Great summary. About your last question. I thought the management mentioned it is not (no more) economical to import plastic containers from China for FMCG. Because it is too much cost as plastics are light weight and takes too much volume for unit weight of material transported. I am bullish on this company from a import substitution and uptake of good/fancy packaging as part of branding point of view.

Any reasons why you would think the company should do sizeable exports in future?

But the company has obtained licenses under Export Promotion Capital Goods Scheme (EPCG) and Merchandise Exports from India Scheme (MEIS) schemes which means it would be doing at least some exports in the future.

EPCG -

Under the EPCG scheme of the Central Government, a service provider or a manufacturer may import capital goods without payment of Customs duty, subject to the condition that such person fulfills an export obligation equivalent to 8 times of the duties, taxes, and cess saved on capital goods, which is to be fulfilled in 8 years from the date of issue of authorization. Capital goods include plant and machinery and/or accessories.

“The Company may avail and enjoy the benefits under this scheme by importing capital goods without payment of duty subject to fulfillment of export obligations.”

MEIS -

Introduced in the Foreign Trade Policy (FTP) for the period 2015-2020 and launched as an incentive scheme for the export of goods. The rewards are given by way of duty credit scrips to exporters. The MEIS is notified by the DGFT (Directorate General of Foreign Trade) and implemented by the Ministry of Commerce and Industry. Till 30th June 2020, the Company has received Rs.49.98 lakhs and as of 30th June, 2020 balance of Rs.8.60 lakhs is receivable.

Exporting of packaging containers usually wont make financial sense to the packaging company. First, cost is a biggest issue out there. Company’s profitability will get compromised. This is precisely why MoldTek had setup a plant in Dubai to sell packaging containers in those markets. That’s a different thing it didn’t take of for multiple reasons. Hence you willl amost always find packaging companies setting up plant close to the client factory. Second, customers, who usually are of larger size than packaging cos, can’t risk distruption of supply of containers at any cost. Hence they prefer packaging companies in close proximity to themselves. Third and last, to get export based customers, one need to invest in right kind of sales force. Getting customer on boarded is atleast year long process with lot of iterations. Travel cost, sales cost etc will eat up the margins.

Having said that, there is humungous opportunity in India itself. MoldTek does not need to step out to get the growth atleast for the forseeable future.

That’s my two cents. Been tracking MoldTek for last 5 years.

Attended the AGM FY21 today. Following are some points -

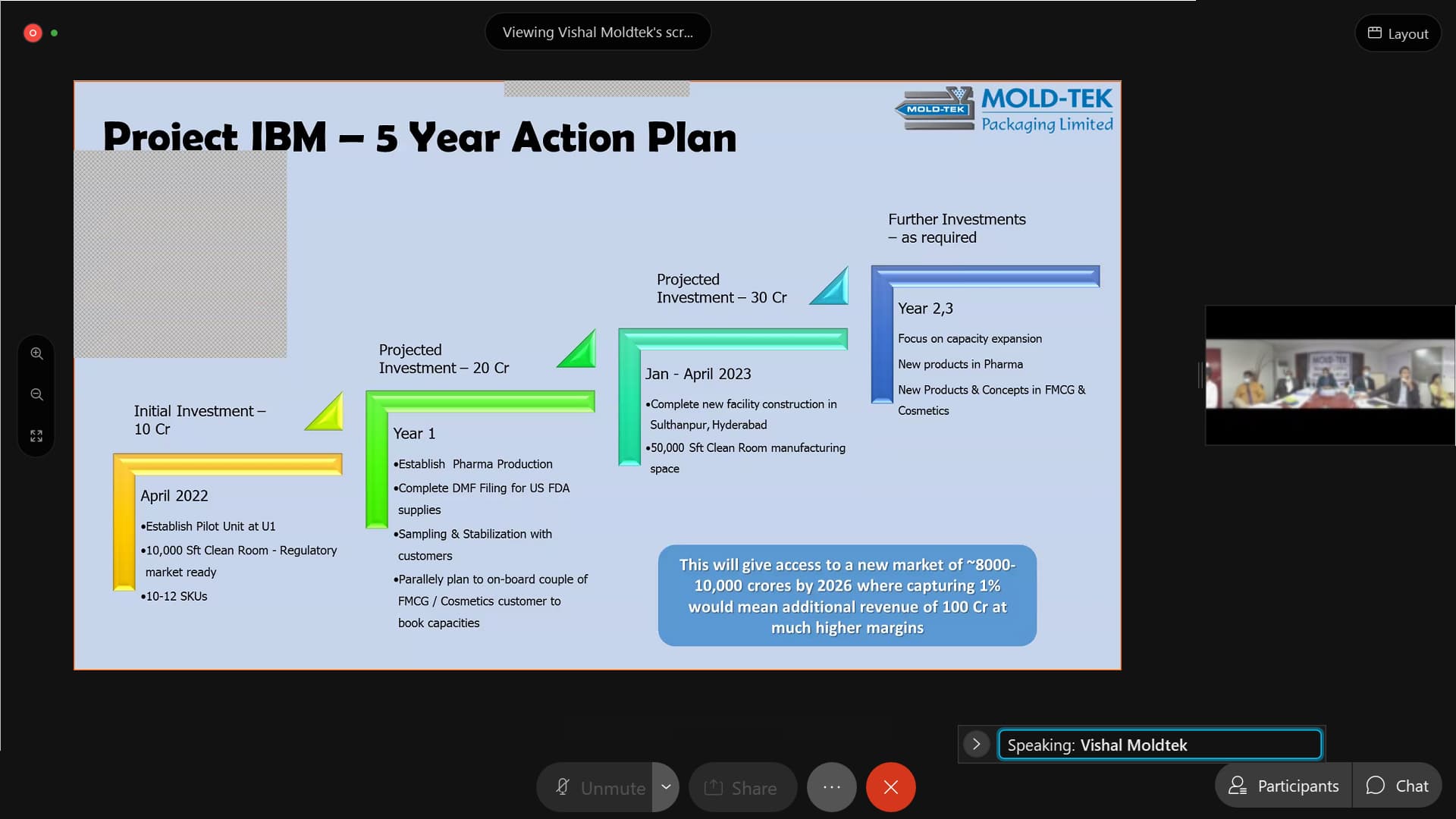

MTPL is expanding to Injection Blow Molding (IBM) technology. This will help them to get into the pharma, cosmetic sectors. Will have IML technology in IBM also.

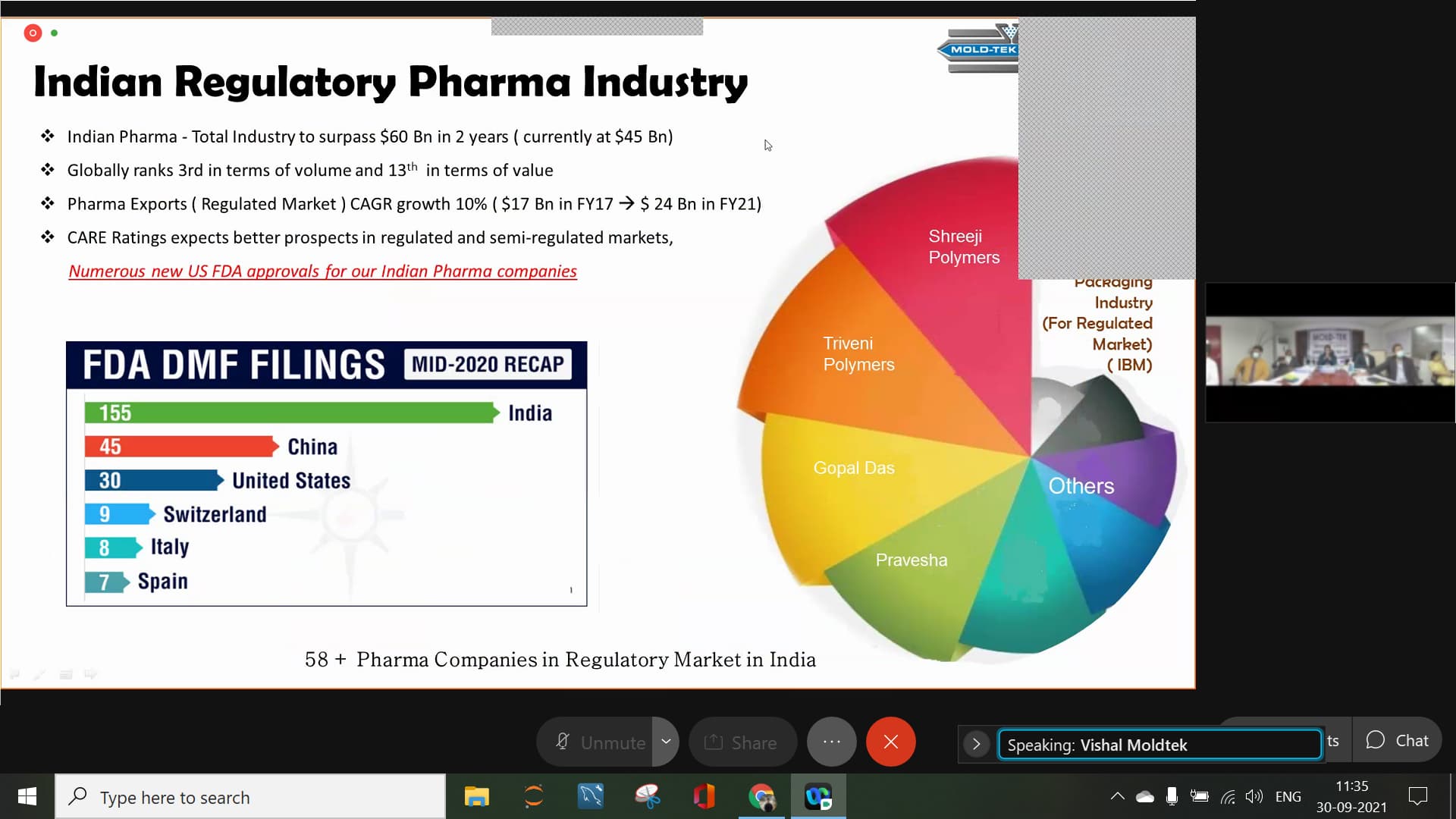

More than INR 5,000 crore opportunity in IBM packaging. Until now, the company was purely in injection molding only.

This tech. has a lot of applications in India. Will focus on 3 fields -

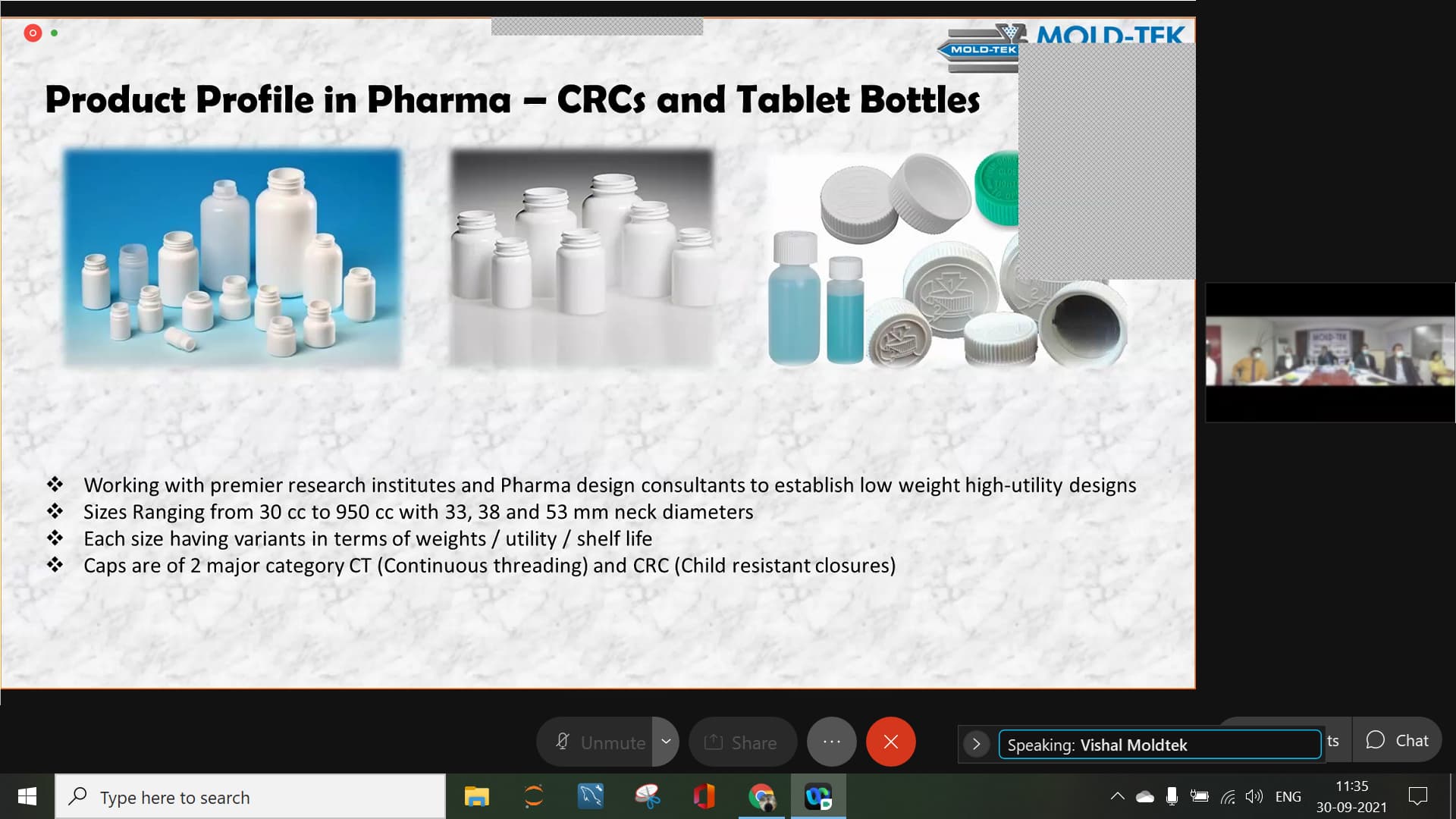

Regulated Pharmaceutical Market - Highest focus will be here (predominated by India pharma giants, they supply it to the US, European nations, etc.) These are tablet packs. Our strategy is to launch designs while working with design consultants in the pharma space. Major requirements in this field are - quality expectations and cleanroom standards are very high. Takes a long time to set up and getting filing and FDA approvals. Profitability is very high, higher than F&F also. Will take next 6 months to set up. Have finalized 10-12 designs to go ahead with.

2 bottle caps are there - CT and CRC (more interesting - completely injection molding - new technology, have a design in mind to go ahead with)

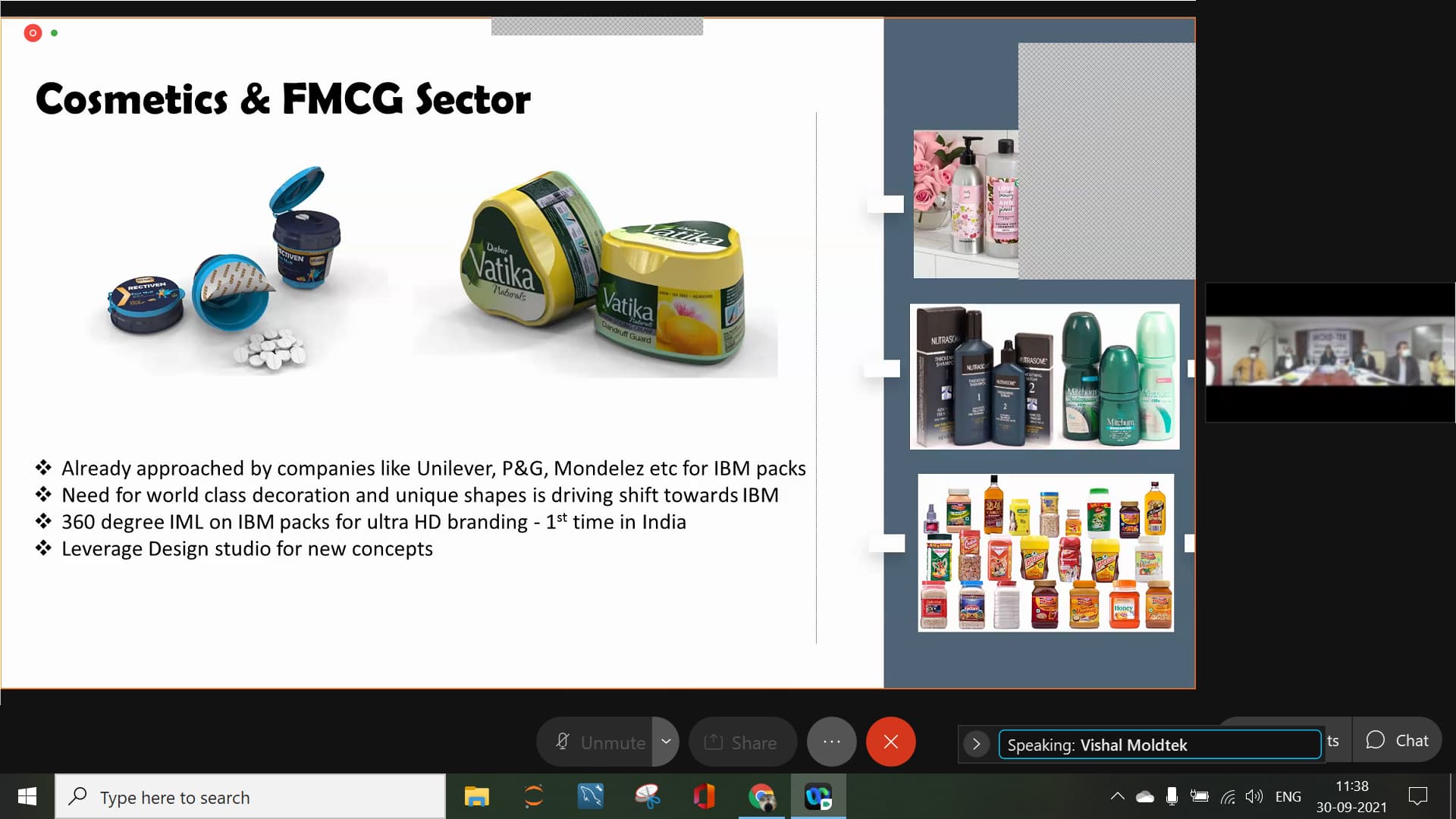

Cosmetics and FMCG - will be the first time in India to introduce IML+IBM for cosmetics and FMCG. Have already been approached by cos. like Unilever, Mondelez etc. for IBM + IML tech. High hygiene requirements, new innovations in products in this space

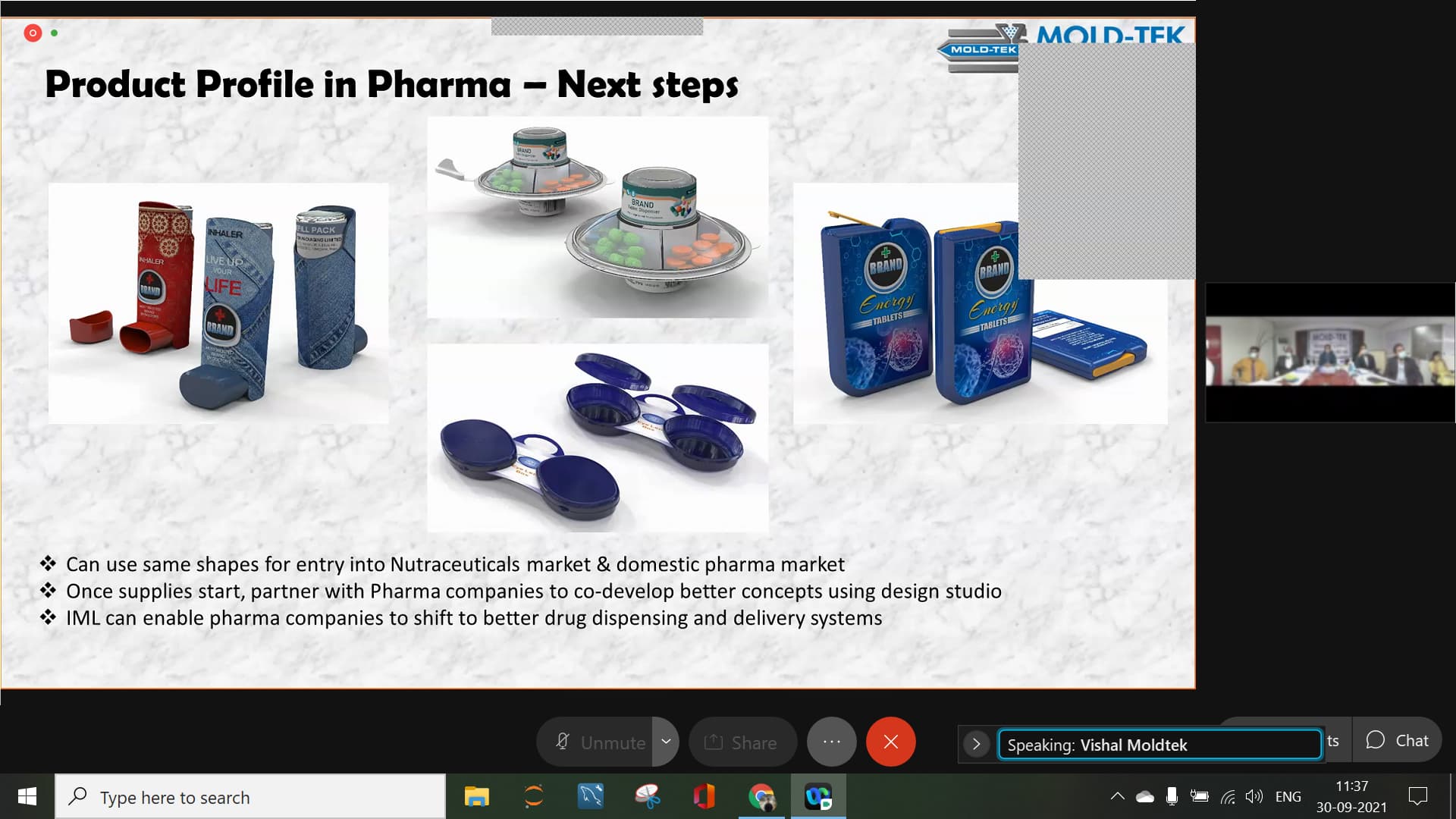

Domestic pharma and nutraceutical market - requires hygiene, innovative new concepts. Small market as of now (margins will not be very high, but will help to utilize plants established) Initially, we want to get comfortable with the pharma sector in 3-4 years and then will introduce various new designs for driving aesthetics and new designs

Edible oil cos. use tin cans in times of high RM prices or acute cost-cutting as they cost 90-100 Rs, whereas packs supplied by MTPL costs them around 125 Rs. so

We are in touch with Aditya Birla Group for supplying to their paints business (Grasim Industries)

Did not go well with JSW paints, their volumes are too low so do not fit our pricing model.

The Kanpur Nerolac plant will also focus on Neroclac’s plant in Amritsar. Unless their Amritsar plant has high enough volumes, we will not set up a separate plant there.

All our products are 100% recyclable. We will try to use recyclable plastics for non-edible packaging and focus more on sustainability in next coming years.

Co. will invest INR 200 crores in next 3 years

Target to reach INR 600 crores turnover in FY 22 (25% growth over FY21), targets to reach INR 1,000 crores turnover in next 3-4 years (entire Press release will be out soon)

All the growth factors + IBM/IML ensure co. has good growth for next 5-7 years.

All in all, positive and aggressive move by the company. Looking forward to how their plan plays out.

Well summarised! Do you have any sources/ videos to understand IBM in pharma and fmcg industry? Also how is the existing competition structure here in pharma/ cosmetic packaging

Any one has any insights on this please reply

I have been tracking Mold Tek Packaging for sometime now, I got a chance to enter last year during the price fall in March and further increased some stake through the purchase of RE and warrants. I will try to play the ‘devil’s advocate’ here and try to counter some of the views put forth by the management in terms of the rapid growth that they foresee over the next few years.

While the management is ‘hopeful’ of achieving 600cr in sales for FY22 and 1000cr in the next 3-4 years, ultimately their growth will depend on the success of the end user industries. Currently, the company caters to three industries, Paints, Lubricants and Food & FMCG, with Paints contributing > 50% of revenues. If there is a slowdown in any of the industries, it will reflect in their sales, as seen in 2017 when the Paints industry was in a slowdown.

While it is miles ahead of the competition due to its innovation, it becomes difficult for it to become the ‘main’ supplier to its clients, as its end clients do not wish to restrict themselves to a single supplier as part of their de-risking strategy. So it will grow steadily, but not rapidly. Besides in the F&F space, not too many of its end client products are essential daily use products.

While moving into IBL and entering the pharma space is a good sign and will give the company more sources of revenues, it will take time for it to penetrate the segment. Hence the sales growth will be a more steady 10-15% over the next few years.

I have been looking to understand how they plan to fund 200cr capex? Their cash on hand is 1 cr (What I see on screener.in). And CFO is around 60-70 cr. Any idea/info from management regarding the same?

This is one unique business whose most of the clients command strong pricing power! Paints companies pass on raw material prices to consumer hence moldtek can do the same too… similarly food fmcg commands pricing power too! With popular brands hence other than lubricants entire portfolio of moldtek is somewhat secure from end industry slowdown… also considering the tailwinds in real estate sector, paints industry will grow well over this decade, food and fmcg is the ever-growing sector too

Count in the outstanding ~53 Cr to be received from the Rights issue (courtesy ICRA report) and ~60 Cr CFO for the next 3 years -

ICRA notes the company’s decision to raise Rs 71.30 crore through rights issue was concluded on November 11, 2020. The company has raised Rs 17.83 crore (25% of the total rights issue amount) and the remaining Rs. 53.47 crore (75% of the total rights issue amount) will be raised consecutively through one or more subsequent call(s) as determined by the Rights Committee. The proceedings from the rights issue of Rs 52.83 crore will be used to reduce the working capital borrowings and the remaining Rs. 17.61 crore will be for general corporate purposes.

True. That’s the base case assumption. However earnings will grow at a much faster pace due to better product mix ( higher contribution from FMCG ,QR coded IML,sanitiser pumps). But I think all that information is already reflected in the price. I believe they ll keep getting in to new areas of growth like they have been and that is yet to be priced

I know it does not make a large difference, but wanted to understand if most of the resolutions discussed in AGM FY21 not getting 95-100% votes in favor means anything negative for the company’s board or its solidity with the shareholders?

Most of the lower votes seem to be for the resolutions around increasing management compensation, but that shouldn’t be an issue currently as the management compensation is within industry limits of around 0.15 times profit before tax and their compensation is increasing with increase in profits. The concern would be more if the management was increasing their compensation, but that wasn’t reflecting in the sales and profits.

Most of the for and against votes seem to have the same percentage for the public institutions, which might indicate that there was one or two main institutions which voted against the resolutions.

One thing that is noticeable is that its mainly the MD, J Lakshmana Rao who attends and speaks on most of the concalls. Probably as the rest of the management rarely appears in the public, that may be another reason for the lower votes in favor of increasing compensation.

If someone is tracking this company for 3-5 years now… you must have observed that the management gives guidance for next year or next three years or so … how many times you have seen that the management given guidance has came true?

Did the management walk the talk in past 3-5 years based on growth they talked about and growth they achieved?