KIRAN PODDAR who is promoter of company is daily buying shares worth minuscule queantity ( in just few thousands). Is it just to get his name in insider trading updates so that people tend to believe promoter is buying so let us buy?

3 Likes

Mayur Uniquoters AR 19 notes

Company will commence PU plant production at the end of Sept 2019

PU leather has good elasticity , high tensile strength , high abrasion ,etc. These properties have played a role in improving PU’s penetration.

Last year was challenging – Due to crude oil price increase our RM costs increased as 80 % of our RM is linked with crude

Due to weak demand we had reduce our finished product prices also.

Revenue was 591 cr vs 581 cr last year

PAT was 89 cr vs 95 cr last year

Current capacity is 3.05 million metres per month

The market for global synthetic leather has witnesses a noticeable growth in the recent past and is expected to remain growing over the coming years.

Increasing use of artificial leather in footwear , increasing awareness about animal rights can lead to growth in synthetic leather industry.

Synthetic leather is a cheaper option to artificial leather

Artificial leather is finding increasing use in footwear and automotive industry.

Revenue from top customer – 90 cr ( approx. – 15.7% of sales)

Threats to business include – foreign currency fluctuation, competitive intensity (fragmented industry with huge unorganized market also), unfavorable crude price fluctuations

Our R&D team is continuously working on creating new products and delivers upto 90-100 samples per day.

Money spent on R&D = 7.42 cr.

the stock has corrected a lot in the past one year. the company is available at a PE of 12 , which is on the lower side . With the PU facility coming on line the company might deliver some growth in the top line . The management has bee continously buying some shares from the open market since a year in small quantities. They have bought securities worth 1.5 cr around in the last one year.

Disc - Invested

11 Likes

Fundamentals have not deteriorated. But, the stock price is under sharp correction as the auto sector is witnessing slowdown.

The price chart shows sharp downward momentum.

I would like to see some consolidation, before getting in.

2 Likes

How much of information available in public domain about Futura aquisition of Mayur? https://www.equitybulls.com/admin/news2006/news_det.asp?id=247665

The news article says “Mr. Arun Kumar Bagaria, Executive Director of Mayur Uniquoters Limited is also holding directorship in Mayur Uniquoters Corp (Acquirer) and Futura Textiles Inc.(Target Company).”

My question is since this aquisition appears to profit one of directors based on what is stated in above news report. Annual report says the following:

"I am pleased to share that your Company has made further investment of 13,700 Shares having face value of USD 1 per share at a rate of USD 73 per Share (face value USD 1 + Premium USD 72) in our Wholly Owned Subsidiary (WOS) i.e. Mayur Uniquoters Corp.

I would also like to share that Mayur Uniquoters Corp, WOS has made investment of 4,50,000 Shares having face value of USD 1 per share at a rate of USD 1 per share i.e. equivalent to 68.18%ofpaidupsharecapitalofFuturaTextilesInc.Afterthe acquisition of 4,50,000 shares Futura Textiles Inc became Step Down Subsidiary of Mayur Uniquoters Limited."

So the aquisition cost of Futura must be around 3 crores at 70 Rs per dollar. Further annual report states turnover of this company to be 73 laks and profit to be 16 laksh. Overall these numbers appear to be non consequential for a company with 1000 Cr market cap and 80 Cr profit per annum. So i am assuming nothing fishy here. Pls correct me if any of you have different opinion.

4 Likes

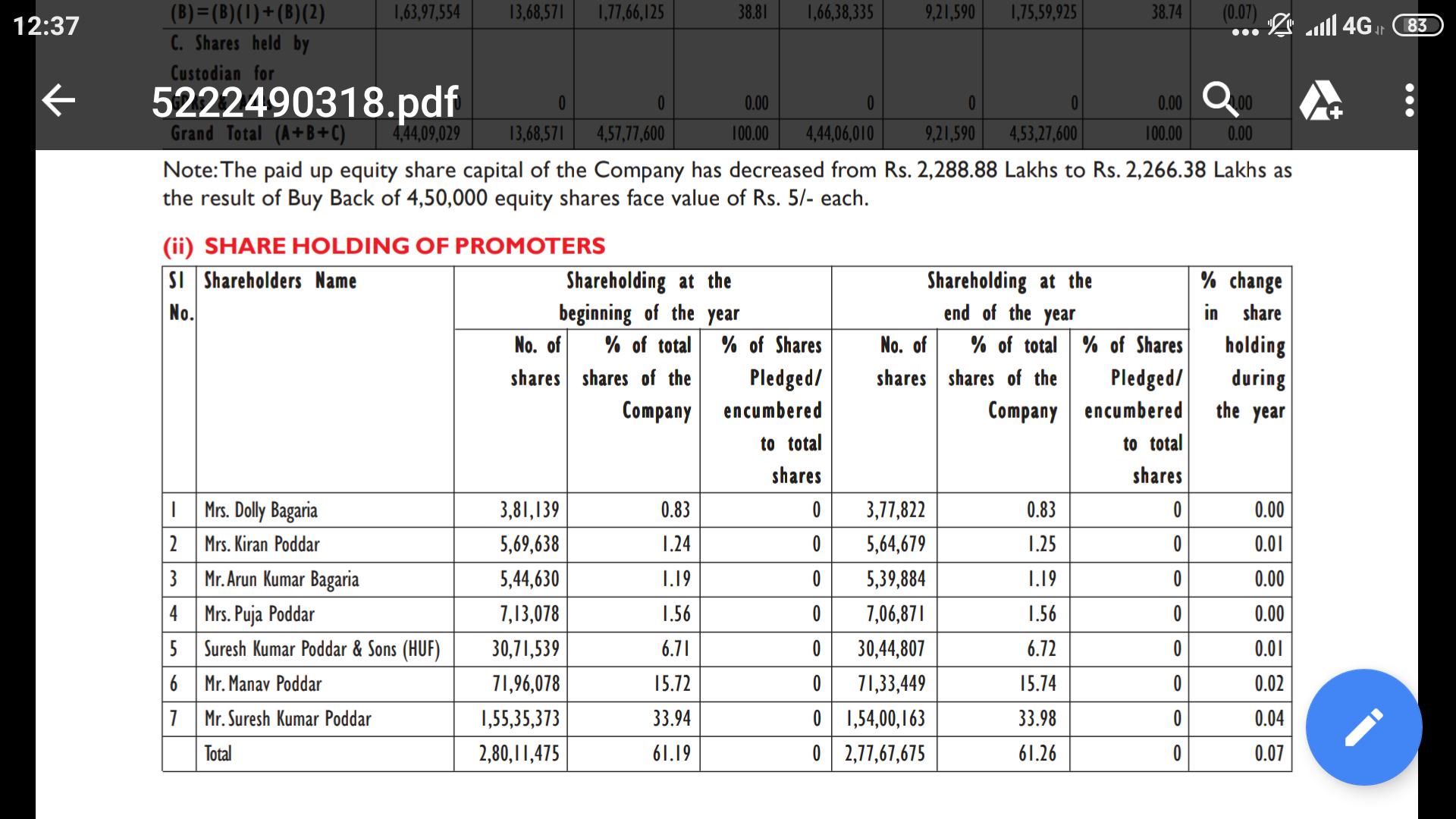

Promoters offload @ 500 and 550 in buybacks. No buyback while stock is at 200. How bad is it really?

In case of buyback through tender, like other sharholders, promoter can also participate. So when in past company did buyback, promoter also surrender pro-rata holding. So nothing wrong on that part.

Buyback is not like dividend and it is normally once in while development when the excess cashflow are returned to shareholder. In current evnironment, I am not aware whether the company has excess cashflow which are available on balance sheet which can be returned.

Further, the company has regularly paid shareholder dividend which is what generally equity investor can assume as cash return in case of sufficient profit. The company can not borrow and buy back equity shares just because equity price are lower.

While I appreciate your point that buyback would have been more beneficial at price of 250 than 500, even the management would not have preceived that share price would decline to current levels. Further, managment did not gain at cost of minority shareholder when they tendered their share in buyback as it is pro-rate entitlement.

So in my limited understanding it is not bad development. One can defintely have concern on scaling up operation and growth, but not on integrity of management in my opinion.

Discl: No investment

6 Likes

1 Like

The responses from the management are quite annoying and unconvincing. There is never a straight answer to any question. The order from Mercedez Benz is being talked about for some years now. Mr. Poddar said they’ll start shipping to Mercedez soon, but when asked is there a contract in place, it was not a Yes. Will Manav Poddar sell his shares? First answer is No, then it is I don’t know. He referred to demonitization for the slowdown in footwears segment, however Bata and Relaxo’s revenues have improved sharply since demonitization.

3 Likes

Bata volumes haven’t grown for past 2-3 years. Only pricing has gone up. It seems you are correlating stock price performance and business growth when there may not be a correlation.

Manav selling - he doesn’t have any control.

Mercedes order - Q3FY 21 sales is starting. The sales is of course dependent on quality of products and if Mercedes continues is happy with that. No guarantees.

4 Likes

Nope, not correlating the stock price performance. Bata have had a 2-3% volume growth in the recent years. https://www.thehindubusinessline.com/companies/bata-india-expects-product-innovation-to-give-a-leg-up-to-footwear-volume-sales/article28805223.ece

Not great but not a de-growth either. Mayur Uniquoter’s footwear revenues have been seeing a negative growth as per management which is the contradiction I was alluding to. Relaxo’s revenues in the last 3 years have grown almost by 50%, not all of it has been without a volume growth.

Regarding Manav’s selling, I understand he has no control but thats not the first response he gave.

Anyways, lets see how things progress from here and if the management is able to decure and execute orders from the BMW and Mercedez.

2 Likes

PU Plant Starts

11 Likes

Given you spotted this early on, do you have any view on the current valuation and new production commencement? Thanks in advance for your help.

1 Like

Hi, had exited and stopped tracking actively since the family issues came to fore. Also, the growth had materially slowed down while the stock continued to trade at good valuations. Now it definitely looks to be available at saner valuations and with the plant getting commercialized, things can become better. Will be keeping a tab.

12 Likes

Thanks @ayushmit

Appreciate your prompt response.

Mayur Uniquoters Q3 commentary:

Mayur Uniquoters Limited being a leader in the synthetic leather industry and an organized player has been able to leverage the emerging opportunity and deliver exemplary performance in past years both in national and international business markets. The current market scenario of automotive industry has affected our Q3 performance also and since revenue decreased by 22.52% as compared to previous years quarter mainly because of the fall in India car market in last 8 years and sluggish demand in our footwear market.

However, we have observed a small raise in the automotive market from December month and in other segments also and we are now expecting a good sales volume due to increased demand in automotive market and its impact can also be seen from the industry performance in the current quarter of FY2020 that is in Q4.

Also the revenue from operation on consolidated basis is Rs.138.61 Crores, which is 5.88% increase as compared to last quarter and PAT amounting to Rs.23.29 Crores, which is increased by 6.28% over the last quarter. However, the endeavor of Mayur is to be the preferred supplier for leading OEM especially is US and European regions and we are glad to update that your company has already approved by Mercedes Benz for supply to their South Africa plant and product supply is expected to start for their new models from Q4 of next financial year 2021.

Moreover, our product approval from BMW is also under progress. Also in FY2021, we are expecting a very good and high volume in both exports markets and domestic markets and export markets we expect 20% to 25% increase and domestic markets we expected 10% to 15% in coming quarter for automotives. Now, I will update on our capex plan. PU plant, most of the project construction activities are completed with the commissioning of weight and dry lines of PU plant, we have done trial run of PU plant on December month and also started commercial operation last month.

A small supply orders also started from the plant. Now, expecting production stabilization of the plant within next 2 months for regular and large quantity of supply orders. While pursuing our business interest, Mayur Uniquoters have also been endeavoring to fulfill our response towards the society and our corporate social response program the company has adopted many schools for education of children. Your company has worked on education especially for the girls and under privilege child education, various health care institute especially child skilled development, water for all school area, distribution of books, bag, box, blankets and most importantly family planning and family welfare schemes.

9 Likes

One of the best things I have seen here is the continuous buying by promoters since last few months.

That shows they are confident about Mayur’s future. Means there can be n number of reasons for selling but probably only single one for buying.

Also one cant do buyback by some account manipulations.( as far as I know)

Though they cater to the footwear industry, it has kind of become an auto ancillary story. So market in not giving it proper valuation.

And when it comes to footwear industry, both bata & Relaxo are trading at all time high PE multiples.

But Mayur though supplies to both of them is trading at around 1/4 th of their PE multiples.

Means probably Mayur is not at the risk of going under. But the Q is what will be the trigger to become a multi-bagger from here. ( Value Buy / Value Trap)

Maybe the trigger can be the confirmed order from Mercedes.

Here is the latest detailed research report that I found.

PLEASE share your opinions.

VIKAS

7 Likes

Hi Vikas. Thanks for sharing the report by Dion global. Very detailed and informative and it also helped me further in my thesis.

I had been tracking Mayur Uniquoters since last 4-5 years but took position until recently few months back and added in the correction. Mayur is India’s biggest manufacturer of synthetic leather. They derive most of their business from auto (51%) and footwear (36%).

My thoughts on Mayur:

Negatives:

The only reason why I am not making this my 10% position is the key man risk. Mr. Poddar is well past 70. He has issues with his son and he has ousted him from Mayur Uniquoters but his son still owns around 15% of Mayur. His son in law is handling all the day to day operations. Also the risk of his son selling 15% of the stock can cause a big fall in the stock. Mr. Poddar has promoted some of his employees to senior positions in order to display to the investor community that the succession plan is in place but when you listen to the concalls you know that it is completely a one man show.

Positives:

The company is the largest manufacturer of synthetic leather in India. It supplies to all leading domestic auto OEM as well in replacement market. It is almost certain that car sales will remain subdued for next 2-3 quarters (maybe beyond) and Mayur may struggle to get decent sales but what I feel is that the unorganised to organised consolidation which the whole investment industry was talking about after demonetization and GST will actually start playing now. Also while we have been talking of chemical, pharma business shift from China to India we have not been considering the same happening in other sectors too. China is a big player in the synthetic leather market and even a fraction shift from China can immensely benefit Mayur. It has already got approval from Daimler (parent of Mercedes) and BMW will be coming next for audit. An important trigger will be commencement of delivery to Daimler. An order from Mercedes Benz will definitely help Mayur to get orders from other European car manufacturer. Mayur is the only company from India exporting to American auto OEM’s. Even during the slowdown in auto sector since last few quarters, Mayur did manage well by adding new clients like MG and Kia.

The newly commissioned PU plant will cater to footwear segment where China holds around 95% share of the 3500 crore Indian PU market. Mayur can take away some of the market share.

Mayur has a healthy balance sheet with investments and cash equivalent of 200 crores (Mar’19). Promoter holding is slightly more than 61% . Promoter was continuously buying from open market in March during the crash.

My thesis is to bet on industry leaders and let them win market share due to the ongoing consolidation taking place all over the industry i.e Big will become bigger theme.

Comments Invited.

8 Likes

Thanks a ton for the detailed reply.

Yes. The One Man risk remains, which is very difficult to predict.

My main thinking is Mayur catering to footwear, which is essential commodity. Yes. Auto OEM have more margin. So its their main area of concentration.

About Footwear, it’s really surprising that both Bata & Relaxo are trading above PE of 60 in such times.

The main thing I am interested in - How much of raw material both of them are sourcing from Mayur. Means is Mayur their main supplier?

This will give some kind of margin of safety.

Does any one have such details ?

Thanks

Vikas

This report is dated July 29, 2019 and states that “Recently, they have become one of the proud suppliers for Daimler (parent company of Mercedes), a great achievement for any Indian company. Strong business fundamentals such as diversified clientele and strong product portfolio along with high return ratios, strong net cash position and consistent pay-outs to shareholders by way of dividends/buybacks make Mayur a compelling investment proposition. We expect the company to deliver a strong Revenue/EBITDA/PAT CAGR of 14%/13%/10% during FY19-FY22E and hence, initiate coverage on Mayur Uniquoters with a BUY and a target price of Rs 360 (17x FY21EEPS/14x FY22E EPS).”

Already 2 years have passed but yet to see the foretasted GROWTH in numbers. Where does the company stand on growth and supply to Daimler?

Disc: Not invested.

I am not invested in this company however I was considering it

At that time I heard some of their concalls as part of research

In one of their concalls they mentioned that car manufacturers don’t change suppliers for exiting models as the change can disrupt a lot of procedures and introduce unforeseen delay

They usually decide on the supplier for a particular part during initial launch and then stick with that supplier as far as possible until that model is no longer built

They make some exceptions but generally this is how most manufacturers work

So you might have to keep an eye on new Mercedes models to get a rough idea when revenues might reflect the new product

2 Likes