I am visiting redtape outlets and buying their products since last 1 year. All products are quality products. Good behavior of sales person.

2 Likes

Bata gives 30 days of return policy. Relaxo and liberty 15 days. Red Tape 7 days return policy.

Regarding my scuttlebut, it was around few years back, maybe 5 years or more. Bought one Red Tape formal shoe in a sale. Sole broke off in 6 months. Maybe shoe was old. Made me think at that time why did not buy Bata as there was not much price difference. They would have improved their quality by now.

Disc: Hold Bata shares, so my opinions may be biased.

Cheers

2 Likes

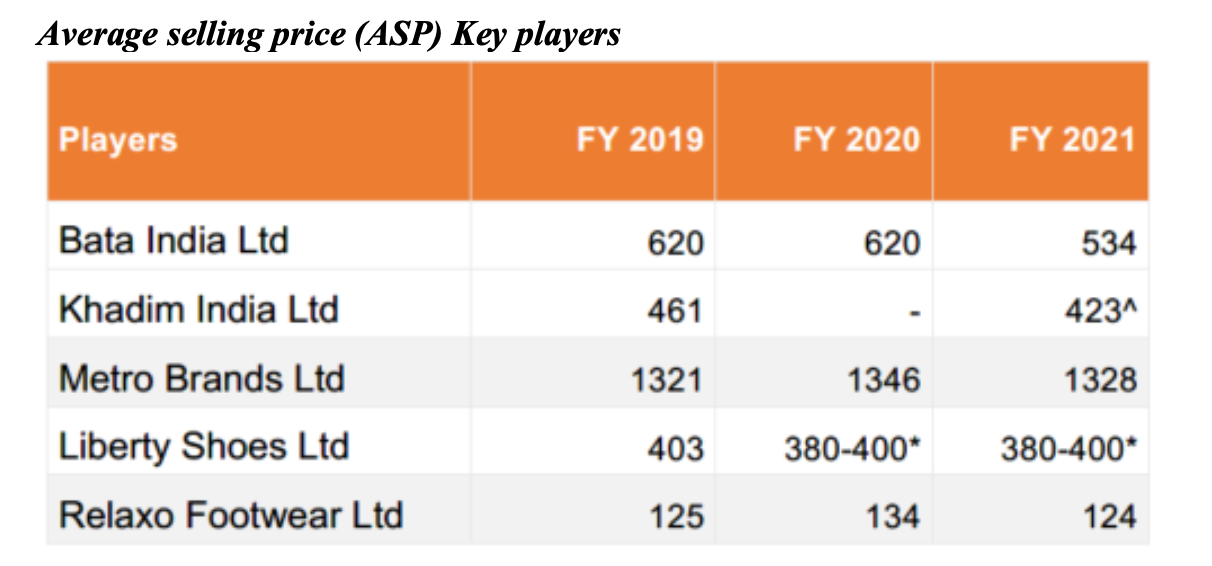

Khadim and Bata are operated largely at the lower end of the spectrum with an average selling price (ASP) of Rs620 and Rs494 as of FY19-20 and Rs534 and Rs519 as of FY20-21, respectively, while Metro operated in the premium segment at the other end of the spectrum with an ASP of Rs1,346 and Rs1,328 as of FY19-20 and FY20-21, respectively.

Does anyone has idea of the ASP of Red Tape?

3 Likes

I think its around 700 Rs. If you go through recent RHP document of Metro Brands you get good information on competation data.

2 Likes

Yes, I was reading the DRHP of Metro shoes and was not able to find the ASP of RedTape.(Mirza)

Source: Metro Brands DRHP Document.

1 Like

Latest Promoter group open Market purchases on 28th Dec - price would have been around 125

Tracking position post demerger announcements - have used products and believe demerged business under Shuja can do well and get re rated, though recdnt run up has been swift post announcements, plan to build position slowly given it typically takes 9 mo+ to get process completed and performance will be visible

4 Likes

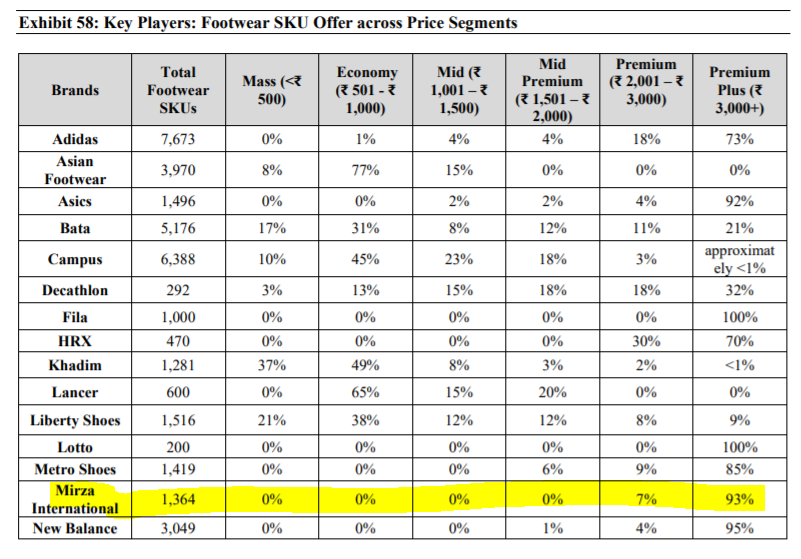

Sorry… I am not able to recollect where I read about ASP of Mirza. Got below info from DRHP of campus activewear. I am bit skeptical about the numbers mentioned here as most of the SKU are sold under discount of 65+% (and usually prices are matched with online prices)

2 Likes

Yeah. Red Tape is a premium brand though. So in no case you get a RedTape below 1k even after best possible discounts. RedTape would most likely be around 1500 to 2000 or higher. Infact, there’d be a high probability of it being >2k (domestic business)

1 Like

I think it cannot be more than 1300 to 1500 as this is the range for metro brands they are much premium than Redtape.

Though I don’t have data to confirm that

I’ve been using RedTape shoes for 2.5 years (thanks to Covid). It is comforatable to wear, costs less, and looks better than Puma which I used to buy before.

Recently looked at their T-Shirts during Myntra sale, it looked good too. They may emerge a competetor for Roadster in few years.

Disc: Invested in the past but no positions now.

3 Likes

Notes form latest AR iro MIRZA INTL -

- Incorporated in 1979. Among the largest footwear manufacturers in India.Also supply leather footwear to international brands and one of the largest supplier of finished leather to overseas markets. Also make and sell processed leather through in house tannery unit.

- Company also foraying into apparels and accessories segments in both domestic and intl markets. Revenue breakup by products -

Branded footwear - 33 pc

Non Branded footwear - 24 pc

Apparels and accessories - 37 pc

Leather 7 pc

- Revenue break up by geographies -

India - 68 pc

UK - 17 pc

US - 5 pc

RoW- 10 pc

- Company’s brands -

Red Tape

Red Tape Athleisure

Bond street ( lower priced for mass appeal )

Oak Tree ( premium leather footwear )

Mode ( Exclusive women’s brand )

Yezdi ( Sports shoes for women )

- Key Infra -

06 Manufacturing units

01 Tannery with state of the art effluent treatment plant ( biggest in India )

02 in house design studios

02 warehouses to serve E Commerce at Noida and Bangalore spread across 70k and 30k sq ft

276 Exclusive brand outlets - out of these, 125 are company owned and company operated.

246 Shop in Shops

05 International showrooms

12 Shop in Shops in Dubai

5.4 cr pairs - annual capacity, 38 pc utilised in FY 21

- Financial performance ( in a Covid hit year ) -

Sales - 1048 vs 1261 cr

PBT - 10.5 vs 65 cr

Overseas revenues - 332 vs 527 cr

Domestic revenues - 715 vs 734 cr ( this is commendable in my opinion if one compares with Relaxo, Bata , Metro brands etc )

Company focussed on driving omni channel sales and bringing virtual engagements that strikes a chord with the customers. Going fwd, digital channel is expected to be a very very imp channel. Company’s brands combine style, quality and value for money propositions.

- India is second largest footwear maker in the world however its exports lags China with the latter having a 65 pc mkt share. This provides a huge runway for growth.

- Business strengths -

Design excellence - has hired best designers to create delightful products. Have 2 in house design studios. Roll out around 900 new footwear designs every year.

Robust Manufacturing - 06 fully integrated manufacturing units equipped with latest machinery enable high quality production. Besides, company also outsources footwear, apparel and accessories.

- With accelerating shift to online channels, company is also confident of its aggressive offline strategy and proactive marketing in order to seize max opportunities.

Channel wise sales for FY 21 vs FY 20 -

EBOs - 462 vs 371 cr

MCOs- NIL vs 83 cr

E Comm - 670 vs 667 cr

- Intl business - Exported footwear account for 32 pc ( 332 cr ) of total revenues. Company supplies branded and white label footwear to UK,US,France, Germany, UAE and others. Have established great relationships with reputed retail chains in these countries. 6 pc of export sales were under the Red Tape ( 21 cr ) brand name. RED TAPE is present in over 1000 MBOs in UK. Company actively looking for China +1 opportunities.

Disc : initiated a tracking position @ 151 by exiting United Spirits ( due expensive valuations )

Views may be biased

8 Likes

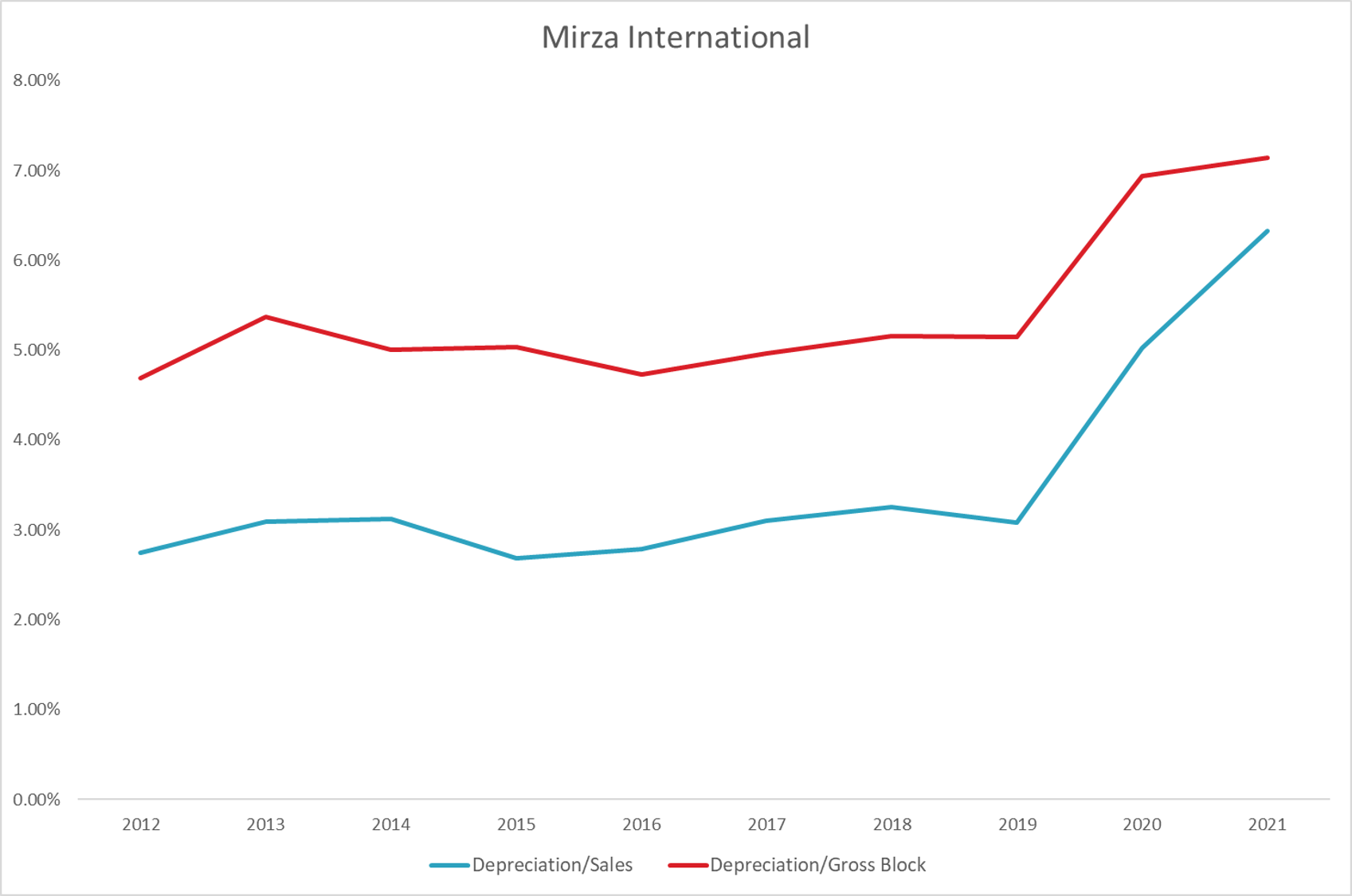

Can an Accountant here help me understand why there is a marked jump in Depreciation (Relative to both Sales and Gross Block) in the last couple of years?

I went through the Annual Reports. I couldn’t find any Accounting Policy change to this effect.

1 Like

Most likely due to a change in the lease accounting standard.

1 Like

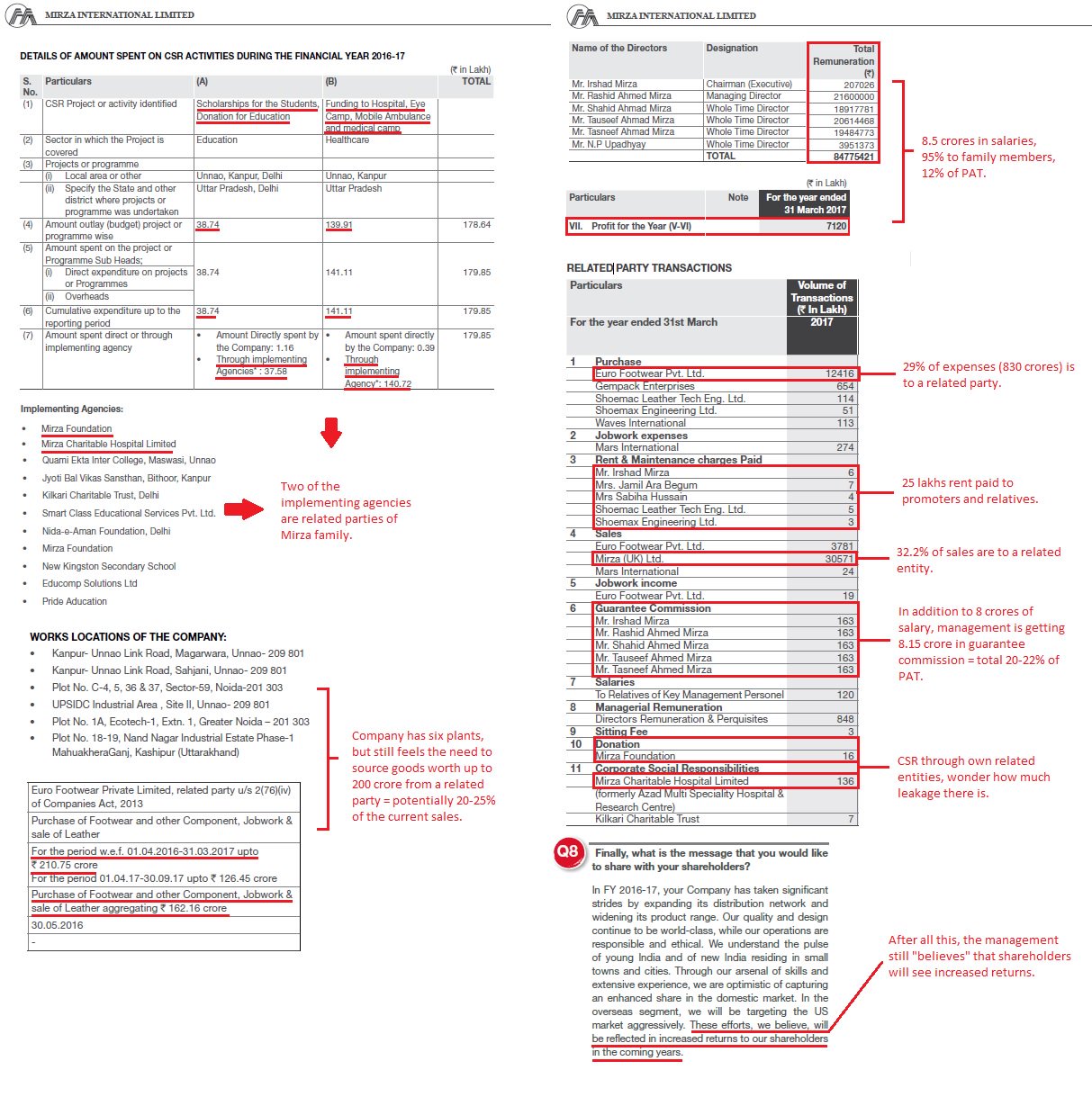

This group had big corporate governance issues in Past … Got this from twitter when I searched there abt this company . Might b helpful

Special situation and bull run - can these clean off the shady image of promoters ?

Y corporate governance is important ? - Recent example of HGS teaches us…

Few here mentioned about the quality of Products- it’s subjective- few have bad experience and few good …

So it can’t b a factor of investment… Personally my experience is not so good with this brand…

N few mentioned about the Popularity of Red tape brands… A company called AFL has world renowned brands under it and after initial Demerger ephoria c the condition of stock price. Even they had capital allocation issue…but many ignored it …

10 Likes

I am not giving any investment advice here … but seems no caution at all .

Twitter threads are popping up , YouTube videos of suggestions , Even special situation PMSs are recommending Without giving any much negative side of it …

People r saying new generation is coming to board … and Hopefully they will learn from past …

Does it mean that old gen will sit at home and have no call in companies affairs…

And how can people assume new gen people r fully of ethics ? Check parabolic drugs - recent fraud case , coincidentally they are young…

And can investment decision be made on Hope ?

And finally if people are saying stock is getting rerated due to it fundamentals … Even MTNL is 6x in last 15-28 months…

At the end it’s individual choice where to invest .

Good luck all…

14 Likes

I do suggest we try and dig more.

The brands listed by you for AFL - are they owned by AFL or licensed by AFL? The owner of IP would more often than not command a higher premium. That’s one. Secondly, AFL degrew from FY2019-20 to FY 2020-21 by a whopping 30%. The EBITDA margins are under 10%. Loss making. Merely having a brand wouldn’t give you good valuation, right?

Coming onto the CG portion. Executing CSR strategy through group entities is very common. What we should focus on is if Donations + CSR expense higher than statutory limits of 2% of AVG NP of past 3 FYs? If yes, then it would be a valid point. If not, its not an issue imo. Even PI Industries has a PI Foundation or something through which it executes CSR activities. A lot of corporates do this since they can’t (and validly so in many cases) rely on third party vendors / organisations.

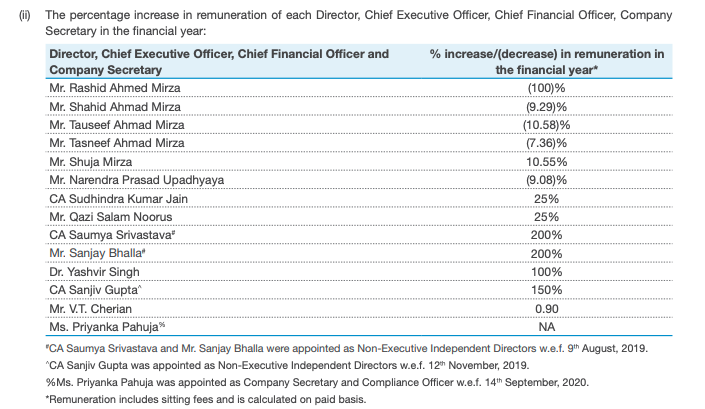

Promoter Salary - Screenshot from FY2020-21

Promoters have not increased salaries in 4 years while Sales have grown from 900crs to 1300crs in the same period. PBT has come down but that maybe due to other issues, lack of focus, increased competition, etc. Certainly not due to promoter salaries.

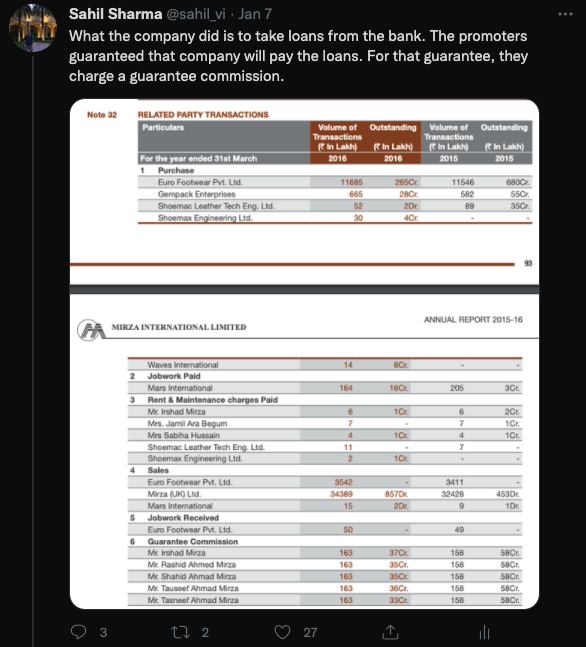

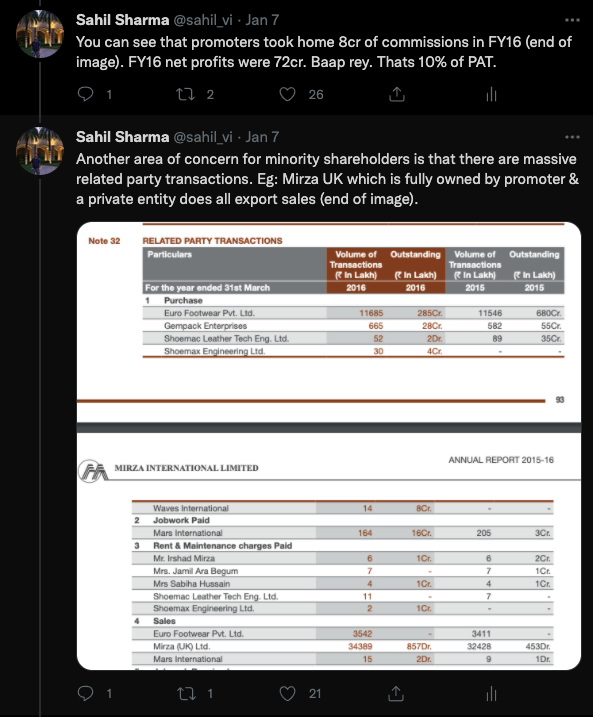

Guarantee Commission - Point already spoken about. For the sake of repetition though - it has come down to 1.5crs in FY 2020-21 from around 8crs in FY 2016-17.

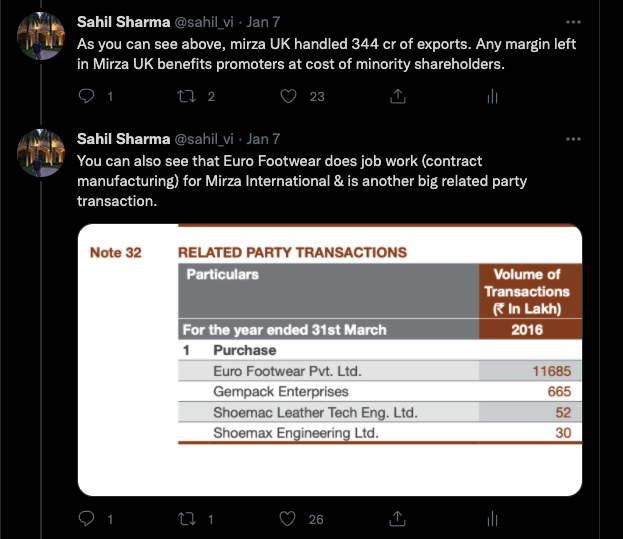

Sales to related entity – Again. This issue doesn’t exist post demerger since the hold co of Mirza UK Ltd i.e. RTS Fashion - which was earlier held outside of the corporate group and independently by the promoters - will now be amalgamated with Mirza International Ltd. We can debate hold co discount or whatever but the RPT issue (to promoter owned entities) will not exist post the restructuring. All profits / valuation of Mirza UK Ltd will now be baked in the valuation of Mirza International Limited.

Purchases from related entity – Yes. This is an issue and will have to look at this in greater detail.

Ahh, yes. Old gen does indeed sit at home beyond a point. Anyone operating a small / medium family business will tell you so ![]() or atleast that has been my experience. On a more serious note, the valuations could be low (compared to peers) because of negative sentiment on corporate governance. How it shapes up is anybody’s guess.

or atleast that has been my experience. On a more serious note, the valuations could be low (compared to peers) because of negative sentiment on corporate governance. How it shapes up is anybody’s guess.

Yes. Biggest case in point would be the astronomical valuation of Tesla or Rivian (with 0 sales) or companies working in very very niche tech space. Hope drives optimism, which drives valuations. Ofcourse its dependent on someone’s risk appetite too.

10 Likes

You nailed it Aniesh. The issue is of commitment bias, once one forms a positive opinion about something, they neglect the risks or grey areas, disconfirming evidence is also brushed aside. The concern is people who are not well versed with these events take these positive opinions and invest their hard earned money. I have significant investment in Arvind fashions and other than initial listing fiasco by exchanges i am not aware about corporate governance issue, can you pls help me if you have some information.

And let me call out loud, i too have small position in Mirza due to demerger arbitrage and relative valuation, but i will never put serious money into it unless there is proof of good governance.

Hindsight bias and assuming certain outcome as confirmation of ones’ right action is very common not only in stock market but in our normal lives as well. Hence all great investors attribute a large part of their success to luck and being at the right place at right time.

Finally as you mentioned every one has an investment process and wish everyone good luck !

3 Likes

very pertinent, my feeling is people rarely change or we should have examples of some companies where people have turned ethical, would like people to look at the threads of dhfl and yes bank, The wadhwans were known for past misdemeanors, but in post after post there is justification saying he has changed and infact it was his brother or cousin who was the culprit.Yes bank thread runs longer and similarly non conforming evidence was shot down. Not saying that similar thing could happen here, but pays to be careful. The second point is about too many of the Mirzas wanting a share in the pie. Not about money only, it is about ego,wanting management control, establishing their own fiefdoms and in short too many cooks spoil the dish.

6 Likes

Some fair points raised by fellow boarders on both sides especially on the corporate governance aspect. It may help to think of the probability for a bull/base case scenario from corporate governance point of view. I’m not going to talk about a bear case scenario as the market is not pricing in any bearish view from corporate governance standpoint. Price action of 3x in 6 months is purely re-rating of management/business as profits or cash flows are not going to become 3x. Also the bear case for bad management / corporate governance will not really be 10, 20% downside - it will lead to severe wealth destruction if not complete capital loss so nothing much to cover in the bear case.

Bull Case - Low Probability

The bull case scenario is quite obvious and low probability in my view i.e. the management team’s character/personality has undergone a complete makeover and they start making all capital allocation decisions by safeguarding and rewarding minority shareholders going forward. And market continues the re-rating of the company with valuations somewhat trailing the superior quality franchises such as Relaxo, Bata, Metro brands, etc. If this situation does play out, this is going to be a mega multibagger.

Base Case - High Probability

Management has noticed the market frenzy for IPOs / demerger listing stories and wants to take advantage of the same. Management wants to present this new facade of a “clean, well run business” with highest standards of corporate governance and announced this demerger of the branded business to reap the same fruits as it’s peers mentioned earlier. However, this is mainly till the demerger process goes through and Red Tape gets listed at the appropriate valuations. So during this time, management wants to ensure it is making all the right moves, acting in the interests of minority shareholders and leading everyone down the garden path. However, sometime after Red Tape listing the management comes back to it’s original colors and poor corporate governance track record which subsequently ends the market participants’ current infatuation. By the time this happens, I expect significant upside from present market cap. However, I’m not sure if CMP provides enough MOS as majority have entered the party earlier.

Why I also believe at least the base case should play out - one of the promoters has been buying from the market as recently as a few days back. The same promoter bought at levels of 58 and last bought more than 1.25 cr worth shares at 128. I can’t think of many ways a promoter will buy crores worth of shares without being bullish on the near term outlook at least.

Disc: Biased as I’ve invested with transactions in the last 30 days revealed on my portfolio thread

9 Likes

everything in this screenshot has been discussed & priced in for about 4-5 years now. If you see carefully, the screenshot is from FY17 annual report Just for a quick recap:

- CSR activity - many corporates have their own foundations.

- Company has 6 plants but still does job work - If the investor took the pains to listen to the concalls investor would understand why this happened. Euro footworks was a competitor & mirza wanted to align the competitor with themselves so they took a minority stake of 49% in the company. Although this is a related party, it is controlled by a private individual. Since mirzas own 64% in mirza international, it is in their own self interest to retain more margins in mirza. Nonetheless this remains one of the corporate governance overhangs. Once Redtape demerges though this would go away since jobwork would be done for leather shoes & will most likely end up in mirza international, not red tape. For me personally, red tape is the company worth owning going forward. I would be looking to exit mirza international post demerger.

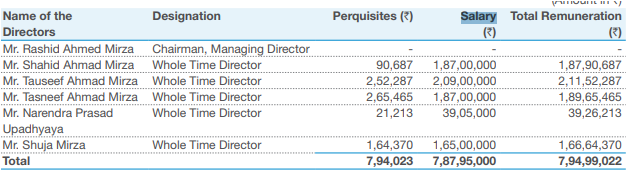

- Toal remuneration of 8.5 cr to mirzas which was 12% of PAT in FY17 has been reducing for some time. Take a look at this screenshot of FY21 annual report. Specially look at Mirzas comp:

some of them have gone down by as much as 100%. Only one going up was Shuja mirza who is the work horse running the business.

Total remuneration to Mirzas has gone down from 8.5cr to 7.95 cr. Notable is fact that Rashid mirza takes home a salary of 0 now. - The guarantee commission has been the biggest problematic issue. It has gone down from 8cr to <2cr this year. Red tape should have no guarantee commission since it will be a cashflow machine which is able to grow from internal accruals & would not need debt. For me one major anti-thesis is if guarantee commission does not continue to head downward over the years winding down to 0 in 2-3 years.

It certainly can and will be. Aggregate of these experiences is reflected in same store sales growth which has been wonderful for Red tape (around 18-20%). Much higher than peers.

6.

Not a fair comparison since AFL does not have the profitability. As i have shown in segmental analysis few posts ago, Red tape has pretty good balance sheet, growth & profitability.

7.

I am personally offended at this insinuation of not covering the negatives properly since you mentioned twitter threads & i am the only one who made a thread in the last few days. The corporate governance issues for mirza have been covered front right & centre. I have also meticulously explained that this is a high risk high reward scenario & that it is important for investor to position size the bet since this is sort of an all or nothing bet. If corporate governance improves on ground, you get a mega upside, if it remains same, you lose everything.

Please dont tell me that the negative side has not been discussed at length, because it has been.

There is no hope involved here, only facts. Please listen to the concalls that happened until Feb’20. Shuja mirza is the one who has been patiently answering investor concerns on CG on all calls, talking about guarantee commission going down, talking about demerger.

9. For those that believe that there is no redemption, once a chor always a chor, please do due diligence & study existing threads on valuepickr. ![]()

![]() Study the relaxo thread to see how CG issues have evolved. Quoting from the relaxo thread:

Study the relaxo thread to see how CG issues have evolved. Quoting from the relaxo thread:

Does the word guarantee commission ring a bell?? Evidence suggests that as long as managements walk the talk on improving CG, rerating occurs. Look at APL apollo, look at borosil group (people mention the real estate transactions even today, despite clean up that has happened & is happening). Whether you believe that such changes are true change of heart or window dressing a pig with lipstick is a matter of personal choice. I am in neither camp. I am not eager to make up my mind. WHat i will do as an investor is actively seek evidence from all investors AND sellers to understand what conviction or concerns they have. And then try to ascertain how much truth there is to such claims. Attaching a few other screenshots of relaxo CG concerns raised on forum.

10.

Market works on probability not possibilities. It discounts current evidence. Evidence is that CG is improving:

(i) guarantee commission going down

(ii) promoter remuneration flat for 4-5 years. Key promoter remuneration down to 0

(iii) Merger of UK privately held subsidiary into mirza international

(iv) jobwork will also stay in mirza int & red tape would not have lot of RPT in my understanding.

11. We have seen prior examples (Relaxo, apl apollo, borosil twins) where cleaning up the mess does result in sustained rerating. There is redemption even for poor CG past if they walk the talk. Whether tthey are walking the talk or not is something which investors need to develop their own conviction about. I for one am not sanguine about this investment. I am actively seeking disconfirming evidence which can show that they have other skeletons in the books which are not priced in. Havent found any yet. If i do , this forum would be the first to know.

12. Let us also discuss why I decided to invest in this company despite the CG concerns (my personal decision might not work for others). Red tape is growing at 30% CAGR. I Expect topline to be at least 3x in next 5 years. The valuations are at around 2x sales. All peers are valued at > 10x sales. The CG is headed in right direction. If it continues to head in right direction, i expect valuation gap to narrow. a rerating would not be out of ordinary. My upside is multifold. My downside is in the case where CG continues to become worse. I lose all my capital & it goes to 0. Hope the disproportionate risk reward setup is clear. Still i have position sized to 3% since loss of capital is a real possibility here.

Disc: invested, but very hyper aware of the possibility of capital loss so position sized to 3% of portfolio.

50 Likes