June quarter result too good  even it’s beat 2019 june quarter result

even it’s beat 2019 june quarter result

2 Likes

Despite being a lockdown quarter Mirza has finally delivered…with all segments in green…overall stupendous results…leather turning black after long time…icing on the cake is PLI scheme being thought upon leather sector which could be next trigger…with lower debt now and better working captial management the stock looks good in near to medium term.

4 Likes

Among three big players in footwear sector only Mirza give positive result this quarter now on only 16pe,

It’s just matter of time or i am missing something?

Hold biased

1 Like

No all good. In coming Q We can See more reduce of debt. Asset light Business Model.

No more Royalty on loan.

Sales improving.

Leather is Back in sales.

Waiting for FPI Policy to be announced for Leather Sector.

7 Likes

Promoters buying in open market 150000 shares acquired.Sign of promoters confidence and markets undervaluation.

6 Likes

at CMP MIRZA is a great value buy. I added this today. last year only 36% capacity utilization was due to covid. New stores opening, BS improving and going forward, growth with PE rerating is on the card. Technically 70-72 is the hurdle. once closed above this zone weekly then New leg of a rally for 2-3 years begins. I have invested for a minimum of 10X in 4 to 5 years.

5 Likes

My few lines on this:

- The products launched under REDTAPE brands like Soldiers, handkerchiefs, Undergarments.

- REDTAPE athleisure has been getting great reviews on Flipkart & Amazon

- Promotors buying from open market in August.

- Heavy flooding in several units of Vietnam results in big surge of export orders.

Technically it formed a Cup and handle formation in progress in Daily charts. If crosses 72, then the new uptrend may start.

3 Likes

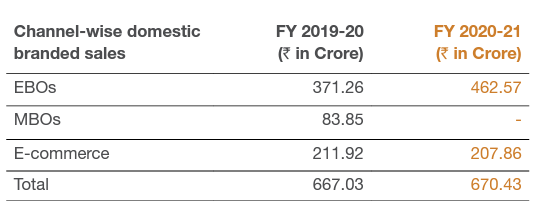

The products of Mirza International have gradually started coming in limelight, mostly credited to the social markets. Red Tape has been a tall standing brand with great stature in itself for the shoe segment. I also see exclusive shops opening every now and then. While saying all these, I have a query on the topline growth which seems to be falling since previous 2 quarters (attached snapshot). While the growth is supposed to be accelerated by the opening of exclusive shops, but the real shot in the arm is expected from the online platforms. Seen some great reviews for its products, wondering what is the reason for the fall!!

3 Likes

Hi @bimalb Agree with you on the great brand they have…and they are further trying to build on the same. Reason for lower June 2021 is due to the covid shut down and usually March quarter is sub par compared to Dec quarter as Q3 is action packed with several things like festivals, wedding season and also winters (company has started selling winter wear like Jackets which have a higher per unit sales prices compared to normal summer wears)…all of this helps them with a strong Q3.

I think they have been able to so far sustain the painful period and going forward if the company is able to grow and at the same time take care of its balancesheet then this could be a big winner.

Hope this helps!

Regards,

Yogansh Jeswani

Disclosure: Tracking

6 Likes

Fii holding increase this quarter, i think slowly they corner stock, products are very good but if they execute d’mart like model and company own store then long term it’s better, but going to big long time…

3 Likes

Value of the acquired shares is below 1cr. With this miniscule buy from the open market, nothing can be said about the confidence in the company!!

Just to update, Heard from a friend. Mirza Int , exploring in UEA , Nepal and Srilanka, You can check the new website , It have started business from Sep. Do check these, Managment now is very clear on his vision, Khadim is re rating , Metro IPO coming , This can be trigger for a good upside.

6 Likes

Restructuring can be , New managment , Might be provate player like BATA and Merto, Could be merger of UK Business , Any thing on re structuring in current senerio is a huge positive for Mirza.

Just things Mirza to re name as Red TAPE like other brands BATA METRO ETC.

5 Likes

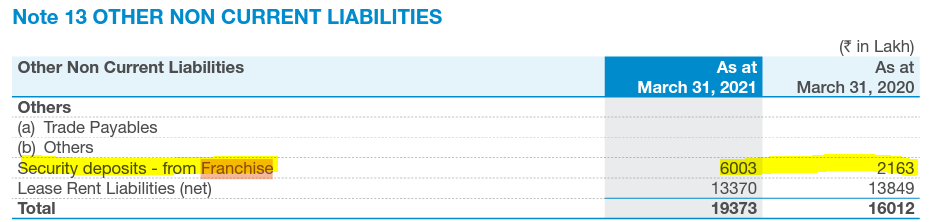

As per the latest annual report looks like company has stopped selling through multi-brand outlets and focusing more on EBOs through franchise model which in turn reduces overall working captial cycle and thus allowed the company to reduce its debt by 2/3.

As security deposits increased by 40cr and given each store deposit as 50,00000 then new franchised stores comes around 80 out of total 92 stores for fiscal 2021

11 Likes

2 Likes

@ayushmit Sir any inputs now how do you see this turn around.

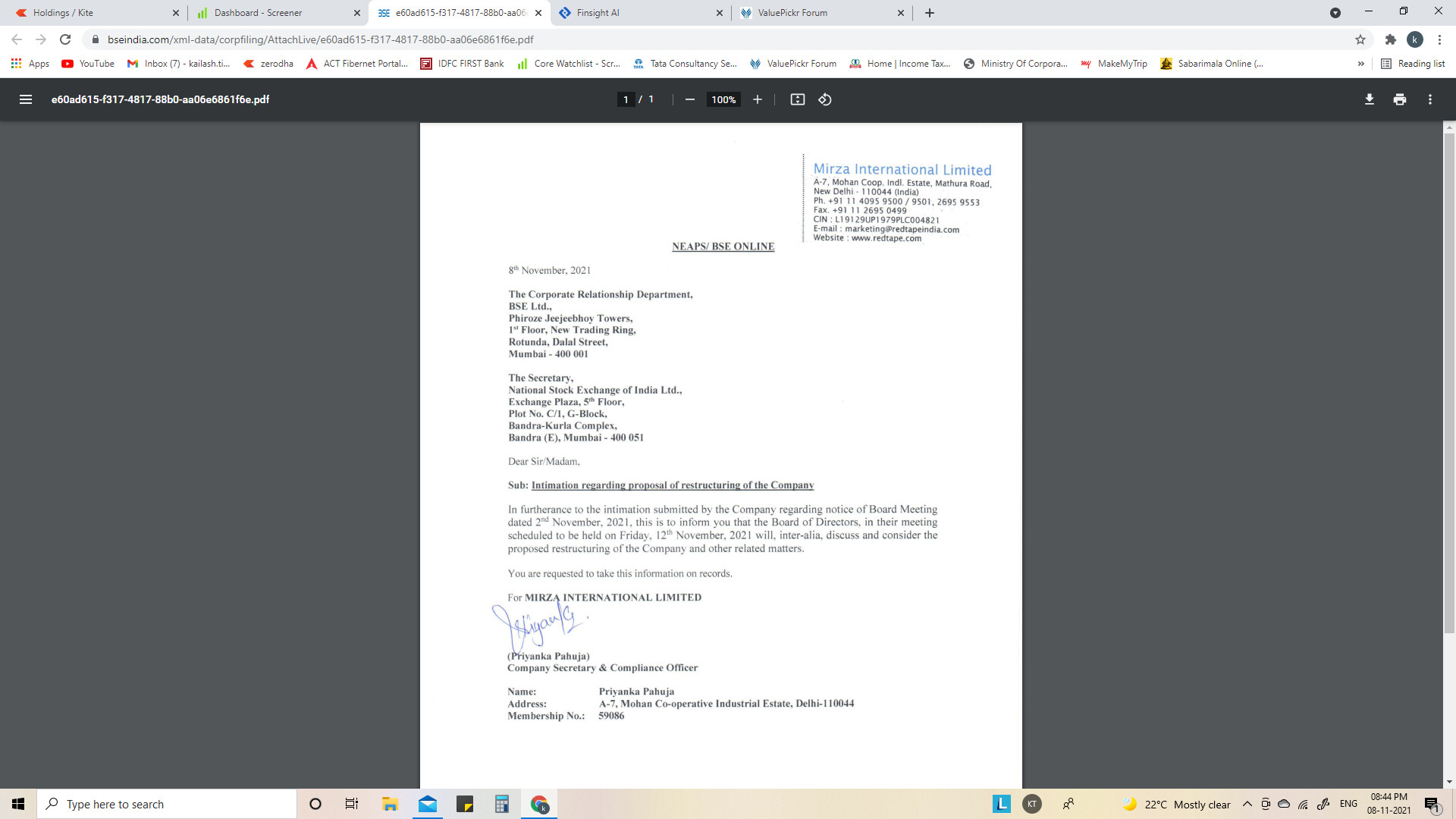

Pursuant to the provisions of Regulation 30 of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2021, this is to inform that the Board of Directors, in their Meeting held on 12th November, 2021, has, inter-alia, in-principally approved the proposal of the amalgamation of RTS Fashions Private Limited, the ultimate holding company of Mirza U.K. Limited, with Mirza International Limited and demerger of Domestic Business of Mirza International Limited into a Resulting Company, on mirror shareholding basis, in such manner as may be deemed fit and proper.

Results are good comparatively but margins are down.

Finally after a long long time some value unlocking taking place

- Long awaited merger of U.K business with the company.( Conflict of interest and Corporate governance issue resolved)

- Demerger of domestic business to be listed separately most probably new company name REDTAPE india limited could be a game changer and create value for shareholders)

16 Likes

The company is going global and expanding its global footprint, Now it has brand outlets in dubai,nepal and srilanka.

Redtape opens exclusive brand outlet in srilanka.

6 Likes

Notes from latest credit rating update -

- List item

CRISIL Ratings has placed its ‘CRISIL A-/CRISIL A2+’ ratings on the bank facilities of Mirza International Ltd (MIL) on ’

Rating Watch with Developing Implications

‘

amalgamation of RTS Fashions Pvt Ltd, which is the holding company of Mirza U.K. Ltd (Mirza UK) with MIL. Mirza UK is a related company of MIL. Furthermore, the domestic business of MIL, which comprised 68% of revenue in fiscal 2021, will be demerged into the resulting entity

The company had revenue of Rs 355 crore and operating margin of 9% for the six months through September 2020 as the operations were significantly impacted by lockdowns imposed to contain the pandemic, leading to debt of over Rs 400 crore as on September 30, 2020. Driven by healthy operating performance subsequently, the financial risk profile has improved with debt reducing to Rs 221 croreas on September 30, 2021.

2 Likes

Hi @siyaram7

As I have not been tracking this business, could you please expand on this statement?

How listing Redtape India separately will be a game changer?

1 Like