News covering mcx

MCX shares zoom over 5% to 52-week high on SEBI Chairman’s comments, precious metal rally; all you need to know MCX shares zoom over 5% to 52-week high on SEBI Chairman’s comments, precious metal rally; all you need to know

2 Likes

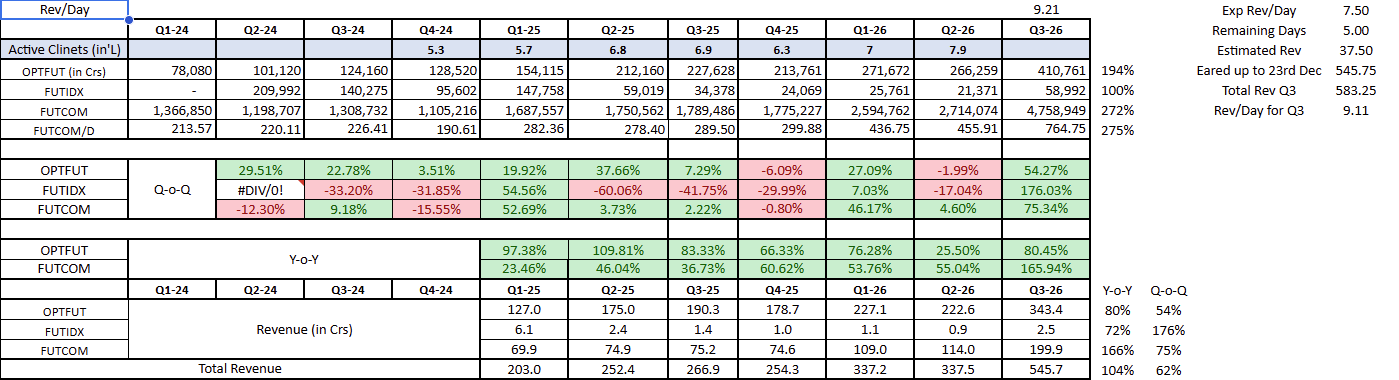

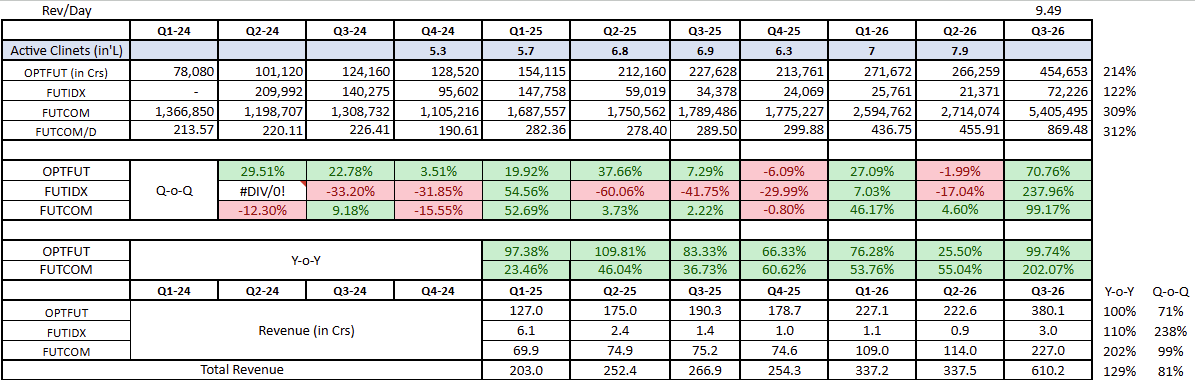

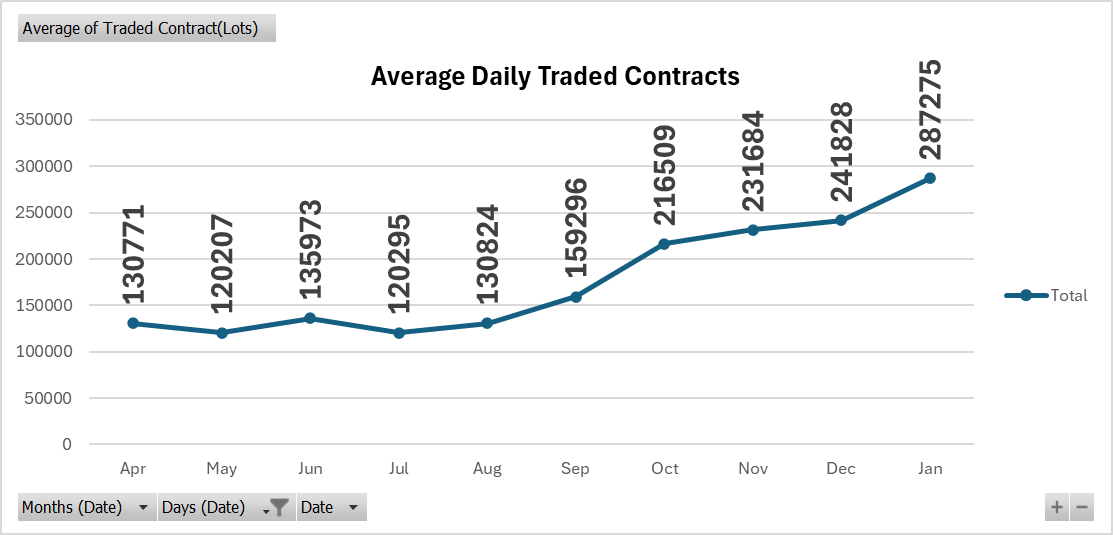

Not sure how that revenue helps MCX earn commission, but contracts traded look flat or stagnating over Oct-Dec

3 Likes

Compare contract# yoy and qoq . Good growth.

Fee income is basically on value of trade and not trade count only.

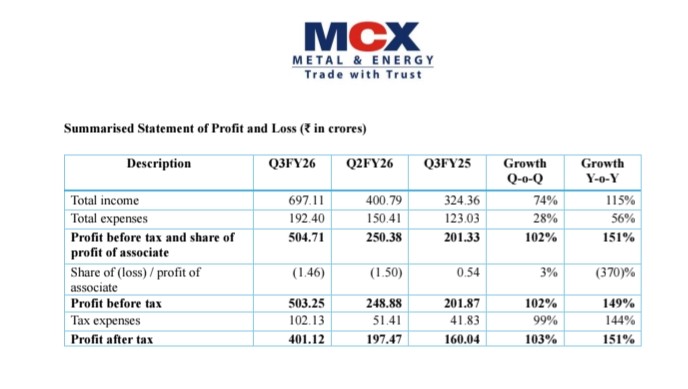

Would be interesting to see if profit growth is higher than revenue growth - this is too expected being a platform.co and now since mcx own the tech platform. I also expect 75% of profit to be distributed as dividend. Definitely >1% dividend yield is expected.

1¹¹

2 Likes

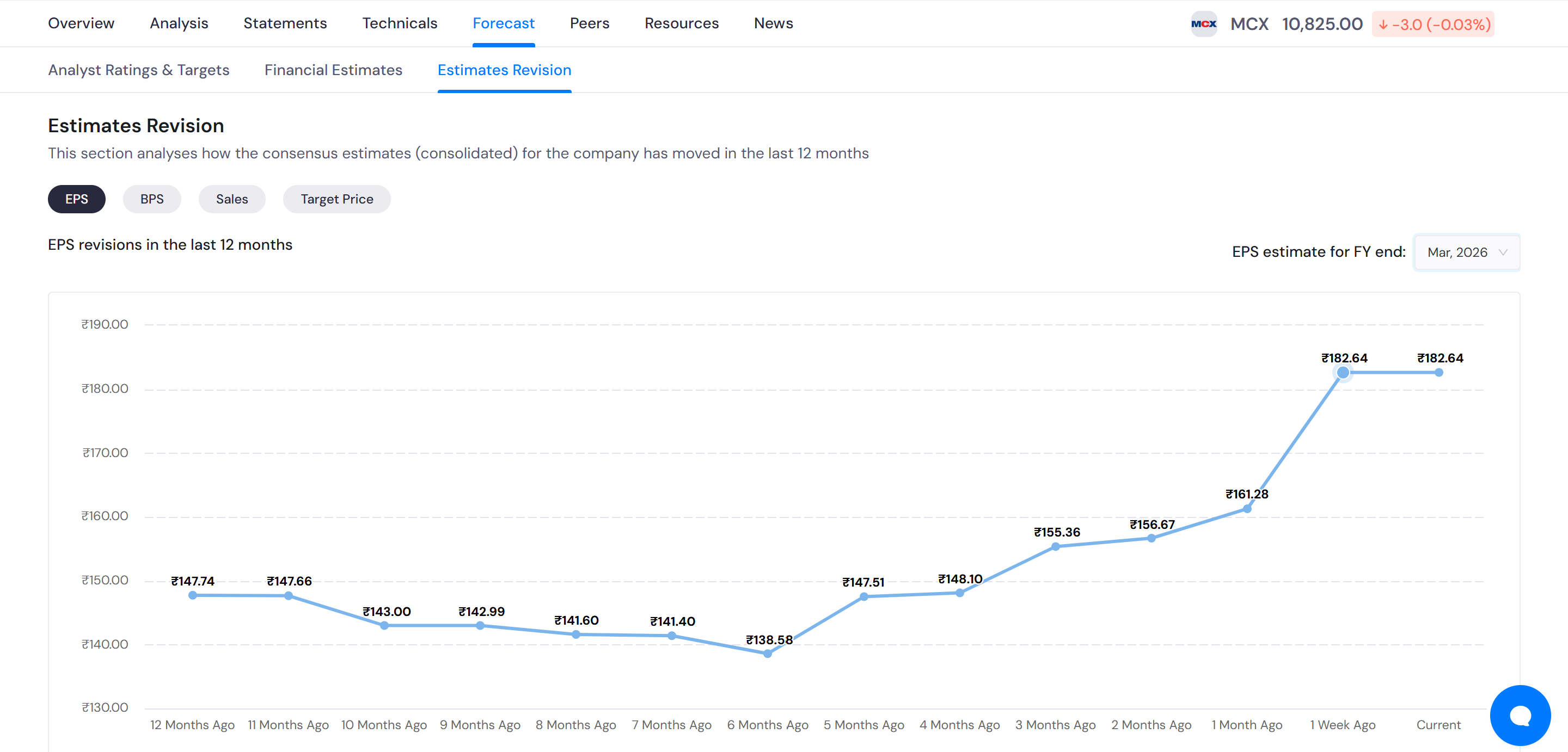

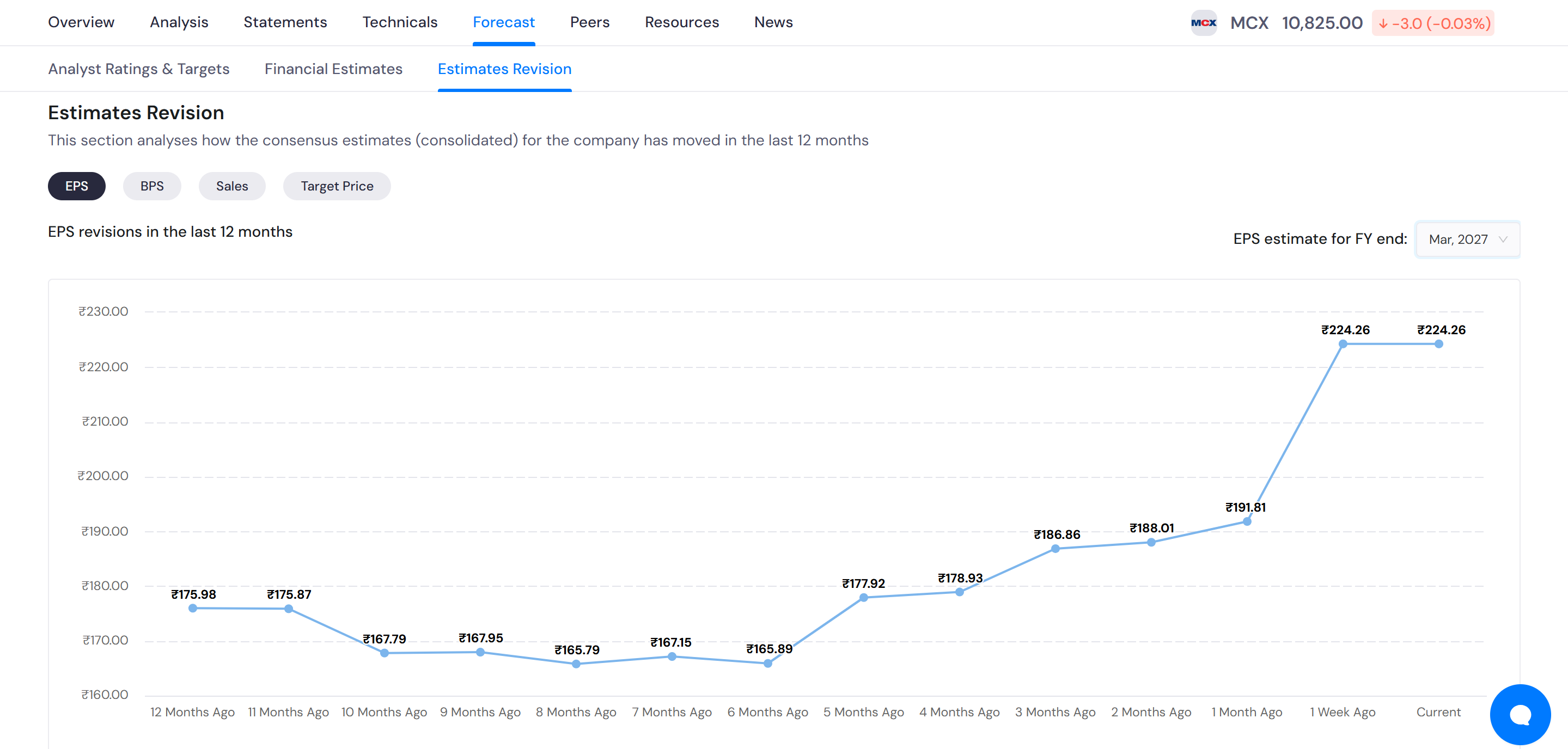

Analysts are raising EPS estimates for FY 26 and 27.

Even if company hits EPS of Rs. 170 (lower than the estimates) and company distributes 75% profits as dividends then yield will be more than 1% as of current price.

4 Likes

The biggest kick in trading value came from higher participation in commodity market , higher and volatile commodity price . These would continue in fy27 too including current quarter and so mcx is poised to clock 1000 crore net profit.

I dont think market has yet acknowledged it though share price is appreciated and there has been earning growth and higher share price target from brokerage. Would love to see mad bullishness in stock price ;)

4 Likes

Thanks for this. I’m new to the company, got a small query:

On calculating the Futures and Options transaction fees, it is 0.0836% and 0.0418% respectively. But this article quotes the following rates : 0.0021% and 0.0418% respectively.

Can you pls help me understand the gap? Seems like I’m missing on something.

1 Like

This is mostly becuse of difference in future and options transaction cost and overall exchange transaction cost.

Overall transaction cost includes commodity charges , taxes also

2 Likes

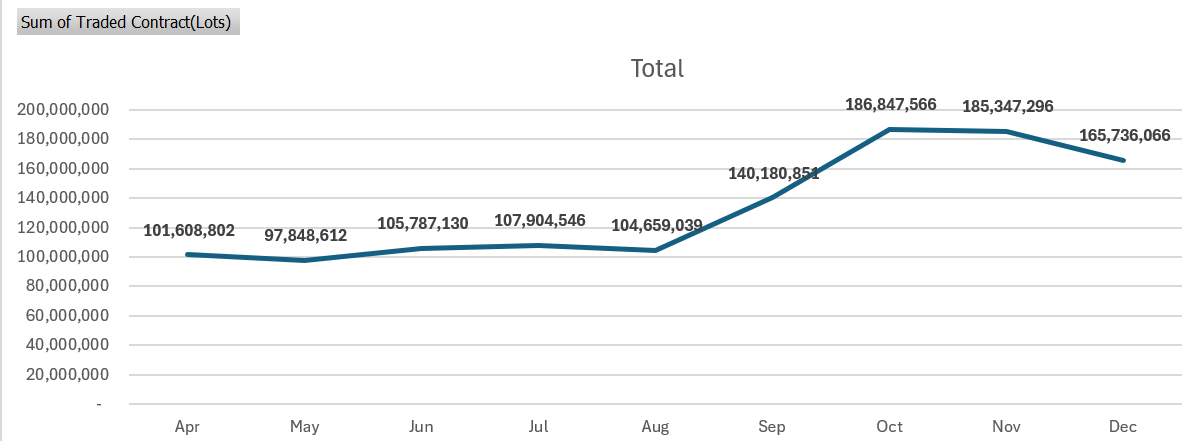

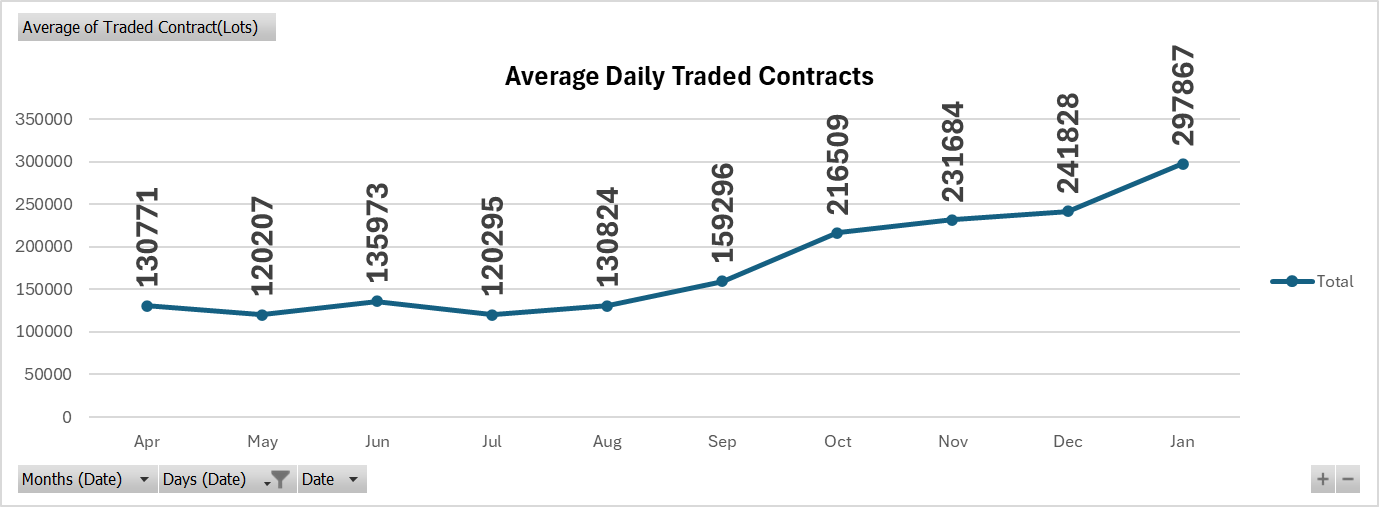

Well, there is more left in terms of volume growth specially in metal.

1 Like

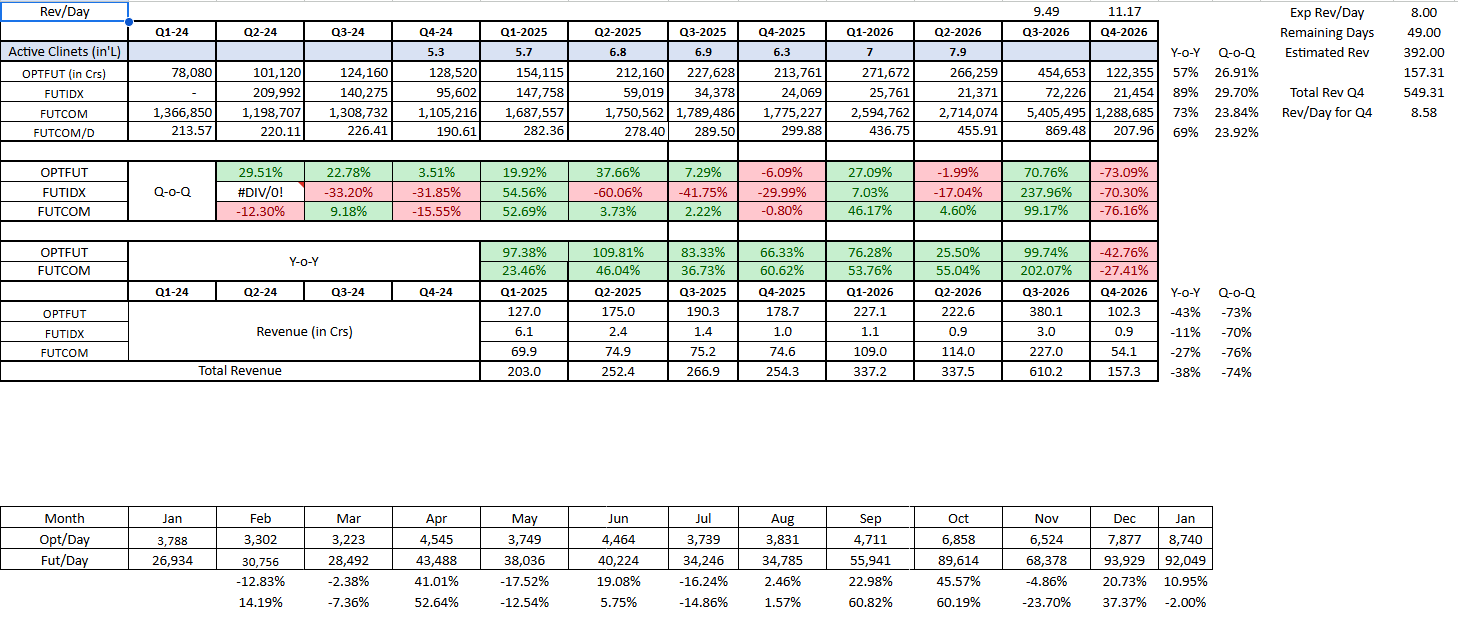

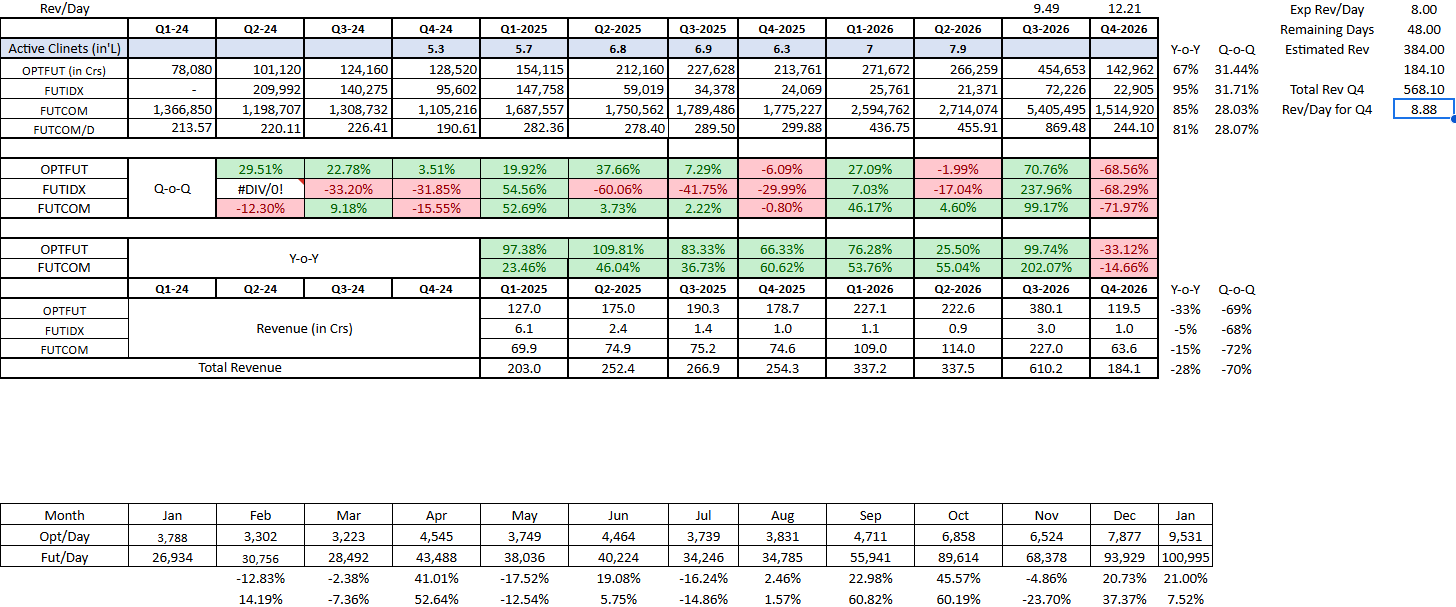

projected revenue is lesser than expected. while counting per day revenue , it should count only trading day.

Based on first 20 days of Jan 26 , q4 revenue would be 700 crore. This is again 100% growth yoy .

2 Likes

im assuming 8crs per day as the days progress the figure will get adjusted automatically.

you cant extrapolate linearly. I like to keep it on the conservative side.

yesterday was a 25crs + day for revenue but we cant assume that for the remainder of the qtr.

1 Like

Superb result. Thinking loud , this is so heartning to see profit growth beating revenue growth. This is truly a platform characteristics. If current revenue growth continue , we are looking at 500 crore quarterly profit.

9 Likes

While FIIs have been continuously selling , they have increased stake in mcx . Looking at retail holding. I dont think mad rush has started even though share has gone up 50% in last 4 months.

3 Likes

MCX benefits from a strong platform model where costs are largely fixed.

Higher trading volumes and volatility pushed revenue up, while expenses grew much slower.

This operating leverage explains the sharp jump in profits.There doesn’t seem to be any major one-time income in this quarter.Sustainability will depend on volumes staying healthy across cycles.

2 Likes