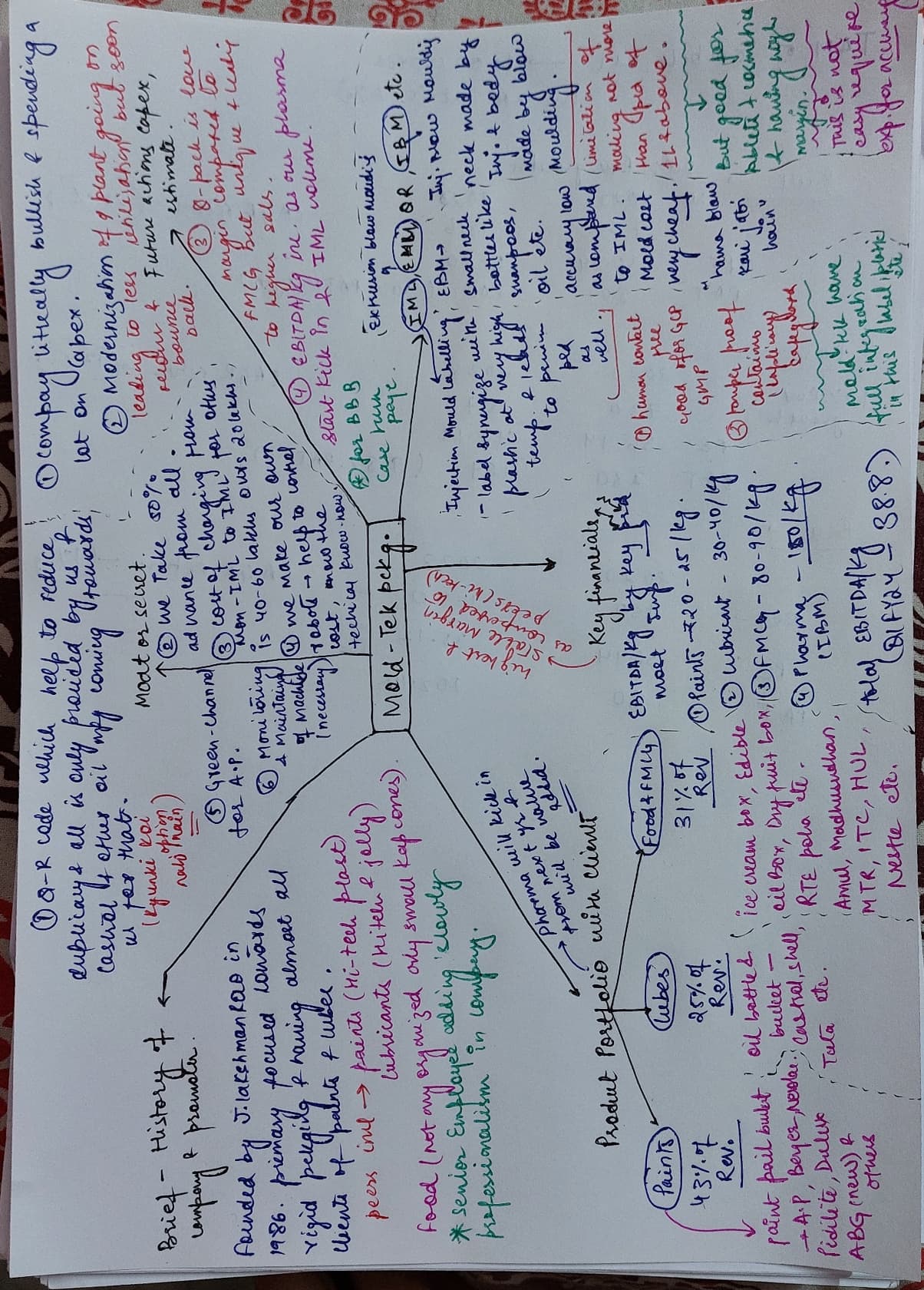

Friends, I want to bring your attention to few interesting facts about Mold-tek packaging

It seems to breach all the major DMAs in last few days

The stock has seen a 100% increase in its price and 83% expansion in its PE.

FII holding in the stock has gone up from 8.3% to 12% during this time

DII holding has also gone up from 14.3% to 16.8%

Public holding has come down from 42.3% to 37% (as expected in most scenarios)

In Q1’ 22 they saw 55% Vols growth and 80% PAT growth

Most of the demand growth is from Food and FMCG as expected however lubricant demand growth (especially for Diesel & CNG engines) was a surprise, per the management

To fulfil demands of Western India customers, they are setting up another plant in Daman, since they mention that their current Daman plant is almost fully utilized

This was the first ever quarter in which they achieved production of 9000MT in single quarter

Gulf, Valvoline and Shell seem to be the 3 new major customer acquisitions from lube segment

They are exploring an opportunity for Wipro in Malaysia.

If the IBM project goes as discussed, they expect a major upside on volumes and profitability

No surprise - it has caught the frenzy of institutional investors - I hope retail investors catch it fast too.

@hitesh2710 bhai, are you watching this stock yet or no longer?

In terms of QoQ, volumes were up by 3% from Q3 22. In terms of revenue, there was a decline of 3.4% and EBITDA declined by 9.2%. PAT decreased by 2.12% QoQ. Revenues were 154.83 cr and PAT was16.83 cr

Since paint pails make up 50% of the turnover, lower paint sales along with new Capex and new project implementation suppressed the margins. Despite 3% increase in volumes, there was 2.12% drop in profits

Capex of 129 cr has been planned for next 12 months out of which 79 crores is already spent. These include new Pharma plant in Sultanpur, brownfield expansion in Daman and Greenfield expansion for panipat and Cheyyur plant

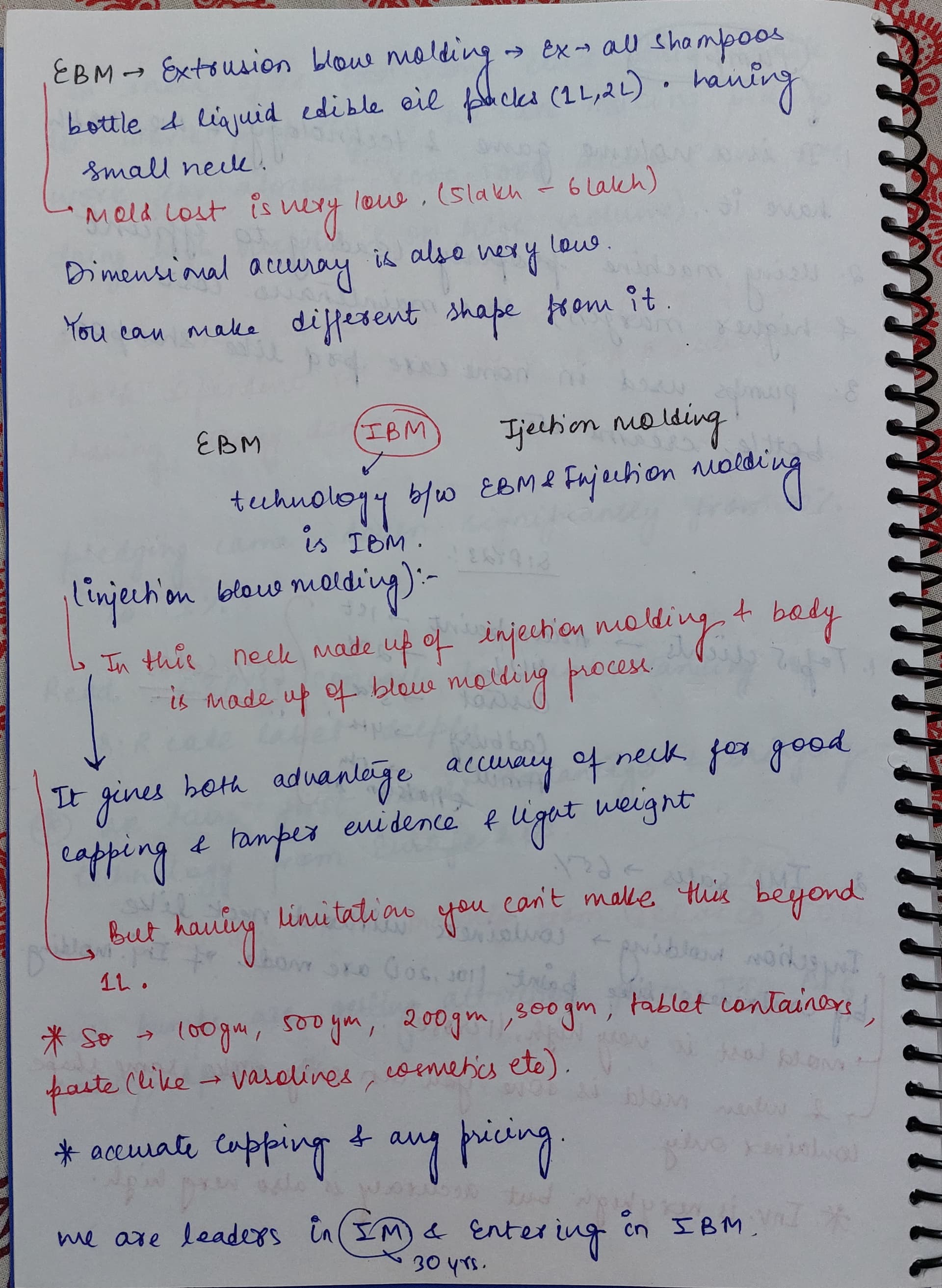

Company is focussed on majorly three initiatives: Injection blow moulding, flexibility in terms of taking low MOQ orders and export potential

Out of the total revenue, 72 crores came from paints, 40 crores from lubes and 43 crores from food and fmcg. Total capacity utilisation stands at 74%

As per the concall, maintenance costs have shot up because semiconductor shortages in the automated machines like printing lines and to some extent robotics and their non-availability has led to loss in productivity and sales actually

Another reason for the decline in performance were power costs and transportation costs due to increase in diesel prices. Power costs comprises of 7% of cost structure. It had been increased by 12%-15%, thus having the impact of 1% overall on EBITDA

Regarding the dispenser pumps, the company took the Capex of 13 cr for manufacturing 25 lac pumps per month keeping in mind the demand from WIPRO. However the utilization is at 4 lacs a month

Most of the dispenser pumps Capex is fungible which means the same gets utilised for food and FMCG sectors. Hence the company is trying to recover the costs from these sectors

For IML initiative, both valvoline and castrol had come up with the design of QR codes on both jars and caps. At least one of these proposal would get closed by end of this quarter which would give a first POC for the much touted IML

Regarding the upcoming capacity at Panipat, it would majorly cater to Grasim paints as well as food industry situated in Baddi. This would save on transportation costs for Baddi since Panipat is 250 km away from Baddi

One major point to come up in the concall was the Capex philosophy for moldtek. On probing by Harsh from Marcellus, the management confided that they are not just putting up the Panipat plant only for Grasim. Rather if Grasim does not work well, they would have a whole lot of food and FMCG to cater to in north.

Regarding the EBITDA level ramp up, the company would be focussing on in-house manufacturing and printing of entire labels rather than getting it procured from third parties. This will increase the supply dependancy and at the same time would be EBITDA accretive to the tune of 3 crores per annum

Regarding the increase in power costs, it takes 3 months to pass the increase of costs to the client in 80% cases. In the remaining 20% cases, the increase gets reflected in 6 months time.

Regarding IBM, most of the containers would be exported to Indian Pharma players for their export business. The competitive advantage stems from nearness to Pharma players in Hyderabad, deep packaging knowledge and limited competition

Yes. It is expensive at 42. But I am still comfortable as my average buying price is 700. But will surely follow how it performs in the future. Will sell if growth falls below 10% or gets overvalued more.

The valuation should not be considered based on PE only. At PE level. it is slightly higher side from mean. However look at the EV/EBITDA and Price/Cashflow as well. Per the recent con-call * The Pharma division will start commercial production in Q2, with some products contributing to revenues in the current financial year. Though I personally see the more revenue coming only by end of FY24 from Pharma packaging .

Please prepare a financial modelling looking forward for 15-16% CAGR growth per the con-call and get the forward PE.

A solid entry and exit criteria has to be in place. Disc: I have personally invested. and could be biased…

I think the TTM PE was in the mid 30s even when the price was in the 600s-700s

What’s crucial here is that the margin currently is below potential because of commodity price fluctuations, spare capacity, and investments in developing new businesses.

Once you normalise for these things over the next couple of years with solid DD growth - they ‘could’ double profits in 3-4yrs. Key here is optimal capacity utilisation and higher margin pharma/FMCG.

But I think profits will stay below potential since they will continue to invest to increase longevity of growth - so stock will keep looking expensive.

Another point is that steady state free cash flow generation is better than profits reflect. A lot of capacity is relatively new, so depreciation isn’t reflective of maintenance capex.

I don’t think it represents very good value at today’s prices though. My cost is below 350 (and I have bought even in the 700s)

That said I am not selling - but if this small cap mania continues and this stock gets more attention I might be tempted to trim.

The discovery factor here has played out - so fundamentally any more multiple expansion will be over-valuation (maybe already is overdone)

DII and FII holding was around 9-12% each when I first bought. Now both own around 18%.

That was a good presentation brother. Thank you for your valuable time and effort.

I think for this kind of steady grower business major stock price correction won’t happen easily. Accumulating it slowly would be a much better option, rather than waiting for a major correction which may or may not happen in near future.

The FMCG segment experienced lower-than-expected growth, primarily due to reduced consumption of ice cream and dairy products caused by intermittent rains across the country.

As a result, there was a 20% decline in volume growth for ice cream and dairy products, leading to a moderate 13% growth instead of the expected 36-37% growth.

The operating capacity of the Khandala plant in Q1 FY24 was only 46%, lower than expected. However, from July onwards, the capacity has increased to 65-70% due to ongoing expansion and maintenance projects undertaken by major clients.

The decrease in profit can be attributed to the recent increase in depreciation over the past few months.

The future outlook appears very promising, primarily because of the upcoming introduction of Pharma packaging products, scheduled to be launched by December 2023.

The Pharma facility will start getting audited by the client from October 2023.

Iodex production is expected to commence by October 2023.

Revenue expectations from the Pharma segment cannot be disclosed at this time.

The QR coding issue has been resolved for Shell, and a further launch is underway for Shell.

EBITDA per Kg stands at 38.8, compared to 40.14 in Q1, for Ice cream and Dairy products.

In Q3, integrated printing facilities from Sultanpur are set to begin operations in October 2023, which is expected to improve the EBITDA.

The Pharma segment is expected to start contributing to EBITDA from November to December this year.

The Pharma Business is projected to achieve an EBITDA of 150 per Kg.

Next year, the Pharma Business is estimated to generate revenue of 30-40 Cr, with a worst-case scenario of 25 Cr.

Volume Growth reached 9200 tonnes, with volume contributions from Paints at 40%, Lube at 28%, and Food at 24.2%.

Grasim’s volume growth is expected to reach 5000 tonnes, and the total capacity for the paints industry is 19000 tonnes, including Grasim.

Since Mold-Tek Packaging is dependent on crude price variation which they source from reliance if I am right.

Do u guys think with boom in bio fuels is it going to help the company with respect to raw material dependency possibly improve their bottom-line margins

Or they are forever stuck to crude derivatives.

Please clarify if anyone has knowledge about it .

Can bio fuel replace their raw material in any way