their annual report says it is for us defense business. i am extremely bullish of silver and if silver appreciate it will add to revenue and pat by inventory valuation. all their business verticals are high quality and innovative. they are the market leader in their 3 electrical contact . New business like silver salt, powder (which they took 2 years to materialize) and this JV and all going to drive the growth.

1 Like

now schneider took the electrical and automation business from l&t and this will increase their export business as well.

Hi,

Quarterly results are out.And they seem to be bad.

fig in lakhs ->

Sales have increased from 4,760.33(30-06-2018) to 4 924.57(30-06-2019),but expenses have increased more which has lead to profit (before exceptional item) to 77.99 only compared to 343.22.

The below figure has lead to increase in expenditure ->

Changes in inventory of Finished goods, Work-in progress and stock in trade. has increased to +235.10 from -797.35.

Guys please explain me what the above figure actually explains.

Thanks,

Deb

actually they are doing the right thing. when price of silver was low they build up a lot of inventory as it shows in last year as -14cr. now the silver is going up and they start selling those with market price it seems. look at cost of material consumed which is actually low.

Hi Hitesh Sir,

Are you still following modison metals now?the recent quarterly results are not that good.

Please provide your valuable inputs.

Thanks,

Deb

LISTING OF EXISTING EQUITY SHARES OF THE COMPANY ON NATIONAL STOCK EXCHANGE (NSE) W.E.F May 03, 2021 UNDER SCRIP CODE MODISNME.

credit rating notes

The demand for switchgears in India is mainly driven by increasing population, fast-growing power distribution and

transmission network, new electrification initiatives and higher spends towards infrastructure by the government. These

initiatives have led to high demand of Switchgears. MML being the largest supplier of electrical contacts to Switchgear

manufacturers will benefit from such initiatives. Also, due to recent spread of Coronavirus in China (which is the biggest

competitor), the company has received higher domestic orders from existing customers recently and is further expected to

receive more such orders. With slowdown worldwide, the company has been able to manage its exports in fact in current year

company is expected to report higher exports.

Electrical contact manufacturing is a very niche industry having very high entry barrier. In India, there are very few companies

present, in which only MML focuses fully on manufacturing of electrical contacts.

3 Likes

borrowing reduced to 11crore, best ever quarterly revenue, qoq and yoy profits are high.

sign of capital cycle because of supply consolidation.

Modison metals looks extremely interesting.

Few pointers that I had in mind which seem interesting

- Low D/E, Reputed clients, Incoming Capex, Consistent dividend payouts 15 year+, Critical application product, niche industry, high entry barriers

Key concern:

- Related party transactions, Trade receivables

Kindly have a look and let me know what do you all think about this thread

1 Like

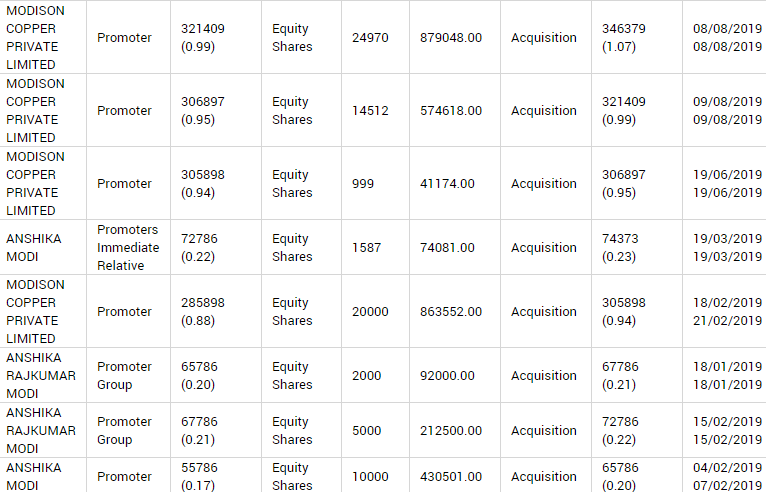

One of the promoters Suresh Chandra Mody has been selling in the open market since last few months. Also few individuals belonging to the Modi family have been categorized as non promoters but they hold significant quantities. One of them namely Vijay Kumar Modi has been selling and buying off late. Seems like trading not sure though. Can anyone please throw some light on the integrity of the promoter group ? Business and growth prospects look interesting.

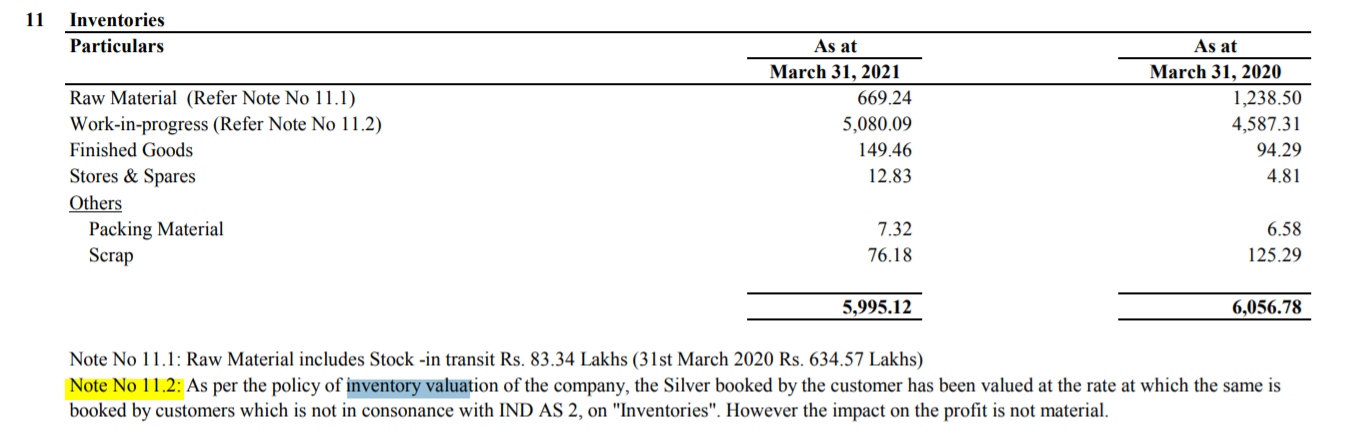

Note no 11.2: Inventory valuation has not been prepared in consonance with IND AS 2 for the last 5 years continuously, what does this mean and what can we make out of this?

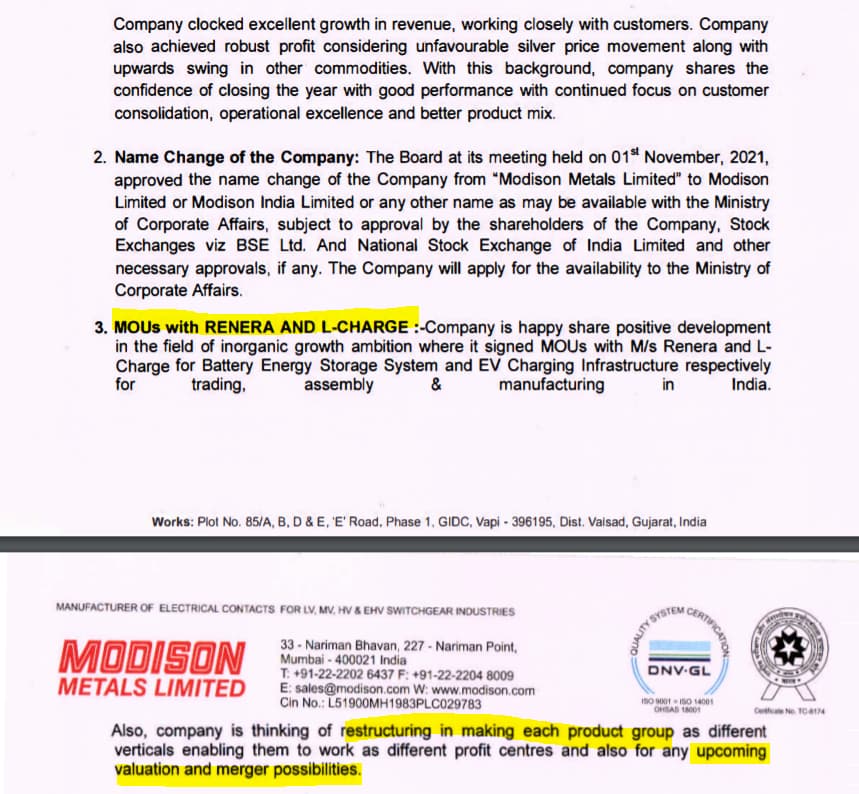

Q2FY22 Results out!

-Signed MOU with RENERA and LCHARGE to explore inorganic growth ambition in the field of battery energy and EV charging infrastructure

-Planning on restructuring each product group to help in upcoming valuation and merger possibilities

Decent Results

Waiting for Annual Results, difficulty to assess quarter by quarter without any concall/Interaction with management

3 Likes

AR22 notes:

- Losses on forex hedging: 3.54 cr. (vs 3.59 cr. in FY21)

- R&D spends: 80.49 lakhs capitalized, 55.3 lakhs recurring (total: 1.36 cr.)

- Employees: 257

- Increase in management salary: 10.78%

- Increase in other salary (except management): 8.39%

- Share price: 43.2 (low), 104.9 (high)

- Shareholders: 17’182

- Audit fees: 6.35 lakhs (vs 6.47 lakhs in FY21)

- Total tax disputes: 10.25 cr.

- Doubtful receivables: 1.4 cr. (vs 1.1 cr. in FY21)

- Purchased leasehold land worth 6.57 cr.

- Witnessing supplier consolidation from key clients thereby having higher wallet share

- Implemented a new Reward & Recognition scheme to create an environment of Performance Excellence

Related party transaction with Modison Copper:

- Purchase: 27.09 cr. (vs 19.55 cr. in FY21)

- Sale: 4.66 cr. (vs 1.63 cr. in FY21)

Engineering Goods sector constitutes >27%, accounting for largest share of India’s total exports. Growth in engineering goods exports in recent years has largely been due to the zero duty Export Promotion Capital Goods (EPCG) scheme

Company manufactures electrical contacts for switchgear (including Low, Medium, High and Extra High Voltage). Switchgear equipment is used in complex electrical substations to withstand fluctuating operating voltage in highly volatile environmental conditions. The development of new industrial structures, including powerplants for safe and reliable operations, is further estimated to stimulate the growth of the market.

The size of domestic switchgear industry was Rs183bn in FY18 and is growing at a steady pace of 9.3%. The low-voltage (LV) switchgear market (MCBs, DBs and RCCBs) derives demand from both residential and industrial sectors (unlike medium/high voltage segments which are used in industry and power utilities only). Retail sales (residential sector) constitutes more than 50% of the LV switchgear market. The electronics & electrical sector recovered by 27% to 14.9 Million ounces (Moz) (464 tons) last year and, importantly, surpassed 2019 levels.

Within the electrical segment, notable growth was seen in both the high voltage and low voltage (LV) switchgear markets. The former outpaced the latter due to higher demand from state utilities and Central Public Sector Undertakings (CPSUs), which related to expanding their sub-station network after a slowdown last year amid nationwide lockdowns. The easing of the pandemic also meant that LV switchgear installations benefited from rising demand from the real estate and manufacturing sectors

About company

It also produces goods for dominant sectors such as automotive, engineering, aerospace and railways.

Modison has the advantage of developing a wide range of silver contacts for diverse industries. Its plant is amongst the largest single site for High Voltage electrical contact manufacturing globally, thereby enjoying a low-cost advantage.

Capex plans

We have started our capex plan for upgradation of our existing facilities by infra expansion , both green and brown field, procuring automated machinery and robots etc. We also plan to build a new factory at our existing premises for increasing the HV segment assembly line. The said capex involves an outlay of Rs. 25 crores, which will be funded through a mix of internal accruals and debt.

The Board approved the Company’s business expansion plan in Battery Energy Storage System and EV charging Infrastructure. The Company has entered into an MoU with RENERA and LDrive (L-Charge), leaders in Battery Energy Storage System (BESS) and Electric Vehicle (EV) charging infrastructure segments respectively. These expansion plans are currently in feasibility stage

Salt, bullion & other segments:

We manufacture silver nitrate, silver sulphate, and silver oxide under this segment. These are high grade precious metal compounds with diverse applications in industries such as silver plating, pharmaceutical catalysts, mirror manufacture, inedible inks, explosives, fine chemicals, performance chemicals, and silver oxide batteries. We booked first export order for Salt from Indonesia.

We also have a consumer bullion segment where we manufacture and sell silver bars and coins. These are promoted through partnership with the Post Office as well as via leading online websites and distributor network. Our bullion and salt markets segment had a mixed year on account of the lockdowns and prevailing uncertainty

Disclosure: Not invested

5 Likes

Management had a recent investor interaction where they talked about their business and growth ambitions. It was a very good interaction.

Disclosure: Invested (position size here, no transactions in last-30 days)

5 Likes

Great to see you on call too. This was a fantastic call and glad to see the management taking interest in shareholder awareness. The greenfield and brownfield expansion is the next growth trigger. One key takeaway was the fact that the big companies with global standards as clients will take Modison to a global level. I have a question for management. What about the status of EV charging Infra that the company had announced a few quarters back.

2 Likes

Investor Meet (2022- 09 - 28)

-

Background

-

Start: 1965

-

make various components which are part of Power Sector (mainly switchgear industry).

-

tech-transfer tie up with DODUCO, Germany (pioneer in the name of components for switchgears)

-

this lasted between 1983-98 (~15yrs)

-

meanwhile devd. there own R&D

-

-

in the same group have another company: Modison Copper Pvt ltd.

- separate company deals with Cu and Cu alloys

-

-

Current Business:

-

LV & HV switchgear contacts

-

mostly Ag and Ag alloy contacts.

-

LV

-

several old series contacts + new series

-

Customers: L&T, Schneider, ABB, GE, Havells.

-

LV Segment: multi customer, multi supplier market (150 Bn USD market)

-

competition: Choksi heraues, Modicon, Hindustan platinum

-

mostly based on domestic demand (mkt share: 16-17% > Choksi > HP)

-

less value add

-

expect higher growth (>15%)

-

attributed to power sector growth

-

RE and urbanisation growth

-

infra boom

-

-

-

-

-

-

HV segment of switchgears + contacts for HV equipment (mainly Cu and Cu tungsten alloy)

-

air-insulated switchgear segment

-

gas-insulated SWG segment

-

Customers: Hitachi, Toshiba, GE, Siemens

-

main player in India (~80% market share or USD 15million)

-

customers changing foot print eg ABB/Hitachi now moved prodn from Sweden to India and Vietnam.

-

-

-

Financials

-

last year: 350cr. revenue

-

LV: 240cr (Choksi did 206cr.) (lower margin business)

- EBIDTA fluctuates as 80-90% cost is of pure Ag

-

HV: 100 (higher margin bsuiness)

-

Last 4 years: 16% CAGR growth (primarily volume growth)

-

-

-

Operations:

-

lean six sigma use

-

BF + GF expansion (total: 25cr.)

-

to make factories future ready

-

globally compliant

-

LV factory almost ready; plan to finish by Nov

-

HV factory plan to finish by end of this FY

-

-

-

Projections

- 500cr revenue by 2025; 1000cr by 2030

(Discl: no investments)

7 Likes

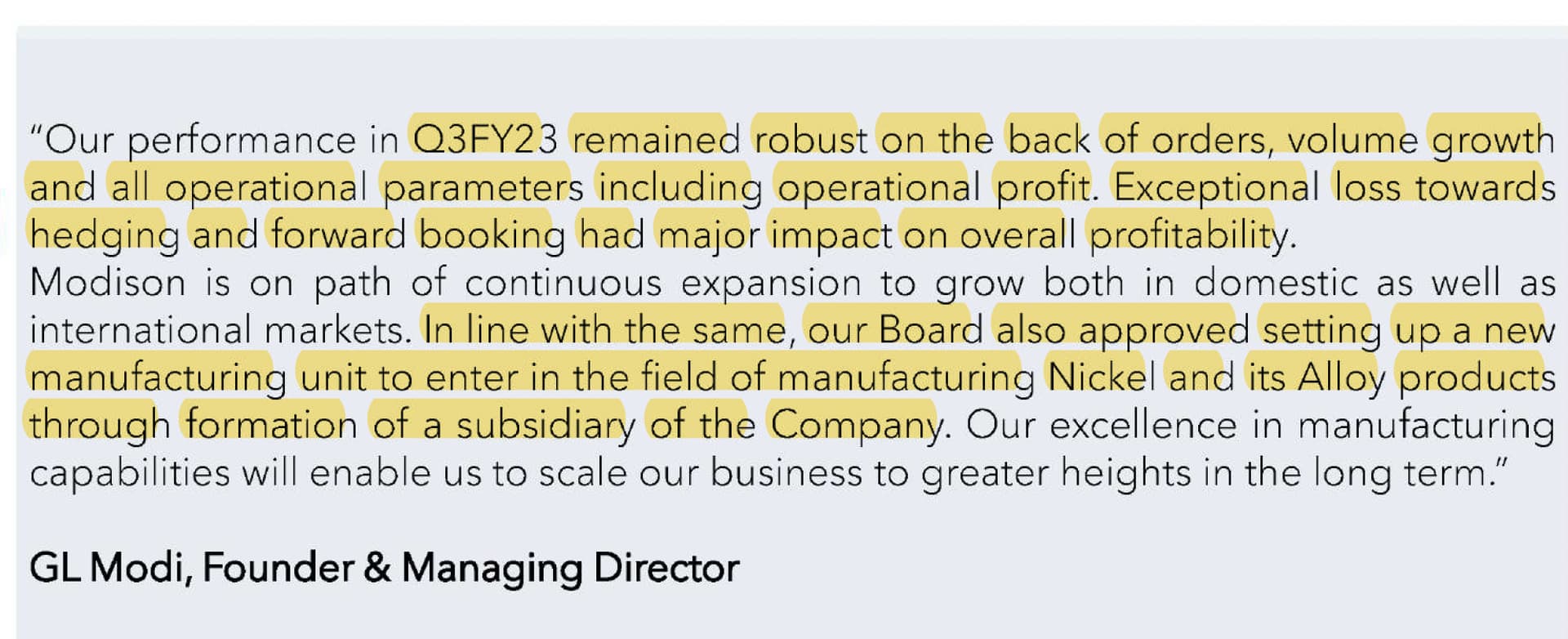

Very interesting announcement from the company, they are setting up a nickel & alloy plant which is a very high margin business.

Disclosure: Invested (position size here, no transactions in last-30 days)

4 Likes