hi

i did attended the concall. mgmt has given interview on cnbc for recent invocation of pledge.

Mgmt is confident abt future prospect and financial closure for new project.

they have good epc order book as well as road project.

arbitration law money recently announce by govt mbl may expect around 10cr

they said they will upload transcript of concall too

With 0.44 book value and 4 EPS, MBL looking dirt cheap. Today had UC almost entire day. Any expertise comment here?

The management had appeared on CNBC 2 months back and had commented on the pledging of the shares. Accordingly to them they plan to de-pledge 100% by end of the current financial year. Hence I will wait and watch until then if their actions follow their words. Many infra companies are due to receive the amount from the government so I think it should help better the situation.

Since the small is small, my investment in this company is limited to 3% of my invested capital. I don’t plan to add futher and will rather have a wait and watch approach.

1 Like

AK Lakhotia , CMD says on CNBC

Yes, the stock was quite volatile and we have learned a bitter lesson. Within this financial year, we will have all the shares de-pledged and we will restrain from pledging going forward.

If he keeps his word, company can see good future going forward. He felt sorry for pledging… This is important

Could anyone throw some light as to why the daily lower circuits… What has changed after the recovery from last September/Oct correction due to the pledged shares issue.

Thanks,

Sridhar

126 crores net loss for the quarter ending sepetember… i hope you have noted it

looks like one - two circuits more before upside

The loss was due to the write off of the MP’s road cancellation of 220CR which were cancelled without due regard and will be contested and be paid back post arbitration.

If we consider that, they still had a 94CR profit even after higher inventory being priced in which can lead to lower cost of inventory in future.

The turbulence is just panic selling and it is also not helped due to the pledged shares and they triggering LCs.

As Lakhotia said, pledge was a bad idea, hope they do not in future. Also we need to kick the Reliance AMC folks who bought at ~280s in placement and sold at 117.

Statement showing shareholding pattern of the Promoter and Promoter Group for June 2016

Statement showing shareholding pattern of the Promoter and Promoter Group for September 2016

The pledged percentage of two major share holders have increased from 16.65% to 97.32% and from 93.89% to 98.03%.

If Lakhotia was indeed planning on de-pledging as he promised, the trend should have been other way round. But it’s a steep increase.

I dont think its wise to park our cash in a company whose promoters own less than 7% of the total shares.

Disc. Not invested. But watching the drama keenly.

The pledge % increased as the value of the pledge lowered with declining price triggering margin calls and forcing the dumping of stock in the market by lenders thereby hitting LCs. To avoid this, the promoter had to pledge more to meet the market value and MTM losses or depreciation in asset value.

This is what the promoter said in the interview, pledge was a bad idea and we got stuck in a spiral, we do not want to get into pledge in future and will try to de-pledge for now.

We have to wait for 1-2 quarters to know the exact nature of his statements, are they just mere words or substantiated by actions.

Can we be sure that the LC isn’t due to some operator game? If Lakhotia is indeed planning on getting the shares back by March’17, then it makes sense if he gets some operators to drive the prices down. The promoters collectively own less than 7%. So they have nothing much to lose. Once the price reaches rock bottom, they can comfortably buy from the open market, rather than release the pledge, which they have pledged at double the CMP.

If that is the case, then we might be looking at a rare opportunity. A company with decent credentials and a fat order-book, quoting at throw away valuations. The prices are sure to go up if the promoters start buying.

Discl. Not invested yet.

MBL infra has orders in hand of 6941 cr as per latest presentation (it was 7950 cr as per Nov presentation). Still its 3x turnover. Visibility is there.

But worryingly pledging has been increasing every quarter. Clearly indicating liquidity issues. Just one tiny release of pledge announced recently. Debt equity is relatively high at 1.6

Mcap of 185cr may look low. But EV is 1175 cr which seems quite high.

Discl – not invested, a clear avoid for me.

1 Like

Sir don’t you think these LC’s are due to margins on pledging…

these pledges are being invoked due to margin …

i believe these valuations are certainly not justified for MBL at present…

New analysis on the company worth reading : http://www.drvijaymalik.com/2017/01/analysis-mbl-infrastructure-limited-research-report.html

Anyone attended the concall?

I did. Here is summary:

- Talking to parties to divest the 2 operational BOT and Bikaner Suratgarh once it is operational (though I am not sure if a developer is allowed to divest before 2 years of operations)

- Bikaner Suratgarh to be operational in March.

- Looking to rope in financial partners for HAM projects

- In-principle approval received for HAM projects, official financial closure soon

- FY17 revenue target ~2100 cr, FY18 ~2700 if I remember correctly

- All pledged shared to be depledged by March end

- Talking to bankers to find out the best possible solution out of the current sticky situations. One of the possible solution might be offering lenders some convertible instrument to bring down debt

Inshort, Mr. Lakhotia did agree that they made few judgement errors and laid out the options they are considering to remedy the situation. But again, lets see what transpires in the future. It is time for them to walk the talk.

Disc: Invested

Anyone got more updates on MBL infra ? I have heard few banks have pressed for liquidations of the company and supreme court lawyer have already taken over for liquidations. Yet to confirm if this is indeed true.

1 Like

I used to have a large holding- liquidated all about a month back at loss. As per one of its filing on BSE, banks had refused to lend it for BG - so it had to surrender two projects. For an infra company - lending from banks is like oxygen- if that is withdrawn - company has to close down.

1 Like

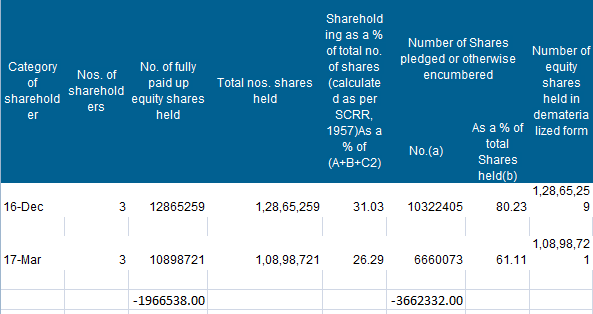

Updates on Shareholding Pattern

Lot of pledging has come down… some has been invoked…

Over all from 80% of promoter holding pledged to 60% now… while from total capital only 17% remains pledged…

So i believe… bad times are coming to en end for this company… and Q4 results will give a better picture…

Disclosure ; 5% of portfolio

Well the company is another example as to why we shouldn’t concentrate our portfolio to just 5-10 stocks. From being touted as a good growth company, the company have fallen to such dismal state. It’s an art as to how management of such companies comes on cnbc interviews and make tall empty promises on depledging of shares.

I do not feel averaging makes sense in such companies, wait and watch is the only approach for me. Luckily the stock is only 1.5% of my portfolio since I don’t believe in trusting indian management much.