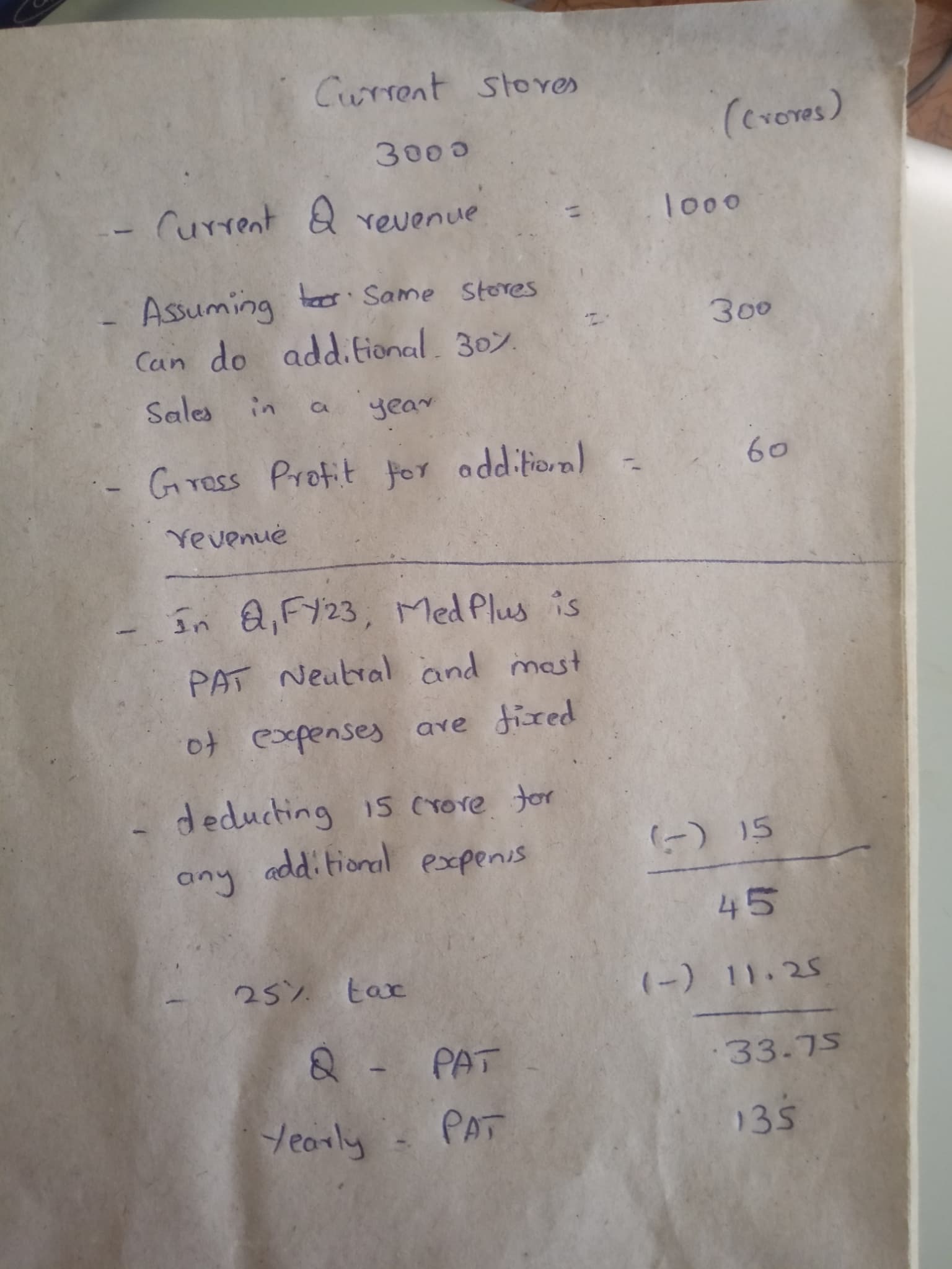

One back of the envelope calculation on why I am currently keeping away

Assuming 4000 stores after a year, assuming 4 Mn as average sales per store after the stores reach maturity in 12-18 months, top line may reach 1600 cr, with 10% EBIDTA - 160 Cr, assuming some depreciation, taxes etc, PAT may become around 110-115 Cr

It still does not deserve rich valuation of 6000 Cr (50x Profits which may be visible if Medplus is able to execute flawlessly during next 1/2 years)

My assumptions lead to similiar PAT, I value 2500 cr for current stores and 600 cr for any new stores they put in and not valuing optics and diagnostics business. I feel anything near to 3500 crore valuation is good. Now its exactly 2x.

In your assumptions, you need to change topline, in last quarter itself, they did 1000 crore topline, you are calculating 1600 crores entire year. You are not deducting enough from ebidta to pat. They will incur rent payments as interest and depreciation after ebidta, so you have to tweek there also

One reason why back of the envelope valuations may not make sense here is that market isn’t convinced that pharmacy retail will see so many players. It believes, like in other mature markets, this market will consolidate to 2-3 players. Once that happens, discounts reduce and margins improve. Even the gross margins would improve as organized pharmacies emerge as big buyers and bargaining dynamics play out especially with generic medicine players.

If you factor in that, PAT margin has the potential to reach 6/7% in next 3-4 years on a ~2x topline, which leads to roughly ~500crs of annual profits. On that basis it isn’t super expensive.

Plus, the optionalities baked into business - diagnostics.

This quarter’s result reveals that there have been 153 new store openings (with 168 gross additions). I had anticipated around 250 new stores to be opened in order to achieve the target of 1000 stores for the fiscal year. After reviewing the conference call, it appears that no one raised a question regarding this matter.

If anyone has information about the management’s reasoning behind the lower number of store openings, please share it.

Shares of MedPlus Health are down nearly 7.75% as of 11.30 am on 31/8/2023 after 12.85% equity changes hands. Buyer saller not known as of now.

CNBC-TV18 had earlier reported citing sources that PI Opportunities Fund or Premji Invest, along with Lavender Rose Investment Ltd., some of the early investors in pharmacy chain MedPlus Heath Services plan on paring some of their stake in the company.

Based on the June quarter shareholding pattern, PI Opportunities Fund held a 14.11 percent stake in the company, while Lavender Rose had a 17.24 percent stake.

It seems selling overhang will be there for some more time. PE selling is major issues with co like HomeFirst, Medplus etc.

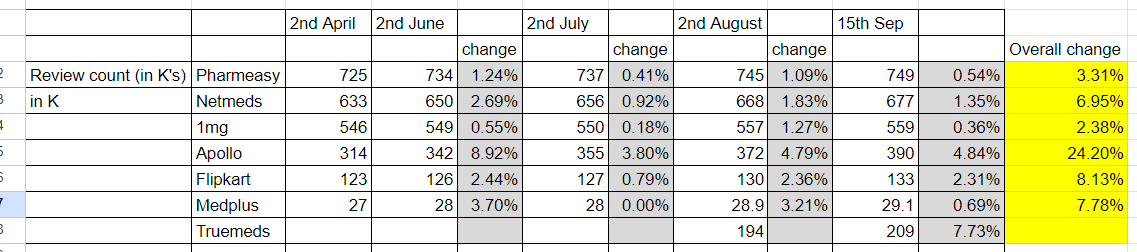

I was trying to collate some play store data about where the incremental interest is going on for online players vs omni channel players. This data cannot be directly correlated with sales, but this can give some indication

AHL - Apollo Health co is valued at INR 14,478 Cr which implies over 15% premium to its closest peer’s listed multiple. (from Apollo hospital disclosure).

Apollo Pharmacy has 5600 stores

revenue 5800 cr, EBIDTA @ 7.7% is 449 Cr

They have separate distribution complany keimed.

Medplus Mkt cap as of 27/4/2024 is 8000 and 4230 stores.

Revenue 5387 cr, EBIDTA 330 Cr.

Studying more on Advant investiment in Apollo Healthco. Will share if found anything interesting

Does Apollo have store generics as that of MedPlus? I’m very bullish on store generics. Waiting for that story to unravel. If MedPlus was able to build generic brand in long term it is very positive. Diagnostics has intense competition and local connections with doctors is key, which is difficult to scale. Let’s see.

generally this is done to replace debt with higher interest rate with new one with lower interest rate.

They maybe able to raise debt now at lower interest rate than what they raised before.

Promotor entity Agilemed and Lonefurrow has good chunk of debt in their book. This debt is via NCD, they were due for payment. They decided to refinance it by issuing new NCDs. For this they created this pledge. This is common practice. It is not illegal, but risky. Both Agilemed and Lonefurrow does not have any other asset or business apart from MedPlus shares. They have no other source of income. I think for very good amount of time, he is going to refinance rather than repaying

NCDs are not issued to promoter entity. In this case, NCDs are issued by promotor entity to other party. In this transaction, MedPlus neither issues NCD nor buys this NCD. Only relevance of MedPlus to this transaction is their shares are provided as collateral to this.

I don’t see it as a threat - I never go for generic generic due to quality concern, although its good for those who have affordability issue. generic generic expanding the market not taking away the market.

Infact that’s one of the USP of Medplus - their private labels are branded generic which they sell at 40-50% discount ensuring quality as they control the whole supply chain unlike others.

Other UPS is - because of their cluster based approach they manage their inventory very well, fill rate is very well managed. Customers mostly find all the medicines they need and doesn’t have to go anywhere else.

For chronic treatment they have Private label - which customers find very cheap and effective.

They are operationally most efficient player in the market due to control of whole supply chain. They use Tech / Data analytics in every area to figure what drugs will be required as per locality.

anyone knows what is the relation of these two companies and Medplus and promoters ?

Agilemed Investments Private Limited

Lone Furrow Investments Private Limited

There are lot of financial transactions between these companies and pledging of shares.

Again some financial engineering - this time promoter reddy revoked his pledge and Lone Furrow Investments Private Limited pledged the same amount . wtf is going on ?

@AmitContrarian explained this in above thread. In short those two entity are promoter owned (not part of any PE firm). Those 2 firms does not have any other business and just holding shares of MedPlus. In past they acquired this shares by raising debt from PE firm. Still that amount is not repaid and they keep on doing refinance by pledging again and again.

Since that debt is a high amount and my guess is this debt will not go away unless he do part stake sale or magically he brings such huge amount. Until that time you will see this pledge and revoke keep on happening