What is the business ?

Matrimony.com Ltd offers online matchmaking services. It was founded in 1997 by Murugavel Janakiraman, who later met his wife through his own matrimony site. The company has 130 offices in India, with offices in Dubai, Sri Lanka, the United States, and Malaysia to cater to its customers beyond India.

Is business is a niche with low or zero competition like Facebook, Twitter, LinkedIn/ Is there any entry barrier

No business is not niche there are a lot of local and national players are present. There is no entry barrier anyone can make a website, advertise it and you are in the game.

Why this business is worth studying ?

This business is based on network effects like Twitter, Facebook, WhatsApp, Dating Apps. The business grows when more and more people join the platform. In my opinion, any business that has a network effect is worth studying.

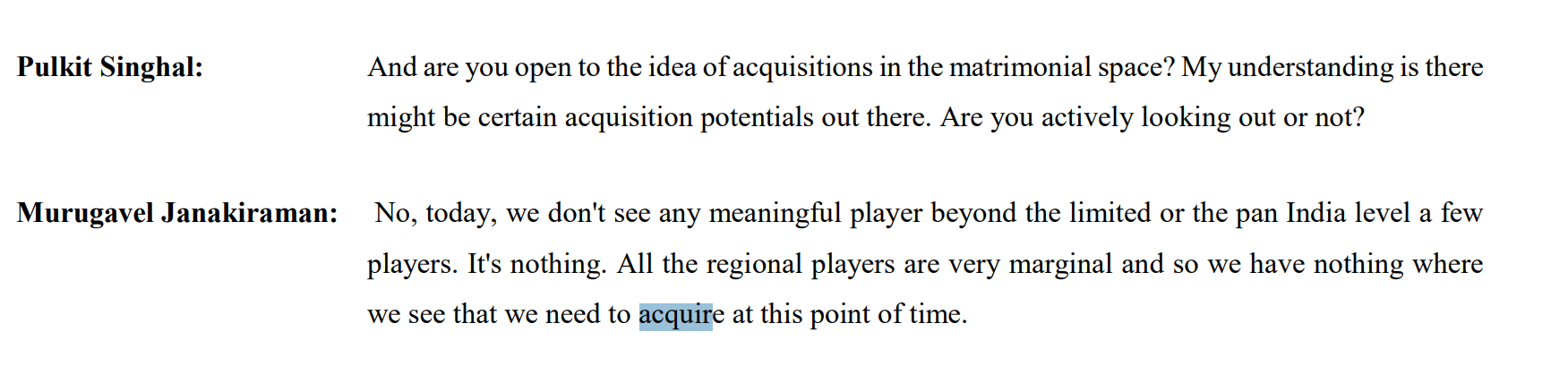

Who are the competitor and what is the market share of matrimony

- Jeevansathi.com (owned by InfoEdge) - Leading share in North India

- Shaadi.com (owned by People group) - Leading share in Gujrat Punjab

- Bharatmatrimony.com (owned by Matrimony.com) - Leading share in South India

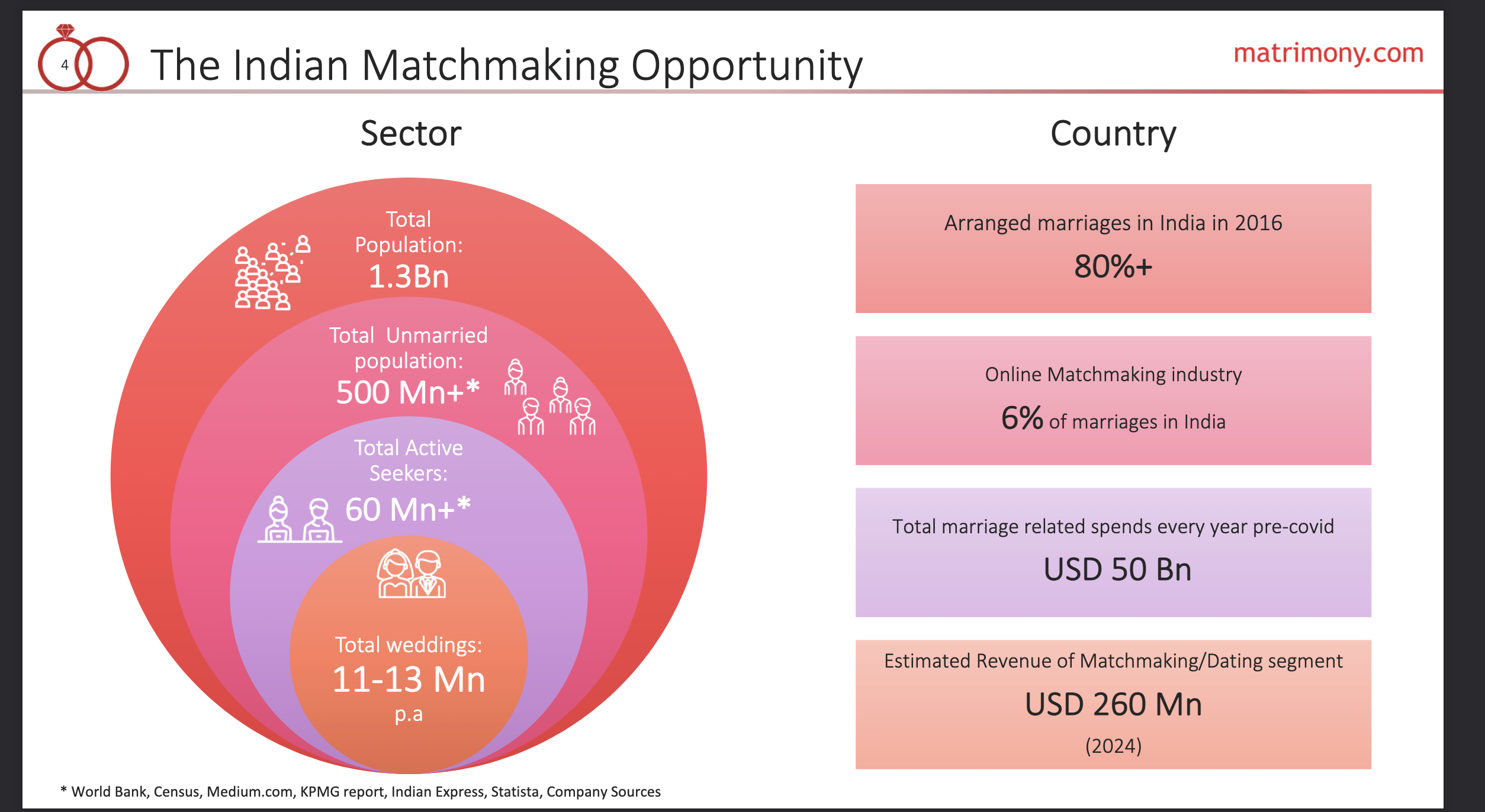

The marker share of matrimony is 60%

Is the company profitable ?

Yes, Matrimony.com is a profitable company but its peers are not profitable, so this business is not a hunky-dory business where everyone makes money. This business is something where the winner takes it all and the obvious reason for it is network and optimization.

What is the major cost for these companies ?

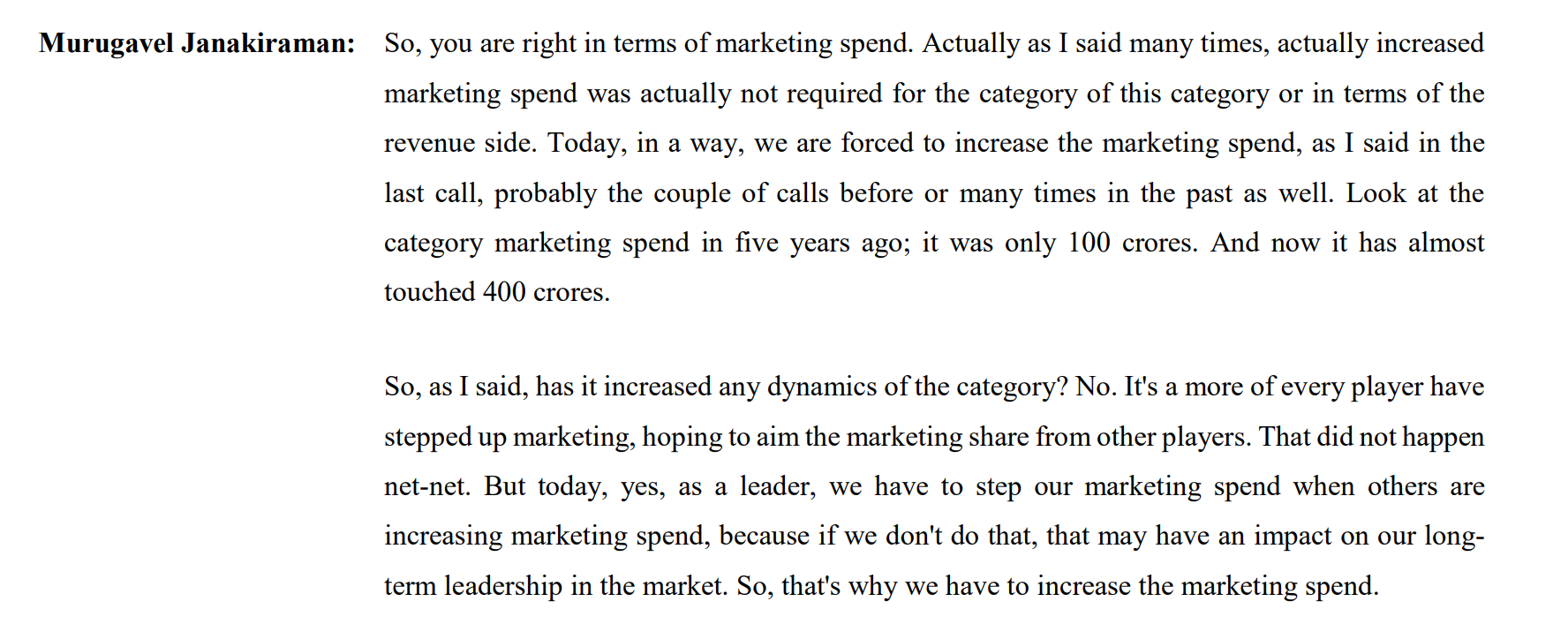

The major spend of these companies is on the advertisement to attract more and more customer and it will not stop any time soon.

Does this company should deserve valuation like amazon, Facebook, Flipkart?

In my opinion, it doesn’t deserve valuation like amazon, Facebook because customers for matrimony are not repetitive, unlike Amazon, Facebook.

What is the growth opportunity ?

- In India 80% of marriages are still arranged so there is a lot of room to grow plus the trend of a nuclear family increasing

- Adoption of Digitization

- Nowadays Parents ask for their children’s opinion as well unlike in history where parents decide and children will not have any say in their marriage, Nowadays I have seen parents are somewhat ok if their children find partners online.

More on business

The company follows Micro Market Strategy: The company offers a range of targeted products and services that are tailored to meet the requirements of customers based on their linguistic, religious, and community preferences for which it has 17 regional portals and 300+community websites. Matrimony.com also caters to the NRI community through its operations in USA and Dubai.

In 2015, the company ventured into marriage services with Mandap.com which offers one of the largest wedding venue booking platforms with over 10,000 wedding venues and Wedding Bazaar, which is India’s largest wedding planning marketplace offering over 10,000 wedding services providers.

They recently started business in Bangladesh (launched website) and by next quarter they will be able to set up the payment gateway and transactions will start.

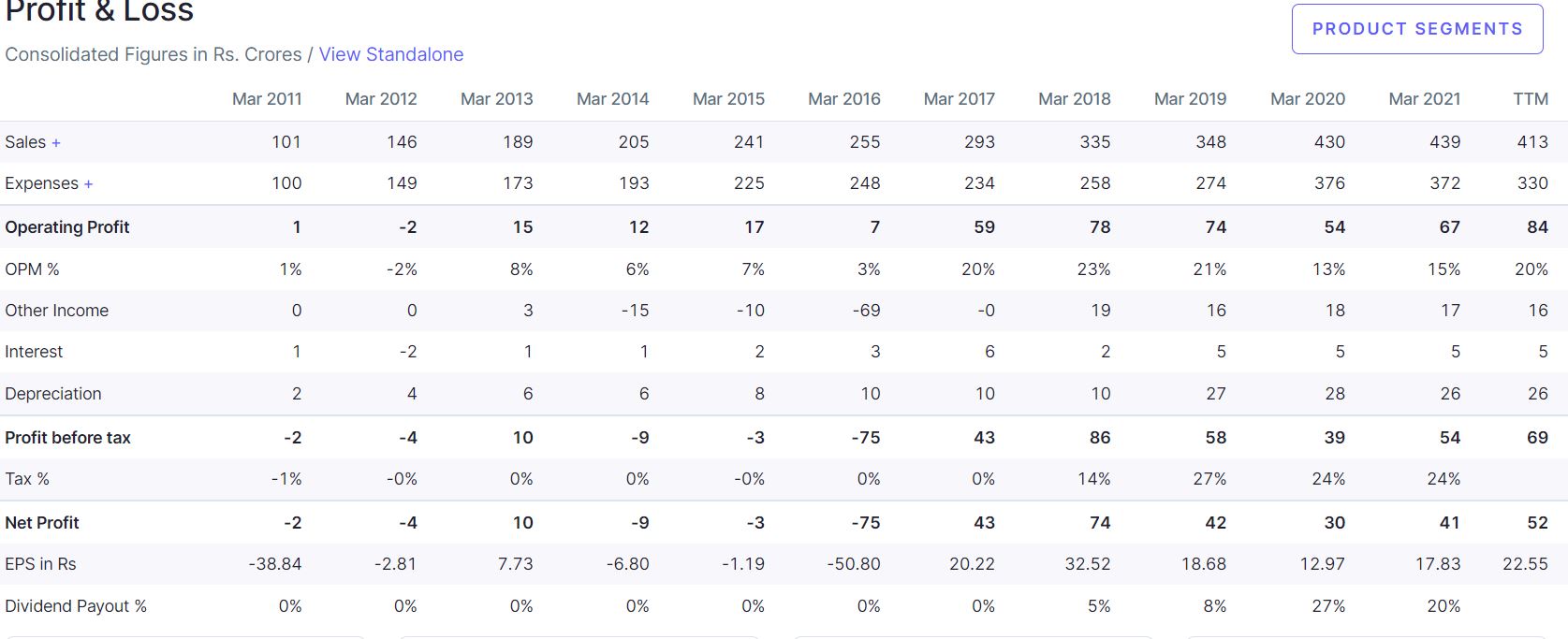

Financials

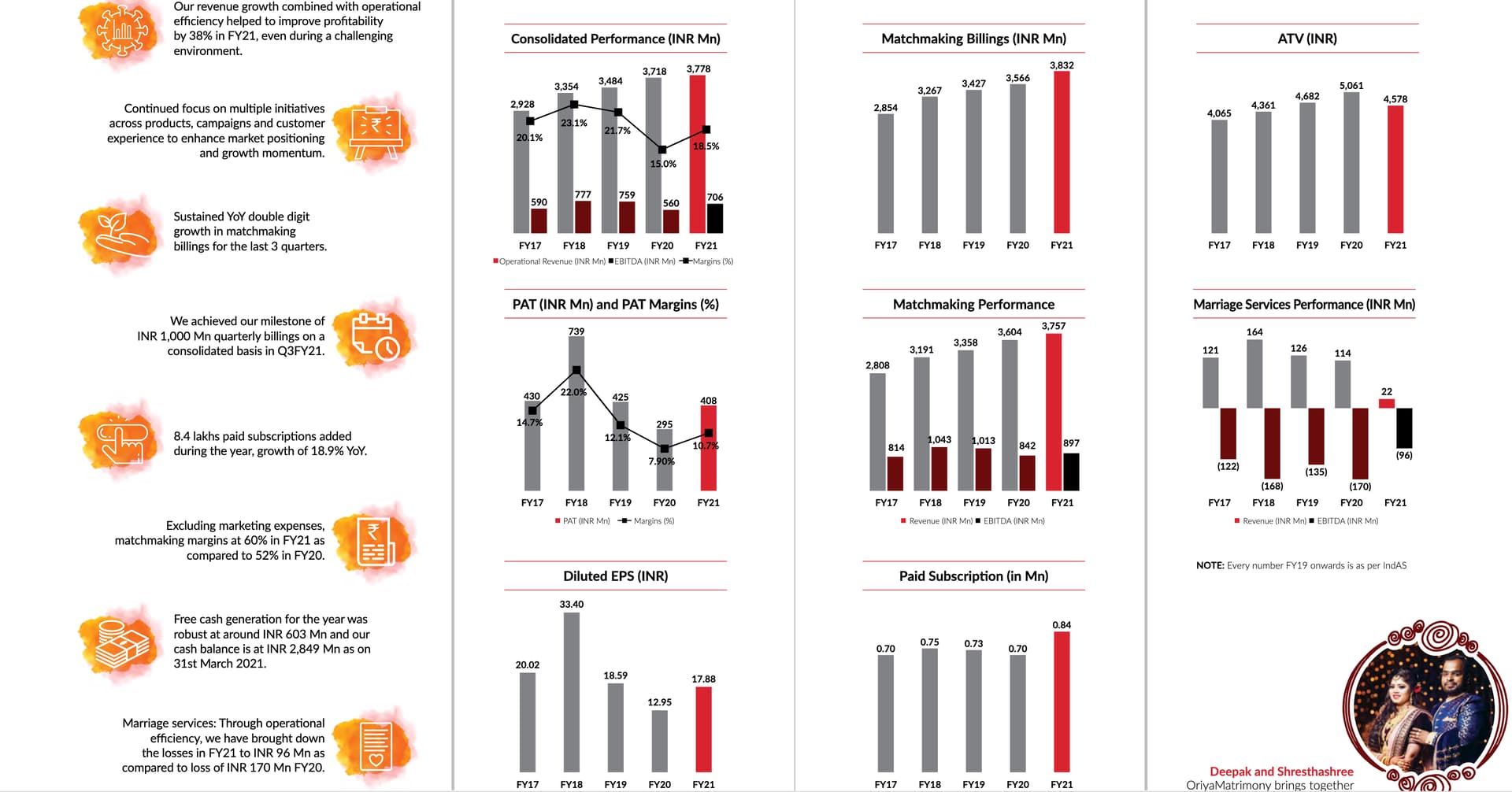

ROC for three years: 20%+

ROE: 15%+

DEBT TO EQUITY: 0.24

SALES GROWTH 5 YEARS: 10%+

PROMOTER HOLDING : 50.2%

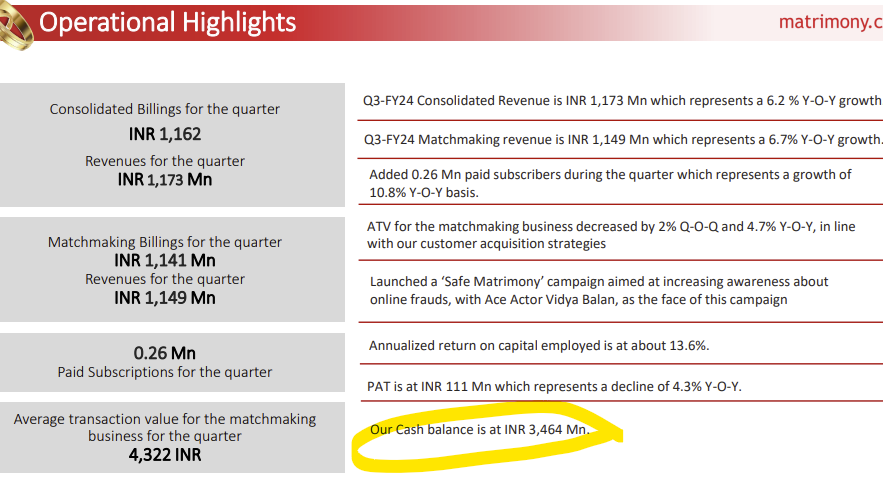

Cash on Books : INR 2849 Million

The other business of matrimony is still loss-making so didn’t talk too much about it as they are minuscule

What can be the good valuation for this company ?

The value lies in the eyes of the beholder

I will be researching/gathering more information in the coming days and publishing the article on my app as well Finbloggers.com

Disclaimer : Invested in this stock and will add more based on how the business grows ![]()