Mayur Uniquoters AR2021 notes

- Mayur manufactures more than 400 variants of artificial leather from PVC polymer which finds application in footwear (shoes/sandals insole and uppers), automotive (seat upholstery and inner linings), furniture & fashion items (apparel).

- During the year the company started the supply to Daimler and has been awarded the supply approval from BMW.

-

Production capacity

PVC: 4.05 mn linear metre per month

PU: 0.5 mn linear metre per month - Plant Location

Unit-I: 4 Coating Lines situated at Village: Jaitpura, Jaipur- Sikar Road, Tehsil: Chomu, District: Jaipur - 303 704 (Rajasthan).

Unit-II: Textile Division and 5th, 6th & 7th Coating Line situated at Village: Dhodsar, Khajroli Link Road, Near Ratan Devi College, Jaipur-Sikar Highway, Tehsil: Chomu, Jaipur - 303 712 (Rajasthan)

Unit-III: PU Plant situated at Plot No- S-1 to S-30 and M-8 to M-13, Sitapur Industrial Area, Phase- I, Banmore, Morena - 476 444 (Madhya Pradesh) - Mayur has forayed into manufacturing of PU coated fabric by setting up a green-field project at Morena district near Gwalior, Madhya Pradesh. Under Phase-I, Mayur has installed 1 coating line (consists 1 wet and 1 dry line) with capacity to produce 0.60 LMPM of PU fabric. The Company has constructed building and other peripheral infrastructure for 4 coating lines considering the future expansion plans.

- Mayur, has a diversified clientele across various industries and caters to the synthetic leather requirements of reputed players like MG Hector, Maruti, Tata, Mahindra, ISUZU, Suzuki, Honda, Renualt, Volkswagoan, Hero, Bajaj, Piaggio, Sonalika Tractor, Lear, TS Tech Sun, Bharat Seat, Krishna Maruti, Sharda Motors, S.I. Interpact Group, Swaraj Auto, Polor Auto etc. among automotives and Bata, Paragon, Action, Relaxo, VKC Group etc. among footwear segment.

- Your Company is trying to enter the European and other export automotive OEM markets by targeting reputed customers and has received product approval from Mercedes Benz (Daimler) and BMW for their specific new car models. Mayur has already set-up its Wholly Owned Subsidiary named Mayur Uniquoters SA (Pty) Ltd, South Africa which will develop logistics to facilitate exports to Mercedes Benz.

- Volkswagen India, is expected to buy synthetic leather from Mayur.

- Despite the challenging business environment by the unforeseen impact of the COVID-19 pandemic, your Company was able to increase its market share and improve profitability through innovations, cost efficiency programs and expansion in distribution.

- The R&D wing delivers 90 to 100 unique samples in a working day.

- Futura Textiles Inc. was incorporated in State of Nevada, USA on December 20, 2010. The Company is mainly engaged in the business of retail and whole sale trading of Upholstery of PVC Vinyl or Artificial/ Synthetic Leather. During the financial year 2020-21 Mayur Uniquoters Corp Inc made investment of $ 2,10,000 in Futura Textiles Inc. and hence, it became Wholly Owned Subsidiary of Mayur Uniquoters Corp Inc.

- Mayur Uniquoters Corp.: Sales Rs. 96.70 cr (Rs. 110 cr) and PAT Rs. 2.92 cr (Rs. 5.64cr).

- Financial

- Company has completed the Buyback of 750,000 fully paid-up equity shares of face value of Rs. 5/- each at a price of Rs. 400/- per equity share aggregating to Rs. 3,000 lakhs

- Consolidated Exports Rs. 150 cr (Rs. 164 cr).

- Sales in USA out of total exports: Rs. 42.66 cr (Rs. 63.59 cr).

- Revenue from One Major Customer: Rs. 82.91 cr (Rs. 99.73 cr).

Q1 results

Key excerpt from concall dated August 5th:

Export OEM:

-

Automakers are facing the production problems at their plant due to semiconductor chips shortage globally. And our – that’s why our OEM sale is also impacted in this financial year and especially in Q1. However, we are hopeful to regain the OEM sales and the demand from the market back within the next 2, 3 months.

-

Suddenly because of the crisis, the sales has gone down, they have to close the business. Now in America, the situation is like this that they don’t have a car to have – to display in showroom. The demand is fantastic. Now it has started increasing from last week. Last week, the sales was improved. And now they say that by third week of August, we will have original sales.

-

There are 3 big interior manufacturer in the world who are spread everywhere in Europe, in America, in India. So they – all of them knows who supply to the OEMs. So they are the people who make the interior and supply to OEM. All of them we know and everybody is satisfied with us. But the problem is, until and unless new model comes, from the old model, it is difficult.

-

Fiat Chrysler: Previously our FCA business was hardly, say, 130,000 meters or 125,000 meters like that, which increased in January and February to 175,000 meters to 180,000 meters.

[My take - This is one of the key monitorable. FCA was going through a rough patch, looks like things are changing for better post moving under the folds of Stellantis.] -

Volkswagen: So Volkswagen business has already started, supply has already started. But from this quarter, every quarter, it will keep on increasing. And I think by the end of the fourth quarter, we will be able to do the whole, whatever we have predicted, because anything which starts it goes slowly. But by end of this year, we will be doing 100% what has been projected in the last quarter. This quarter also July we have increased. So it’s already on the path of increase.

[My take: Their initial projection is for ~40,000 meter, at Rs. 500/meter realization. Q1’ has not been very encouraging so far. May take longer than expected to reach projection.] -

Mercedes-Benz - your company is already approved by Mercedes-Benz for supply to their South Africa plant and product supply has also started with some quantity for the new models from this quarter.

Domestic Auto OEM:

- India is doing quite well. There is no issue in India. We have increased the prices also when the prices were increased, and they are giving us price increase also. So far as business is concerned in this year, I’m very much optimistic compared to last year. See, in last 2 quarters, it was fantastic sale in last year. And this April was the record highest sales in Mayur’s history. But again, that because of this pandemic, May and June were back. Now July had picked up. August is also picking up. So if there is no pandemic and I hope so, it will not be that bad what has happened, I mean the future is very good.

Polyurethane (PU):

-

More than 1 crore meter is being imported in India from China every month. So far as market is concerned, there is not a big issue. The only issue is pertaining to the malpractices, which is done in India under invoicing and all those. For that also, we are working. Already, we have filed the anti-dumping duty on PU resin. We had first hearing 4 days back. Now we are working very seriously on that because what is happening from China. China is the biggest problem. And then the problem is our country.

[ Must be referring to this ADD investigation. Also there was a reference to 10% interim duty during last call] - Now we have started PU also, which nobody is supplying at the moment in the automotive industry in export, and we are quite close. Maybe it takes 3 months, 6 months’ time to get approval. But once it approves, it’s a big business. I mean, $25, $26 like that, and we are very close.

- And once it is approved, then there is only 1 supplier in the whole world. So we are working on that also very seriously and hopeful that maybe in '22, we may start having this business also

- PU Value/Volume Trend - ~50,000 Meter, Last month, we reached INR 1.5 crores

- PU Impact on PnL - Including depreciated interest, it is around INR 90 lakhs per month loss.

- PU Customer Profile (projection): 75% same and 25% new

RM Cost Escalation Pass-on:

- The prices of raw material are increasing. PVC prices have increased by more than 70% to 80%. Plasticizer prices have been increased to 100%. And all these increases started from the end of the fourth quarter. So fourth quarter, it didn’t affected because we had a lot of material in stock. Generally, we have 45 days stock of these specific materials. So that was the advantage. We have started increasing the prices.

- we also increased almost more than 30%. We have increased more than 30% prices with this increase. So now since the prices have started going down, we have decreased 6% in July.

- See, we – all our general export, we have passed on this freight cost to them, and they are accepting, 90%, 80% are accepting.

- But so far automotive is concerned, they are very strict. So – but we have given them ultimatum that from this quarter – I mean, third quarter, this is the second quarter, from third quarter, if the things are not normal, we will increase the price. And they have to increase because so many supply – even leather cloth supplier, they are declaring force majeure because if you are not giving the supply – prices what the supplier will do? A force majeure

CapEx/Backward Integration:

- We are very serious that we had to fight with China. I think with China is only 2 things that all the fabrics should be in in-house and PU chemical also we have to start manufacturing. For that also, we have started looking for an engineer, who is expert – who are expert in PU, so that in course of time, we’ll start making PU also. This is necessary for the long term.

- We are making knitted fabric. Now we are going to start very soon, maybe in 1 year time, this warp knit fabric, then nonwoven, then PU also.

- CapEx plan in '22. Clearly, it will be around INR 25 crores to INR 30 crores.

Misc.:

- I’m less interested in top line, I’m more interested in bottom line. That’s why you will see the bottom line has always increased. Today, so far, top line is concerned, every 2 years, I can double myself. But what is the use of selling, if I get 3%, 4%, 5% margin. I’m not interested in those businesses.

- FY '22 volume, the way things are moving, what we have seen in July and what we are seeing in August, already orders have started coming in a good way. I think it should be better than 2021. '21, '22 must be better.

Thanks,

Tarun

Disc: Invested

Hi Tarun

Thanks for the summary.

With regards to the semi-conductor chip shortage, Mr. poddar seems to suggest that August onwards the situation has been better. But many in the industry are seeing this problem persist till Q1 of the next financial year. The reason, the situation is not so bad in India is because a few companies had created a buffer stock of semi-conductors. Wondering how Mayur will do well, when the PV & 2 wheeler segment will not have sales traction cause of the supply issues. Any thoughts on this?

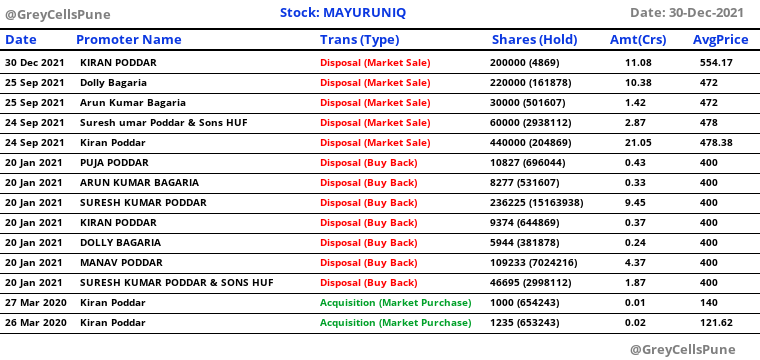

Insider trades

Growth seem to be missing on longer term, margins have also been on flat/downward trajectory.

Their fortune seem closely linked with OEMs , industry has multiple headwinds. Good promoters, impressive clientele, quality focused , risk taking, PU bet, need to see what coming Qtrs hold

Tracking position

Very good result by Mayur uniquoters

Mayur uniqoters qtr 2 results 111121 .pdf (2.7 MB)

Research Report from Sharekhan on Mayur

Mayur-Uniquoters-khan-13122021.pdf (259.0 KB)

Board meeting +buy back considerations

Some data points

Good parts

- Good cash balances close to 200 cr

- Last buy back was Nov 20 at 400( prevailing stock price was sub 300 then), this one could to be attractive levels too

- Part of promoter group sold out in Q3( nearly exited) - 2% type in last 1 Qtr

- Fixed assets have nearly doubled from 124 cr in 2019 to 206 cr now, revenues haven’t moved much ( 500 to 600 cr type) - in past have done 4-5X asset turns - Q2 had glimpse with 188 cr/qtr , possibilities of operating leverage playing out with auto mfg looking up

- Looking good on charts, recently took out ATH and consolidating thereabout

- Mgmt has successfully built relationships in major auto OEM worldwide - Mercedes, BMW - long drawn process and a kind of quality Moat with stickiness

- One of very few PU mfg in world - only one in India, significant Capex done already, utilization improvement scope

- Both end industries- auto and shoe - looking good( shoe reflects in Q3 numbers, Auto with semi conductor shortage going away should do better QoQ)

- Unorganised to organized play given large Unorganised base

- Rare Auto ancillary with margins of 25%, mgmt is clear about margins focused revenue growth

- Very focused and sharp promoter

- Opportunity size 8K cr+ per screener data

Risks

- Operating de leverage playing out since last 2-3 years with no growth

- Keyman risk with active promoter 75+, though hired COO and open to more professional hires

- Market perception given last few years flattish, reflects in institutional holding

Interesting case as it may be right at inflection point with good few years ahead, has been market darling in past glory days.

Invested with small allocation

Q3 results with Buyback details -

Results are decent given the issues with supply chain faced by Automotive companies. Buyback is for up to ~ 40 Crs. (about 2% of market cap). The premium is handsome (buyback price Rs. 650/-)

@sajijohn - How do you see the results and do you see - tendering in buyback a good opportunity?

When is the exact buyback window for retailers and what is the % available for buyback

Its not yet announced.

23rd Feb was the record date.

Buy Back Letter of Offer has been released today evening

(MUL_Letter of Offer - without tender forms and sh-4.pdf (486.3 KB))

Key call outs:

-

The ratio of the Buyback: (i) in case of Small Shareholders, 1 Equity Share for every 29 Equity Shares held by such Small Shareholder on the Record Date; and (ii) for Eligible Shareholders other than Small Shareholders, 1 Equity Share for every 79 Equity Shares held by such Eligible Shareholder on the Record Date.

-

There are 55,114 Small Shareholders in the Company with aggregate shareholding of 27,21,181

Equity Shares as on Record Date, which constitutes 6.10% of the outstanding number of Equity Shares. The reservation for the Small Shareholders will be 93,750 Equity Share. General Category shall consist of 5,31,250 Equity Share. -

Key Dates:

BUY BACK OPENS ON: THURSDAY, MARCH 24, 2022

BUY BACK CLOSES ON: WEDNESDAY, APRIL 06, 202 -

Assuming response to the Buyback is to the extent of 100% (full acceptance) from all the Eligible Shareholders up to their Buyback Entitlement, the aggregate shareholding of the promoters, members of the promoter group and persons in control post Buyback may increase from 59.43%, which is the shareholding as at date, to 59.51%

Thanks,

Tarun

Disc: Invested

Mayur uniquoters says

PVC Resin Prices Have Gone Up By 75% And Plasticizers By Over 200%

Have Not Increased Prices By Required Quantum

Expect Revenue To Grow By 18-20%

Margin May Contract By 400-500 bps

PU Plant Sales At 30 Cr PA Currently

Can Scale It Upto 75 Cr

Disc: Invested. This not a buy or sell recommendation

Relatively good result in tough environment

Mayur qtr 4 result 2122 .pdf (7.1 MB)

Monarch Networth Capital

Mayur Uniquoters | LTP:Rs363 | Mkt Cap: Rs1,598crore

4QFY22 Result - First Cut

•Mayur Uniquoters’ 4QFY22 consolidated revenue declined by 9.2% YoY to Rs1.6bn.

•A 9.4% increase in RM cost, led to a gross margin of 39% vs 49.4% in 4QFY21.

oEmployee cost declined by 7% YoY

oOther Expense also declined by 19% YoY

•EBITDA came in at Rs301mn vs a high base of Rs489mn in 4QFY21. EBITDA margin came in at 18.6% vs 27.4% in 4QFY21.

oDepreciation/other income decreased/increased by 2.7%/55% YoY respectively, oInterest cost declined by 73% YoY.

•The consolidated PAT came in at Rs249mn vs Rs347mn in 4QFY21. The PAT margin stood at 15.4% vs 19.4% in 4QFY21.

oThe consolidated EPS stood at Rs5.6.

Outlook:

•As mentioned before, 4QFY21 was an exceptional quarter which created a high base. We feel that volumes can only go up from here as the chip shortage has hampered new vehicle volumes for quite some time now. We continue to maintain our positive stance on Mayur as stronger volumes should come in from export OEMs once the chip shortage eases.

•On 20th May 2022, Department of revenue has imposed ADD on all (barring one manufacturer) imported leather from China. We feel that Mayur’s continuous efforts over the years in PU leather should finally payoff going forward as it should attain pricing power with quality.

•Currently, at CMP of Rs 363, according to our existing estimates, Mayur is trading at an extremely cheap valuation of forward P/E of 10.4x. We currently have a BUY rating on the stock with a target of Rs620.

Monarch will be hosting Mayur’s Earnings call tomorrow, 31st May at 2:00 PM, Dial-in Numbers: +9122 62801455/+9122 71158828*

Discl: Baised bcos of my holding

Annual Report is published!

My notes are below -

The company is in the process to expand its PVC coated fabric capacity by adding its seventh coating line at Dhodsar plant

Domestic clients -MG Hector, Maruti, Tata, Mahindra, ISUZU,

Suzuki, Honda, Renualt, Volkswagoan, Hero, Bajaj,

Piaggio, Sonalika Tractor, Lear, TS Tech Sun, Bharat Seat, Krishna Maruti, Sharda Motors, S.I. Interpact Group, Swaraj Auto, Polor Auto etc. among automotives and Bata, Paragon, Lancer, Action, Relaxo, VKC Group etc

The supplying to Mercedes Benz by Mayur has already startedin the year 2021. While supply to BMW is expected to start in soon.

With PU plant ramp up, commencement of Mercedes business,BMW business in future and VW India business getting traction, we estimate strong earnings growth in coming Financial Years

Now Mayur is also planning to enter into a retail business by setting up 100% Wholly Owned Subsidiary in India with the name Mayur TecFab Private Limited.(Is this diworsification?)

For FY21-22, Increase in Material consumed cost from 287 Cr to 402 Cr (~35%) - 45 Cr additional material left compared to last FY. Effective increase ~24% inline with revenue growth

Increase in other expenses from 66 Cr to 83 Cr (~25%) caused reduction in margins despite decent revenue growth of ~ 25%; Freight cost increase by ~ 54%, (20% of total other exp.),Power & Fuel cost increase by ~ 32%

(Hope the company will be able to pass on these increases to customers during FY22-23)

@sajijohn , @T11 , @harshitgoel - How do you company’s foray in B2C segment for luxury furnishing

Disc - Invested

Thanks for the comprehensive notes. I am adding some remainder points from the annual report.

- Global synthetic leather market size was valued at $34.30 bn in 2021 and is expected to grow at 8.3% CAGR from 2022 to 2030. PU synthetic leather segment accounted for 60% share in 2021

- Company is following TPM, TQM and lean management to improve efficiency

- Mayur has added a flame lamination machine (capacity: 47 lakh linear meter per year) to overcome product quality and delivery issues that it faced earlier when the process was outsourced. Flame lamination is the process of laminating flexible material with an open flame. This technique is used to seal materials such as PVC to foam and fabric without using additional adhesive

- Added 6th coating line from ISOTEX, Italy which is of wider width of 2 meters resulting in increased production with the fixed cost remaining the same

- Mayur Uniquoters Corp (USA): Supply goods to OEM customer in USA on just in time basis

- Dhodsar plant is Zero Liquid Discharge (ZLD) plant. Effluent water is treated in Effluent Treatment Plant (ETP) & RO plant & recycled in process

- CSR spends: 2.4 cr

- R&D: 8.5 cr. (vs 6 cr. in FY21). Delivers 90-100 unique samples every working day

- Trade receivable loss allowance: 4.5 cr. (vs 5.11 cr. in FY21)

- Employees: 495 (803 contractual), median remuneration increase excluding KMP was 5.45%. Remuneration increase was 17.17% for KMP

- Auditor remuneration: 46.71 lakhs (vs 38.47 in FY21)

- Share price: 336.9 (low), 635 (high)

- Number of shareholders: 57’031 (vs 28’667 in FY21)

Geographical breakup:

- India: 489.84 cr. (vs 361.61 cr. in FY21)

- US: 117.33 cr. (vs 42.67 cr. in FY21)

- Other geographies: 49.29 cr. (vs 108.43 cr. in FY21)

Disclosure: Not invested

Superb Q1’23 for Mayur. Both Revenue as well as Profit have almost doubled compared to respective quarter last year. Probably the uptick in Auto sales is providing good demand. Would be interesting to hear management’s narrative on growth drivers and outlook.

Disc - Invested

Mayur Uniquoters Q1FY23 Concall Update

(Nirmal Bang Securities)

Growth & profitability to resume on the back of (i) improvement in availability of automotive chips for PVs, (ii) new client additions in Auto (iii) bounceback in footwear industry and (iv) Easing RM pressure

Outlook: Positive in long term

• Revenue came at Rs. 204 Cr (+26% QoQ, +73% YoY) vs QoQ Rs. 162 Cr, YoY Rs. 118 Cr

• Gross Profit Margins came at 40.6% vs QoQ 38.9%, YoY 40.8%

• EBITDA Margin came at 17% vs QoQ 18.6%, YoY 14.9%. EBITDA Margin has declined sequentially despite improvement in gross margin due to steep increase in other expenses. Co attributed the increase due to high freight cost.

• Supply to BMW will start from Q4FY23.

• Co has not been able to scale up revenue from traditional customers like GM & Chrysler since many years as they are preferring production lines which are in US.

• Co has forward integrated into foam manufacturing.

• Will expand furnishings dealers from 75 currently to over 1,000 in coming years. This segment has good margins.

• On succession planning: Son in law of Mr. S K Poddar is already working in the co. His son has also started working together and will take around 1-2 years to groom him.

• Current utilisation is 70-72%. Co expects to reach full utilization in 1.5 years. It takes 1 year to put up a line. Putting up one line of PVC costs Rs. 30 Cr in a brownfield site while in a green field site it costs Rs. 100 Cr.

• Revenue mix during Q1: Exports general 50cr, exports OEM 32cr, domestic OEM 36cr, domestic replacement 44cr, domestic footwear 63cr, domestic furnishings 6cr.

• PU revenue during Q1 was 7cr.

Stock is trading at P/E of 16.7x FY24E EPS