No business is perfect we have to do few compromises with every business… low promotor holding and dilution of shares for growth is one compromise i have done for this business! Because i haven’t yet found integrity related issues with promotors .

The debt is working capital debt so won’t be there for long term their debtor days have increased hence the debt once it goes back to normalcy i don’t think they will continue with working capital loans…

Also dividends payout is one concern but I didn’t find anyone asking this to management so that we can get their rationale behind high dividend payout…

1 Like

I had contacted the company 2 quarters back and asked few doubts posting here the answers i got from the company…

- i recently heard in concall that, some of the big MNC players refused to deal with us because they aren’t finding other packaging companies which can do packaging for them so that those MNCs will reduce concentration risk. How you look at it? Have we lost them permanently as our customers?

A:

I think there is a misinterpretation here. Some companies are not upgrading to superior products (IML) because there is no second supplier. However they continue to take existing products (HTL, Screen printing) for all their brands from MOLDTEK. We have not lost any customer permanently because of this.

Where as many of our customers opt for superior product for some of their premium brands.

- how we control our product prices based on volatile Raw material prices? Do we pass on the raw material prices to customers or take a hit on our own margins? And if we pass on to customers, will we be able to do same irrespective of any price of raw material?

A:

Our pricing model is Cost+ ; hence any uptrend or downtrend is passed on to the customer based on the terms of our agreements. Yes, we have been able to pass on all the price increase to our customers in the last 6 months.

- historically company is consistently distributing dividends to shareholders but at the same time reducing stake to pay debt. so ultimately we are paying major part of free cashflow each year as dividend to shareholders and borrowing money for new capex? Don’t you think shareholders would be more happy to see debt free status instead of steady dividends each years?

A:

We have been a dividend paying company for many years and we would like to continue to be the same. Please note that majority of increase in Debt is working capital. Majority of Capital expenditure is funded by internal accruals. We aim to have the optimum level of debt.

- have we pitched our packaging solutions to the two biggest edible oil brands in India namely, Fortune and Saffola? And if yes what was their response? Because edible oil is big market and having two biggest brand in our list of customers is like a major boost to our long term growth.

A:

Yes, we are in discussions with major top players in Edible oil industry. Companies are showing interest for some of their brands. We cannot specifically talk about customers when discussions are happening.

15 Likes

Thanks for this Suyog.

I was just reading marcellus little champs newsletter they posted yesterday which has some recent developments on Mold tek also. Marcellus guys use two frameworks for determining the operational efficiency:

- Lethargy tests- to keep a check on moat.

- succession planning- does the company have institutional aspects or is it just a promoter driven company.

They have explained these points regarding Mold tek on Lethargy tests:

They will explain succession planning in next newsletter. But as to succession planning or institutionalization of the company I’ve less enthusiasm bcoz many managers are relatives of the promoter:

(Source: Annual report 2021 page 155)

I had a question, Is this Company Friends Packaging engaged in same business as mold tek?

9 Likes

The first plant in North India inaugurated. As far as I know, this is a leased facility, built in order to save time before setting up of plant in Sandila Industrial Area, UP.

Disc. - Invested

4 Likes

8 Likes

Management has missed the commentary expectation on Pumps completely. Earlier was doing 1.5 million and expectation was to increase to 3million, instead there is reduction and they are currently averaging 1million. With the new entry now into IBM and given previous failure in UAE is there a threat here of diworsification?

2 Likes

It is not diworsification.They are in same business line.

Failure is part of game. Not single management always wins.What i like is that they try new things and they are mostly first initiator for their products.

Some product succeeds and some may fail

5 Likes

I think this is due to sharp fall in sanitizer sales as mgt mentioned. They said they are focusing on shampoos and handwash which will be more sustainable.

2 Likes

A month since this post and I have exited the position recently, Following are the changes/reasons for exit:

- Unpledged promoter holding has decreased from 34% to 30.74% in Sept. quarter.

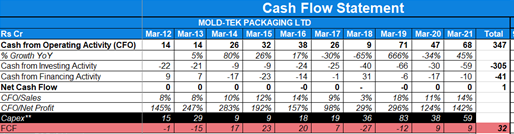

- Company has generated FCF of 32 crs and has paid out dividends of 92 crs from 2012 to 2021, which implies dividends for approx. 60crs are paid out either from debt/equity dilution.

Free cash flow:

Total Dividends

- Company today has announced to Raise 150 crores via raising equity. 4th instance of equity dilution in last decade.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/6852f6f4-59b5-4a39-b1bf-e4d43adea2e2.pdf

The operational efficiency is amazing in mold-tek but due to my own discomfort and parameters of low promoter holding which I have personally set, I’ve exited it.

I’ll appreciate the endeavor of mold-tek going forward but prefer to skip the ride.![]()

5 Likes

The equity raising is quite uncomfortable…

They have recently did rights issue for reducing debt and now this…

Red flags :

- Pledge holding (few shares though)

- Low holding

- Reduced holding multiple times

- Debt free ? Not yet

- Capex from raising equity+debt

- Dividends never reduced though

It would be helpful if others share their views on these red flags, @vivek_mashrani @neil991 @Raghav_Malhotra

4 Likes

On Point 2, you should be looking at “Operating Cash Flows” and not “Free Cash Flows”… FCF is net of what remains after paying dividends (which is part of Cash from Financing Activities component of Cash Flow statement)

1 Like

In their last concall mgt had clearly mentioned that they are seeing a very large business opportunity on the horizon and that if it comes through,they’ll have to quickly do some spending.They had also said that they’ll raise money in that case.This business opportunity will significantly improve their volume growth in FY23.Most likely the business opp has fructified.

3 Likes

(Free Cash Flow (FCF) Definition) ### Free Cash Flow

(FCF) is often defined as the net operating cash flow minus capital expenditures. Free cash flow is an important measurement since it shows how efficient a company is at generating cash. Investors use free cash flow to measure whether a company might have enough cash, after funding operations and capital expenditures, to pay investors through dividends and share buybacks.

From above it is clear that FCF does not include dividend. FCF is simply deduction of Operaing Cash Flow and Cash Flow from Investing Activities. Dividend comes after that and under ’ Net cash inflow (outflow) from financing activities’. So, ideally company is paying part of dividend through debt/ equity dilution. Please correct if wrong.

Disclosure: Invested

1 Like

This is incorrect.

Free cash flow is the remaining amount of cash from operations after Capex. You can read Dr. Vijay Malik blog on the same. Directly jump onto Hind zinc case in the blog it is similar to mold tek.

Right interpretation.

So they are going to do a QIP of 150cr

avg of CFO/PAT for the past 6yrs 140% and avg of cfo/ebitda is 68% for the past 6yrs, but FCF is not growing that’s a matter of concern, product diversification is there, may have threat from China, tracking not invested,any one put some light on cash flow

=Better marker is comparision of cummulative CFO with cummulative PAT of last 10 yrs

=As company is doing capex,fcf will be less or negative

=When company’s ROE is good ,than it is better to reinvest in capex rather than paying dividend

Disc…invested

7 Likes

double bottom most probably on the charts.

Qip is also annouced here. Some good investors entering here.

Product diversification is great. China is the joker in the pack when it comes to packaging and plastics. So that is something to watch

Ground-breaking ceremony for co’s. 11th plant tomorrow. First plant dedicated to IBM technology.

The pilot project is expected in April 2022. Numbers will add from next FY.

3 Likes