Dude I asked question on ROA. U have replied ROE.

I’m seeing huge red flags

Dude I asked question on ROA. U have replied ROE.

I’m seeing huge red flags

Dude ROA was calculated on Gross Block of assets. At least open the Balance Sheet before relying…So your depreciation point is invalid.

Btw…many people visited factory of Omkar also…we all know what happened to it.

I think I am balancing the discussion here by posting negative reviews. I see several red flags in this business and at this valuation and would seriously caution everyone to stay away

Well even this high ROA is fine, Meera is not the only company likewise. A micro cap with such excellent revenue growth, rented property can have such high ROA, I guess, though my experience and knowledge is limited in market. BTW, I think you should work to tone down while replying to others, that is not required in stock discussion. I seen you spreading negativity and attacking few investors here in VP. I think we can always avoid arguments/personal attacks here; sometimes it’s better to ignore. And as I said, you stay with the stocks you like and avoid the stocks you don’t. If company consistently post good numbers, investors will anyway chase the stock/price irrespective of what we discussed here in VP forum.

Guys I have a dumb question, what are the competators of this business. If they are increasing sales do they have any competation from china? All I can see from the photos present in their website is a bunch of motors and threads + spindle., Do they have any patients? Seeing such low volume feels scary to add the stock.

The machines are used to make carpets ? Correct me if I am wrong…

Meera is mainly into machinery in filament yarn sector, Technical textiles, carpets, stitch yarn (quilt yarn, footwear) are the major application segments.They also make machines which can make niche items like medical sutures, bandages, parachutes, nets, bullet proof jackets and harnesses.And their yarn mfg division is more to showcase their machine capabilities…but also runs as an independent profit centre.

I think their major competition is from European equipment manufacturers, but Meeras machines cost substantially lower than European machines. On the other hand European machine will have some higher automation. Meera operates in the gap between the costlier European (high end) machines and low cost low end machines. Asia africa Europe are major exports markets. USA unit also doing good, they have pacts with two companies for supplying machines for yarn twisting and winding process.

They should not have major competition from China. These are innovator products, some of them have been introduced for the first time. But I don’t think they have any patent. Regarding low volumes since the Stock is in SME segment and has a lot size of 500 qty retail participation is low, once it moves to mainboard volume may increase significantly.

Company makes machines for textile cos and itself owns very few machines. How does it manufacture these machines. What is the process. Where is iron and steel in inventory.

How can you manufacture machines without having a proper process plant of your own. Look at the fixed asset schedule of Meera.

Also you need inventory of oil, steel, consumables etc to make those machines (raw material). Where and how much do they own.

I have never suffered losses in any of the dud stocks you own, because I ask questions which u are conveniently ignoring. (Purposely)

Meanwhile Meera Industries secured new orders from three new countries.

China - NANTONG GOD OF HORSES THREAD CO.

Mexico - MURTRALEON, S.A. DE C.V.

Brazil - TNAX INDUSTRIA E COMERCIO DE CABOS SINETICOS LTDA

The company got entry in Chinese Textile Machinery market which is dominated mostly by western world, which is a very good development. They export to 26 Countries now.This will further strengthen Meera’s Brand Value worldwide.

Another set of great numbers from Meera.

h2fy19 (comparing with h2fy19, standalone)

Revenue ![]() 57 % from 1184 lacs to 1862lacs

57 % from 1184 lacs to 1862lacs

Ebitda ![]() 62% from 224 lacs to 364 lacs

62% from 224 lacs to 364 lacs

Ebitda margin ![]() …19.5% compared to 18.9% last year

…19.5% compared to 18.9% last year

Pat ![]() 63% from 150 lacs to 244 lacs

63% from 150 lacs to 244 lacs

Pat margin 13.1 % compared to 12.6%

Meera fy19 (consolidated, comparing with fy18)

Revenue ![]() 66 % from 2194 lacs to 3642 lacs

66 % from 2194 lacs to 3642 lacs

Ebitda ![]() 91% from 370 lacs to 709 lacs

91% from 370 lacs to 709 lacs

Ebitda margin ![]() from 16.8% to 19.4%

from 16.8% to 19.4%

Pat ![]() 99% from 247 lacs to 492 lacs

99% from 247 lacs to 492 lacs

Pat margin ![]() from 11.2% to 13.5%

from 11.2% to 13.5%

Consolidated eps…12.5

Meanwhile Meera bagged domestic order (from Creative Textile, a Leading Textile Group from Mumbai) of Rs. 1.68 crore. Too good, huge headroom for Meera to grow.

Long term loans and advances , inventory and short term loans is the place where red flag is occuring

Where is the provision for warranty. How many cos sell machines and do not provide warranty.

Try comparing this with other cos which make machines. Eg Praj

Meera is exhibiting it’s next generation models at World’s largest Textile Machine Exhibition to be held in ITMA 2019 at Barcelona, Spain between 20th - 26th June 2019.

https://www.textileassociationindia.org/meera-at-itma-2019/

ITMA is the trendsetting textile and garment technology platform where the industry converges every four years to explore fresh ideas, effective solutions and collaborative partnerships for business growth. Organised by ITMA Services, the upcoming ITMA will be held from 20 to 26 June 2019 in Barcelona at Fira De Barcelona, Gran Via.

There are numerous drawbacks/risks/open questions with investing in this stock. Here is a list:

Despite profits going up from 2.5 to 5 crores in FY 19, the Trailing 12-month P/E is around 20. Price to book value is around 7. This is expensive.

Over the last 2-3 years, we have already seen microcaps rally due to increased profits and P/E expansion, however, when profit growth tapers down, price reduces drastically taking TTM P/E to single digits. A price reduction of 50% at the least has been seen over the last few months in numerous stocks. The same might happen with Meera.

The case for Meera has numerous open questions. What products does their machine manufacturing division actually produce? What is the market size for these products? Who are the major players locally and abroad? Looks like Meera has hit a niche opportunity, what exactly is it? Why is it sustainable and why should it be considered a moat, how can it enable growth? Making statements like the following means nothing:

“Meera’s machines cost substantially lower than European machines. On the other hand European machine will have some higher automation. Meera operates in the gap between the costlier European (high end) machines and low cost low end machines”

I read that Meera either makes technical textiles or makes machines that can help make technical textiles. That is hard to believe. There is another company, Fiberweb that makes technical textiles: They have spent 20 crores for machinery that can manufacture spun bond textiles, 20 crores for melt blown textiles and another 50+ crores for flat bond fabrics. While Fiberweb is a poor quality stock riddled with corporate governance concerns, the numbers spent on machinery cannot be far off from truth. Meera has net assets of 4 odd crores, what does it exactly do with respect to technical textiles?

Why do Meera’s machines cost lower? Is it because of low cost labour? Is it labour intensive ? If yes, how so? Material cost should not differ substantially between countries, so where is the competitive advantage?

While profits have doubled year over year, cash has not, because the incremental cash generated has gone towards increased working capital requirements (more inventory on books). Hypothetically, if Meera wants to expand, how will it fund expansion?

Let’s assume that profits double from 5 crores to 10 crores next year. P/E for today’s price as of next year will be 10. Can Meera grow from there? If not, expect a rapid correction in price. Today’s price is still expensive.

Look at the price and volume charts for a moment, around why timing is so important in illiquid stocks like Meera.

The stock was clearly manipulated upwards to around 400 in Feb 2018. (At around 400, a 2.5 crore profit (as of March 2018) generating company was valued at around 150 crores). Volumes were much higher as the stock price was going up. Retailers usually get attracted to rapid price increases with high volumes and high delivery rates. This is easily achieved by operators who buy and sell amongst themselves raising prices and delivery rates. Post the peak, stock hits daily lower circuits with abysmal volumes and within days, stock has lost 50% + from the peak. Even if one wanted to sell, one could not till a 40% drawdown occurred. This is not a good situation to be in. If one wants to park their money here, do get the entry/exit points right.

Also, why would anyone want to invest in stocks that are sub 100 crores in market cap and overpriced plus illiquid, when you have numerous midcaps and small caps that have corrected severely, and which can offer very good returns even in the short term? Even the bluest of the blue chips like Tech Mahindra can also give decent appreciation (plus dividends and buybacks), so the case for risky investments is not strong.

Finally with respect to technicals: The stock has consolidated between 175-225 for the last year. That could just be the operator accumulating stocks. So, an uptrend to 300-350 is not ruled out. But that will make the stock even more expensive and increase the risk of (not) being able to bail out on time.

On an unrelated note (not related to Meera), there are just 2 reasons for investing in a micro/nano cap, according to me: a) You get a very low price (Heads I win, Tails I do not lose much kind of a situation) while technicals support and you understand the dynamics behind potential future revenue growth. b) You know the promoters personally very well and can vouch for their integrity and competence (Integrity first priority and competence next). But then again, that’s just me.

Upcoming FPO

Hey guys,

I am a small individual investor and I am really interested in this company but I don’t own any shares due to the lot size and minimum investment. I am thinking of attending the AGM and meeting the management before I invest. Does anyone have a suggestion as to how how I can attend the company’s AGM without being a shareholder? I tried writing to the CS of the company but she hasn’t responded yet and it has been a week. Is there anyone here who owns shares in this company and is not going to the AGM willing to make me their proxy?

Thanks!

The concern raised about honesty of the promoter looks to be genuine as they have dumped around 10% of shares in open market to retail investor when share prices has gone up after IPO. I would have understand if they would have sold to some institution FPI or MF.

Story looks interesting but only if you can keep close watch on promoter because most of the Indian Promoters are chor in the beginning but talks about business ethics once become big.

Disc: Not invested.

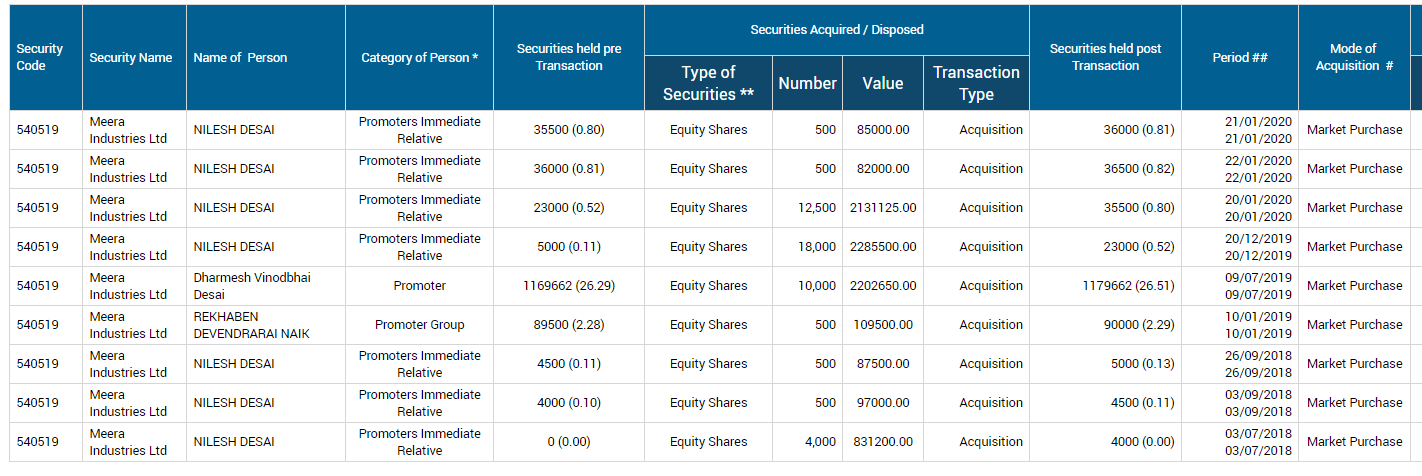

![]() where do you see the dumping?

where do you see the dumping?

Promoter was holding 27,94,500 shares during IPO (Apr-2017), and now holding 28,28,000 (as per Dec 2019 shareholding).

And in between there are only acquisitions as below;-

Promoter shareholding over past 4 qtrs are below;-

Q4fy19 28,00,000

Q1fy20 28,00,000

Q2fy20 28,10,000

Q3fy20 28,28,000

![]()

![]() Where are you seeing dumping in open market to retail investor?

Where are you seeing dumping in open market to retail investor?

Incorrect information!

Yes! You are correct. I didn’t notice this thing.

But promoter shareholding which was around 73% in March 19 has gone down to 63% in Dec. 19.

Maybe they have issued some preferential share around 5 Lakhs or so? Any idea, why they have done so and what impact it will have on minority shareholders?

Thanks!

I have small doubt to clarify:-

Erection commissioning of a machine to be done by M/s. Meera or customer. If done by Meera what would be the cost of E&C charges.

Commissioning charges payable after completion of E&C or in advance?.

Spares: What would be the revenues from spares parts. Is there any chance that Customer may purchase from other source?. How frequent spare orders placed on M/s. Meera?.

What is the time period bank guarantees lying with customers ? is this till expiry of warranty ?.

4.What percentage of penalty levied on late supply of items and E&C by customers?

Here is the Meera FPO doc, from last year;-

https://www.chittorgarh.com/ipo_basis_of_allotment/meera-industries-fpo/994/