Hello,

Meghmani Organics Lts. (MOL) is in to the business of manufacturing and marketing of pigments and pesticides. Product range is visibly good.

4 manufacturing plants located at Gujarat. Marketing team in 15 states which has been increased in 17 last year. More than 1000 stockist in India.

Warehouse located at Belgium, Uruguay, China, Russia, Germany, USA. Offices at Belgium, China and USA. More than 20 stockist overseas.

Overall they have 200+ customers of pigments and 90+ of pesticides.

Application of pigments: printing inks, plastics, rubber, paint, textile, leather, paper etc

Application of pesticides: Farming community, pest control, termites in wood etc

Promoters holding marginally increased from 50.36% to 50.67%

CMP 15.80, book value 21, EPS decreased drastically in last 5 years but doubled comparing to last year, D/E 0.68, Net profit has doubled from last year but almost 1/5th comparing 5 years.

Last year shifting of a plant took some toll on the production outcome, which has been successfully completed. All environmental norms has been fulfilled last year and this year they have announced to launch 3 more generic products and registration of new products in overseas market.

Company is technically very sound and has own R&D department. Management is well experienced.

Possible Risks: Adverse rain, Low awareness among farmers (as low as 30%)- positice sign as there is much room for market penetration, input cost (for this they have done some long term tie ups with the distributors), any policy change by govt. which will affect the currency. Apart from this major risk, according to me, is Genetically Modified (GM) seeds. I don’t know what is the new govt’s take on GM products but I am sure it will not be accepted by many and won’t happen anytime soon.

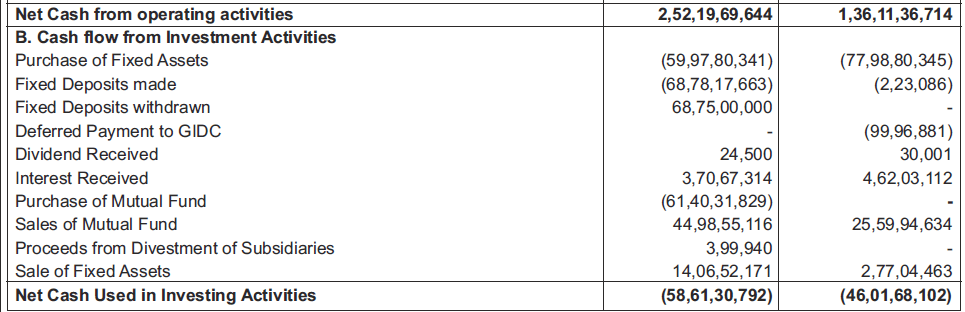

I request experts and seniors here to add their views and comment on the aspects of cash flow and balance sheet.