As per Q3 FY’20 concall, supply to Mercedes may start from Q4 FY’21 onwards.

Yes, there have been delays due to which the stock has corrected a lot. But going forward do we see now an increase in earnings (post COVID-19) and re-rating of the stock in next few years.

Vikram:

I assume that you have done a deep dive. If not, please do so as hope may not help when you have skin in the game. The report shared by @vikasbargale is created by the same organization which conducted Q3FY20 Con call. I do not follow the business but had a quick glance, thanks to our beloved Screener.in,and the numbers looked good except lack of SALES Growth.

AR FY13:

The company is likely to enter European countries in a huge way.

Concall Q3FY20:

Your company has already approved by Mercedes Benz for supply to their South Africa plant and product supply is expected to start for their new models

from Q4 of next financial year 2021…The goal post is another 1 year ahead and that too is an open statement.

All the best.

2 Likes

Good to see that after so many years, investors have started to talk about this script. I have also started a small position here. Here are the main points for me –

-

Mayur is the market leader with strong cash position and return ratios. So it can handle covid-19 related financial setback. Can other competitors handle it? I guess few can but few may not. So going forward less competition.

-

The PU plant started operation ( yes after changing goal post many time). As it will replace the import from china, I think generating sales and profit should not be that tough. How much profit and sales growth? I don’t know. Need to keep eye on the numbers in future. As per management, they don’t expect much profit from here in next 1-2 years.

-

As od today i.e 24’th March 2020, market cap is around 650 cr and avg PAT of 75 crs for last few years. It has some cash in book. So actually we are getting it around ~8 PE even if sales and profit don’t grow. I feel most of the negatives are factored in the valuation.

-

Supply to Daimler or Marcedes: I don’t know when it will happen. I don’t consider it in my calculation at all.

-

Another facility in south India: Same as #4.

If point #4 and #5 happens, I think mayur stock will be rerated. But investors don’t have much faith on management due to multiple goal post change. Successession plan is not at all clear. The son-in-law is not that knowledgable as per many.

Keeping all negatives and positives, I have started my position here. If sales and profit grows double digit from next FY, i will slowly increase the allocation.

2 Likes

If you listen to Q3 concall promoter focus more on premium and high margin business which is PU segment. He is very optimistic and has seen many business cycle he told in the call. PU plant plant under test stage, Holding small position. Not added any position in the recent correction. Waiting for the situation cooled off.

Dis. Invested

1 Like

@zygo23554 and @ayushmit :

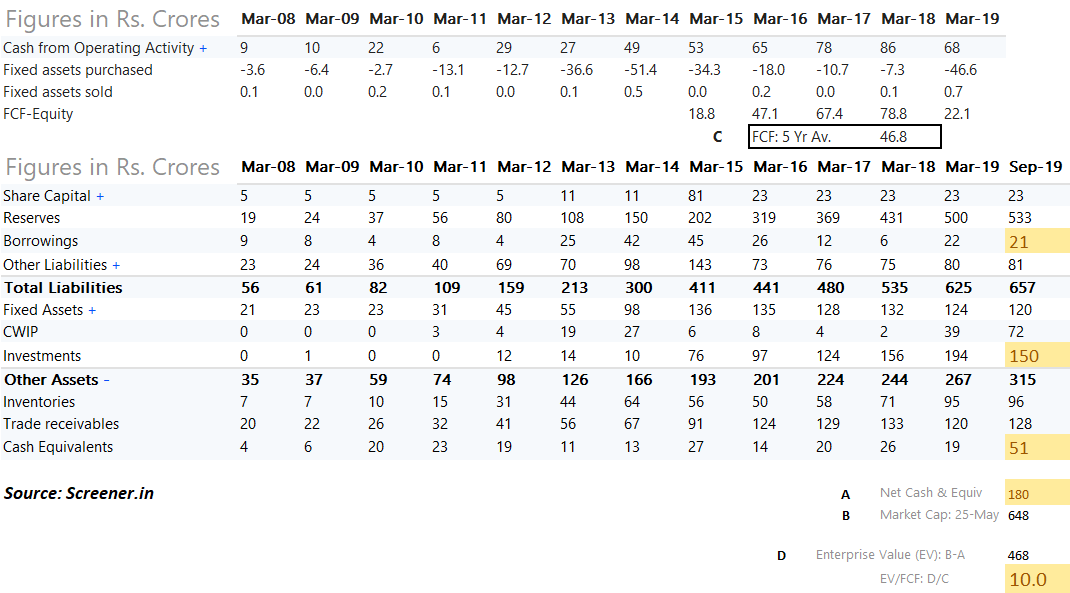

Request you both to share your evolved thoughts on this business. The market does not seem to be in a mood to appreciate the improved FCF capability of the business in the last 5 years. As of today, the business is available at 10X of EV/5 Yr. Av. FCF besides the optionality of returns on PU plant investment, and supply to European OEM.

My thoughts on the succession issue of Mayur:

In my opinion, the key-man risk is the highest in businesses that by their nature see a lot of change. For example in IT companies, consumer technology etc. Also companies which have high R&D (you need to figure on what to do R&D, how much to spend, upside potential etc) cause you don’t know before hand if that spend will yield any result. Next, in micro caps or start-ups, where the business model is being figured out along the way and there are many inevitable twists and turns. Also, in an industry like banking where the leadership has to decide on who to lend, at what rate and how to cover for risk

Coming to Mayur - to me, it is a simple business. Make artificial leather. The product (i.e. high quality artificial leather), plants and processes have already been laid out. The main job of the key person now is to respond to competition (price), identify new industries where this product can find application in and satisfy existing clients with a quality product & service.

Hence in my mind, the job now is less visionary and more execution based. The risk of the promoter not continuing in business still remains but these points make me feel that it may not be as bad as people think

7 Likes

In this interview, management reveals that footwear revenue is significantly impacted due to demonitization. It looks Mayur supplies to unorganized sector in footwear. I also had a similar question in mind as why this company is struggling to grow its revenues when Bata and Relaxo are having decent revenue and earnings growth.

1 Like

Is there any other way that they will be able to make up for the loss in the unorganized footwear sector. I work in footwear and know that there is no chance of revival of the unorganized footwear sector which is the main consumer of PVC in footwear.

2 Likes

GOOD NOS.PU PLANT COMMISSIONED MAKING MUL ONLY MANFR IN INDIA,ADD ON PU FROM CHINA INCREASING BENEFITTING MAYUR,

4 Likes

@Vivek_6954 but lower demand from Auto going forward will impact the growth in near term right, possible more than offseting benefits from PU plant?

2 Likes

Why hasn’t their depreciation gone up after commissioning the plant?

1 Like

Maybe in short term but bagging Mercdes as a client after years of efforts speaks volumes about tenacity & quality of Mayur.

Good growth coming back from 2 wheelers & 4 wheelers in India besides footwear sector.

PU plant can be a game changer due to increase in ADD & consumption moving to make in India production from China.

Do listen to concall for all queries raised here.

invested.

4 Likes

Mayur Uniquoters Q4FY20 Concall Is he back?

Business

-Company recorded a 12.7% revenue growth YOY

- There was little improvement in Auto OEM demand in Q4FY20, recovery was hampered by Covid outbreak.

-Product supply for Mercedes Benz, South Africa to start from Q1FY21. Expecting approval from BMW soon.

-Pu plant has completed the trial run and is commercial now. Despatches started in Q4FY20.

-Expect Pvc plants operating at 35-40% utilisation in July. OEMs guiding for normalcy in Q3FY21(difficult to believe)

- Cash flow have received 75 crores out of the 138 crores that are outstanding.

All about PU plant

-

China is the only competitor in PU, government has increased the import duty by 10%. Earlier on Chinese Pu it was 10%, now 10%+10%+surcharge= 22%

-

We are doing massive sampling from the PU plant.

Results expected to be seen. -

Our PU cost is higher than China mainly due to Pu resin is imported from China.

-

We are manufacturing the fabric and Pu resin we will start manufacturing soon (12months)

-

There was a 2 year delay in PU plant due to lack of water availability. We went to MP, as Shivraj Singh Chauhans govt gave a lot of Sops like cheaper electricity etc. We set up the plant there. (Gwalior)

-

Only 4 manufacturers of PU in the country including us. Other 3 are really small and have only 250,000 metre capacity.

Mayurs capacity (600,000mt)

-Looking for Value added products in Pu. As competitors sell cheap PU. Very close to tie up with a Korean company for technical know how of PU for automotive. Eg- for Ford motors we will be the first people to supply PU for auto, as 80% material is approved.

- Have hired a guy from Taiwan who has worked in the last 25years on making any kind of PU product.

Pvc

-

Per meter realization improved from rs 500 to rs 550 as OEM export was very good in this quarter and we added more products.

-

OEM business has higher margin, especially the export OEM.

-

In Fy 20, 55% sales were from auto, 30% from Footwear. Rest from others.

-

Have 30-40 clients in the domestic OEM. Mainly working with Maruti, Mg motors, Hyundai (recently added), Mahindra, Tata and all the 2 wheeler players. Expecting to get Hero Moto as a customer in next 3-4 months.

Sale break up

-

Export growth in Auto OEM of 76% in Value and 56% in Volume. Domestic OEM degrew by 3% in Volumes, but value was up by 6%.

-

Replacement down by 6% and total Auto OEM growth at 23%.

Management

-

Took us 7 years to get Mercedes Benz contract. We have taken market share from German competitors .

-

Professionalizing the company, daughter in law has joined. Recently hired people from USA, Portugal and England in research and development as they have more experience in working with PU.

-

Hiring a COO from outside as more or less very few people have R&D knowledge in India.

Risk

-

Key man risk of the promoter, he is Professionalizing now.

-

Underinvoicing of PU imports from China.

-

Footwear industry asking for concessions on PU imports. Have appealed the government to not provide it, as India is self sufficient in PU now.

-

Auto OEM demand crashing.

My view

After a long time, we have finally seen execution. Won’t blame the management as doing business is a difficult task in India. Near-medium term headwinds visible in Auto OEM demand. Still no other credible competitor in the same breath as Mayur in this segment. Mercedes-Benz contract is a big positive.

Disclosure- no positions, tracking to see how the execution goes.

19 Likes

Not an exact verdict of how polyurethane plays a dominant role in airless tyre :

However am sharing this article here because it adds value to this industry in field of polyurethane for tyre - currently the airless tyre are not being productionalized but seems good for the near by future - it will not be easy to tell demand raise on polyurethane and this will show up - am just resting the case on the table for future benefits

polyurethane - Artificial leather, Foam, Shoes, furniture, bedding, tyres, anti corrosion, gloss, carpet underlay and much more

2 Likes

Really bad numbers in Q1

Bad numbers with very low utilisation of newly comisioned PU plant is going to dent balance sheet significantly…

It will not really dent the balance sheet as they did not have losses. And, I think they have quite a lot of cash balance. Why do you say the balance sheet will be harmed?

2 Likes

Q1FY20 no major sales happened around the globe. OEM’s are under low sales volume. it will take some time to pickup demand. I believe another couple of qtr expecting muted growth.Let’s hope on FY21.

Disc: Invested

2 Likes

Posting Q1 FY21 results concall summary along with my comments.

Attended - Suresh Kumar Poddar - CMD and Vinod Kumar Sharma - CFO

Taken cost control measure in times of pandemic. Pandemic affected operations of company during the quarter and hence results are not comparable.

- Mercedez has approved products and supply to SA plant will start from last quarter of FY21.

- BMW approval also expected soon.

- PU plant project is completed expect DMF tower and production started from this plant.

- April was completely washed out, May little bit started bcs of the pandemic. From June Ops are recovering.

**Personal comment - **from voice felt that Mr. Suresh Kumar Poddar is not feeling well. Might be a minor health issue - Mayur has 50% business (read revenue) from automotive industry and increasing. Automotive industry recovering from June and this quarter will be much better than last quarter.

- Automotive approvals take much more time. Products get approved for new models and not existing models.

- BMW new model supply will start from 2022. Volkswagen India supply will also start from next year.

- PU plant samples are being provided to customers. PU material 90% is being imported from China. Hence supply chain was affected badly

- current stocks with customers will clear and new order will start in 3 months time.

- Mayur produces high and medium quality material. Do not compete with cheap quality suppliers.

- Taiwanese technician is at Mayur who is having 30+ experience for plant set up and production fine tuning.

- Within years time Mayur will be able to produce all type of Synthetic leather qualities that are being supplied form China.

- Good future and things will be much better from FY22 for Mayur.

- Q1 capacity utilization is 27% bcs of Pandemic. Q2 expected to be 60%.

- Cost control measures - executives took salary cut. Travel cost is drastically down. Mr. Suresh is supervising all costs and not even allowing Rs. 500 discretionary spend. At current times cost control is utmost priority.

- OEM export in July was at 70 to 75% and expected same for current month. Demand was weak in Q1.

- Its matter to survive for another 1 year and will see better future.

- Q1 PU leather revenue was minor - aprox. 50 lakhs.

- Total volume was 15.62 lakh mtrs for Q1. All products.

- Volkswagen supply we can assume 30K mtrs per month. 1 Cr revenue per year we can expect from Volkswagen India. They are buying form Germany at the moment.

- Mercedez will also be same volume but value will be aprox. 15% more.

- Kia is importing from Korea and Mayur not supplying currently.

- MG Mayur is supplying.

- PU material of price 2000 Rs/meter is being evaluated by customers. This elite material do not have much volume and will take time. Mayur is competent to compete with anyone on quality parameters.

- Depreciation is expected to go up after PU plant is operational. Currently, depreciation was down as PU plant was operational for single shift in last week of June for some time.

- COO (operations manager) for automotive division - search is going on.

- PU plant volume is expected from Sept 2020 like 1 Lakh meters per month. Value will be 1 to 2 Cr.

- Footware industry - China exits - Business environment is not conducive in India - quantity cannot be meet for the kind of supply needs of these global players. Taiwan and Indonesia are gaining more from these exits.

My Comments - Effective cost control measures helped company to prevent losses despite 75%+ revenue loss. Very competent and confident management and having clear view and required experience to play as a global supplier. Interesting area to watch will be export revenue share and improvement in margins because of gradual shift from quantity to quality approach and downward integration for the final products. Would like to hear more from Mr. Manav Poddar as the next flag bearer for the company and smooth succession planning.

Discl: Invested 5% of portfolio value.

19 Likes

Q2/FY21 Results - Decent numbers. Topline and bottomline are approaching YoY numbers. Q2 EPS is ₹4.41 compared to ₹4.83 last year…

Buyback has been announced - ₹400 per share - that’s a ~60% premium over the CMP! And the promoters plan to participate in the buyback. How do we interpret this huge premium?

3 Likes