I am also curious why markets love MFL and treat MOL as an ugly duckling. MFL is also commodity Chem. It cannot be promoter history. Perhaps I am assuming MFL products have a less seasonal and more predictive perhaps domestic demand pattern. Perhaps something that imports cannot compete with. MOL has a higher export exposure, high agchem seasonality and mostly postpatent chemicals that may lose if China opens up.

Note that currently MOL AgChem is benefitting from seasonal tail winds, esp in the Americas. I am a shareholder in UPL and UPL is also showing the effects of these tailwinds (UPL has its own set of issues).

MOL agchem products are postpatent, I would love to hear from others what their moat is. MOL is bold

In pigments, titania was a bold move as an import substitution, enjoys demand predictability.

Agree, market is ignoring this company for quite some time, maybe because of past CG issues. TiO2 foray is not a small thing and the way india is progressing to become a major supplier of agrochem, company is rightly placed. I am expecting 900 Cr EBITDA by FY25 and basis the multiple one considers is fair for the company, the expected return can be quite handsome.

Per their CEO, they are confident that by 2025, they can achieve a top line of Rs 4,500 crore and the EBITDA is likely to be around Rs 765 crore and this compares to around Rs 2,500 crore run rate last year and a PAT figure of around Rs 170 crore.

I agree.

It seems to be periodic in the case of MOL.

Studied the con-call , the view from management is that everything is on track with some hiccups due to global events.

But events like these raise definite questions on the picture behind. Its so hard to analyse and get answers to these kind of situations. Its like a mental dilemma for me right now, on one hand i want to add to my investment and buy on dips but these kind of repetitive fire accidents raise a definite question.

@ayushmit : What is your view on the outstanding RPS of 198 Cr. The senior gentleman on the call asked very pertinent question on raising debt to finance capex while this money is not called yet even though MFL has been generating good cash.

Yes, it has been an overhang. I think it was an earlier arrangement and the loan was for 20 years which the management has reduced to 5 years. But I agree that this should be returned asap. And perhaps this is the reason why MOL trades at low valuations while MFL has been re-rated

Disc - I have a small allocation in Meghmani Organics, purely based on undervaluation and capex coming on stream.

One of the issues is capital allocation decision with TiO2 capex. Company will have 33K MT capacity at the capex of ~600cr.

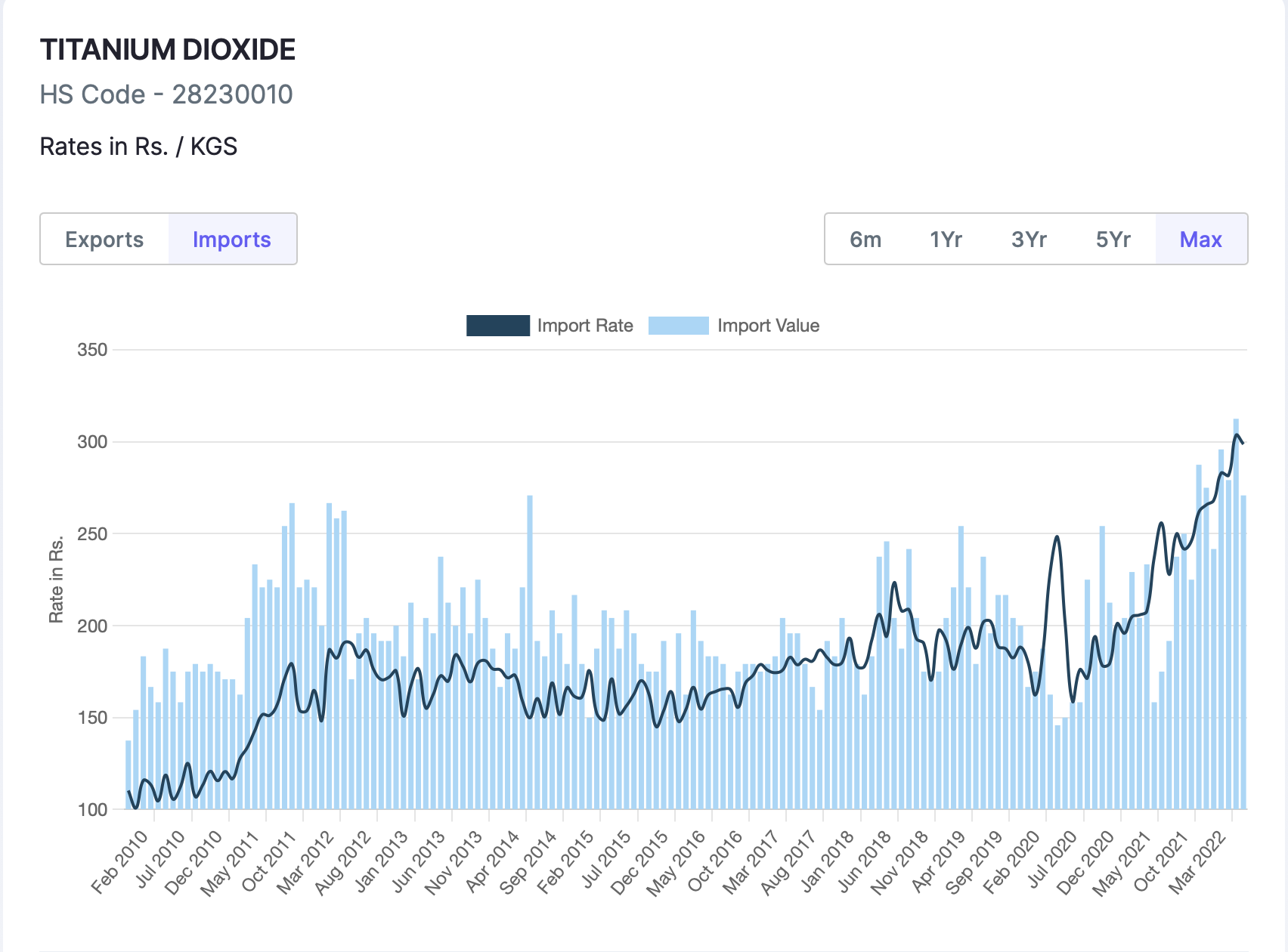

There are two grades ot TiO2 - anatese (lower grade) & rutile (higher grade). Following is realisation chart of TiO2 (rutile) grade. Long term average price of TiO2 is 200rs which went to 300rs in commodity upcycle. The prices are now correcting and they have settled at 240-250rs.

Anatese grade prices are 30-50rs lower than rutile grade prices.

At full CU, revenue of the company would be 33K * 250 * 1000 = 825cr. Assuming highly efficient net working capital cycle of 2 months, WC requirement would be 825cr/6 = 135cr.

Total capital employed - 600cr + 135cr = 735cr.

To get 15% ROCE, company has to make PBIT of - 110cr i.e. PBIT margins of 13-14%.

Assuming very less depreciation of 40cr, EBITDA of 150cr i.e. EBITDA margins of 18%.

If one wants to make 20% ROCE, required EBITDA margins are even higher.

If WC goes to 3 months, margins have to be higher.

Optimum CU will be 85-90% and not 100%.

Company will make anatese grade of TiO2 first which has lower realization and hence lower margins/ROCE.

Overall, it is quite clear that TiO2 will be a drag on capital efficiency and ramp up will be gradual. Eventually whether it will generate 18-20% ROCE is not yet fully settled.

Further, capacity in China is 46L MT and buyers for TiO2 will be 5-6 really large players who will try to extract as much purchasing discount as possible.

Some support in the form of PLI, ADD will help to make this business capital efficient. Otherwise, it remains a poor/average capital allocation decision.

1- Update

MCNL a wholly owned subsidiary has entered into a licensing agreement with one of leading domestic fertiliser manufacturer for producing Nano Urea (Liquid) Fertilizer by using their domestically developed patented Technology.

MNCL is expected to commence the commercial production by Q4 FY24. MNCL projects to achieve a top line of INR 1,000 crores on an annual basis.

2-Understanding on How is Nano Urea Different as Learned from Internet

On an average, a farmer in India applies two bags of urea in one acre per crop season, with the quantity varying slightly according to the crop. According to a press note from IFFCO, field trials have shown that a 500 ml bottle of nano urea can replace one bag of conventional urea as it has 40,000 ppm of nitrogen, which is equivalent nitrogen nutrient provided by one bag of conventional urea.

Mark the point that it’s being implemented in 100% subsidiary, so all the cost will be borne by MOL and then all of sudden something like MFL deal may happen and the public shareholders will again be wondering…

@rupeshtatiya Thanks for the thoughtfully done analysis, Rupesh ji. Just one doubt, you have calculated WC requirements on revenue. Shouldn’t this be done on Cost of goods and services?

Meghmani organic results are out. Pigment business significantly impacted and drags the bottom line.

Along with that significant jump in interest cost also impacts profits. This is now even more pertinent and again raise corp gov issue. On one hand MOL pays higher interest cost but does not recall loan given to MFL and MFL has announced dividend in this quarter. Very bad for MOL minority shareholders.

Since mr Ayush has attended the concall request him to shed some light on the other income and finance cost accounting they have spoken. They are saying 73 cr as gain ( shown in other income)and 38 cr ( shown as finance sort) loss both are as non realisable profit and loss on 9 month basis. Can ayushbhai pl throw some light on this

Listen concall but unable to understand why finance cost increased so much? Management is telling about Mark to market losses due to Euro strengthing and are notional losses. Can anybody help us to understand more clear picture.

Management has cleared the picture about Nano urea and TiO2. Investor fraternity is very much concern about quality of TiO2. Management is saying that they have hired old kilburn employees and have long experience in pigment manufacturing.

Given the current share price and future expansion and topline growth and complexity in Tio2 production, still confused to buy further.

Disclaimer: Holding @60 rupees pre demerger.

On the balance sheet front, the Company’s cash and cash equivalents stood at INR 77 crore, as on 31st December. The debt to equity ratio stood at 0.43 as on 31st December

Pigment business contributes nearly 25% of the revenue. Currently, the pigment business is witnessing slow export demand and contraction in the prices due to the challenging global macro environment. During the quarter, pigment performance has been adversely impacted due to liquidation of high cost inventory and exceptional loss due to the fire in the finished good warehouse. The Company has adequate insurance cover. We expect to recover in demand in pigment division in the next few quarters.

Not just for the 2,4D overall in the agrochemical division also, there has been reduction in most of the products and this is across globally all the chemical industry has been facing. If we talk particularly in the case of 2,4D then the average price is around nearly ₹225. As of now, it’s holding on what we believe that this the global condition has occurred because one of the factor was that China was facing the COVID situation. They were under kind of a lockdown. Now, the China has opened up and their consumption will also start rapidly at the same time, some of the global factors of Ukraine-Russia war has also impacted demand. Also, partly in Europe and US has a recession point of view. However, the things are going back to the normal. As for the global condition, that is what we feel. So, in the next few quarters, we believe that price should not go further below. In fact, it should start improving.

Nano Urea

India per acre, urea usage approximately one bag of 45 KG. Now, this nano urea is a patented technology developed by IFFCO, so only half a litre bottle is equivalent to 45 KG of bag.

So you can say it is just 1% volume will be equivalent to giving the same kind or rather better result in the one acre land. And the cost point of view to the farmer, it is cheaper to the farmer now this patented technology by IFFCO it is so efficient that it gives better result.

Nano urea does not has a single rupee subsidy. So, we are not talking about the conventional urea or we are not entering into any subsidy based fertilizer.

We are coming with Nano Urea and later on we’ll be adding some other crop nutrition products which is helpful to the farmer’s i.e., which uses less volume and it is more efficient.

At the same time, it is making a synergy with our agrochemical division. The customer base, the dealer distributor remains the same and there is always a demand for the better product. So it is a right moment for us.

At the same time, we have signed the agreement with IFFCO. So we are going to manufacture under the license of IFFCO patented technology. So it’s a proven technology.

the CapEx would be nearly INR 150 crore for this project and working capital requirement on the full year of operation basis would be about INR 200 crore.

The conventional urea bag costs around ₹265 to the farmer. Where on the same bag that is 45 KG bag on the same bag government gives the subsidy of close to ₹2,000. So, the farmer gets that product at hardly 10% cost, so there is a heavy subsidy cost on government at the same time this Nano Urea bottle which is only 500ML bottle that costs around ₹240 to the farmer. So it is even cheaper, 10% cheaper than the conventional Urea bag at the same time there is no subsidy on this product, so government is banking heavily on this product. There is a huge pressure from the government side to convert conventional urea into Nano Urea so that they reduce the subsidy loan. Which is INR 2,50,000 crore.

as far as the effectiveness at the farm level is concerned it gives better result than the conventional area, because conventional urea is hand broadcasted and it goes into the soil and gets absorbed by the plant through the root, whereas Nano Urea is a foliar spray application where the product is sprayed on the plant. So the plant absorbs directly by the leaves, so it gives much better result.

This quarter, the other income is INR 19 crore from forex, while MTM loss in interest is INR 38 crore. So during the quarter, there is INR 18 crore loss on the Foreign currency borrowings. But majority of the MTM is unrealized as we have long term borrowing, which are restated at the closing rate on last day of the quarter.

As on 31st December, we have around INR 260 crore of short term debt and while INR 430 crore is our long term debt. In KCL, we have spent so far INR 275 crore and we have taken debt of around INR 100 crore. MOL is foreign currency almost 90% plus, Kilburn is domestic INR terms.

In case of KCL, we have opted for 25% tax rate, while in MOL tax rate is 25% while in the new subsidiary this Meghmani Crop Nutrition, we will get the benefit of the lower tax rate of 15%.

titanium dioxide. Also with this kind of price, what is prevailing today. On the first phase, it should generate nearly INR 300 crore top line which is lower as per our expectation.

As far as the Agro is concerned, so we have already consumed the high cost inventory which was in Q2 FY23 and slightly it will be used in this Q4 FY23. So despite that so we are confident of maintaining the EBITDA margin in line with the current 18% to 19% in Agro division. In case of pigment division, which we had inventory of high cost and due to contraction in demand, there was some softening of the prices finished products also. So which has led to, you can say reduction into the EBITDA margin pigment division. We expect in the coming quarter this demand should start picking up and then there should be improvement in the EBITDA margins of pigment also.

going forward things should improve and we should be able to achieve this 14% EBITDA margin.

we hope that the thing should go back to the normal by the end of March and things should start improving from April onwards. So still one quarter will be little difficult from the pigment point of view particularly. But as far as the inventory loss is concerned, we don’t see much loss coming because of the prices going low and high price inventory.

due to fire. There is a loss of around INR 43 crore out of which INR 39 crore has been recognized as a claim receivable and only INR 4 crore as per the policy provisions where some deductibles are there. So to that extent of INR 4 crore has been accounted for as a loss.

So for the current plant, if we don’t consider the new plant, then in the case of agrochemical division, the utilization is about more than 75%, nearly 80%. In the case of pigment, it is little low, about 55% to 60%. And because we have added the new capacity in the agrochemical division. So which will take some time to again reach at 80%.

the 2,4D price is in the range of nearly ₹225 when it comes to the Cypermethrin, the prices is in the range of somewhere about ₹600 to ₹650. the 2,4D point of view, the prices is more or less in this line. In last three months when it comes to the Cypermethrin, yes there has been some pressure there. There is some reduction. From ₹650 to ₹700, it has come to ₹600 to ₹650. There has been reduction by ₹50.

the Agro chemical point of view, the first plant we have mentioned on the full year of operation basis it should generate revenue of nearly INR 650 crore. So we feel that in the next financial year the plant should generate about INR 300 to 350 crore kind of revenue from the new plant. In the case of titanium dioxide again. The full year of operation for the first phase would be the next year, where we feel that we should be able to generate nearly INR 200 crore plus kind of a revenue

Titanium Dioxide: we are going to ultimately produce rutile grade only. So as per our plan, first phase is. Going to be the Anatase and after one year the full capacity will be converted into rutile because we are doing the Capex for the Rutile grade in the second phase.