Do you have any source for this ? I didn’t find it anywhere in DRHP also. Although by doing that they made a killing trade

@AmitContrarian Search for credit rating of both entities, you will see the fact that both these enties are just holding entities without any other business and it also has debt.

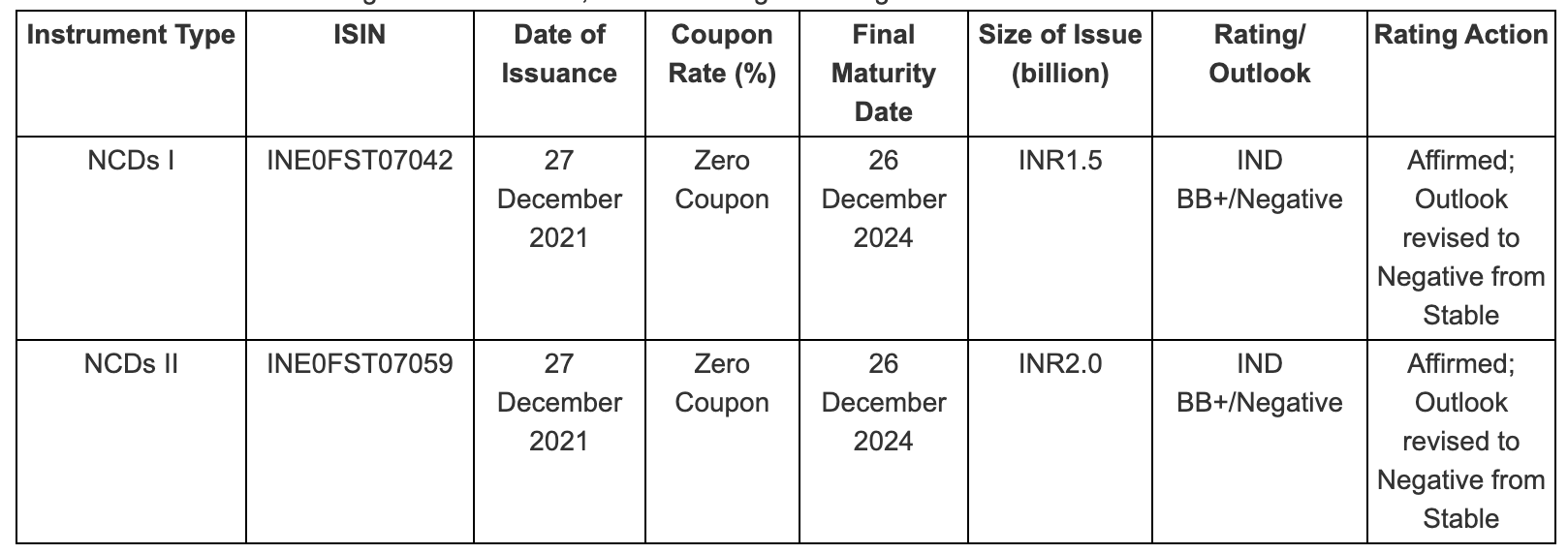

https://www.indiaratings.co.in/pressrelease/67742

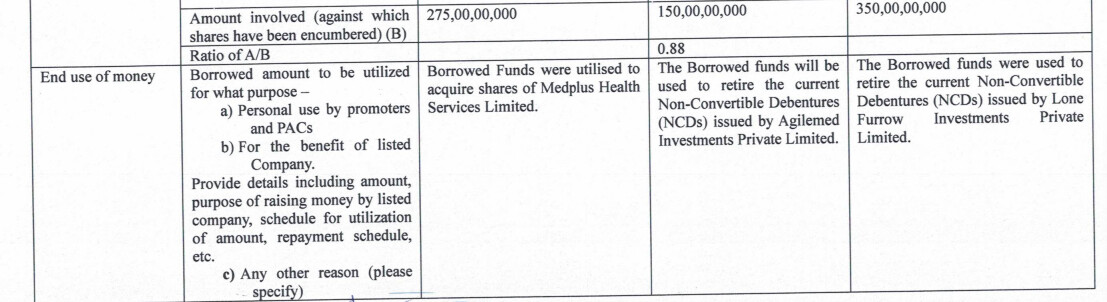

In this attached doc, you can find they issued some NCDs in 2021 to acquire the shares of Medplus

https://nsearchives.nseindia.com/corporate/spect_sandeshc_21122023134533_disc1.pdf

1 Like

Thanks , These are zero coupon ncds means they will have to keep re-financing it depending on price of stock either pledge more or un-pledge it. ( i don’t know how long they could do so) Crazy gambling by promoters.

As we can see Maturity is happening on Dec 2024, they will have to pay interest over it either by selling stocks or by issuing new NCDs by pledging more of stocks. They have been selling recently … To re-pay the debt they have to sell atleast 300 to 600 Cr (not sure how much debt is on these companies) worth of shares which is about 5 to 10 % of the company at current Mcap.

Also point to be noted is Agilemed Investments Private Limited defaulted in coupon payment in 2022 of total debt 275 Cr.

There are other promoter entities we don’t know how much of debt is there too.

3 Likes

I was reading about this company recently and just went about a background check on the promoter and the company through publicly available information. There is not too much out there but from what little I could gather we can see some points on how the company and the promoter has evolved from 2006 when the first stores came up

Promoter

The promoter has invested in other verticals in the past as well. In 2008 he had a failed start in apparel retail. In 2011 he launched something similar to Nykaa in online beauty retail. In 2014 he launched a venture in online furnishing space after raising funds from multiple investors. He comes off as a serial entrepreneur who wants to build businesses and then sell at a higher valuation considering one person cannot manage so many entities.

The business model has not grown with one model. Earlier in 2016 they were open to giving franchisees. In fact in one interview the promoter mentions that the franchise route will help them scale up to 10000 stores by 2019. This was in 2016. However by 2021 they had decided that they will open their own stores and were closing down the remaining franchisee as well post the IPO. The reason given was low margins in the business which will not allow them to make money.

The company has also recently gone full throttle on its own private label as well while partnering with two other listed entities namely Akums and Windlass for manufacturing MedPlus branded medicine which will be sold in its own store under the “MedPlus” brand so there seems to be a pivot from opening as many stores as possible to now serving own label products in the existing 4500 odd stores

There have been talks of sale of the whole business as well two times before the IPO where the promoter and other investors have offered shares for sale but the reason given has been valuation mismatches which is why the sale has fallen through. This along with the promoter starting other ventures though small, gives an impression that promoter might not be involved in the business for a long time

There were thoughts on raising more capital recently as well with the company passing an enabling resolution for a QIP but those seem to be on a hold for now going by the recent communication. Noticeably store openings have taken a back seat while diagnostics too seem to be a Hyderabad only play for now

5 Likes

Two interviews of the CEO on media explains his philosophy, how he built the company, mistakes along the way and vision going forward quite well. These are quite old though. I have summarized them and also provided the link to the original talk below.

- Was able to start in 2006 with 48 stores in 4 months with initial borrowed capital

- Plan is to add 1000 stores a year for many more years to come in the future

- Initial sales strategy was to go to corporates and sell them discount cards which were additional discounts over an above offered to general public

- Entered Bangalore market pretty early post Hyderabad and burnt a lot of money as the openings were too fast

- Expansion in Hyderabad was easy as had many personal connections which worked and made the task easier. However in Bangalore and Chennai this did not work as there was no connection

- In a retail business scaling up via a cluster based approach is far better and profitable as well

- Tried the experiment of putting up clinics and pharmacy adjacently but failed because stores are not well built and thus difficult to get good name doctors to come to these clinics

- Failed in Medplus beauty which was launched at the start of the ecommerce stage but suffered cash burn and this was not able to take off as it was earlier than the business should have been

- For a chronic patient medicine is basically a commodity as they are buying it every month

- Facing resistance in terms of non validity of e prescription which has made it difficult but still able to sell online due to the omnichannel model

- Main reason for existence of branded generic in India is because it enforces quality of manufacturing

- The medicine is not just about chemical composition but also because of the way the medicine is made and the efficacy it will have

- 24x7 opening of stores makes no financial sense and cannot be done on a full scale model considering the costs. In an emergency situation hospital is better than a medicine shop

- Second son in the family and first son is an engineer

- Till 2019 from 2005 used just Rs 260 crores of capital post which Premji Invest put in Rs 200 crores and post that in the IPO in 2021 end raised Rs 600 crores

- Auditor has been Big 4 and Warburg Pincus was on board and also invested for a long time

- From 2011-19 the company had raised just Rs 100 crores including both debt and equity

- Promoter mentions multiple times company would have gone bankrupt but funding came in at the right time since inception

- CTO was one of the initial hires who helped build all softwares in house and that is now helping in save licensing costs for softwares

- Since Day 1 have been very clear that Medplus as a brand should be known only for value pricing and not fancy stores

- Better to focus on one good idea as capital is limited, energy that a human being can devote is limited and small things that entrepreneurs keep doing eventually are not successful

- Promoter admits that he too is guilty of falling under the excitement of starting a business from an exciting idea but his ultimate understanding is that all of this is a waste of time and a promoter must focus on just one business

- In a retail business profitability is not a challenge but scale is

- Differentiates with Apollo in the sense that Medplus is not fancy and just provides value

- Apollo is backed by a big company and hence was able to grow faster than MedPlus for some time and has fancy stores while MedPlus is more functional with best price and frugal operating structure

4 Likes

The recent deal between with Advent buying stake in Apollo pharmacy gives a good idea of private market valuations in the retail pharmacy and online pharmacy space with some over view of peers in this space as well. I have posted a summary below:

- For FY23 for the pureplay online business of Apollo pharmacy housed under 24x7 the numbers looked like: Revenues- 709 crore, EBITDA Loss- 676 crores

- The holding company which houses both offline pharmacy operations of Apollo and also the online housed under the name “healthco” has recently raised $300 million at a valuation of $1.73 billion. This money was raised from Advent which is a PE firm

- Keimed, owned by promoters of Apollo has an enterprise value of Rs 8003 crore while health co is valued at Rs 14478 crores. Advent will get a 12.1% stake in the combined entity which will result in an EV of around Rs 23000 crore

- The pure play offline pharmacy business of Apollo had numbers in FY24 which is for nine month ending: Revenues- Rs 5139 crore and EBITDA of Rs 375 crore

- Keimed had numbers in FY24 which is for nine months ending: Revenue: Rs 7756 crore and EBITDA profit Rs 262 crore

- Online pure play pharmacy market share:

- One mg: 30%

- Pharmeasy: 28%

- Apollo Healthco: 18%

- Netmeds & Flipkart: Low single digits

- While Apollo Healthco has 6000 stores the other online pharmacies have recently decided to open offline pharmacies as well with One mg planning to open 300 stores

- Numbers for One mg which is the leader in online pharmacies. This is for FY23: Revenues: Rs 1627 crore and losses of Rs 1254 crores

- Apollo’s offline pharmacy business and Keimed which houses the private label business of APollo under which it sells various products are both independently profitable

1 Like

-

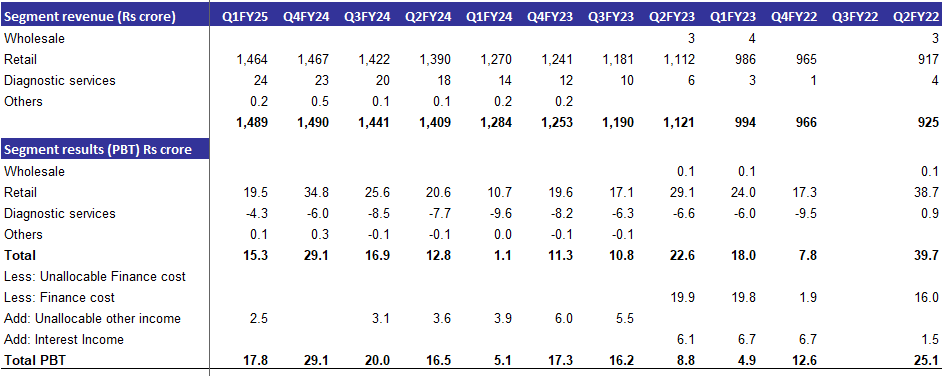

Net addition of stores peaked out in Q2FY23 when 348 stores were added during a quarter. Average store openings over the last three quarters have been below 150. Q1FY25 was an aberration because of general elections. The management continues to guide for 600 store openings on an annual basis

-

Consequently stores open for 2 plus years have seen a bump up which has improved the margins as well. Management maintains stores open for 24 months plus contributes higher to EBITDA

-

The diagnostics business has seen its annual run rate increase every year since its opening going up from Rs 30 crore annualised to Rs 100 crore annualised in FY25. Consequently PBT losses in this business in Q1FY25 were at their lowest. Hopefully this business too starts contributing to the bottomline by FY26. The margins in diagnostic business are much better than traditional pharmacy retail. This for now remains a one city operation confined to Hyderabad only

-

Private label contribution at 15.8% of overall revenues in Q1FY25 is highest for the last few years. As per management guidance this will improve overall margins for the business

Disclosure: I own shares in the company

1 Like

Med Plus Health Q2 FY25 Earnings Call Summary

Overview and Key Metrics

- Network Expansion: The company now serves communities in 680 cities across 12 states with a total of 4,552 pharmacy stores.

- Diagnostics: Operates four full-service diagnostic centers, eight level-two centers, and over 100 collection centers, aiming to provide affordable diagnostic services.

- New Stores: 198 new stores opened in the first half of FY25, with a net addition of 108 stores in Q2. Most new stores were in Tier 2 and beyond.

- Private Label Sales: Constituted 18.4% of total revenue, significantly boosted by the recent launch of Med Plus branded products. Private label adoption is expected to grow by ~1% each quarter.

Financial Performance

- Revenue: Consolidated revenue reached INR 15,762 million, up 11.9% YoY and 5.9% QoQ.

- Pharmacy: Accounts for 99% of revenue, with 18.4% YoY growth. Pharmacy operations recorded an operating EBITDA margin of 4.6%.

- Older Stores (12+ months): Contributed 94% of pharmacy revenue, with a store-level EBITDA margin of 10.2%.

- Diagnostics Segment: Revenue grew to INR 283.15 million with an operating EBITDA of 7.4%, a significant improvement from the previous year’s loss. A recent restructuring in diagnostics led to a one-time cost of INR 19.7 million.

Working Capital & Inventory

- Net Working Capital: At 61 days for Q2, with inventory levels of 38 days in warehouses and 95 days for new stores (40 days for stores older than 12 months).

- Impact of Private Label: While private label goods could improve inventory management over time, immediate inventory reduction is unlikely due to the need to balance branded product stock with private labels.

Growth Potential in Private Label Products

- Revenue Mix: Private labels (Pharma and FMCG) offer higher margins, estimated at 50%. Private label sales are anticipated to incrementally improve overall margin.

- Pharma vs. FMCG: Private label penetration in the pharmaceutical segment is around 10.5%, while FMCG accounts for ~7.9%. Chronic medicines make up over 50% of private label sales, as customers find value in savings from these long-term medications.

Capital Expenditure and Expansion Plans

- Store Expansion: Although the initial target was to add 600 stores this fiscal year, management projects 400-450 net additions due to Q1 disruptions.

- Funding and Leases: Most stores are leased, with minimal reliance on franchises, which are limited to remote locations.

- Free Cash Flow: Less aggressive store additions in Q2 led to stronger cash flow, though the addition of new stores may moderate free cash flow.

Operational Enhancements and Margin Sustainability

- Gross Margin: Management expressed confidence in maintaining the Q2 gross margin (23.7%) into the coming quarters, driven largely by private label growth.

- Rental Costs: Average rental cost per store stands at ~INR 43,800 per month, consistent without any significant one-time costs.

- Quick Commerce Strategy: Management remains cautious about entering quick commerce, given the complexities of prescriptions and delivery logistics for pharmacy products. The focus will remain on expanding their own online channels.

Diagnostics Business and B2B Expansion

- Corporate Partnerships: The diagnostics business is exploring B2B options, collaborating with companies to offer diagnostic services as part of employee health plans, especially targeting OPD (Outpatient Department) policies.

- Diagnostics Capabilities: Expansion of services, including OPD, is under consideration but no immediate implementation was mentioned.

Key Investor Questions & Management Responses

- Working Capital Improvement: With increased private label sales, working capital might see gradual improvement, though the company prioritizes product availability over strict inventory reductions.

- Store Growth & Cash Flow: The Q2 free cash flow boost came from fewer store additions. Expansion plans are conservative and focused on 400-450 new stores for FY25.

- Gross Margin: Expected to sustain Q2 levels at 23.7% through private label expansion, with management optimistic about achieving even better margins.

- Branding & Marketing: Current efforts focus on in-store education and influencer marketing; no significant ATL (above-the-line) advertising is planned.

- Quick Commerce: Management remains skeptical about quick commerce viability in pharmacy, but continues to monitor developments in customer demand and competitor moves.

Summarized by chatgpt

3 Likes

interview: MedPlus Bets On Private Labels To Drive Profitability Over Next Two Years

private label boost is all there is to it

Diagnostics (particularly Radiology) looks more promising, more importantly with the kind of disruptive pricing that the Company is offering these services.

Isn’t low promoter holding (40%) and high pledged share a concern?

- Promoters have pledged 54.2% of their holding.

- Promoter holding has decreased over last 3 years: -56.2%

Are you sure? What’s the source? Screener says 40.43 to 40.39?

Low promoter holding is not concern as the company is backed by PE investor. Just my opinion.

Disc: Used to invest, not invested as of now

3 Likes

Company can grow at a pace of around 15% to 20% in the longer term , however expecting that the company would grow at a rate of more than this would be unfair because getting an ROE of more than 20% for a retailer could be a tough task that too when you are competing on price majorly and trying to disrupt the unorganized market by price only.

4 Likes

Couldn’t agree more , management is trying to disrupt the unorganized pharma retailing sector in India. This was explained very thoroughly in Sept’23 concall by the management.

6 Likes

We get regular reports of store drug-license-suspension like this:

Though it helps to see the revenue per day for these suspended stores, I wonder what could be the reason for such suspensions.

We don’t find any suspension of our neighbourhood medical stores ever. I don’t think their standards are any better than Med+.

Is Med+ not taking care of health inspector or something unlike the other stores? OR my assessment that this is not happening to other stores is incorrect? ![]()

By the way, I don’t find such drug-license-suspension reports from Apollo Hospitals which run Apollo Pharmacies.

4 Likes

Routine, short-term suspensions for issues like the absence of a qualified pharmacist or improper record-keeping are common across all pharmacy retail establishments in India. While Apollo may receive such orders, they are not obligated to disclose them to the stock exchanges as frequently as MedPlus does for Optival, unless the impact is deemed “material” to the entire company. The lack of constant public disclosure of short-term suspensions does not mean they never occur.

2 Likes

This questions arises many times, let me give my pov.

Apollo Hospitals Enterprise Ltd (AHEL) holds ~25.5% in Apollo Medicals Pvt. Ltd. (AMPL) which, in turn, wholly owns Apollo Pharmacies Ltd. (APL), the company operating the retail pharmacies. The remaining ~74.5% of AMPL is held by external investors.

Due to this AMPL is associate of AHEL (not subsidary). As associate operational details (like how many shops suspended, compliance issues, etc.) are not required to be disclosed by AHEL.

4 Likes

I have written the email to promoters every now and then, never got the reply. If you guys have any idea please let me know ? or please ask this to promoters over email as a shareholder this is the thing blocking your returns in my view.

To -

ir@medplusindia.com,

manoj.srivastava@medplusindia.com,

cs@medplusindia.com

I have following query to the promoters -

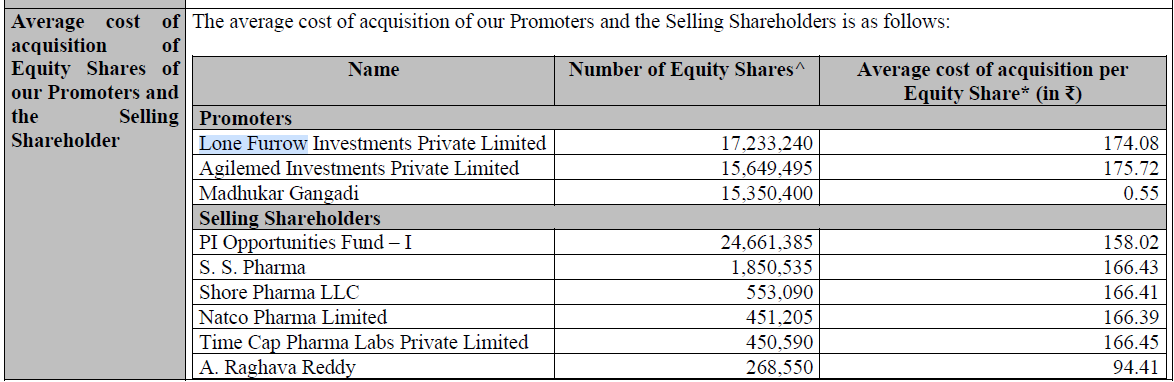

I have noted that promoter group entities like Agilemed Investments Pvt Ltd and Lone Furrow Investments Pvt Ltd, which appear to be primarily investment vehicles without significant standalone operations, have raised non-convertible debentures (NCDs) totaling around ₹870 crore, secured against approximately 56% of the promoter group’s equity holdings in MedPlus. Could you please elaborate on the strategic rationale behind this structure and the overall end game? Specifically, what is the plan to manage and reduce this debt over time—such as through refinancing, internal cash flows, or other means—and do you anticipate any potential divestment of these entities’ holdings in MedPlus in the long term to support repayment?

---------xxxxxxx--------------------

My personal take on this is - one day they have to sell promoter holdings through these shell companies and pay down the debt - that will obviously create lots of pressure on the share price.

but they should tell us the plan ? will they just sell little bit over time or will they just sell it to some PE or strategic investors at the right time ?

2 Likes

I have heard I don’t know how true it is but mom and pop pharmacies have to shell out 10-15K every month to drug inspector if you don’t give that bribe they suspend your license.

this is very common practice.

1 Like

how long this nonsense has to go on ?

1. Promoter Share Pledge for NCD Refinancing (Dec 19 & Dec 18, 2025)

There are two connected disclosures:

a) Creation of new pledge – Agilemed Investments (Dec 19, 2025)

- Promoter entity Agilemed Investments Private Limited has pledged 48,51,066 Medplus shares (about 4.05% of total share capital).

- This takes Agilemed’s encumbered shares to 1,56,49,495 shares (13.06% of total share capital).

- Overall promoter shareholding in Medplus: 4,82,80,627 shares (40.29%).

- Encumbered promoter shares: 3,34,99,895 shares (69.39% of promoter holding).

- The company notes that encumbered shares are >50% of promoter holding and >20% of total equity.

Reason / context (their own words, summarized):

The incremental pledge is “in connection with the refinancing of the Company’s existing debt in the form of non-convertible debentures (NCDs)”.

- During the refinancing process, promoter pledge will temporarily increase from 23.91% to 27.96% of company equity.

- After the old NCDs are repaid and earlier pledges are released, the promoter pledge is expected to come down to 24.48%.

Implication:

This is not a fresh borrowing at Medplus level, but promoters pledging shares to refinance existing NCDs at the promoter entities. Risk-wise:

- Promoter pledging is high and remains a key monitorable, though this step is positioned as a refinancing / rollover, not incremental leverage for unrelated purposes.

b) Debenture Trust Deed & NCD details (Dec 18, 2025)

This is the formal disclosure of the refinancing structure:

- Promoters (Agilemed Investments Pvt Ltd and Mr. Gangadi Madhukar Reddy) have executed a Debenture Trust Deed with Catalyst Trusteeship Limited on Dec 12, 2025.

- NCD issue size: “up to INR 175 crore”.

- Coupon: “12.72% per annum, compounded monthly, together with an initial coupon of 1% on the principal amount.”

- Medplus itself is not a party to this agreement; it is at promoter / promoter-entity level.

- The disclosure reiterates:

- Promoter pledge will temporarily move from 23.91% to 27.96% of company equity,

- Then is expected to reduce to 24.48% post-refinancing and release of earlier pledges.

Implication:

- Confirms high-cost promoter financing (12.72% + 1% initial coupon).

- No direct balance-sheet impact on Medplus, but share pledge remains a structural governance & risk factor.