Hi @arjunbadola , The company has a loss making Tannery division as well as white label export business which has been volatile and has been laggard from last three years which is hurting overall margins of the company, on the other side, the domestic footwear & apparel business have been growing significantly under the franchise model.(Just like Bata,Metro), hence a separate entity listing would give its due valuations.

8 Likes

Today in Neil Bahal’s newsletter, he was discussing about this demerger opportunity. Thanks for the explanation.

3 Likes

Neil has written this, quote,

"3- Mirza International: Demerger of RedTape shoes.

Mirza is currently a mix of many things. Very confusing.

They have recently announced plans to demerge their footwear brand RedTape along with associate businesses.

Due to the complex structure, the conglomerate trades at low valuation. But I find it hard to believe that a standalone ‘Shoe’ business can trade near 1x revenue.

Metro Shoes IPO could set some valuation benchmarking for RedTape.

Risks:

It is early. Demerger has just been announced and it could take a long time to fructify.

Details are yet awaited.

Conclusion: The important take away here is the power of Special Situations as they emerge.

Since announcing demerger and good results around Nov 9th, Mirza is +33% while the Nifty is -4.7%.

Luck?, I think NOT.

That is it from me today folks.

Lot of amazing Tech data points and Special Situations to discuss with you in coming time.

By the way, Portugal has made it illegal for your boss to send you texts after work hours.

Who’s coming with me? ;)

My best,

Neil Bahal

Founder & CEO

Negen Capital PMS"

Unquote.

Mirza is currently trading at 1300 crores market cap.

Demerged entity " Red Tape" has around 650 crores sales. Relaxo & Bata is trading at around 10 times sales. Khadim, Lehar is trading at less than 1 times sales.

At what valuation Redtape will trade?

9 Likes

d245c77e-1a98-422f-81b6-56178bf0a0b6.pdf (2.6 MB)

Demerger scheme

5 Likes

Got a chance to visit one of the newly opened store in Bengalore. When I enquired about the model, the owner said that its company owned and franchise run. Shop is running out of inventory due to some issues in the supply chain. He said we are better compared to other stores but still they have space for 50% and the inventory issues seems to be present across all the stores in Bengaluru (I am not sure though). I could able to find the shoes I was looking for in Nykaa fashions and the price was same in online/offlline.

Disc: Invested

5 Likes

One of the biggest concerns with Mirza has been (and possibly remains) corporate governance. Otherwise, there is no logic due to which a domestic branded retail segment play with 17%-20% EBITDA margin 20-30% annual growth should trade at such valuations.

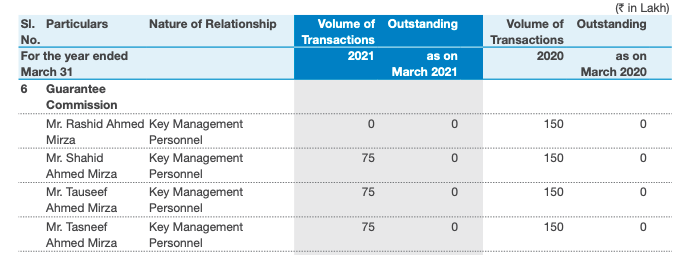

- The guarantee commission has been coming down. It was around 8.2cr in FY16. It is now around 2.25cr in FY21. It was around 6cr in FY20. Drastic reduction in latest FY. If there were a concall today, this would be the first Q i would ask, that does the management commit to reducing the guarantee commission monotonically over time & taking it to 0 in the medium term?

- The UK subsidiary which is owned by promoters & got around 70cr of biz in FY21 will get merged into Mirza international so that huge RPT will go away.

- The domestic business which has grown from 225cr brand in FY17 to 700cr brand in FY20 & 21 is getting demerged into a separate entity which should unlock value for all shareholders.

- It is quite remarkable that the domestic sales were flat between FY20 & FY21 for Mirza domestic. Metro shoes which just had an IPO had significant degrowth in FY21 & still managed to get valuation of 13x sales or 75+ P/E

I think it is time for investors to sit up, take notice, study hard & deep dive into Mirza. The highest amount of value is generated in change and the winds of change seem to be be a tailwind for Mirza.

Some of the other concerns which remain are around weak balance sheet position with 200+ WC days. (Although position has improved since 2018).

Disc: small tracking position, studying.

26 Likes

Bang on, that`s been my investment thesis.

Little incorrect to compare with Metro and other shoe companies because Bata gets around 8% from accessories and Metro gets around 10% whereas Mirza aka Redtape business has a significant contribution from apparel and accessories so it should ideally get better valuations than a shoe company

Also, Metro is at the uppermost end of the spectrum with crazy valuations along with Bata, Relaxo, etc and then we have Liberty, Khadim, etc at the other end with extremely low valuations due to poor margins, growth, ROC, etc. Mirza falls somewhere in the middle and should get re-rate post demerger.

5 Likes

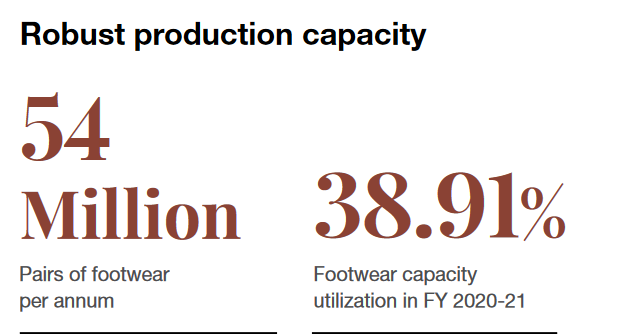

Am I missing something or some mix-up by company. As per Mirza AR 2020-21, production capacity is 54 million!!!

Whreas, till last year they were reporting somewhat close to 6.5 Million pairs capacity. (with ~75% utilized capacity)

What is it that I am missing?

9 Likes

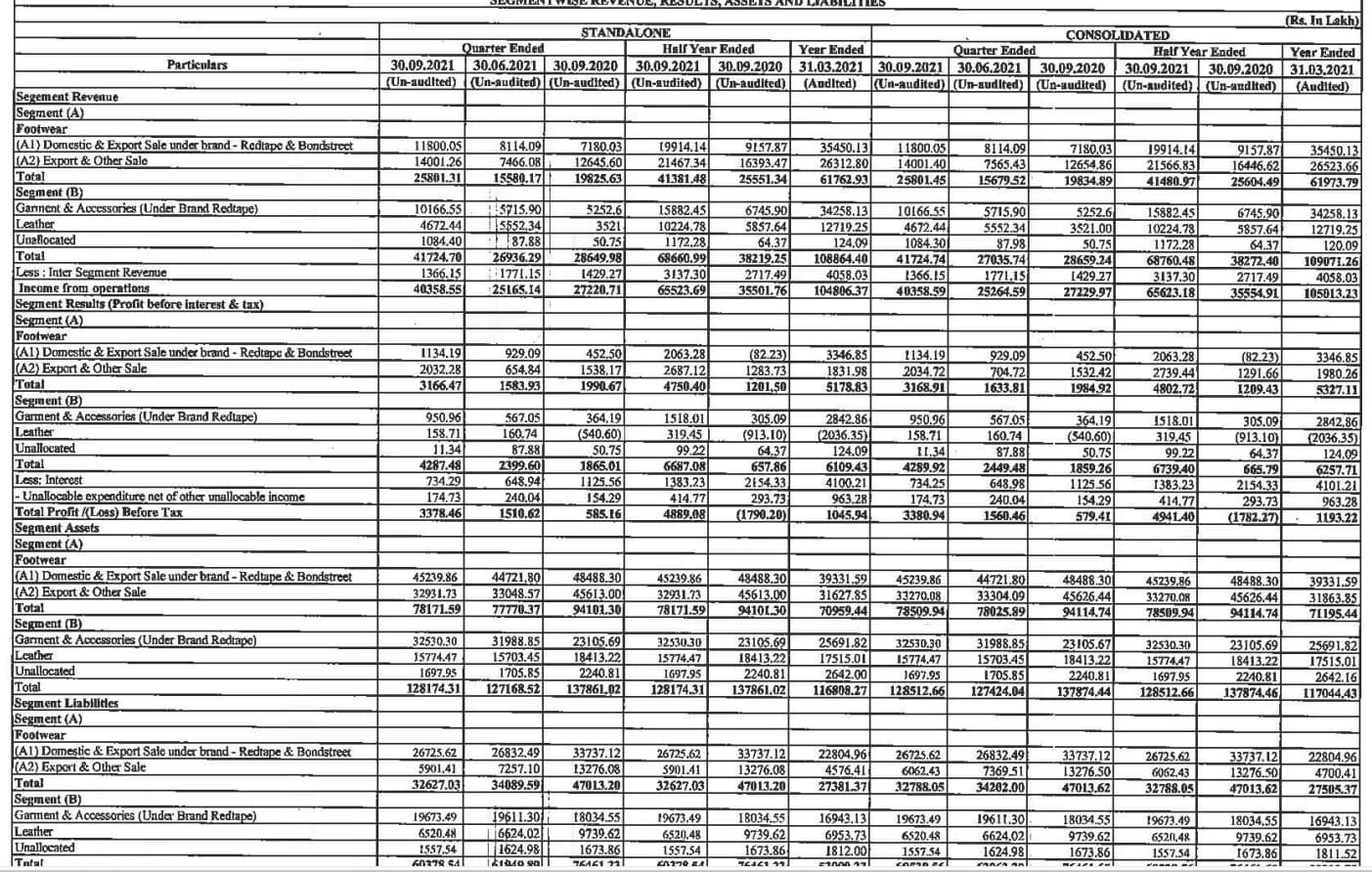

Let’s analyze the segmental return ratios for Mirza international Domestic business.

This is from Q2 mirza results.

- Domestic shoes division: Segmental (consolidated) assets are 452.39 cr. Segmental liabilities are 267.25 cr. This means that segmental capital deployed is 185.14 cr (Assets - Liabilities). This segment’s quarter EBIT (Proflt before lnterest & tax) is 11.34 cr. Since last few Qs were covid disrupted I will annualize Q2 EBIT to get annual EBIT. One can generate better estimates. Annual EBIT is 45.36 cr. Thus, the segmental ROCE is 24.5%. Not bad at all.

- Redtape Garments division: Segmental (consolidated) assets are 325.5 cr. Liabilities are 196.73 cr. This means that Segmental Capital deployed is (325.5-196.73) = 128.77 cr. This segment’s Q2 EBIT is 9.51 cr. This leads to annual EBIT estimate of 38 cr. This leads to Segmental ROCE of 29.5%.

- Domestic Business together: Capital Deployed = 128.77+ 185.14 = 313.91 cr. EBIT = 38+45.36 = 83.36. Thus, domestic business ROCE is 26.55%.

Also note that domestic business is flat between FY20 & FY21 while number of stores has gone to 276 in FY21 end from 222 stores FY20 end. This significant operating leverage is yet to play out. I believe that ROCE can cross 30% in 1-2 years sans Covid wave 3.

Disc: I have a tracking position.

24 Likes

Some scuttlebutt.

Ordered their sweatshirt, socks, shoes, ladies (mode) shoes.

The sweatshirt is good quality. Comfortable. The shoes are comfortable. Light weight the socks are comfortable too.

The ladies shoes are comfortable too, and my wife likes it.

All in all, the shoes are quite good and it’s hard for me to tell difference from a more expensive one. I might actually switch to Indian brands going forward and not wear foreign brands purely from saving money pov. The sneakers are about half the price of similar ones from puma.

PS: i am wearing my socks very high over my pyjama (which is not redtape) so that they are visible in the photo.

On another scuttlebutt a contact owns redtape store one of the earliest in North India (Ludhiana). They were telling that there is definitely some change in strategy. They are trying to focus more on standard operating procedures. How to behave with customers, ensuring consistent customer experience, how to paint something at the store etc. Will ask for more feedback as soon as possible.

24 Likes

I also did some scuttlebutt, found sneakers and trousers comfortable and at par with expensive brands

3 Likes

If it’s worth anything, I bought Red Tape shoes for my entire family and wore a pair too during my wedding last year. Needless to say, everyone loves it. My Dad used to be a banker and financed many leather goods stores in Chandni Chowk area in Delhi in the 90s. He tells me that all those businesses swore by the quality of Mirza’s products. Quality has never been a problem with Mirza. Their business strategy over the years is another matter.

17 Likes

I never knew RedTape was a listed company. The brand value of Red Tape is definitely more than Bata. RedTape is among the aspirational brand, competes with Hush Puppy of Bata imo. Will have to study it more.

6 Likes

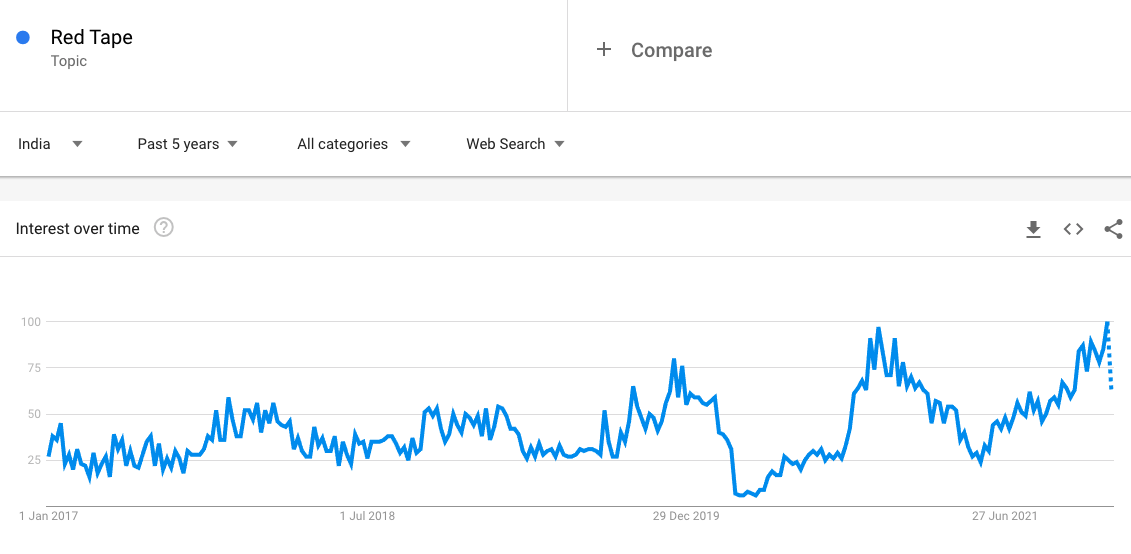

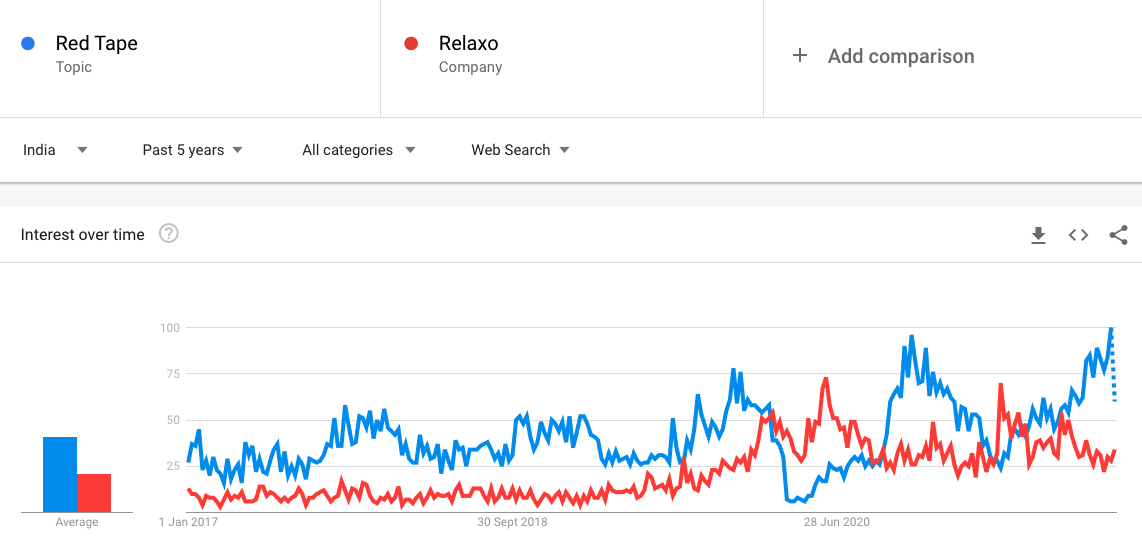

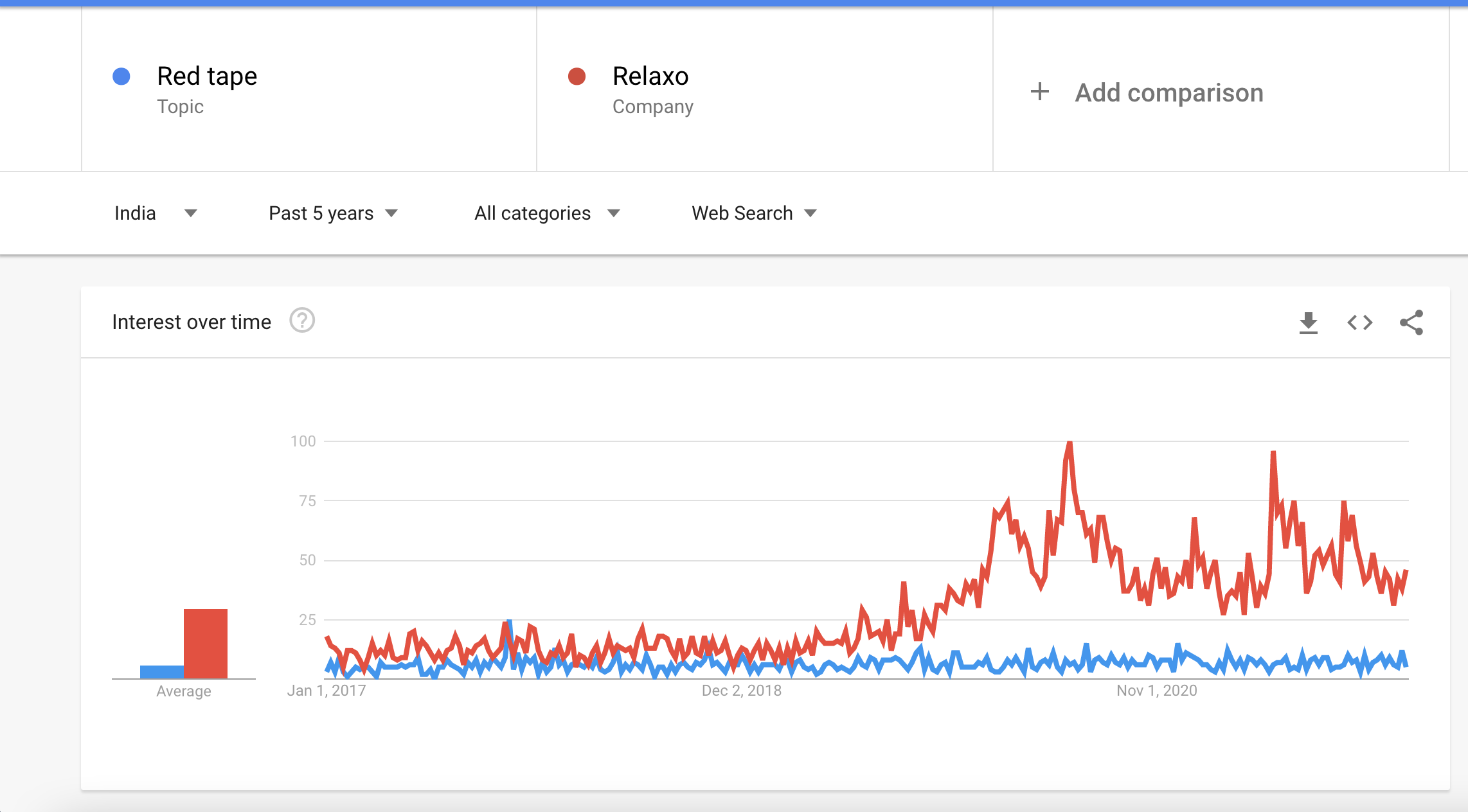

Google Trends based Analysis

For a consumer facing brand, while it is important to have a scuttlebutt based approach we must also rely on aggregates in order to not get derailed by sampling bias (essentially the fact that a small set of opinions need not be representative of the mean or the mode). Brands need to capture eyeballs & mindshare before they capture wallet share. One of the best ways I have found to analyze consumer facing brands is through Google Trends. This represents organic customer curiosity & eagerness to learn about or buy products of the said brand through google search.

We can see that customer interest in red tape has been going up over time. We can also see the dips due to covid waves as customer priorities would have shifted from shoes to essentials. We can see that wave 1 was much worse than wave 2. We can see that customer interest as of now is at all time high.

Let’s also compare the brand interest for Red Tape to that for Relaxo:

Surprisingly Relaxo has much lower brand interest than Red Tape. To me, that means that potentially relaxo audiences might be more interested in or otherwise prefer offline purchases rather than researching online.

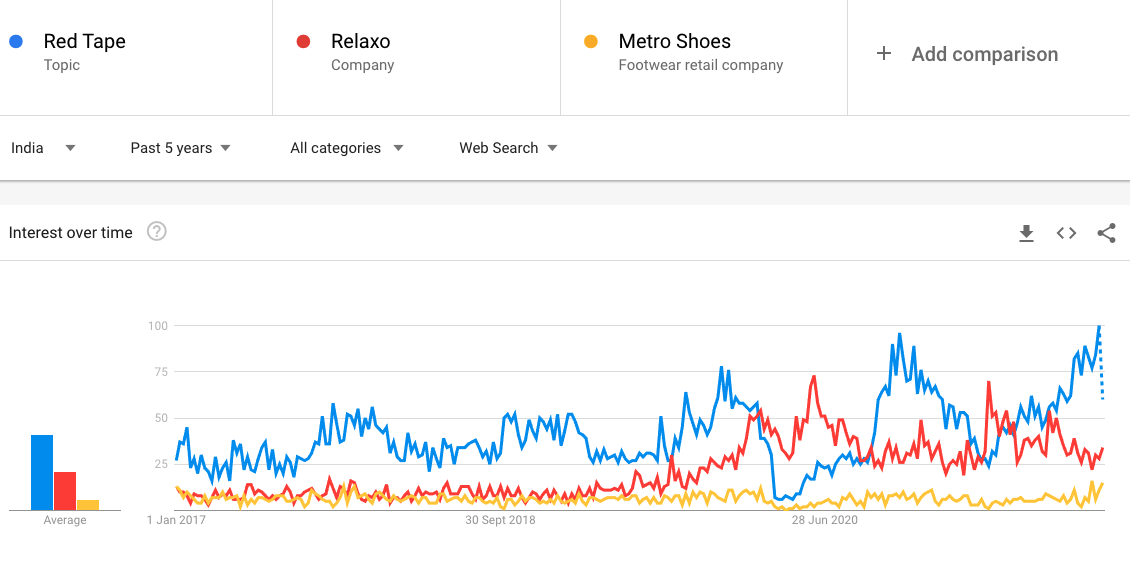

Let’s add Metro Shoes.

Metro shoes interest is even lower than Bata. The interest has also been going nowhere for last 5 years. This should be of concern to Metro & its investors because what it shoes (pun intended) is that any online sales might be based more on advertising & less on organic interest from customer side. That might mean that the online presence is less organic & sustainable.

All in all, I find the data quite satisfactory for Red Tape. Need to see how the customer interest evolves over a normalized covid free period. I fully expect Wave 3 to (in the conservative case) dampen customer interest as focus of the consumer shifts from non essentials to essentials & staying at home.

Similar Web Based Analysis

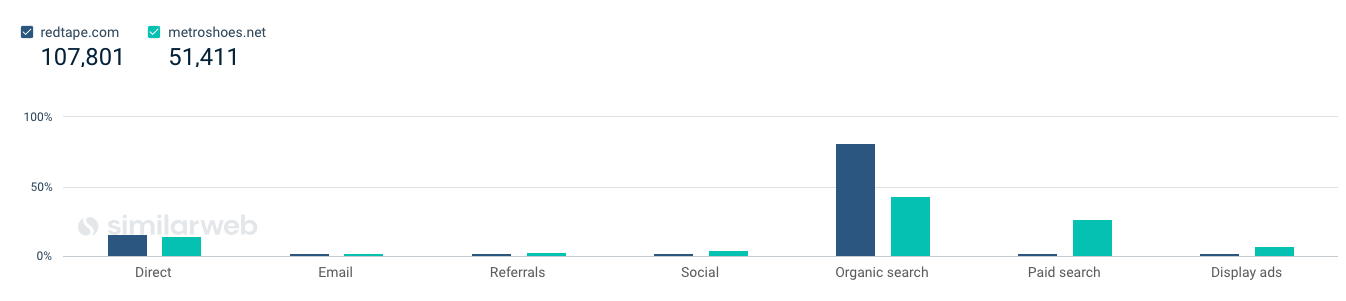

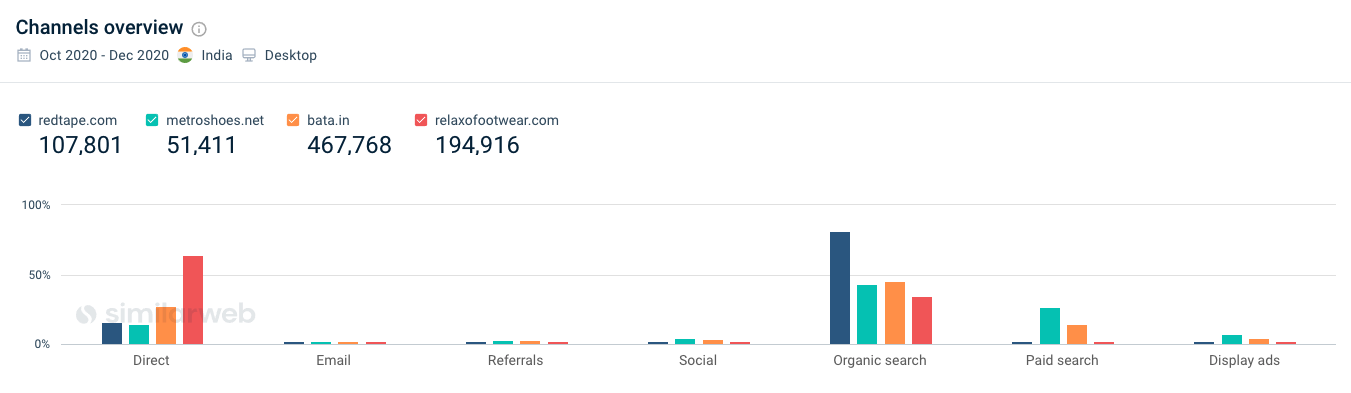

That is this website called similarweb.com which allows you to analyze websites. I took their 7 day trial of pro & analyzed redtape & competitors. Do note that this only analyses traffic coming on to redtape & competitor’s own websites such as redtape.com & metroshoes.net not the traffic going on to 3P aggregators like myntra, amazon, paytm etc.

As suspected, redtape has much better organic traffic than metro shoes:

Lot of metro traffic is through Ads & Paid Search.

In fact Redtape’s organic search leads are far better than relaxo, bata & metro all three. Whereas relaxo has lot of direct traffic which makes sense too since it is a much older brand than red tape. Bata is somewhere in the middle where some of its traffic comes from direct, some from display ads & paid search.

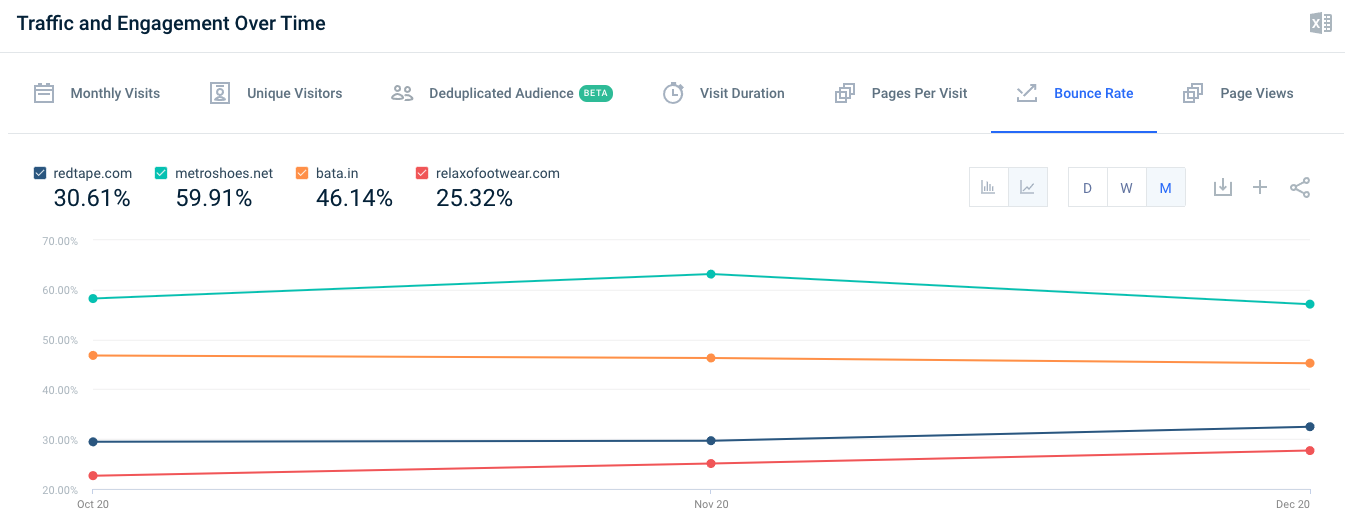

Bounce rates compare how many customers landed on your home page but did not go to any of the children pages (essentially they ‘bounced’ from the home page). Relaxo is at 27%, Red Tape at 35%, Metrio shoes at 57%!!! This means that 57% of visitors to metro’s own website dont do anything after that, they drop off.

Short summary: Relaxo is an established brand. Red tape is an upcoming organic brand that people want to learn about & perhaps commerce in. Metro is paying customers to visit its websites but unable to convert them to commerce.

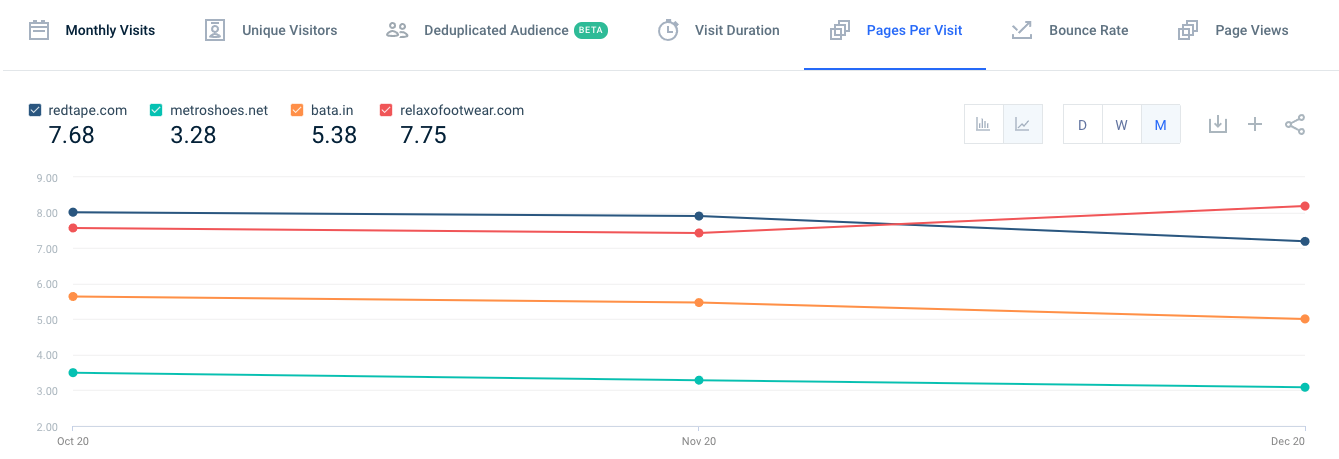

This also shows in the number of pages that customers visit each time they visit the website. Relaxo & red tape fare far better than Metro & Bata.

Unfortunately i dont think i can buy this awesome service its priced at 3000$/year.

Disc: Have a small position, evaluating the company.

29 Likes

@sahil_vi what are your views on promoters as compared to relaxo and bata. How will you rate then on a scale of 0-10.

1 Like

What matters is Not the rating. What matters is the direction of the rating.

What matters is where the puck is moving.

Read my only 2-3 posts to know what i think about the management. Condensing it to a number brings false precision and reduces a complex decision to something which is an oversimplification.

Relaxo had some corporate governance concerns too some years ago, read through relaxo thread. ![]()

![]()

I think management rating was X about a year ago. And it is X*1.3 now.

X can be 4 or 6 depending on the person. But the improvement is tangible. Both in strategy & perhaps in willingness to resolve corporate governance concerns (merging private subsidiary, demerging domestic biz, reducing guarantee comissions.

6 Likes

+1 to the analysis,

Note: You should have compared Redtape with Sparx on Google trends, not with relaxo.

6 Likes

Hey Sahil, The brand search should be uniform and should not be google account specific. Any idea, why I am getting different representation here.

2 Likes

Observe carefully. The red tape topic you searched for has a small t. That relates to a different query topic as compared to “Red Tape” which is the better search term to use.

4 Likes

You should also discuss/compare return policy of bata, redtape, metro and relaxo to compare who is more customer friendly.

Cheers

1 Like