Above suggests that paid subscribers are rising on continuous basis, though growth rate is muted. ATV’s are not able to keep pace, signifying that pricing power is not intact, probably because of competitive strength, or may be some other reason.

Overall, matchmaking revenues are increasing due to increasing subscribers, but partially offset by declining ATV.

While reading Matrimony concalls starting 2017, I realized a painful truth. The story line in 2017 was exactly the same as today (2024), that is :

We have leadership in matchmaking business

Growth in business will come

Target addressable market is huge

High Operating leverage in business, meaning dispropnate increase in profitabilty with slight increase in revenue.

Marriage Services business, a joker in the pack, will grow and get profitable.

However, 7 years have passed none of it has materialized. In fact, things that have detoriated include:

Competitive intensity has multipled, causing high marketing expenses, eating away most of the revenue growth

Customers never traded up from basic 3 month / 6 month pack

Growth has been extremely tepid.

Valuation derated to half from the IPO price.

Its difficult to be a long term investor and bear this pain. Those who believe in the story have to have patience and go through difficult time. It looks to ME that last bull in matrimony has left the market.

However, past may not be the mirror of future. Things may turn up well in the future, as the underlying story STILL remains the same with reasonable valuation.

Disclosure - Invested and hence biased/ blind. Not a SEBI registered analyst.

My view on Matrimony is that jeevansathi is loosing steam. They have tried multiple models (freemium etc), burnt a lot on marketing for several years but have not gained market share.

Investors are asking tough questions to infoedge (during conf calls) and they can not continue to burn endless money on jeevansathi. The management is also showing signs that they have to stop at some stage.

Matrimony has stood against relentless competition. That shows strong moat. Once the competitive pressure reduces matrimony will get re-rated as their margins will improve substantially.

Further, they are cautiously playing out new bets on mandap, luv.com and investing wisely. We have to see how these bets will turn out going forward.

Disclosure - Invested and hence biased. Not a SEBI registered analyst.

If the profit pool is large enough no one is going to hand it over on platter - it has to be fought for - that is the reality for competitors.

Chk 13:00-14:30 of

If one believes Matrimony to be the El último hombre of the category one should look at it.

Sometimes due to widespread neglect & under ownership & absence of sellers - the stock may just take off due to a small trigger -

For the time being mr.market not interested in matching services globally incl. $BUMBL & $MTCH

Q4 2024 and 2024 annual results were announced a couple of days back.

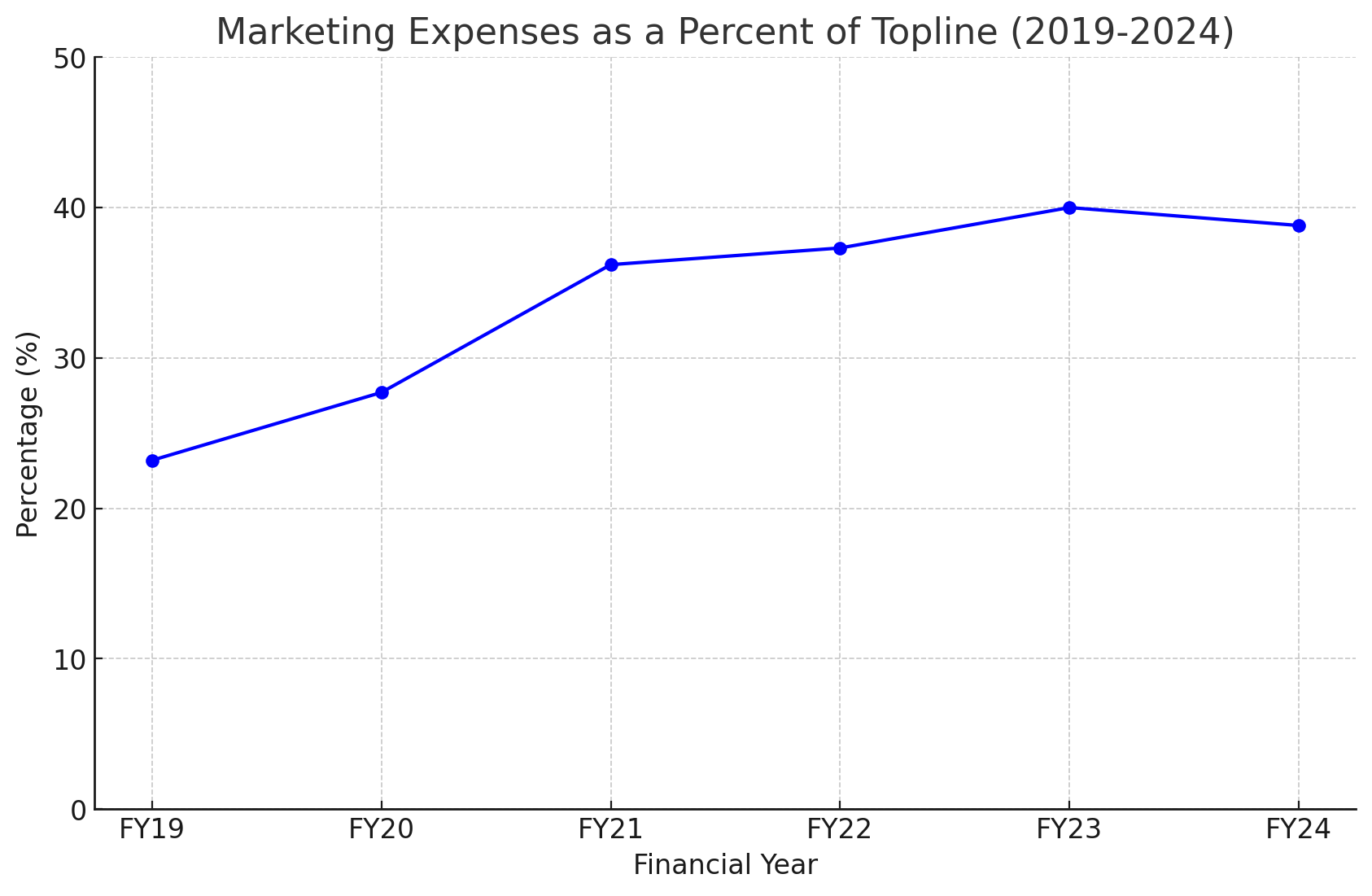

Core matrimony business topline is growing at ~8% CAGR in the last 3 years. The growth comes primarily from higher # of paid users, which have also increased by 8% CAGR. There does not seem to be a big shift in market share between the 3 players or a pricing change or offline→ online movement.

On the other hand, EBITDA has not kept pace with revenue increase because increased intensity on marketing expenses (increased from 22% to ~40%)

An interesting point to note is that out of the INR 50 Cr PAT in FY 2024; INR 26 CR is from interest income from their INR ~340 CR cash pile.

Potential triggers:

Irrational competition reduces and marketing spending comes back to 20-30% range

Able to re-invent and open new markets with Jodi or Luv (2+ years)

Find a new revenue stream through ads/other partnerships

Breakout with wedding services marketplace (looks unlikely as they have already invested 5 years)

I am going to stay invested. I believe consolidation will happen in this business and margins will improve. Plus they have a good shot at making other segments big.

Wonder if they intend to invest in Online Astrology as well which has an expected growth rate of 45%, can probably prove more profitable for them than online wedding services.

actually they should just copy paste Astrotalk biz model & integrate it in their services. i think it will give them most bang for their buck than their other ventures such as mandap.com or luv.com

As an ex-user of their platform, disappointed with the data quality and poor moderation. They seem to purposely leave data of married, inactive and duplicate profiles despite reporting. Have used their competitor platforms as well, found the data quality was better and the profiles relatively more responsive.

Disc: No holdings. This is just my view, others experience might differ, which is fine.

A lot of companies announced buyback after the current budget, matrimony.com also announced a buyback in the first week of September. However we haven’t seen any announcement related to that , I wrote an email to the investor team this morning but no response. Company’s share price has been stable since last month, while mid/small cap corrected during the same time. Not sure but something doesn’t seem right here.

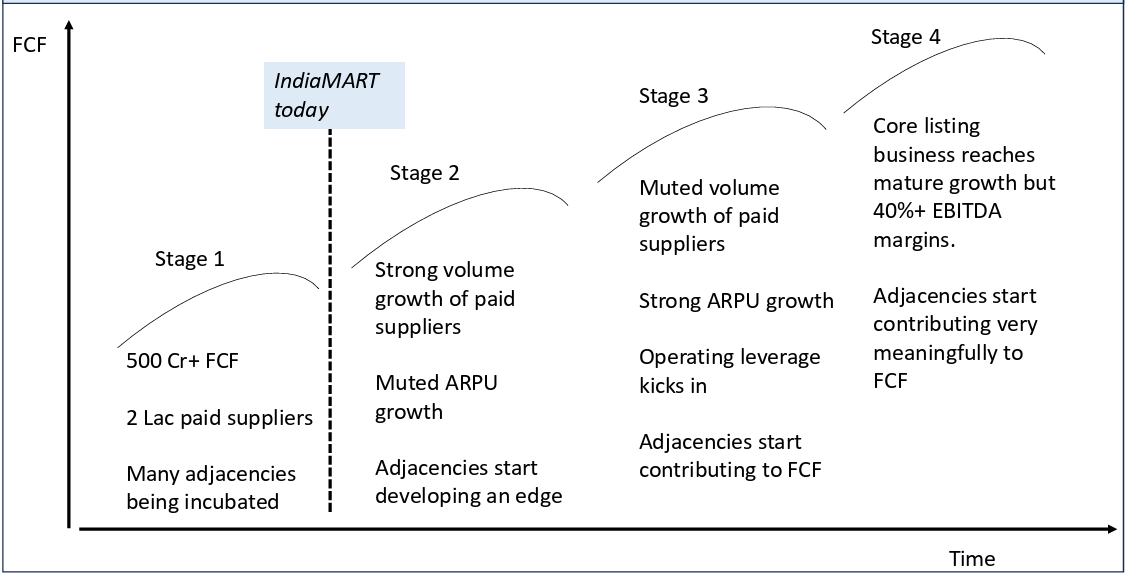

Gathered few more insights about network effects / non linear businesses. The idea is to increase the network effects (stage 2), which is possible by adding more users. If you want to add more users, you don’t want to deter them by charging heavily. So, you keep charges down, let the network grow, while your revenues still increase as you add more subscribers.

Then, comes stage 3, when you conclude addition of subscribers is exhausted, and now you want to grow by raising charges on existing user base.

While the idea applies for Matrimony, it remains a company that’s written off by the market , probably for the right reasons.

5% CAGR in revenues for 10 years, can run the PAT by 15% CAGR due to high operating leverage, but it just does not seem to be working out (since long long time).

Some confidence comes from buyback, where promoter continues not to tender and increases his stake during every buyback.

Patience will be tested hard, and there is a possibility, that patience may not reward at the end. Lets see

Disclosure - Invested, biased, though not blind now.

Company is struggling for growth and new initiatives can be further leading to initial losses (pain) for its profitability.

One must see how they scale up and whether any optionality plays out.

Hi manivannan . Thanks for sharing . Very well written .

One question .

Keeping advertising spend aside.

The management recently keeps on talking about growth and increase in revenue . What I want to understand is where is this going to come from . I understand the matrimony business will grow in single digits . Is manyjobs the area where they are expecting growth .

Can manyjobs be the growth vehicle in the quarters to come ?

The core Matchmaking platform has been growing at high single digits taken over a decade. There is definitely scope there to keep improving - Geography wise, Community focused, better paid conversions across the markets

They are targeting two diverse end of the profiles - Elite and Tier2 focused Jodi. Both have potential and let’s see how that turns up

They are trying services focused on alternate ways of matchmaking like Luv.com. Not yet monetized but need to watch it

Then wedding focused but allied services like wedding services, they have been trying it for a while and need to see if they are able to do a meaningful breakthrough there

Do you think there can be any Optimization in marketing spends within the next two years ?

what do you think of manyjobs as a idea on a whole. From the looks of it , it’s filling a huge gap in the job space. Of course it might take 2-3 years for it to reach into anything meaningful.