The buyback is just in lieu of dividends. nothing much to read into it.

5 Likes

Business:

- Automotive has picked up 80-85% since covid.

- Revenue from operations is Rs.125.75 crores, Profit Before Tax: Rs.26.19 crores for the quarter ended.

- Product approval received from BMW.

- Automotive companies are doing well all around the world.

- The government has put 10% extra duty on imports.

- Resin (raw material) prices are going up & Mayur is already prepared with good stock.

- Mayur has increased increased prices by 5% in October then another 7% recently and going forward, it will increase it by 5%-7%.

- Revenue split by segment: Exports- 22 %, Domestic- 78%

- Export general: 9%, Export OEM: 13%, Domestic OEM-19%, Auto Replacement: 22%, Footwear: 26%, Furnishing & others: 7%.

- Total Volume: 58,44,868 meters

- Approved by Volkswagen and supply will start from March or April next year. Quantity for the order: 30,000-40,000 meters per month.

- Supply to Mercedes will also start by the end of next quarter.

- Approval has been received from BMW but it will begin from FY22 onwards.

- 6 PVC Lines Capacity: 27 to 28 lakh meters per month depending on the product mix.

- Backward Integration Plans: Mayur has 40 circular knitting machines. Ordered warp knitting machines and the usage will start in the next 4-5 months. Also ordered foam lamination, this costs a lot of money when done through outsourcing and it will save you around Rs.30 on freight cost only. Foam lamination will be ready soon.

- Trying for micro-fibre as it is very expensive & starts minimum from $78 wheen you make a product.

Management:

- Mayur is getting repeat customers.

- In the 5th linee, Mayur has made 45,000 meters & generally it is 27,000-28,000 meters.

- PU Price: $12 to $15 per meter.

- Mayur is the only the 2nd company in the world which is working on PU for the automotive companies.

- Plans to enter to automotive, footwear & furnishing with PU going forward.

- It will cross 2.8 million meters.

- Profitability per meter was Rs.40-42 in 2019 & this will increase going forward.

- Shortage of raw materials has led to the price hike.

- Break up of Auto & General exports: Auto 13%, General: 9% (Total Exports: 22%)

- Gwalior Project: Most of the PU plant is completed except technical commissionioning.

Risk:

- Delay in orders.

- Volatility in raw material prices

- Industry slowdown

20 Likes

I have visited local office few months back. Few points noted from interaction:

Company has started approaching customer’s for PU synthetic leather from last one year.

Around 600 customer’s have been approached by sending e mails/ppts.

Company has been getting enquiries. Few customers sample quantity has been sent.

Customer’s are ready to buy from Mayur once we start producing. They are all importing from China. PU leather is mainly for premium /super premium segment. Subcontractors of footware companies like Adidas are ready to buy from us.

Tamil Nadu /Kerala are big hub for leather. Company has appointed one guy in Chennai who is exclusively looking to market PU leather.

Regional office looks after overall south market. Have distributors in other states.

PU leather is costly and end product price will go up.( Comparison: if natural leather cost is Rs100, PU will be Rs 60 and PVC leather is Rs.30)

We need another six months to get big orders for PU leather.

Margins will be better. Company doesn’t sell without margins and better quality. Because of which Mayur has lost customer’s in the past.

30 days of credit for customers in general.

90% of South India market for is from footware companies.

Customers will be different for PU leather (not the same pvc leather customer’s)

Discl: invested

26 Likes

pls share the link of earnings cal transcript

very rough notes Q221. apologies, moderator can delete if inappropriate

India automotive market doing very well…picked up 80-85% ?

footwear hasnt picked up

If dec/jan good…full year…should be 10-15% down for fy 21.

in Europe…

i am very hopeful…things will be ok. in last 2-3 months…traffic jams, fully packed. the way auto sales is increasing…ppl are spending money. i hope things should be alright

Auto is doing good as trains, busses not doing well. Dec/and Jan are crucial. should continue to do well

footwear not doing well. ppl in market buying essential things. ppl not going for holidays, marriages…very quiet manner. marriage season…ppl go out…buy clothes, footwear…that sales is down.

footwear : 80% down…inn q1…importers had imported from china and had stock. now PU…isnt imported…as govt has put 10% import duty. ppl are waiting for their stock to clear. will take 6 months time for PU to come to right direction. from price point of view…no one will order from china…now 10% import duty…additional. so total 20% additional cost for imports. price of RM been increasng…PVC resin and PU prices goinng up. chinese are also increasing their PVC and PU leather cloth. due to covid…plastic gloves sales very high. foretunetly we have good stocks. 5% price hike and now 7%…price hike again we did. in dec also 5-7% price increase we will do.

exports : 22%; domestic 78%. 9% export general, 13% auto oem

19% auto replacement, auto oem : 26%; 26% footwear; furnishing ; 7%

gross margin : dependent on sales …gross margin is low…as sales is down 11% in q2. q3 will be good results…gross margin in q3 will be better. our RM cost is same.

ebitda margin should increse when sales. inn q3…we will come back to old margin if things continue how they are

VW will supply in March /April…with 30-40k meters…at 500 rs a meter. Mercedes will also start by end of next qtr. BMW is approved …will start in 2022. we are working on Ford & chrystel. fy 22 should be much better. i see very good market of exports.

lot of footwear cos coming from china to india.

PU : our product has got accepted whoever used it. whoeevr we supplied are repeating. will take 12 months to establish. once product is available …no one will import as no need to keep stocks…

Auto motives cos take a long time…VW will start in Oct…we said…delays…for embossing role…now i am sure within next 3 months must start

in PU we made 45k meters…in one day…versus 20 k . Ford & Chryseler : $12-15 per meter. we are second co. only who is working on PU…

KOREAN’s very slow

PU : working on footwear, leather goods. coagulated PU. wherever we selling PVC…we will sell PU. no one was giving right product in PU, our best technican we hired in Taiwan cannot come to iNdia. in last 2-3 months…we have spent lot of money…making all products…we are making 70-80%

we did 28 lac meters in fy 19 per month. now 2 orders VW and Mercedes…30,000 meters a month…should you surpass 28 lacs…in fy 22. yes…definetely. incremental 7 lac …higher realisation …rs.42 earlier in fy 19…per meter profitabulity. yes profitability will increase

we have 6 PVC lines…max vols : 28 lacs per month (min 27, max 28).

7th PVC line :

i am trying to move my customers from PVC to PU…; China moved PVC to PU. my competition will be less…and my compettiion will be less. we are in very technical products. Footwear…nothing extraordinary innoavation left in PVC. hence i am focussing on PU . i am focucsed on value added and different products…takes time.

PU we can make 400,000 meters per month. revenue : 100-125 cr annual revenue…1 machine…with full capcity what we have. now we are doing 35k meters per month…but incresing… last month increased 10k…next month should go to 50k. This material footwear ppl for exports. things will pick up after 15th Jan

MG Hector order : on goinng…no reduction. we are the only supplier

in 2008 : auto business was fully down for 1.5 year.but footwear was doing well. footwear biz hurt only due to covid. Bata is working with 50% capaicty utilisation. this is temporary

will take us 2 years to compete with CHina in PU

why you raising prices. PVC resin prices in very short supply…hence we are raising prices

realisstion : 558 rs…has dropped sharply ?

No one can raise price…due to demand…there is big reistance to raise prices.

most exports to US. Auto exports : mainly to US ; General exports to all over world

Exports general : 9%; exports OEM 13%…total 22% of sales exports

product with microfibre : product starts with $8-9…then goes to upto $12-20 ?

my target is to make PU chemical myself…so i can control everything…on products, and quantity. we started with 4 machines…now 36 machines…goinng on automatically…?

in next 2 years…i will do all kinds of backward integration…we used to $2 a meter perforation…now we doing in house. if i am selling at x price…competitiors will come in. how to increase price, reduce costs…to mainntain margins …always thinking

capex : i m doinng it gradually.

9 Likes

hi All, sorry if its not value add. recieved email from mayur on the buyback. since its a tender route, how can i tender the shares online ( from zerodha/hdfc ). will i be able to do that online or have to do physically submit forms.

is it the same process as below link for tender route?

1 Like

You can do it in Online in both zerodha and Hdfc securities. In HDFC APP there is no option but in website it’s available for buyback you can look into that.

1 Like

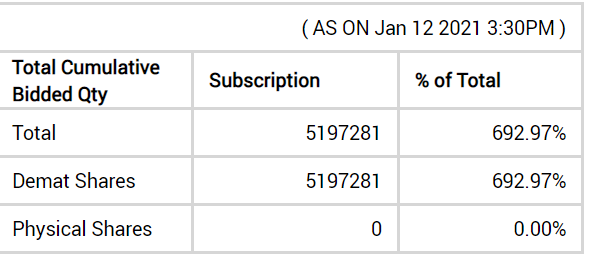

Hi All, With the buyback in progress, any idea on acceptance ratio for retail during buyback. With only upto 750000 shares for buyback, the entitlement was anyway pretty low.

Per current data available on BSE, the total number of tendered shares is slightly above 40 lakh. This is about 10% of the total shares outstanding. If the number of shares tendered does not increase significantly by end of the day, the small share holders are likely to get a substantial portion of their shares accepted.

AJ

Thanks. Since buyback is limited to only 7.5 lacs share and current subscription being close to 52 lacs, chances of anything over entitlement is low. Promoters too participated in this buyback.

Hi, As per my understanding this is not exactly how this works. We cannot go purely by the number of shares tendered - it depends on actual number of share holders who tendered their shares. Usually a large number of share holders wont participate in buy backs - not because they dont want to, but they are just not aware of the process/ some times not even aware of the buy back being announced by the company - this is very common for share holders who are elderly and not tech savvy - note that the companies are not issuing physical letters announcing buy backs anymore - shareholders are just informed via emails and for a person who doesn’t check his emails regularly, it is most likely a missed opportunity. Secondly, while the buy back letter defines the number of shares eligible for buy back - share holders are allowed to tender all of their shares in the buy back window - again most share holders are not aware that they can do this. Usually the number of share holders who participate in the window remain below 80%(while i dont have any data to prove this - this is a general observation i have made based on my experience over the years and you should be able to get the data if you do some research) and because of this the eligible share holders who have tendered all of their shares likely get all/ most of it bought back(especially if you are small share holder as the rule favor them).

Disclosure: I’m a small share holder and can confirm the number of shares accepted in this buy back once announced.

AJ

4 Likes

The acceptance ratio for small share holders is about 8.4%. I have computed this based on the number of shares tendered by me and accepted by the company. The original entitlement as communicated in the offer document was 2.6%.

AJ

how to check how much accepted

Mayur Uniquoters Q3FY21 concall notes

- From September 2020 month, the OEMs industry started doing well, and auto sector is now back in demand, both festive and tourism in auto sector continues in current quarter also.

- Consequently, in quarter 3 has improved our overall business performance in current financial year FY '21. Our sales revenue increased by 47.67% as compared to last quarter and 31.06% of previous year’s quarter. We are expecting to achieve the same pace of sales volume in quarter 4 of FY '21 also.

- in next 3 years, we are expecting the increase in sales of automotive sector within – from 75% to 100%, hopefully.

- I’m pleased to share that your company is already approved by Mercedes-Benz for supply to their South African plant. The products supplied from U.S. India also started for their new model in next quarter. we have started supplying to Mercedes, and I hope that things will go all right definitely. And within 1 year, once we are fully convinced with our reserves, they are willing to transfer some of their USA business also to us. our volume in the Mercedes will be also between 30,000 to 40,000 per month.

- The product approval from BMW is also received by us. We are working very closely with BMW also, but their new model, which will start in '22, they have approved us. The supply may start from the end of '21 or beginning of '22.

- we have been selected by Volkswagen India, and they have approved of material, which one was imported from Germany till now. Now we hope a very good business, close to 30,000 to 40,000 meters every month from – maybe first quarter end of the next year, maybe from May or June 2021.

- Now MG Motor. This is also a new company, which has started buying from us. They are buying 100% from Mayur, and we expect good future from them.

- most of the PU plant project activities are completed except some civil and site development works. The small supplies order and dispatches also started for PU plant and expected to increase gradually in coming months. PU sale in last month, we had a good sale, INR 1 crore. Quarter 3 is INR 2.5 crores.

- now PU is becoming gradually popular in automotive industry also. We are working very seriously on automotive setting material and other materials in PU to replace PVC because PU is more environment-friendly compared to PVC. And the prices are also very, very high, like it starts from $15 to $20 a meter. One of the German company is supplied at the moment and maybe Mayur will be second in the world to start this new business. We have got a support from FCA USA to make this material. They are very eager. Once our material are approved, they may start working with us.

- all of you knows the China problems. So a lot of business are coming back to China – from China to India by big manufacturers. So many companies are coming in, and we hope that more and more will come.

- seventh coating line, we have started fixing. And definitely, by end of March, we will start seventh line. We’ll get the capacity of More than 6 to 6.5 lakh meter per month. Because this is a bigger machine with bigger oven and bigger width, so we will get minimum 6 lakhs.

- Footwear also is improving but not at that speed because one of the reasons automotive business is increasing is because of this COVID, people have stopped moving in the like public transports. So many people who can afford that started buying 4-wheelers, 2-wheelers. That’s why it was also improving.

From November, we are seeing a good sign. And in fact, in footwear, this quarter compared to last year quarter, our sales have increased. By volume – 14% compared to last year third quarter. So the sign is improving. - I think we should be able to do at least INR 50 crores to INR 100 crores in next 2, 3 years’ time from PU plant. Now things have started picking up. Now you see the biggest problem in PU in lower product today, you see in India everywhere, 70% market is for lower grade, 20% is medium grade and 10% – 7% to 8% for high grade. I’m not entering in lower grades because in lower grade, you will make nothing. So I’m concentrating on medium and medium high grade and higher grade.

- We talked about setting up a plant in USA. Any nearby idea or any firm decisions from when we can think of it or?

Suresh Poddar

So you see, I have to expand the business first. Today, at the moment, we are doing export OEM about 180,000 to 175,000. So I will first bring it to at least 400,000, which we are doing and hopefully will be done. And as soon as I see that okay, this is happening, which will happen, then we will start – have already started working on seeing the land and sites and all that. We have already started working with USA, government and what kind of a benefit they can give. This all – preliminary work has started.

Regards

Harshit Goel

39 Likes

It seems that the Mercedes and BMW orders have opened the floodgates for Mayur and a lot of other OEMs are now seriously considering them.Margins should hold steady here,if not improve.Poddar ji’s hard work of so many years has begun to pay off.If one had to summarize the concall one can say,“The Peacock is dancing again”

7 Likes

Taken price increase… Poddar sounds very upbeat!.. https://twitter.com/Nigel__DSouza/status/1361939520178900993

3 Likes

Lamborghini, Mercedes Benz to post record numbers in 2021

1 Like

Investor Conference Call Highlights (From https://smartsyncservices.com/mayur-uniquoters)

- The product supply to Mercedes Benz’s South Africa plant will start within a month.

- The 7th PVC line is still commissioning and is expected to start production at end of July.

- Currently, the company is selling around 40,000-50,000 metres of PU but the breakeven level is at 2,00,000 metres.

- Demand from US auto OEMs has been down as many players are reducing their production targets due to the IC chip shortage.

- The margin profile is expected to stay up as the product mix shifts towards PU. The management has stated that the adoption of PU is gaining momentum in USA due to it being environmentally better than PVC and more cost-efficient than real leather.

- Although the material costs have gone up due to the production of PU, the margin profile has gone up even more which is preferable for the company.

- EBITDA margin for FY21 was at 24%. Volume decline in FY21 was around 8-9% YoY.

- Mayur sold almost Rs 7-8 Cr of PU in FY21.

- The management assures that the demand from global OEMs is indeed intact but has been delayed due to the chip shortage and will come back up once it is sorted.

- The company will start supplying 30,000 metres per month to Mercedes Benz at the start and it expects the volumes to rise to 50,000 metres by the end of Q3.

- The company is not looking to expand the PU lines as the current line has a peak capacity of 4,00,000 metres but it is making only 30,000 to 40,000 metres currently. The management expects that this capacity should be sufficient for growth for the next 1-1.5 years.

- The company is looking to make PU resin and will require a capex of Rs 150 Cr to set up a facility for it.

- The company is now in talks with a South Korean company to make a JV with them for coagulated PU used for automotive companies. Coagulated PU is mainly to be sold to South Korean OEMs as most of the OEMs from USA use solid PU only.

- The sales breakup was 32% export and 68% domestic. In terms of industry, sales breakup was at 8% for general exports, 24% for export OEM, 13% for domestic OEM, 21% for replacement, 33% for footwear, and 1.5% for others.

- The management states that there is no proper competitor for Mayur in India for the OEM supply and there are very few companies making PU for auto in the world.

- Mayur is currently pitching for Chrysler and once the process is over it will start approaching domestic auto OEMs.

- The PVC capacity for Mayur is at 3.15 million metres per month.

- The company sold 79 lac metres in Q4 & 2.31 Cr metres in FY21.

25 Likes

Screener shows sales have decreased while inventory and receivables are increasing. They compensated by getting higher payables. Mayur is B2B company but inventory trurnover is low at 1.87. Main problem is they are in industries where inventory turnover is low.

Very true. The care rating report also mentions that. I am betting on the forays into the US and European auto market outcome. https://www.careratings.com/upload/CompanyFiles/PR/Mayur%20Uniquoters%20Limited-12-23-2020.pdf

2 Likes