Incorporated in 2010, Megatherm Induction Limited manufactures induction heating and melting products using electrical induction such as induction melting furnaces and induction heating equipment.[1]

KEY POINTS [ edit ]

Business Profile [1] The company manufactures upstream and downstream equipment and machinery for steelworks, such as transformers, ladle refining furnaces, continuous casting machines, fume extraction systems, etc., as well as electric arc furnaces for the alloy and special steel industry.

Turnkey solutions [1] The company also offers turnkey solutions for steel plants, which include the planning, engineering, delivery, assembly, and commissioning of steel plants with its own or outsourced systems and machines, as well as customer service with maintenance contracts and spare parts business.

User Industries [1] Megatherm’s key market segments are Secondary steel producers that recycle scrap, primary steel producers that convert iron ore into sponge iron and then convert it into steel through induction melting, automotive suppliers, Ordnance factories and railroads, DI pipe manufacturers, and various engineering industries that produce critical parts in their casting, forging, and metal processing facilities.

Product Portfolio [2][3]

Induction melting furnace

Induction Billet Heaters

Induction Hardening & Heat-Treating Equipment

Induction Heating Power Source (Static Frequency Converter)

Transformer

Ladle Refining Furnace

Electric Arc Furnace

Continuous Casting Machine (CCM)

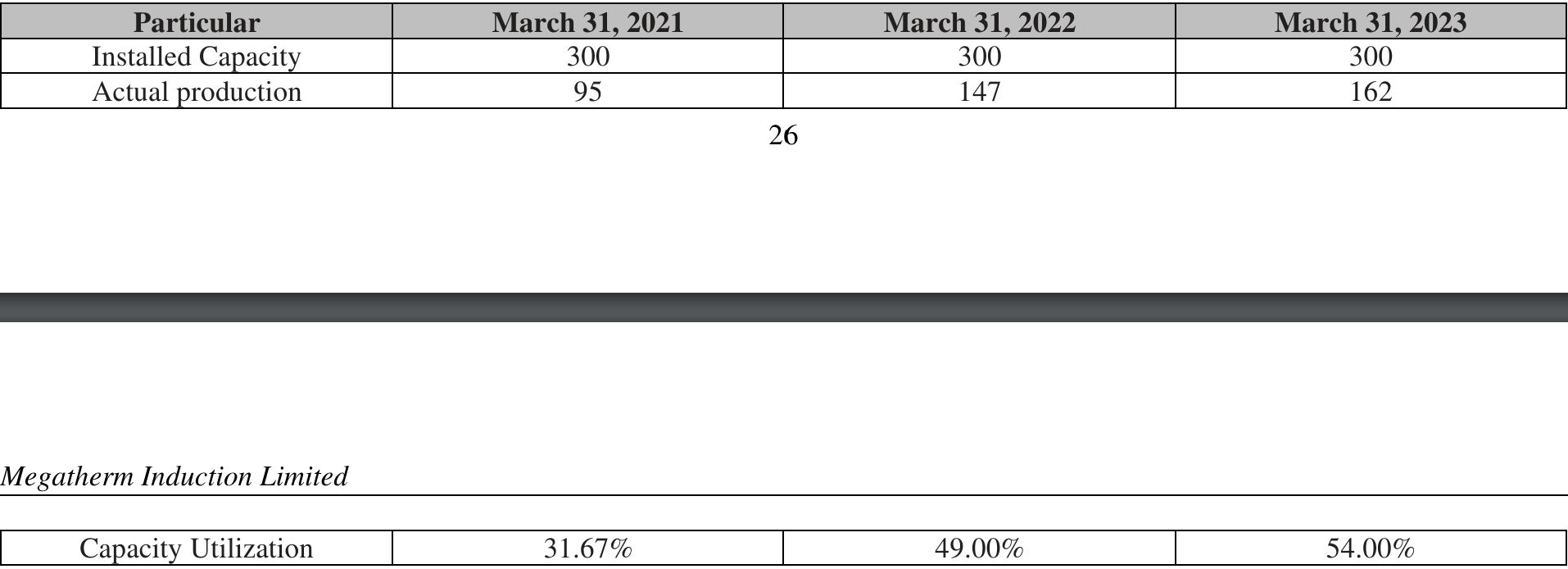

Manufacturing Facilities [2] Co’s Induction’s manufacturing unit is located in Kharagpur and has a production capacity of around 300 furnaces and transformers.

International Presence [4] The company exports products to South America, Africa, the Gulf region, Europe, SAARC, and Southeast Asia.

Geogrpahical Revenue Bifurcation [4]

Domestic - 74.5% in FY23 vs 80% in FY22

Exports - 25.5% in FY23 vs 20% in FY22

Employee Count [5] As of July 31, 2023, the company had 278 permanent employees.

Clientele [6] BHEL, Indian Railways, Tata

Motors, Mahindra, CESC, Hindalco, Sundaram Fasteners, MM Forging, Talbros Axles, Shyam Metalics, Sarda Energy, Rashmi Metaliks, Prakash Industries and others

Revenue Bifurcation Customer-wise [6]

Top 10 Customers - 42% in FY23 vs 31% in FY22

Strong Order Book [1]

As of December 31, 2023, we have an order book of approximately Rs. 280 Crs.

IPO Details [7]Co. intends to raise 53.9 Crs through the IPO which will be utilised for:

A) Funding capital expenditure

B) Working Capital requirements.

C) General Corporate Purpose.

| MEGATHERM INDUCTION LTD | SCREENER.IN | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Narration | Jan-00 | Jan-00 | Jan-00 | Jan-00 | Jan-00 | Jan-00 | Mar-20 | Mar-21 | Mar-22 | Mar-23 | Trailing | Best Case | Worst Case |

| Sales | - | - | - | - | - | - | 131.63 | 109.01 | 187.83 | 265.88 | - | 376.36 | 265.88 |

| Expenses | - | - | - | - | - | - | 115.94 | 95.85 | 179.26 | 238.33 | - | 343.40 | 265.88 |

| Operating Profit | - | - | - | - | - | - | 15.69 | 13.16 | 8.57 | 27.55 | - | 32.96 | - |

| Other Income | - | - | - | - | - | - | 0.57 | 0.26 | - | 0.55 | - | - | - |

| Depreciation | - | - | - | - | - | - | 2.28 | 2.10 | 2.06 | 2.43 | - | - | - |

| Interest | - | - | - | - | - | - | 5.92 | 7.06 | 4.99 | 5.84 | - | - | - |

| Profit before tax | - | - | - | - | - | - | 8.06 | 4.26 | 1.52 | 19.83 | - | 32.96 | - |

| Tax | - | - | - | - | - | - | 2.53 | 1.16 | 0.42 | 5.83 | - | 0% | 0% |

| Net profit | - | - | - | - | - | - | 5.53 | 3.09 | 1.10 | 14.00 | - | 32.96 | - |

| EPS | - | - | - | - | - | - | 6.06 | 3.38 | 1.19 | 15.16 | - | 17.49 | - |

| Price to earning | - | - | - | ||||||||||

| Price | - | - | - | - | - | - | - | - | - | - | 278.45 | - | - |

| RATIOS: | |||||||||||||

| Dividend Payout | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | |||

| OPM | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 11.92% | 12.07% | 4.56% | 10.36% | 0.00% | ||

| TRENDS: | 10 YEARS | 7 YEARS | 5 YEARS | 3 YEARS | RECENT | BEST | WORST | ||||||

| Sales Growth | 26.41% | 41.55% | 41.55% | 26.41% | |||||||||

| OPM | 9.36% | 9.36% | 9.36% | 8.76% | 0.00% | 8.76% | 0.00% | ||||||

| Price to Earning | - | - | - |

Risk -

-

Moderately large working capital requirement: The company had gross current assets (GCAs) of 164 days and inventory of 109 days as on March 31, 2023. Inventory primarily consists of work in progress (WIP). The working capital cycle is likely to remain moderately and hence, a key monitorable.

-

Susceptibility to volatility in raw-material prices and foreign exchange rate fluctuations apart from MIL’s presence in the cyclical capital goods industry: MIL is exposed to the risk of cyclicality inherent in the end-use industries such as metals and mining and the capital goods industry. New orders or repeat orders largely depend on the economic condition as the new or expansion projects by industries mainly depend on the level of expected economic growth. However, MIL has largely been able to insulate itself from the inherent cyclicality associated with the industry due to its presence in a niche segment and by catering to clients across diverse geographies (within as well as outside India) as well as due to good share of spare parts and service income at around 15-20% of its total sales

Disclosure - Invested