Just found out about this stock while using screener. Crazy stats in Roe/roce/sales growth/profits and no debt. Is there any particular reason why this stock has not consistently gone up considering they’ve always posted good results? Am I missing something here?

here are the latest numbers:

Trying to go deep dive in to it. Very limited info.

Disc : Not invested.

Tried to have a look in to the previous year AR. Few points which I may consider as red flag :

FY 18-19 : Travel expense (consolidated) Rs 3.9 Cr on a revenue of Rs 35.5 Cr. (approx. 11%)

FY 17-18 : Travel expense of Rs 1.75 Cr on a revenue of Rs 21 Cr. (almost 8%)

Any growing company would have a spend of max out 7-8 %.

(I have a travel startup which is in to Corporate Travel).

Even a company like Honeywell India which uses its Intl standards & spend as per Intl guidelines have 7-8% of travel spend. A well settled company would have less than 5% of travel spend (most Indian IT co’s have around that). IT co’s are one of those travel massively for their projects.

Hypothetical situation : With an employee base of 100, if they have 20% travellers (this is again very high side).

Per employee spend comes at approx. 20 lakhs per annum.

My Concern : Are these guys using 5* hotels & Presidential suites to stay.

Are these guys flying Pvt Jets or only business/first class & using exclusive lounges.

Some thing is not right.

KMP Salary of more than 50 lacs.

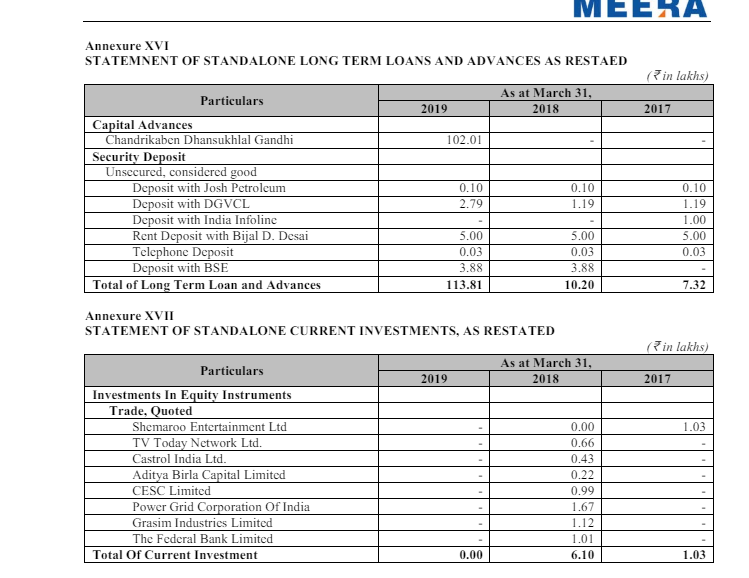

Unsecured loan given amounting to Rs 10,201,000

Previous year AR talks about Audi worth more than Rs 32 lac.

I am keenly waiting for this years AR. Would like to see on profit of Rs 52 lacs in FY 19-20. What is :

- KMP Salary

- Travel Spend

- Status of unsecured loan.

Disc : Not invested. But Interested  .

.

2 Likes

In last 5 months, the company received orders of around 14 Cr.

June 14th – $159,000

May 11th – Rs 1,91,00,000

Apr 26th – Rs 3,45,00,000

Apr 2nd – $114,100

March 8th – $180,000

Jan 27th – ₹2,95,00,000

Jan 19th – $171,000 and ₹94,00,000

1 Like

Anyone who attended the AGM today; if so you share the notes? (or if the video link is still live on youtube or anywhere)?

Does anyone have update on the potential of this Value addition.

3 Likes

I think the SOP - Standard Operating procedure is mainly for client side Operators, for better operation and for error free assemble of machines/installation. Around 6 months back, I tried to speak with Meera USA management and after a very brief call what I concluded that many midsize local/north American customers are holding up their orders because of the pandemic and shortage of trained technicians to install/assemble Meera machines.

We have already seen an export Order of USD $136,000.00 from USA in this month –

In their Corporate announcement/ as per this Announcement of Order Receipt document – The use of eco-friendly products has become increasingly popular since global warming is a concern of many. MEERA is successfully making inroads into this market with its upgraded version of twisting and winding machines.

1 Like

From the Annual Report –

Along with many minor developments, we can categorically say that, we developed two new major products which can be marked as a major milestone. They are -

- CT-260 Cabler / Twister with Individual Tape Drive System for BCF Carpet Segment.

- DTX-300 Twister with Precision winding for Technical Textile Segment.

And lately with the development of new models like CT-260, DTX-300, TPRX-50, AWX-250, we are gradually winning the confidence of big guys in this segment.

1 Like

Any one from the thread active on Meera Industries, looks like at multi year low , would like to know any fundamental trigger!

With the textile industry down the gutter and the inactivity of this thread, decided to give this a look and looks like the past conversations have been heavily biased by the stock price and the member’s orientation(contra vs momentum). Here are my two cents:

I started tracking this when they amended their object clause to include business of machines related to cast polypropylene films, PVC pipes/films etc and then my interest was further piqued when they disclosed that they have 4cr of assets allocated towards the Plastics division in 4Q24 results with no revenue or profits from it just yet.

This is incorrect. It’s 3.9 million and 1.7 million rupees respectively which 39L,17L.

If at all any concerns should’ve arisen, it would’ve been the exhibition expenses(which was 1.08cr in FY20). However, the company singles out exhibitions as a key pillar of their marketing strategy and hence differentiation. In 2019, they had attended four different expos from China to Germany. This expense has been in line with the number, type, duration and location of expos over the last few years. eg. It is 33L in FY23.

In picocaps like these, promoters are extremely high leverage people with involvement in operations at a much deeper level and hence their remuneration shouldn’t be compared with those of relatively mature, larger, institutionalised cos.

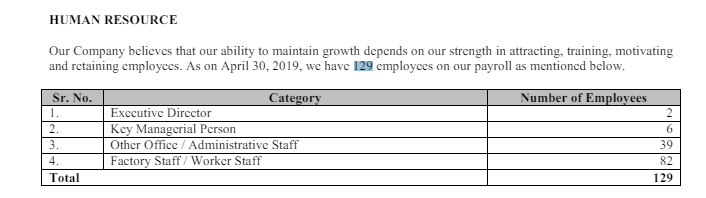

eg. employee distribution in 2019

And I’m considering a portion of the rent that’s being paid to Mrs. Desai as a part of remuneration.

If you’ve worked a knowledge job, you’d understand Price’s square root law and that if you want more output, you shouldn’t hire more. You should pay your best people more.

This was given to a certain Mrs.Gandhi for acquisition of Land for expansion. The item was no longer on the balance sheet post acquisition.

I would like to see a promoter who is focused, ambitious,well-incentivised and competent rather than robotically applying “red flag filters” like having an Audi. (PS: They have a Ford Ecosport too)

Mr. Dharmesh Desai does not have any meaningful businesses outside this. Also, I LOVE that the only other directorship the promoter holds shows his passion for the game which other valuepickr members have described.

Mrs. Desai doesn’t seem to have massive conflicts of interest either.

The promoter has undoubtedly involved in activities that aren’t ideal, like:

- talking up the stock price in ARs

- not ideal remuneration levels

- could be more transparent with remuneration instead of taking extra money via rent

- Having expensive cars on the BS

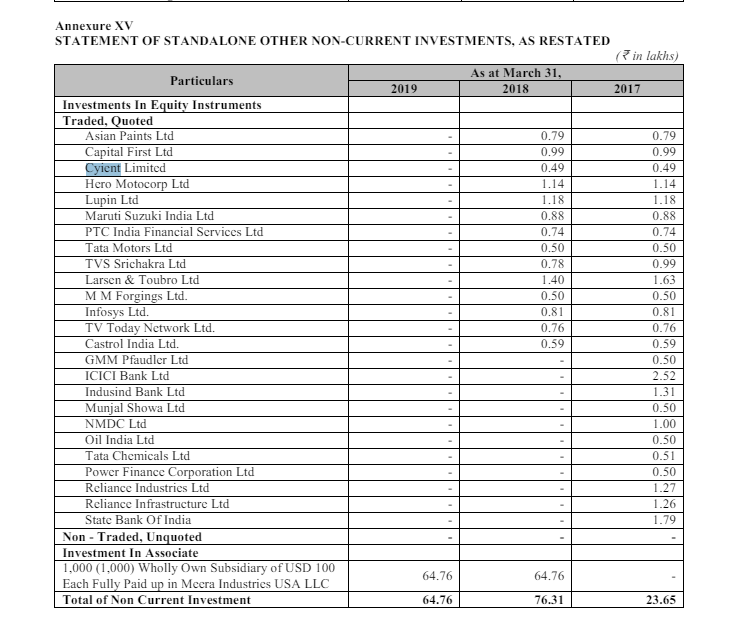

- Buying stocks suddenly at/near the top on the balance sheet (FWIW, they didn’t buy shitcos, sold out in time and probably even made some money lol)

I see the promoter as being a little immature/ “not public market trained” instead of as red flags.

For some others who posed the question, “where are the machines that make the machines?”, I’m not an expert but I’d say that IP-led manufacturing would be different from low value mfg.

I compared the gross and net carrying values of plant and machinery relative to sales for textile machinery peers like Lakshmi Auto Loom Works, LMW(both are mentioned as peers in the prospectus), Stovec industries- an MNC, and Rajoo engineers - another machine manufacturer(Meera could be a future peer if they make CPP extrusion machines in that new plastic division) and the numbers were similar across the board.

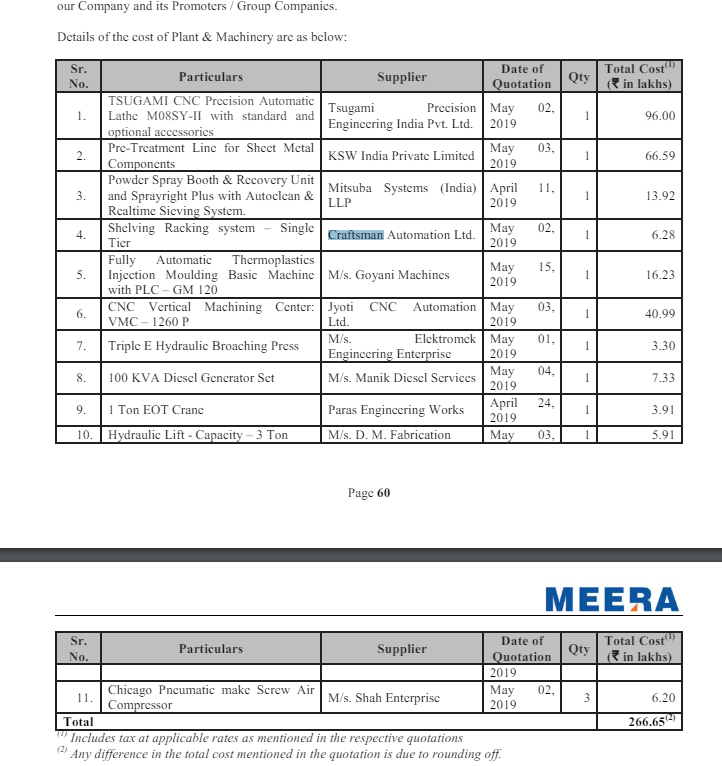

They’ve specified their entire list of machines and other assets somewhere too. I’m not able to find it right now. People really skeptical can use this list to research further.

Lack of industry knowledge hasn’t allowed me to fully understand their capabilities and source of differentiation independently.

European players like Galan from Spain seemed to have better specs for their machines but that would be irrelevant if Meera wants to be the Zoho of this industry.

So, based on management’s detailing of new products developed etc, they seem to have developed significant capabilities. The employee count has risen to 150 in FY23.

I tried to use the HScode for their products(8445) to see if they have maintained a consistent marketshare in exports but that doesn’t seem wise either since in an industry like this, orders would be volatile and highly susceptible to the end customer’s financial position, especially if these machines are customised(since units sold per year is very low).

Their customers seem to have a good mix of repeat ones and with good reputation.

eg. SRF had been a repeat customer. First it placed order of 1.91cr in May 21 and then a massive 5.7cr order in Jun 23(both for ring twisters)

TL;DR:

Overall, I see a focused, passionate, ambitious, well-incentivised and probably moderately competent promoter in a company which has built significant capabilities over the years but have nothing to show for it in terms of stock price over the last 6 years, probably due to the vagaries of the end user industry. The management seems to want to address this too by entering into the plastic machinery industry, which made me interested in the first place. Expectations for this stock seem to be very low due to lack of stock price driven investor enthusiasm and misplaced cynicism. Hence, this could be the subject of a massive delta in expectations even for moderately good execution.

Welcome pushback. If you find this deluded, I will not be selling what I’m smoking right now.

Disclosure: Invested, transactions in the last 30 days

3 Likes

Meera Industries just declared a dividend of ₹0.5 per share to non-promoter shareholders.

I see this action as a HUGE vote in favor of my above hypothesis.

Strong revenue and profit growth YoY with the plastic division yet to contribute.

Looking forward to the AR to learn more about said division.

3 Likes