2 Likes

Understand from source that MDL has appointed consultant RHD for development of new building and repairs yards. This should take care of next generation carriers,etc.

1 Like

FY 2024-25 Q4 Results: Company announced its Quarter 4 numbers, yesterday at 7:24PM.

So, if we talk about the commentary from the company’s Board of Directors, the company has announced the results. Then a final dividend was also announced, which is ₹2.71 per share. After that, no other announcements are visible, neither regarding bonus nor split. So, the company has certainly recommended a small dividend this time.

So, let’s see how the consolidated numbers were this time. The total income, which in last year’s Quarter 4 was ₹3452 crores, has now come to ₹3483. So there is a 1.5% upside, yearly. And quarter-on-quarter, it has gone from ₹3430 to ₹3483. So even here, there is about 2.5% growth. So, this time the income has increased very slightly, both quarterly and yearly.

Then if we talk about expenses, since the income increased, the expenses also went from ₹2600 to ₹3100 yearly, and from ₹2300 to ₹3100 quarter-on-quarter. So, the income increased just a bit, but this time the company’s expenses are significantly higher. And if you look at the biggest expense, it is the provisions. Provisions this time were ₹510 crores, which in the previous two quarters were only ₹170 and ₹91. So here, provisions have become four times for the company, due to which the expenses are much higher this time, and because of that, the profit is also visibly affected.

So, let’s discuss the net profit, which in last year’s Quarter 4 was ₹662 crores — this time it has come down to ₹325. And in Quarter 3, the profit was ₹807, which has come down to ₹325. So, due to significantly higher expenses this time, we are seeing a major decline in profit. Same with EPS — from 16, it has almost halved to 8 yearly, and from 20 to 8 quarter-on-quarter. So, just like profit has decreased, we are seeing a decline in EPS as well.

If we talk about the entire financial year, in FY2023-24 the total income was ₹10568 crores, which this time came to ₹12553. So, if you look here, the company’s income appears to be growing steadily. Then if we talk about the company’s net profit — in FY2023-24, the total profit was ₹1993 crores, which went up to ₹2400. So annually, the numbers are quite impressive. But if you compare it with Quarter 3 and last year, the performance isn’t good. So, based on this, today a decline is possible.

4 Likes

He is right. You fail to keep count of the socalled famous investor’s calls. Recently they have favoured ‘only’ large caps, ‘only’ banking stocks and may be pharma to go along with it, and before that FMCG.

Like my grandmother used to say, ‘suniye sab ki, kariye man ki’ (listen to all of them, but do what your heart tells you).

3 Likes

In my view , this is a company manufacturing sophisticated War ships , submarines. which take years to deliver.

So Q to Q performance is not the yard stick to measure. It is Y to Y performance which should be seen for last 3-4 yrs.

All defence shipping companies performace would be in this line only

You can also see Garden reach and Cochin shipyard.too.

Discl : Invested from 300 level..Still holding. and will continue to hold considering the order book and huge pipeline orders from ThyssenKrupp- MDL jt venture for submarines.

I may be biased. Not a buy sell recommendation. please do your own assessment before investing

6 Likes

till the order is cancelled, check the order pipeline orders every year, it should typically north of 25,000 Crs, as each ship, sub is about 6000-9000 crs. and build out time is from 3to 5yrs.

for defence companies, order pipeline AND execution is pretty much the only criteria to see if the numbers are in green and growing

2 Likes

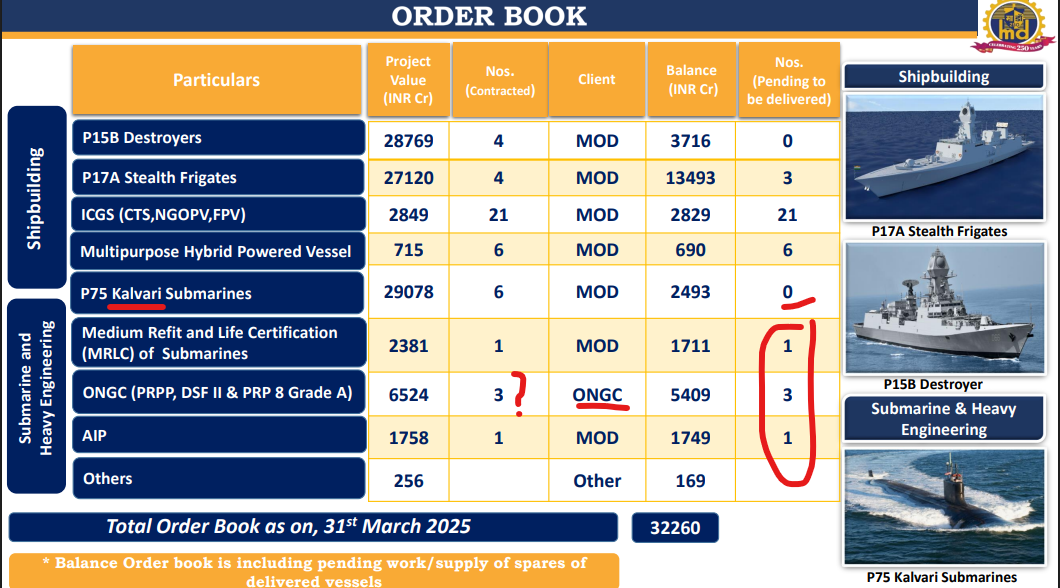

Mazgaon Dock current order book and forthcoming orders during Fy 2026-27.

Current order book Rs 36000.crore for MDL

The orders under pipelines 2.35 Lakh crore for all 3 defence shipping companies.

Overall, orders worth Rs 2,35,400 crore are lined up in FY26–27, which are 3.1 times combined order book of the three listed defence shipyards

Antique said the DAC has plans to place a repeat order for three Kalvari-class submarines with Mazagon Dock. The order will be on a nominated basis. The order value could be approximately Rs 36,000 crore and could get placed in FY26.

In addition, the P75I involves construction of six conventional submarines with AIP capabilities under the Strategic Partnership (SP) model. Unlike the P75 order, which was placed on Mazagon Dock on a nominated basis, the P75I order is based on competitive bidding. This order could be value at around Rs 70,000 crore at today’s prices.

Although several news are floating around P75I submarine with AIP. It has not come to the order book yet. Also ToT may bring lots of hindrance. Current submarine capacity of Mazagon Dock is 11 mentioned in presentation. Submarine capacity is not looking healthy as per the screenshot. All order book is queued in shipbuilding.

1 Like

Your points are correct.

But , I have an update

(1) The P75I project order is not built in current order - the order value is 75000 crore.

The plus point is that the competition was expected from Navantia - L&T , which no longer exists now. So the overhang is over.

This submarine order would be picked up by only by Mazgaon dock.

(2) Capacity expansion - i believe it is on track

2 Likes

3 Likes

@1957 , hi Om, Just a novice doubt…In concall, management is talking about 1.25 lakh crore worth of order expectations and if export and private orders included, they said may be 2 lakh crore orders expected. If that is so, then why they are saying revenue growth will be around 10% in coming years, while if we consider 1.25 lakh crore also, then revenue is becoming 10 times in next 3-4 years…What is lacking in my understanding?

1 Like

Order book (₹1.25–2 lakh crore) reflects contracts to be executed over many years, not immediate revenue. Revenue is recognized only as work is completed, and shipbuilding projects typically span 5–10 years. Management’s 10% revenue growth guidance maybe due to gradual execution, certain capacity constraints, milestone-based nature of defense contracts etc. So annual revenue rises steadily, not in proportion to the total order book value.

5 Likes

@Jadewade , Totally agree…

. And during initial Phases, while design and prototyping, may be revenue Recognition is slower…but still I feel Management is too much cautious and downplaying the growth to the extent that its creating doubts in the minds of investors…![]()

![]()

3 Likes

@Mudit.Kushalvardhan @Jadewade

Agree with your views.

Sub-marines take years to build and deliver.

As of today , there is no competition for MDL as far as newer class of submarines are concerned.

.

L&T with Navantia from Spain had given a proposal for P75I project worth 75000 crore.

Finally MDL -ThyssenKrupp Germany was approved after extensive testing.

These submarines are to be delivered for next 10 years.

MDL had capacity constraints and they tried to do some subcontracting in the previous quarters whereby the quarterly performance got affected. Now with collaboration with HSL and capex plan , they want to increase their capacity.

So, the quarterly performance of defence shipping is always lumpy..it is not like IT companies where we watch QoQ incremental performance..

What we need to watch out is Year to year performance.

5 Likes

Many times clients wants to lock the prices now with limited variability and ask for staggerred deliveries

Mazgaon Dock buys controlling stake in Colombo Dockyard

India’s state-run Mazagon Dock Shipbuilders Limited (MDL) is acquiring control of Sri Lanka’s Colombo Dockyard PLC in a USD 52.96 million deal—an aggressive move aimed at expanding India’s maritime footprint and blocking China’s growing influence in the Indian Ocean.

The takeover, MDL’s first international venture, includes a mix of primary capital infusion and share purchase from Japan’s Onomichi Dockyard Co Ltd, which had owned a 51% stake. With the Japanese firm pulling out and Sri Lanka’s dockyard in financial crisis, the Indian government stepped in, recognizing the strategic vacuum.

3 Likes

2 Likes