With the high amount of cash that the company is generating, what could be potential areas which the company could target for potential acquisitions (backward integration, forward integration or perhaps new chemistry altogether - another chemical which they can sell along with TiO2 for paints? Biopesticides, seeds, branded agro formulation, etc?

TiO2 downward price trends continues. Plus side is raw material (sulphur pricess which MOL follows and is more cost effective) is also down.

Per the concall, they need 2 mths to stabilize plant. How quickly will prices revive is the question? Note that article says that Chemours (a large player) declined production and APAC was exporting (reference China is the largest manufacturer).

MOL might also have to lower its prices to gain market share and introduce new product vis-a-vis imported product from China. If anyone has insights on its cost of production (is its technology superior than China and thereby being cost down?), pls share. Concalls do not have any mention except that MOL is not backward integrated in TiO2 which tells me that cost can be higher in comparison to existing players who are

3 Likes

How you are sure that meghmani will deliver on the quality front of TiO2? In my opinion, demand and supply scenario will be second. First and foremost is about quality of TiO2.

Disclosure: Invested before demerger @ 60 rupees and buyed in small amount recently.

Recent management interview (link)

31.03.2023 ET Swadesh

- Pigment: Prices have stabilized in Q4 (vs Q3), utilization has increased from 30% to 50%. Also seeing improvement in end product prices

- Agrichemical margins will be maintained as raw material costs have softened. Currently global demand is facing contraction (operating at 75-80% utilization due to diversified global presence)

- Newly commissioned agchem MPP plant will be ramped to 50% in FY24, evaluating next phase of expansion and will be announced depending on demand recovery in global markets

- March 2024: will commercialize nano urea (hoping for 50% utilization in first year)

- Projecting 15-20% growth run rate in next 3 years

Disclosure: Not invested (no transactions in last-30 days)

10 Likes

FY23Q4 concall notes

- Pigment: Low demand + fall in realizations. Expect growth in pigment division in FY24 over FY23

- TiO2 plant with installed capacity of 16,500 MTPA is under trail run and expected to be stabilized in Q1FY24

- Muted demand in agchem sector continues in Q1FY24, RM prices have come down significantly. Hoping for revival in Q2FY24

- Agchem technical prices have come down 40-50%, but RM prices and logistic costs have also reduced significantly. Similar situation happened in 2008 period after China Olympics

2008 background

- Sales growth was muted in FY10 and revived in FY11, but margins only started reviving in FY12. So sales was flat for a year but it took 2-3 years for revival in profitability

- Volume growth in agchem sector will not translate into revenue growth for FY24. Hoping to see positives in Q2FY24

- MTM gain on receivables (76 cr.) shown in other income, MTM loss on foreign currency borrowing (-46 cr.) shown in finance cost

- Commenced manufacturing of Lambdacyhalothrin, Flubendamide and Beta Cyfluthrin, Cyfluthrin and Spiromesifen from the Multipurpose plant at Dahej catering to domestic and export markets. Will ramp up to 50% in first year, 65% in second year and 75% in third year of operations.

- Expect 650-700 cr. of revenues from this facility (no new incremental capex is required to achieve this)

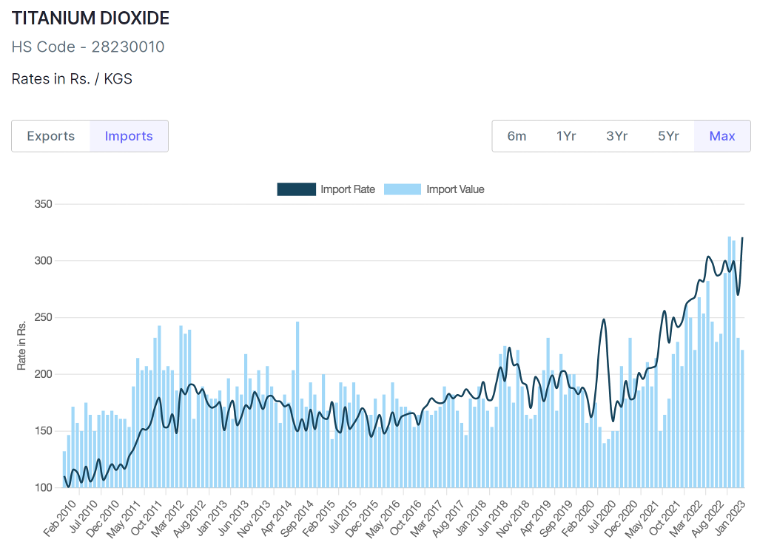

- TiO2 prices have started improving from 160 to 190+, ilmenite prices have gone down from 44-45 to 28

- TiO2: Will manufacture using Sulphate process and will have captive power plant. Not targeting medical grade TiO2. In good years, it can do 20%+ margins and should do 15-18% in average years

- Average cost of loans is around 3.5% (due to foreign currency loans)

- Current production of all agchem cos are lower to minimize high cost inventory

- $100mn agchem contract has already commenced, it will be equally distributed in 5-years, have all the required registrations

- Demerger will happen in 2-3 years once pigment division is normalized

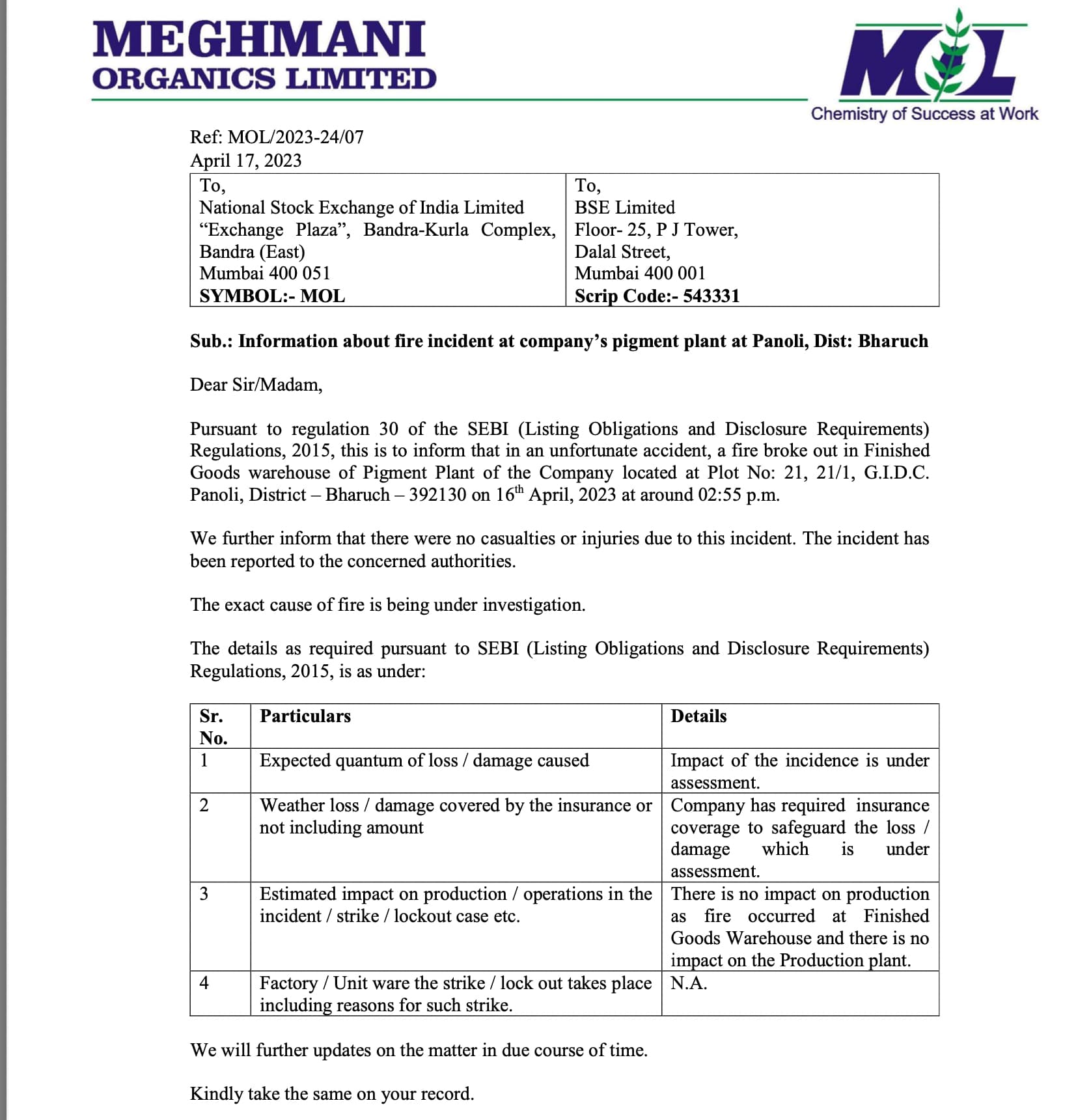

- Fire: Bringing in more automation to reduce such instances, management is seriously working on this to bring down such fire instances

Disclosure: Not invested (no transactions in last-30 days)

14 Likes

@harsh.beria93 Seeing lots of institutional interest showing up in this counter. Also slowly seeing volume build ups. Can we expect green shoots to emerge after Q2? or More visible growth can only be expected after Q4FY24?

Disclosure: Not having any exposure to this counter. Evaluating different value pick from Agro Chemicals due to tailwinds.

Happy Investing,

Karthik

FY24Q2

-

Agchem: lower realization, high channel inventory across the market. Prices have definitely bottomed out

-

Nano Urea and Titanium Dioxide will start contributing in FY25

-

TiO2: should achieve 12000 tonnes (75-80% utilization) and 225-250 cr. Margins are under pressure recently

-

Nano urea has not seen good adoption from farmers. Expect 17-19% margins

-

2,4-D price: $1.9-2; Bifenthrin price: $20; Lambda: $15-16

-

Capex

-

TiO2: Stabilization will finish in Q3, have spent 275 cr.

-

Captive power plant: have spent 100 cr. with 10-12 cr. more to be spent

-

Nano urea: Will commission in March 2024. Out of planned 150 cr., will invest 75 cr. by March 2024

-

Phase 2 of agchem MPP expansion has been put on hold

-

Maintenance capex is 10-15 cr.

-

-

Receivables have increased from 90-100 to 100-110 days

Disclosure: Not invested (no transactions in last-30 days)

3 Likes

Promoter buying in may 2023 and Feb 2023. Why is the promoter holding decreasing then?

1 Like

There is long history of fires, corporate misgovernance issues and I have put all such stocks in never buy category. One can still make money but all such are type of gamble stocks…

4 Likes

Anyone still tracking this? Promoters have repeatedly pointed out that the prices have bottomed out and that they see better days ahead.

1 Like

- Strong volume growth in both Crop Protection and Pigment segments in Q1 FY25

- Revenue remained flat at INR 411 crore, EBITDA increased by 194% YoY and 40% QoQ to INR 14 crore

- Profitability impacted by lower product price realization across markets

- Management expects price improvement and demand recovery to enhance profitability going forward

- Crop Protection segment revenue was INR 272 crore, EBITDA of INR 11.3 crore with 73% capacity utilization

- Pigment segment revenue was INR 138 crore, EBITDA of INR 9.4 crore with 45% capacity utilization

- Management is optimistic about regaining normal double-digit growth trajectory

- Focus on new product launches in Crop Nutrition segment to provide comprehensive solutions for farmers

- Inventory levels have become reasonable across most products after a period of destocking

- Received Responsible Care Accreditation for Crop Protection segment and Committed Badge from EcoVadis for sustainability efforts

- Launched 8 new products in Crop Nutrition segment during the quarter

- Demand recovery seen across both Crop Protection and Pigment segments

- Gradual price improvement expected going forward

- Focus on new product introductions and improving capacity utilization

- Headwinds: Lower product price realizations, volatile raw material prices

- Tailwinds: Improving demand, potential antidumping duty on Titanium Dioxide from China

- Launched 8 new products in Crop Nutrition segment

- Titanium Dioxide plant in Phase 1 running at 35% capacity utilization, expected to reach 70% in H2 FY25

- Nano Urea plant expected to run at 35-40% capacity utilization in the first year

- Potential antidumping duty on Titanium Dioxide imports from China expected in Q3 FY25

- Targeting 20% revenue growth this year and next year

- Expecting EBITDA margin of around 15% in the next financial year

- Confident about regaining normal double-digit growth trajectory

- Expect profitability to improve from Q2 onwards

- Focus on sweating the current asset base before considering further capacity expansions

- Debt reduction is a priority, targeting significant reduction in the next 2 years

- Question on demand recovery and pricing trends:

- Demand has started improving across both Crop Protection and Pigment segments, not just in one market. This is due to destocking of high inventories and improving market conditions.

- They expect gradual price improvement going forward as the demand picks up.

- Question on Brazil market and monsoon impact:

- Inventory levels have become reasonable in most products, and they expect good demand from Brazil due to the positive monsoon forecast.

- Question on product pricing:

- Prices have been at the bottom level but expect improvement as demand recovers, as the current pricing is not sustainable.

- Question on China behavior and freight challenges:

- Chinese prices are already at rock bottom levels and cannot go down further. They expect the freight challenges to normalize from Q3 onwards.

- Question on new product launches and their contribution:

*Launched 8 new products in the Crop Nutrition segment, which are relatively high-value and have better profitability. These new products will be a key focus area going forward. - Question on Pigment segment performance and capacity utilization:

- Focusing more on profitability rather than aggressive capacity utilization in the Pigment segment. They expect capacity utilization to improve gradually but not drastically.

- Question on Titanium Dioxide facility and its economics:

- Provided details on the Phase 1 capacity, revenue potential, and the expected 20% margins once the facility reaches 70% utilization, along with the potential benefit of the antidumping duty.

- Question on Nano Urea segment’s profitability and utilization:

- Expect 15-17% margins on Nano Urea and the plant is designed to be profitable even at 30-40% utilization in the initial years.

- Question on capital allocation and return thresholds:

- Typically target an IRR of 18-20% for new projects, but the dynamics have changed, and they are now more focused on sweating the existing assets before considering further expansions.

- Question on revenue and EBITDA guidance:

- Guided for 20% revenue growth this year and next year, and an EBITDA margin of around 15% in the next financial year.

2 Likes

The fire in Meghmani is back again like clockwork.

2 Likes

Key points for investors regarding Meghmani Organics Limited:

- Strong Financial Performance: The company has demonstrated robust growth, with revenue increasing 42% year-over-year (YoY) and 30% quarter-over-quarter (QoQ) in Q2 FY25. EBITDA also saw significant growth, rising 179% YoY and 190% QoQ.

- Growth Across Key Segments: Both the Crop Protection and Pigments divisions experienced healthy volume growth in Q2 FY25. Crop Protection, which constitutes ~75% of overall company revenue, reported a 50% YoY increase in revenue and a 75% YoY increase in EBITDA. Pigments, representing ~25% of company revenue, saw a 23% YoY rise in revenue and a 268% YoY jump in EBITDA.

- Strategic Investments Driving Future Growth: Meghmani Organics is investing strategically to fuel future growth. They have commissioned a multi-purpose product plant to manufacture high-value insecticides within the Crop Protection segment. They also entered the titanium dioxide (TiO2) market through the acquisition of Kilburn Chemicals Limited (KCL), positioning themselves in a high-growth sector with significant import substitution potential.

- Focus on Crop Nutrition: Meghmani Organics is expanding its presence in the Crop Nutrition sector, with the commissioning of a Nano Urea (liquid) fertilizer plant and the launch of eight new products in fertilizers, biostimulants, and micronutrients. This initiative presents an opportunity to capitalize on the growing demand for sustainable agricultural solutions in India.

- Global Footprint and Strong Market Position: Meghmani Organics has a well-established market presence, being the largest producer of copper phthalocyanine (CPC) blue and a leading integrated manufacturer of pesticides in India. Their reach extends to over 75 countries, demonstrating their global distribution capabilities.

Remember that investing in securities involves risks, and it is essential to conduct thorough research and consider personal investment goals before making any investment decisions.

1 Like

Meghmani Organics Limited - Q2 FY25

| Division | Revenue (INR Crores) | Revenue Growth (Y-o-Y) | Production Volume (Metric Tons) | Production Growth (Y-o-Y) | Capacity Utilization |

|---|---|---|---|---|---|

| Crop Protection | 397 | 50% | 11,473 | 38% | 84% |

| Pigment | 135 | 23% | 3,692 | 24% | 45% |

| Titanium Dioxide | Not Available | Not Available | Not Available | Not Available | 40% |

| Crop Nutrition | Not Available | Not Available | Not Available | Not Available | Not Available |

Key Financials (Q2 FY25 - Standalone Basis)

- Revenue: INR 532 Crores (42% growth year-over-year, 30% growth quarter-over-quarter)

- EBITDA: INR 41.2 Crores (179% growth year-over-year, 190% quarter-over-quarter)

- Net Profit: INR 8.6 Crores (compared to a loss of INR 3.6 crores in Q2 of the last fiscal year)

- Revenue Mix:

- Crop Protection: 75%

- Pigment Segment: 25%

Key Pointers

- Demand Recovery: The company is seeing a gradual recovery in demand in both the Crop Protection and Pigment segments. This is attributed to:

- Completion of channel inventory destocking.

- Gradual increase in demand.

- Anticipated Price Improvement: The management expects pricing to improve in the coming quarters. This is based on:

- Expectations that demand will continue to outpace supply.

- Decreasing logistics costs.

- New Product Launches: The company has introduced multiple new products in the last two years, including:

- Flonicamid

- Ethiprole

- Cyfluthrin

- Beta Cyfluthrin

- Dinotefuran

- Spiromesifen

- Flubendiamide

- Cyhalothrin

- Brazil Expansion: The company is establishing a subsidiary in Brazil to facilitate product registrations and expand their market reach in this significant market.

- Capacity Utilization:

- Crop Protection: 84% in Q2 FY25

- Pigment: 45% in Q2 FY25

- Titanium Dioxide: 40% in Q2 FY25

- Titanium Dioxide Performance: The performance of this division is uncertain and dependent on the imposition of anti-dumping duties on Chinese imports.

Future Outlook

- Return to Double-Digit Growth: The company anticipates regaining its historical double-digit growth trajectory based on its infrastructure, diverse product range, and market reach.

- Focus on Operational Efficiency: Management plans to focus on increasing capacity utilization and reducing debt in the near term to improve profitability.

- Limited Capital Expenditures: Meghmani Organics does not plan significant capital expenditures in the coming years.

Challenges

- Titanium Dioxide Uncertainties: The success of the TiO2 investment is heavily dependent on government action (anti-dumping duties). The management is exploring ways to improve efficiency and profitability even without these duties.

- Pigment Segment Competition: Managing competition from smaller players, potentially operating with lower costs, will be critical to improving margins in this segment.

3 Likes

Anyone studying this?

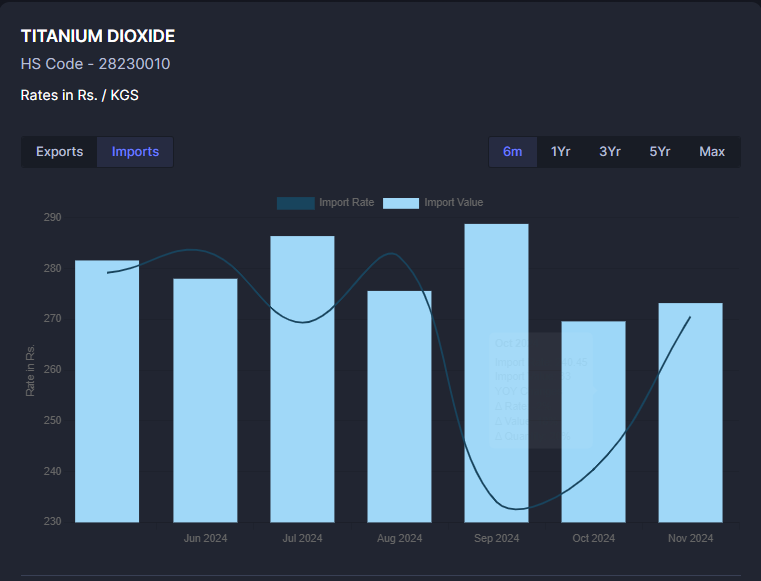

TiO2 pricing will improve after the import restrictions, and the core business seems to be improving too.

1 Like

- Yes, TiO2 pricing is improving. But keep watch on antidumping duty on TiO2 by indian government. If it is happening, then it will only be beneficial for Meghmani Organics.

- Right now, the Meghmani chart looks very negative. Hope there is no negative news for Meghmani

2 Likes

DGTR has recommended ADD, Link below.

India imposes ADD on imports of titanium dioxide from China - Fibre2Fashion.

3 Likes