An article published on substack. Here I discuss about Kaynes Technology India Limited - The EMS giant in making and Cohance life science ( older name Suven Pharma ) ~ Demerged CRAMS Arm of Suven Life Sciences. In fact the prices have gone done from the anchor price discussed here

FALLING KNIFE OR PHOENIX BIRD

The year was 1963. Tino De Angelis was the undisputed vegetable oil king in the US. He and his establishment: Allied Crude Vegetable Oil refining Company (Allied) was a big player in the Vegetable oil futures market and had cornered the market. They peddled stories of impending crop failure in Russia leading to Russian purchases of US oil and kept pushing the futures prices up. Their positions were backed by vegetable oil stored in containers. AEFW (American Express Field Warehousing Co) had issued warehouse receipts confirming the Oil stored in tanks held by Allied. AEFW was one of the 4 subsidiaries of American Express (AMEX). AMEX was the dominant player in the travel and financial services domain. But oil prices couldn’t be held artificially high for long. With each subsequent oil price decline, Allied needed to provide more money in margin accounts. By November 1963, the exchanges and government commodity agencies finally realized that Allied was driving up futures prices. When a commodities exchange investigator demanded to see Allied’s records, the gig was up. Allied filed for bankruptcy. Futures prices plummeted. AEFW’s warehouse receipts had totaled twice as much vegetable oil as all the oil in the U.S. That’s when all hell broke loose. Allied filed for bankruptcy and when AEFW inspectors went and checked their collateral they found that the tanks were filled with sea water.

AMEX stock tanked in the aftermath. That along with the assassination of JFK ensured the AMEX stock took a royal pounding. Since AEFW was a separately incorporated subsidiary AMEX was not legally bound to take responsibility of the losses incurred by AEFW. But the CEO Mr. Clark, accepted moral responsibility and vowed to do good any of the damages due to the banks and financial system at large. While this statement soothed the nerves of the bankers, the stock market didn’t like the move as the liabilities amounted to almost 1-year revenues of AMEX.

That’s when a fund manager from Omaha, Nebraska one Mr. Warren E Buffet spung into action. Mr. Buffett wondered what impact the scandal would have on Amex’s reputation. With travelers cheques and credit cards, trust mattered. Buffett needed facts. So he and an acquaintance visited restaurants and other places that accepted Amex cards and cheques. They talked to bank tellers, bank officers, credit-card users, hotels employees, and restaurants workers to get a feel for whether usage had fallen off. Based on that research, Buffett concluded that while Wall Street had punished Amex by battering the stock price, Amex’s reputation hadn’t been tarnished on Main Street.

Having got convinced that AMEX is here to stay despite a temporary incident, Buffet committed a substantial sum of $ 3mn amounting to 17% of Buffet Partners Limited total AUM to AMEX stock in 1964 at an average price of $ 41.22 . As he had suspected AMEX was able to manage the fiasco and 2.5 years later AMEX was quoting $ 92.5 at a cool 124% gain.

The reason for narrating this incident is not only because I am a huge fan of Warren Buffet (which I am), but there are interesting parallels in the current Indian market. Since September 2024 we are in a sideways market and even though most of the front line indices have moved to Highs after almost 15 months in Novemeber 2025, there is wide spread pain beneath. The broader markets have been benign and Small and Midcap stocks are getting beaten up left right and center. Some of the darlings of last year have fallen bigtime from their all-time highs and are now available at reasonable valuations.

I plan to discuss 2 such businesses. When I analyze a business one simple mental model I follow is to think if this particular business can double from the current prices in 3 years (circa 26% CAGR). If I can visualize that happening, despite the current headwinds that is suppressing the stock prices then I believe benign prices are a boon to a long-term investor.

Kaynes Technology

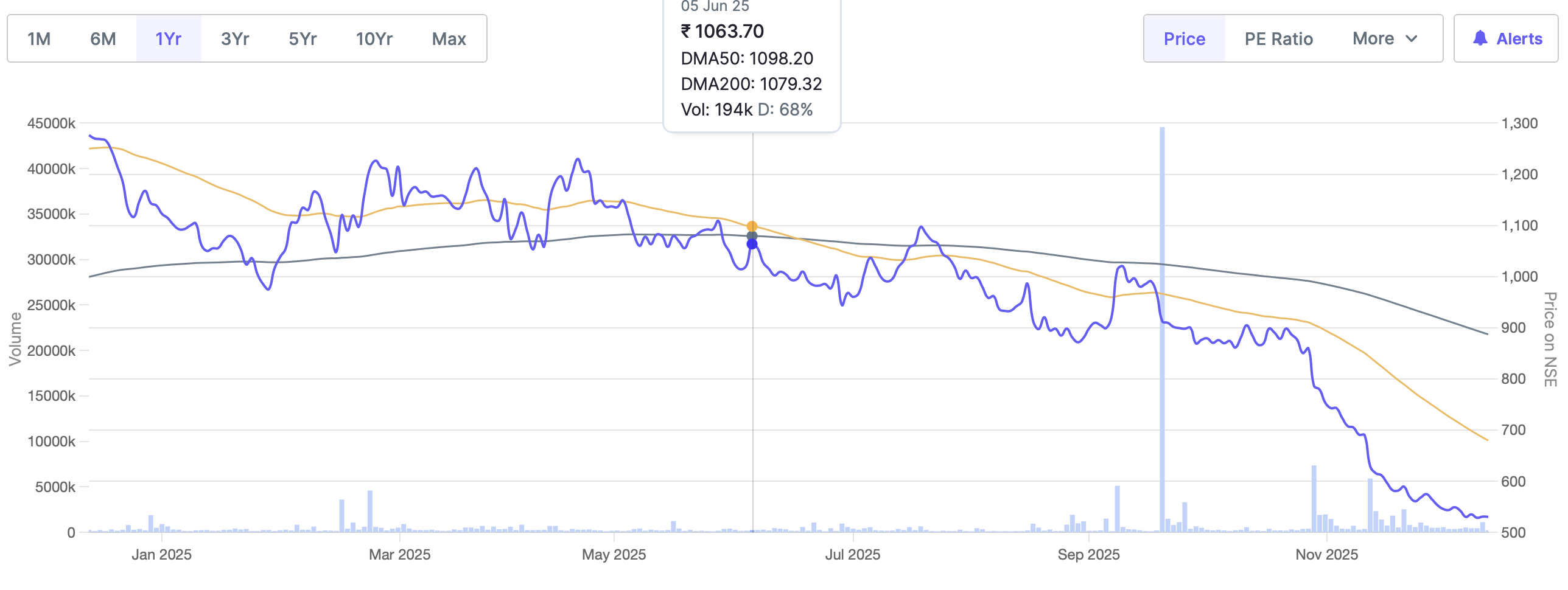

CMP: Rs 3875 | Market Cap: Rs 26000 Cr | 52 week high: Rs 7600

Recently Kotak Institutional securities came out with a report mentioning accounting irregularities from their annual report analysis. Management later came out with clarifications in their investor call. While they accepted one inadvertent omission in their standalone notes to accounts pertaining to related party transactions of Iskreameco (Subsidiary acquired by kaynes for Smart Metering business), they were able to give satisfactory clarifications to most of the other allegations.

Despite these clarifications the stock took a pounding and is currently down 50% from their 52-week high. The reason why this temporary blip can be an opportunity to the Intelligent investor is as follows:

1. Kaynes technology is transitioning from an EMS player to a full fledged ESDM player with design and IP capabilities.

2. Kaynes is one of the first and very few companies present in the nascent Semiconductor eco system with its OSAT facility (Outsourced Semiconductor Assembly and Testing) coming up in Gujarat.

3. Kaynes is also setting up a multilayer PCB manufacturing unit in Chennai which is one of the first in India and is an import substitution.

4. Kaynes is growing at a blazing pace & has given an ambitious target of growing 50% per year for the next 2 years.

So, the final question is will they go belly up ?, if not then with so many optionality’s under their belt , the market is bound to reward high growth and once the new capabilities and optionality’s come on board,Kaynes might get valued basis its long-term averages.

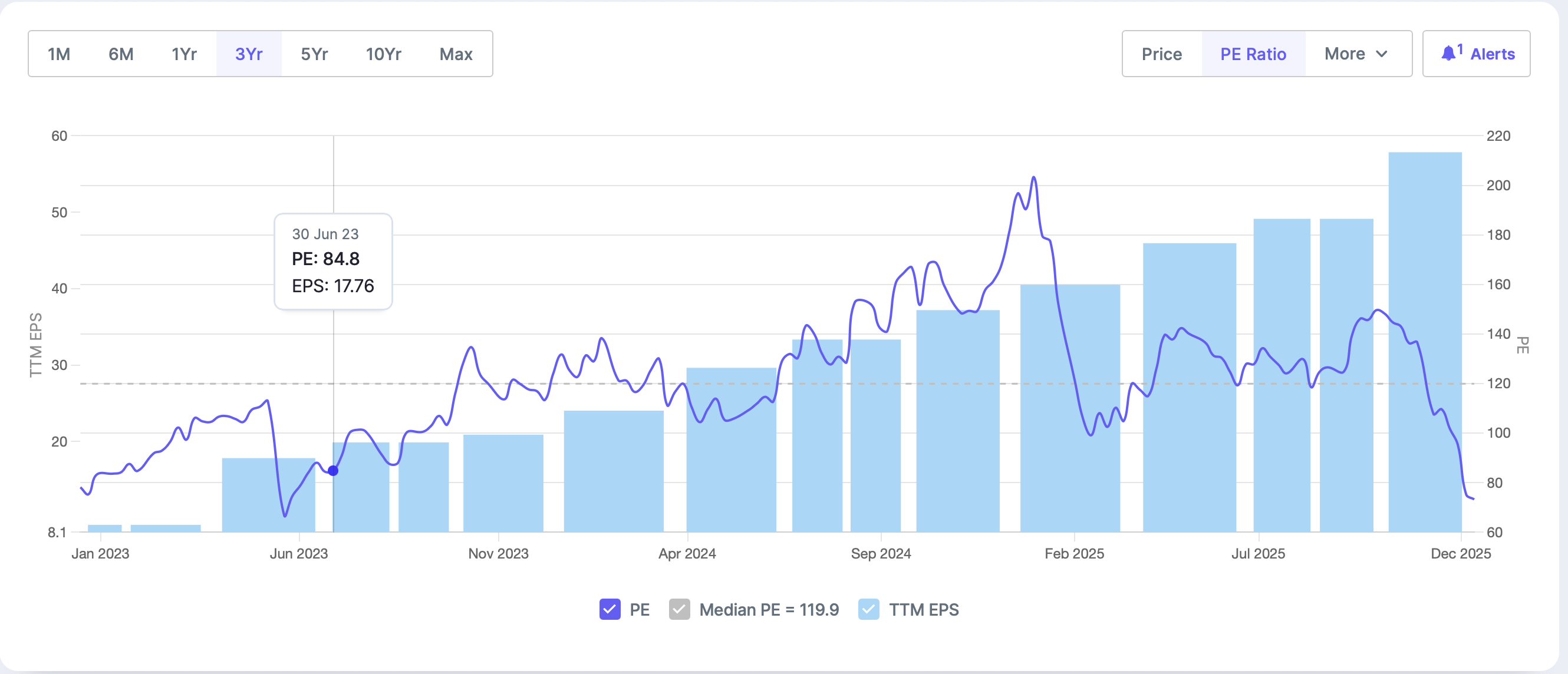

Presently at a P/E level Kaynes is trading at its lower band of the 3-year averages. While still P/E of c. 70 might look optically high I believe this must not be viewed in isolation but in line with long term averages and scale of growth.

In conclusion I believe that Kaynes as current levels (c. Rs 4000) presents descent value considering all the business tail winds and optionality.

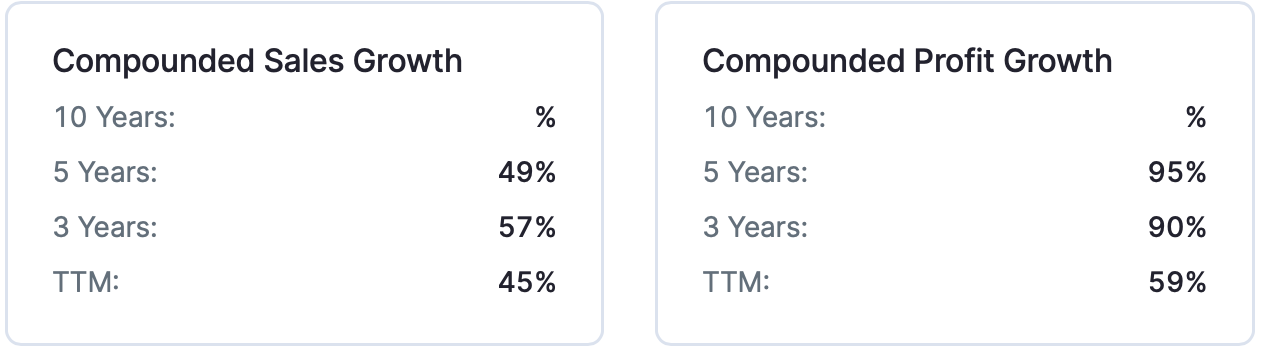

2. COHANCE LIFE SCIENCES

CMP : Rs 535. | Market Cap: 20,500 cr | P/E: 59.5 | 52 week high : Rs 1276

BRIEF HISTORY

COHANCE Life Sciences is the current form was born out of the merger between Cohance Life sciences and Suven Pharmaceuticals. Suven pharma was the demerged entity to carve out the CDMO business from erst while Suven Life Sciences (Suven Life is still run by old promoter Venkat Jasti and it is focused on Drug discovery). Suven Pharma prior to merger with Cohance has already acquired 2 entities namely Sapala and NJ bio , both having specific capabilities. Cohance was the entity controlled by the PE firm Advent. It was envisioned by Advent as a Pharma platform combining three entities Viz: RA Chem, ZCL Chemicals and AVRA Labs. Now post-merger the combined entity is called Cohance with Advent at the helm.

Advent post-acquisition has brought in top industry talent to run the show. Post merger the combined entity had drop in margins (Suven Life Sciences was known for its industry leading margins of 40%+) since Cohance was lower margin business compared to Suven.

But the Merged Cohance Entity is not small fish. It is one of the few entities that has the capabilities of ADC (Antibody drug Conjugates). ADC therapy is one of the hyper fast-growing therapies worldwide with an expected growth rate of c. 25% CAGR till 2030.

Cohance in addition to ADC also have capabilities in Nucleotides

Nucleotides are the building blocks of DNA and RNA — the molecules that carry genetic information in all living things. In biology, they are essential for:

They are fundamental to genetic therapies, vaccines, molecular diagnostics, and modern biological science.

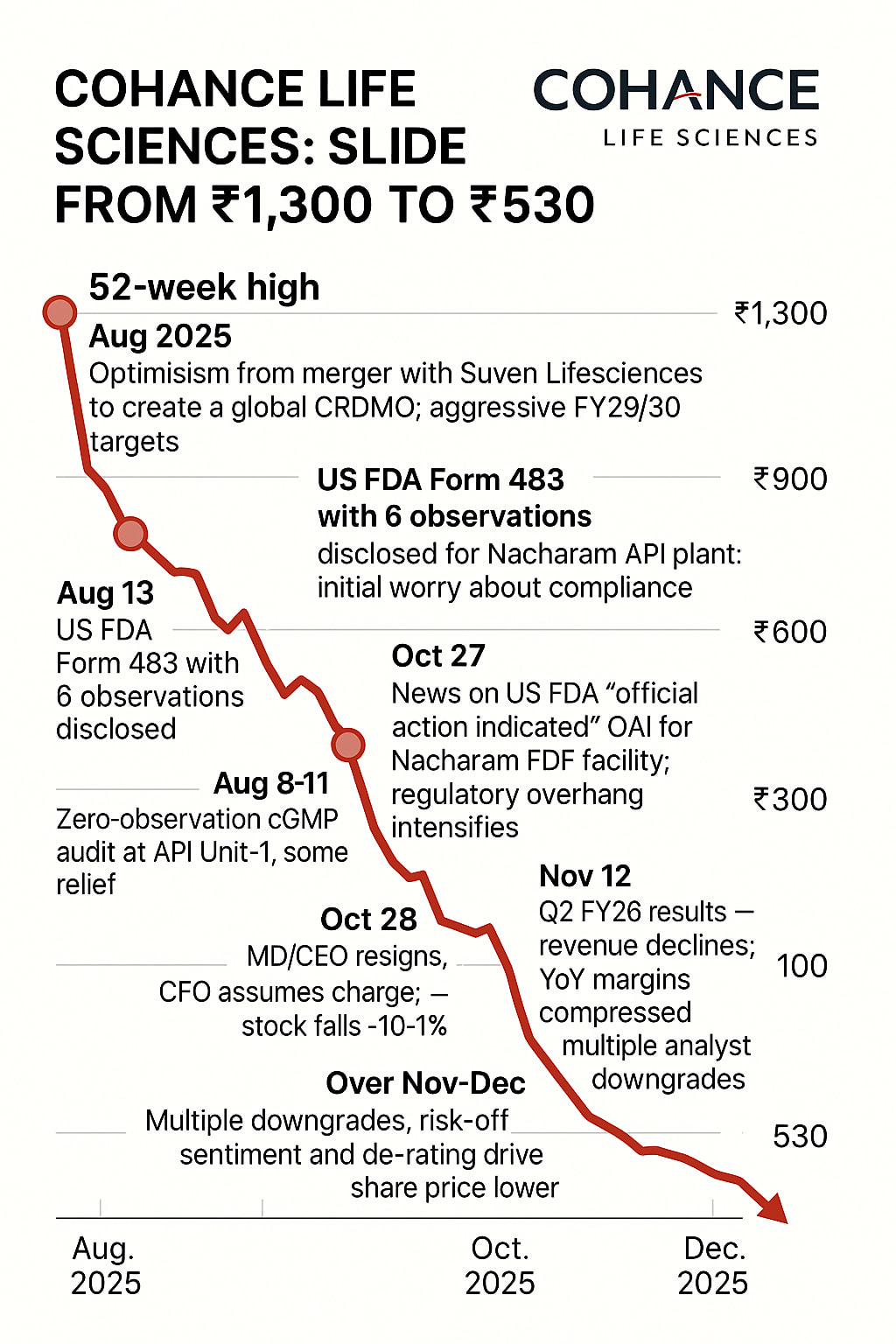

Despite all these cutting-edge capabilities the stock price has been moving South wards since the merger took shape. Below infographic shows the events that are part of the reason for the sharp correction to the prices.

THESIS

o The market seems to be over reacting to temporary blip due to the merger. Since the merger of 2 large entities take shape (Which in itself is a combination of several big entities in their own right), it normally takes time to settle down and for the synergies to take effect.

o The reasons for slowdown in revenue and drop in margins are due to destocking, funding winter for biotech and timing related shipment deferrals. These are not structural in nature and should turnaround.

o The management has reiterated the vision of clocking 1 bn $ revenue by FY 29 (Current revenue is C. Rs 2500 cr v/s FY 29 plan of Rs 8500 cr).

o The management has guided for flat revenues with higher margins for FY 26. For that to happen H2 FY 26 has to be significantly better than H1 FY 26.

o The combined Cohance + Suven entity is currently trading at the market cap of equal or lesser than Suven Pharma (which had c. 35% of combined entities revenue).

Based on the capabilities and the ambitious growth targets of c. 28% CAGR revenues till FY30 I believe the current price drop is a good opportunity to accumulate the stock for the patient investor. This thesis might take time to fructify as the management has indicated benign growth in the next couple of quarters. But we believe if one has a 3-year view then at the current levels this business should give double in 3 years.

Disclosure: I am invested in Kaynes (CMP below my avg purchase price ) and evaluating Cohance for investment.