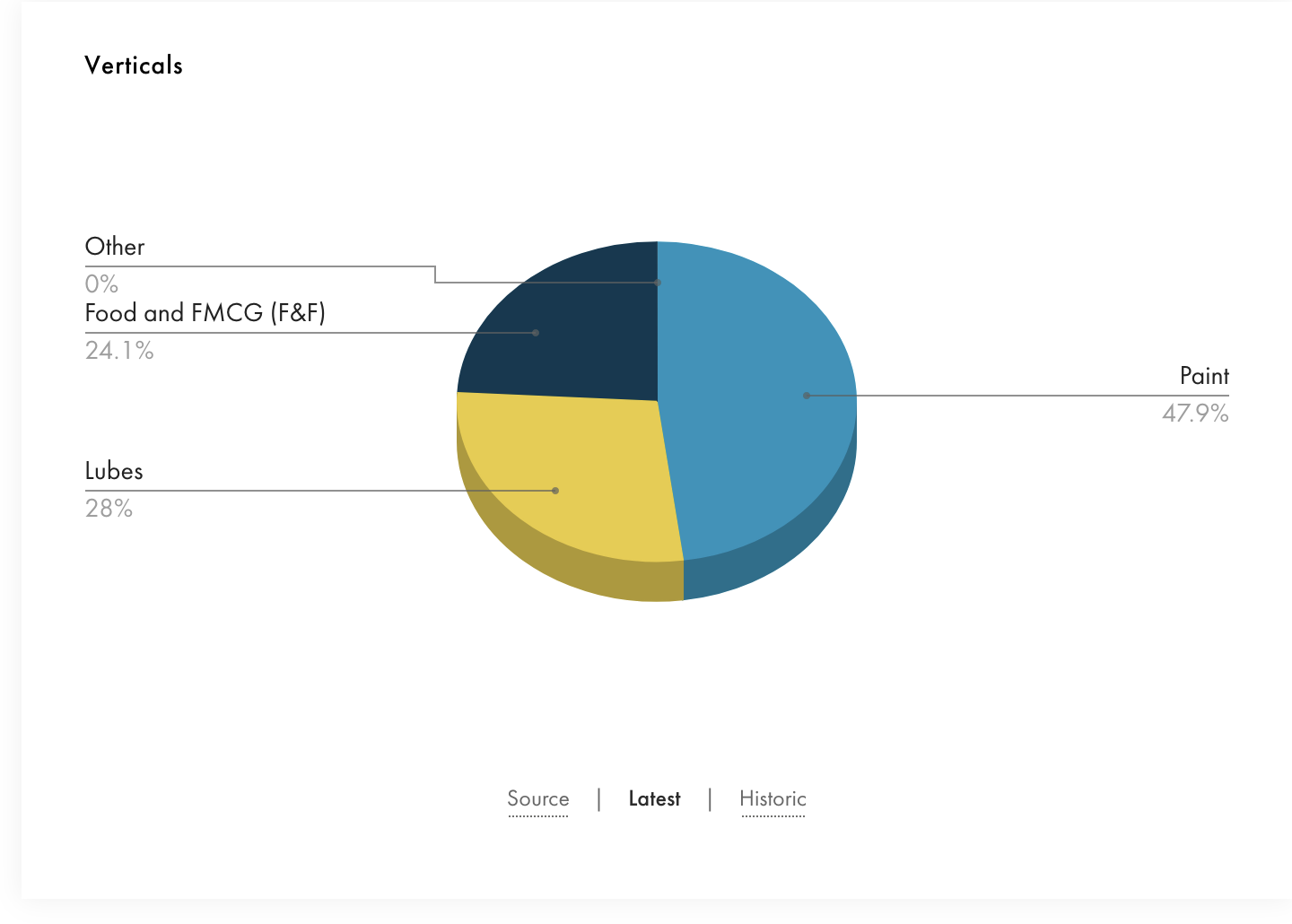

Moldtek is not present in entry level Paints segment.

Abnormal Rains is a major reason wrt ice cream sales specially

Moldtek suffered the most coz of these factors.

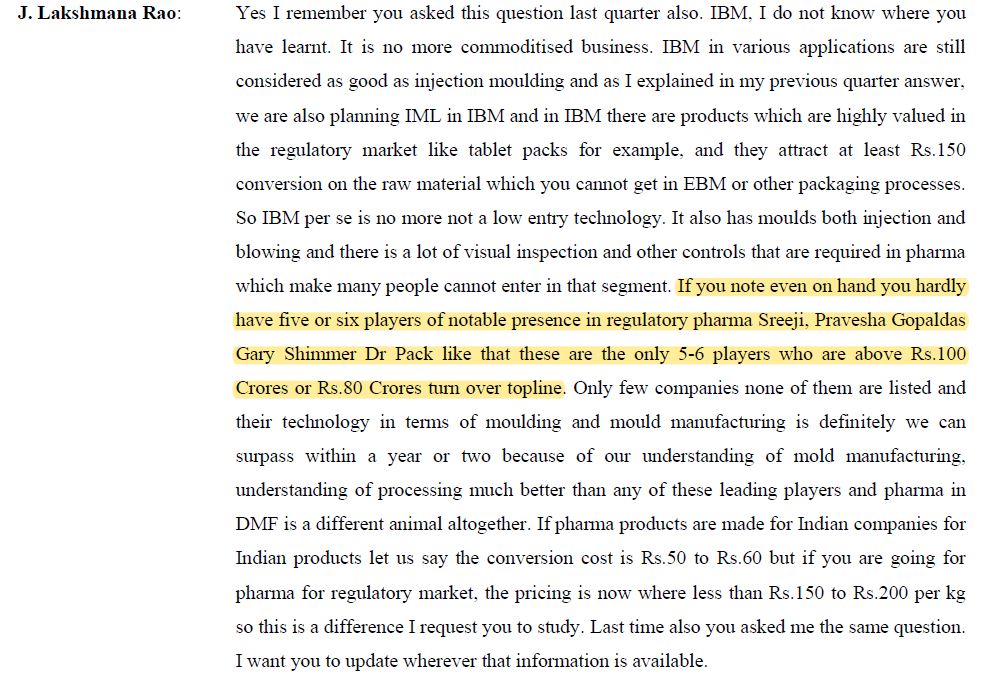

Pharma segment is where IBM can be good - Lets see

Festive season - they make Sweet box too - Something to check is fmcg segment

Yes, you are absolutely right about the festive season - I saw many small to mid-sweet shop shift to IML boxes and sooner or later Moldtek will be their first choice as they get confidence in IML boxes.

If things start falling into place as the management has guided then we are slated to see a period of high growth for the company.

Paints division to be benefited from the high competition among the paint companies as volumes will increase materially for the industry

Food and FMCG is witnessing increasing demand trend towards IBM & IML and will continue to see increasing growth

With the pharma plant coming up ebitda/kg should see a upwards blip with ebitda/kg for pharma materially higher than paints business

Even on conservative estimates I see upwards of 25-30% growth for the company for next few years

This news has relevance because it can be a good quasi play on the paints industry. If Asian Paints doesn’t perform, Grasim might (or maybe both will do well). Serving multiple players and new deep-pocketed entrants in the space, bodes well for Mold-Tek.

The business still continues to be driven by Paints sector. Nifty FMCG has done really well in the past 1.5 year. But Moldtek Profits as well as market cap have moved sideways. I wouldn’t call it a FMCG play, we might find better direct opportunities there.

Certainly bullish on Pharma packaging business though, given 1st stage of production started from December onwards.

1500 tons of capacity for pharma - assuming realisations of 400/kg - 60 crs at peak capacity utilisation - so roughly 1.5x as total investment is 45 crs, but i think subsequent brownfield capex would be at significantly lower cost so future capex asset turn should be 2-2.5x

Who are the listed competitors for Mold-tek?. Trying to find how the market share is divided… Does Mold-tek have leading market share in any segment?

Tried to find competitors

uflex,Polyplex - More on Films?

TCPL - Cartons

EPL - more on fmcg

rajshreepolypack; ArrowGreen – Seem too small

Hitech Corporation - Seems to be the one with similar areas and size.

Can you share your thoughts on whom I should look for similar size and whether any market share information is available.

Unable to read the names clearly. Can you share who are the competitors you have listed under paints and lubs?

Also any other competitors you know of for the other segments - Pharma etc?

According to their Q1 & Q2 FY24 Concalls, their competitors to pharma packaging are Sreeji, Pravesha Gopaldas and DrPak. I have been tracking the company concalls for the last two quarters and I couldn’t find their competitors in the paints & lubes segments.

Mitsu chemplast in Pails, National plastics in containers, and many more in various segments. However, MoldTek is innovative and offers superior quality to its customers.