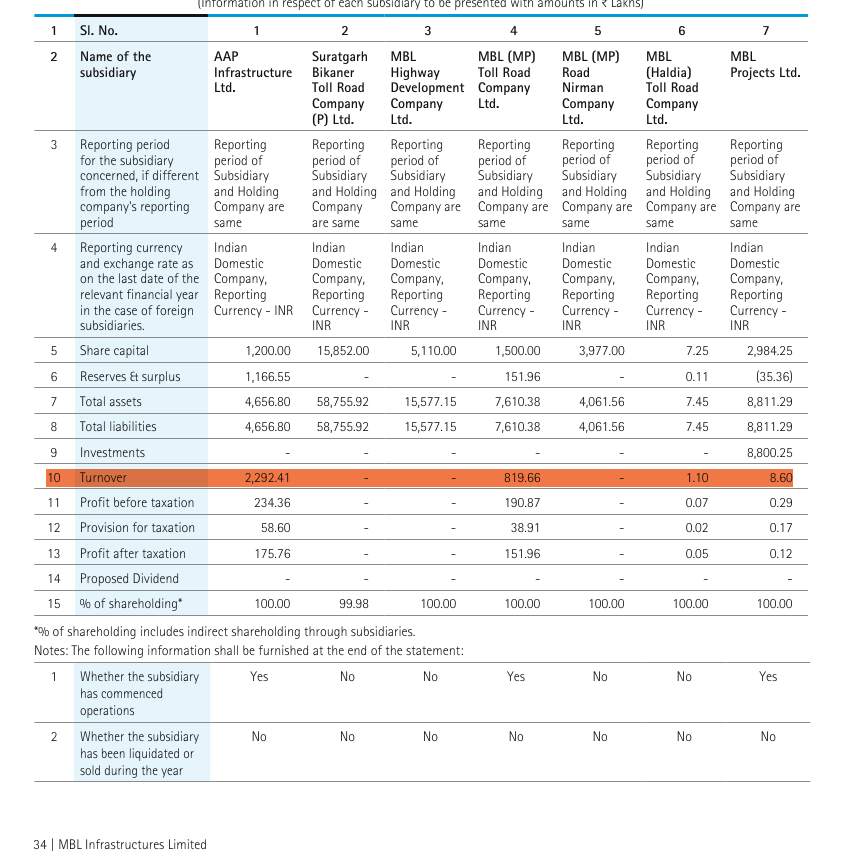

MBL is engaged in the execution of civil engineering projects. The Company provides integrated engineering, procurement and construction (EPC) services for civil construction and infrastructure sector projects. In recent years, MBL has executed and commenced a number of praiseworthy projects in 14 states of India. The Company has successfully completed the execution of the BOT project of 114 km long Seoni - Balaghat - Gondia State Highway (Madhya Pradesh), which is operational since February, 2008 and another project of 18.3 kms of Waraseoni-Lalbarra Road Project (Madhya Pradesh) is operational since August, 2015.

The Company has a large fleet of sophisticated equipment, including hot mix plants, sensor pavers, tandem rollers, soil compactors, stone crushers, loaders, excavators, tippers, motor graders, concrete batching plants, transit mixers, concrete pumps, dozers, cranes, etc.

-

MBL has over two decades experience in executing infrastructure projects as Prime Contractor and has established its ability to deliver quality jobs within budget and schedule. -

MBL was among the first batch of contractors to be awarded the contracts of prestigious North South East West Corridor by NHAI and was the first to complete the project. -

MBL was amongst the first batch of contractors to be awarded the contract for maintenance of National Highways by NHAI. -

MBL was awarded the first ever contract for comprehensive maintenance of Inner & Outer Ring Road of NCT, New Delhi. -

MBL has witnessed a Continuous Growth in Bid Capacity and Pre-Qualification Capability. -

MBL has been judged as 2nd Fastest Growing Construction Company (Medium category) in India at 13th Annual Construction World Global awards and 3rd Fastest Growing Construction Company (Medium Category) at 10th, 11th and 12th Annual Construction World Global awards. -

MBL has been judged among India’s top Challenger Companies in the Construction and Engineering value chain FY14 at 12th Annual Construction World Global Awards. -

MBL is the Winner of India’s No. 1 Brand Awards 2016 in India’s Best Infrastructures Company Category awarded by International Brand Consulting Corporation, USA.

The company have almost doubled its revenue from 1251 (2012) to 2314 (2016), however the margin have been under pressure falling from 5% to 3.67 in 2016.

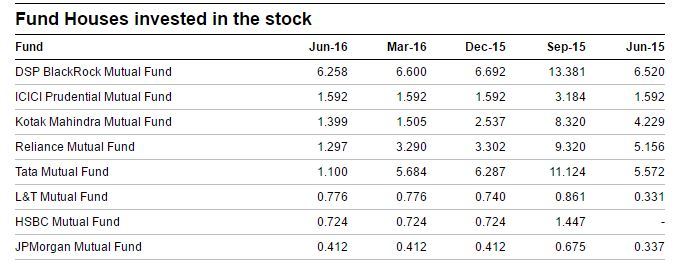

Mutual funds and Institutions also have a stake close to 26%. Promoters are holding 49% stake. It has also been paying dividend continuously since 2012 at least.

During the year they had order inflow of Rs 3,600 crore odd and during the last quarter they had orders of Rs 3,149 crore.

They are a low geared organisation with low long-term gearing. Rs.125 crore of long-term borrowings on the standalone basis. If we take the working capital, the debt to equity ratio is 1.21. If we take the build, operate and transfer (BOT) projects, it is well within 2:1.

The company bagged orders worth Rs 3,190 crore in Q4 FY16, and a delay in their execution led to low EBITDA margins, said AK Lakhotia, Chairman and CEO. The profitability of these orders will be recognised in FY17, Lakhotia maintained.

The stock has recently corrected maybe due to incorrect interpretation of quarterly numbers. At 114 the stock is very cheap with expected EPS of at least 15-16 at the minimum.

I took a small exposure today, the stock represents 2% of my portfolio.

Views are invested from the ones tracking it more closely.