PS: not my intention to attack anyone or their opinion. You have your right to your opinion just as I do to mine.

Yes this pattern of posting negative opinions just after results is an observable pattern; not all SME companies are bogus; if we make allegations lets substantiate that with proof; u can’t make an allegation and ask the other party to prove that they are innocent; the one making allegations will have to provide proof that the other party is guilty so as to substantiate what they are claiming; and if truth comes out , well isn’t it good for everyone?

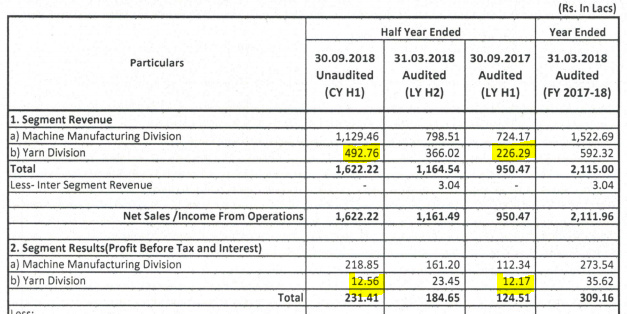

@MSSMurthy@thestocklady : I looked through the HY report and the numbers look good. Since you both have been tracking this for sometime, i had quick question around yarn division margins. If you see the screenshot below, the revenues for yearn division doubled 100% but the PBT numbers remains same and profit margin seem to be reduced by 50% .

The yarn division has been started primarily to demonstrate the functioning of the machinery to the buyers since the machinery involves modified technology developed in house and varies from the traditionally designed machines .This division in situated in th same premises Where the machinery is fabricated. So I think the economics of this division may not be viewed from the angle of a full pledged yarn manufacturing unit . This is my layman’s view.Any body more acquainted with yarn manufacturing business may please opine on this.

@MSSMurthy- Thank you for taking time and sharing your thoughts. Let me first apologize for not replying sooner due to a personal health emergency.

My thoughts on the yarn business are- Even if the yarn business was supposed to be a demonstration division, it is commanding nearly 30% of overall revenue. Any portion of the business that contributes so significantly to topline should be looked as a profit generation division. Playing devils’ advocate, this is a division which can slowly turn from profitable to negative and suddenly we will be staring at losses and some cooking of books. Nevertheless, i am optimistic about the company and its promoter and will keep tracking it until the next results are out. Unless, there is corporate governance issue, this can hopefully become a decent size player with good returns for all investors.

Meera Industries has announced regarding securing orders amounting to USD 130000 from three new countries adding to a total of 23 countries for its twisting machines . Achievement indeed for a micro enterprise .On the existing base of sales registered for FY2018 being Rs 21 crores this order seems to be significant . Watching the developments with interest.

Asset turnover ratios of many other manufacturing companies , for instance Symphony Ltd is as high as 10 as against the figure of 7 obtaining for Meera Industries . Don’t you think such a high ratio is an indication of the healthy demand for the innovative products of Meera whose details are available on the website of that company.While I note your view that the numbers of Meera cannot be trusted , I am optimistic on the ability of the company to deliver which would be relatively easier from the present small base . I continue to hold.

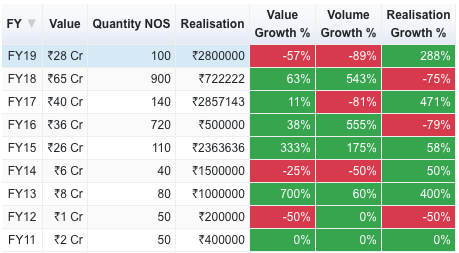

Meera’s topline has grown alongside yarn twisting machine exports. Looks like the market was good for this between FY14-FY18 but FY19 looks to be showing a slowdown (its 6 month data though).

I think this is a small market that wont attract big players and it is sort of believable why they could be exporting these machines to developed nations. The low asset base as well I can live with, because I think this is more material and labour intensive than fixed-asset intensive. These must be indigenous machinery but nothing that would have a strong IP and hence a big pricing power. However, the valuations here are very high and if we annualise FY19 numbers so far, there might be a drop in topline in FY19 which will be a risk for investing here.

Disc: No Interest

Symphony is a branded play. They outsource manufacturing which is why their asset turns are high. In Meera’s case, going by their margins I wouldn’t compare asset turns of these two simply because their margins aren’t comparable.

Announcement to BSE to the effect that the company is acquiring land adjoining the existing premises for expansion , and proposal for raising funds for the acquisition .

Just saw your post.I am invested in Meera based on what I perceive about the company .Monitoring the same and continue to contribute here as and when I see any new developments. I don’t see any ‘ operator ‘ here , either some body who want to jack up or any person with vested interest to bring down the stock in any artificial manner in order to corner . If you have specific information if somebody creating volumes in the stock kindly furnish the details on the forum for benefit of members . In the mean time let us continue discuss with facts and perceptions rather than implications which I feel is not fair. As for MRSS I am not able to comment as I am not tracking that company nor invested in that.