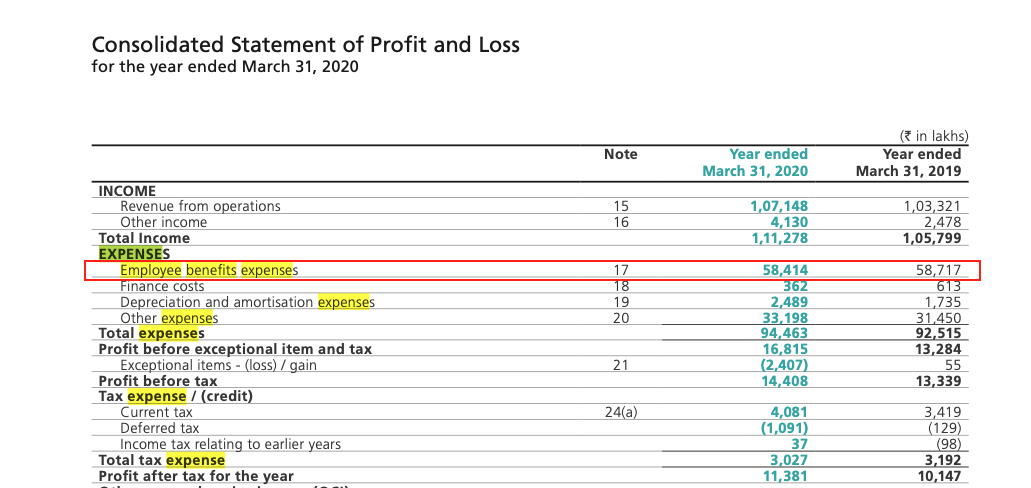

Total Employee Benefits Expenses for FY20 were lower than FY19, even as head count must have increased (due to organic hiring itself, EvoSys acquisition happened in Feb-March), implying salaries were decreased:

From FY20 annual report:

"The percentage decrease in the median remuneration of all employees in the financial year was 14.

Average percentage decrease in the salaries of the employees other than the Managerial Personnel in the financial year was 4% vis a vis decrease of 14% in the salaries of Managerial Remuneration."

The profits were growing and the company didn’t seem to be under any financial pressure. Anybody know why this happened?

Mastek has traditionally been on-site heavy ( compared to peers)company with lot of external consultant / contractors working for them - particularly in govt projects in UK. Last year meaningful proportion of this work would have been delivered remotely( from India )due to Covid and thus cost savings even after adding head counts evey quarter. Q3 AND Q4 concall transcript has more details.

Recently started analyzing and there could be more reasons as well.

I read somewhere 80% of Mastek revenues come from Digital. Is it true? If yes why is this stock so cheap when at 22x FY22E when Happiest Minds is at 101x FY22E?

The backlog is up 40% YoY so does that mean this company can grow dollar revenue 25% plus in FY22?

Other IT companies give guidance. Why doesnt Mastek give guidance or does it?

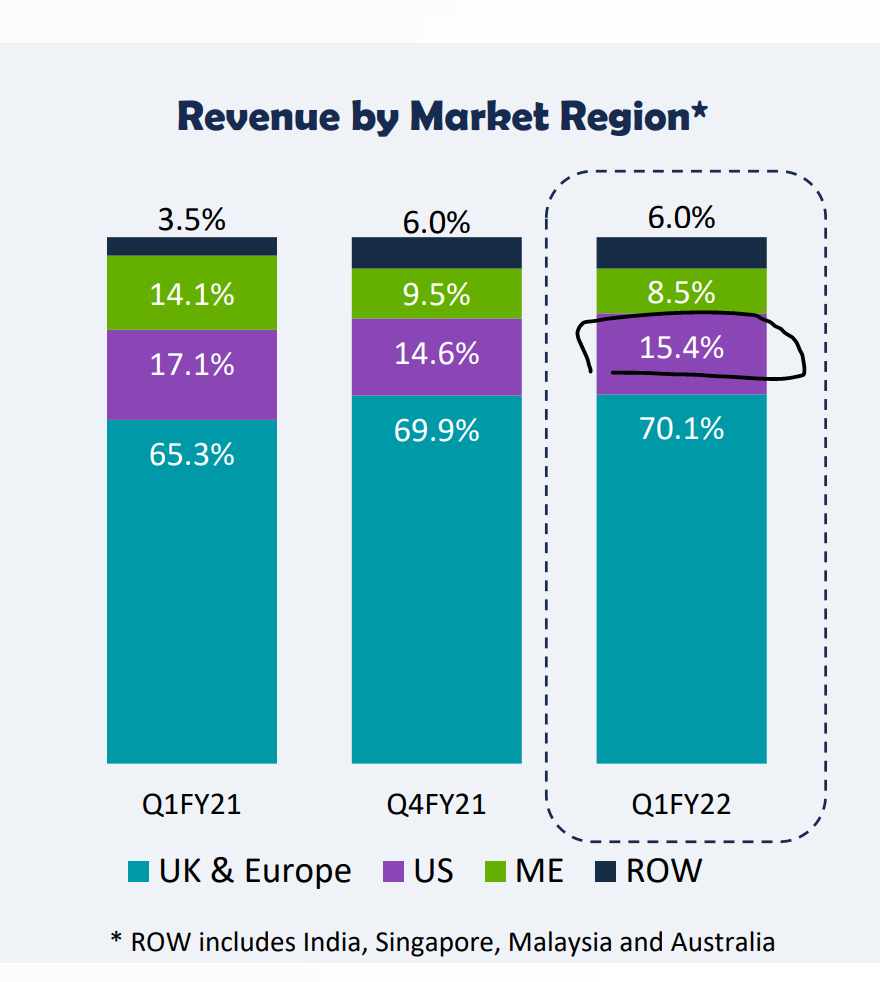

Because the markets are inefficient. Because HM IPOed in latest bull market. Because Mastek IPOed long time ago. One key driver of mastek rerating will be larger deal wins in geographies except UK. Right now the UK revenues are too large a part of the pie.

I think the order backlog is computed in terms of current forex rates. Assuming no forex movement in next year, some part of that backlog will get executed. Some new projects that come in FY22 will also get executed. I personally expect 25% revenue growth in a bear case, and 35%+ in a bull case including inorganic acquisition(s) in US. They also have a large cash pile they are waiting to deploy in inorganic growth.

Their guidance is to grow faster than market. Digital transformation grows at 18-22%. (snippet from mastek fy20 AR):

Mastek is not trading at PE of 27. We have to take 15-17% dilution due to happen in coming 2 years. These shares will be given to EvoSys management as per the acquisition terms. So Actual TTM EPS is 71 and PE is 32. Which is not cheap, though reasonable given company’s potential.

Would it be fair to value Mastek purely on the basis of its earnings? PE or any other earning related metric will completely miss out on that huge cash pile Mastek has and which it can deploy in EPS accretive acquisitions. With Evosys, they have already shown that they know how to make smart capital allocation decisions.

I don’t think PE should be the ideal metric for a co like Mastek. Thoughts?

I was not talking of trailing numbers. Was talking of future numbers FY22. If there will be dilution in shares, more of Evosys profits will also get added (minority interest will reduce). I think post dilution EPS will be > Rs90/share

Mastek share is trading at a premium valuation it’s historic averages. It never traded beyond PE of 20 on a sustainable basis over the last two decades. Also, any company that is trading at triple digit PE has very high expectations build into it, which are very difficult to maintain.

To put the things in context, Infosys, Wipro shares were trading in 100 + PE in 2000. Even if their business grew many time in next decade, their share price has hardly given any returns. Just my two cents.

I think Mastek’s share price or multiple should only be compared with the last 5 years history, i.e, after the Majesco demerger in 2015. But yeah, your take on HM, Infy and Wipro is correct.

I read somewhere 80% of Mastek revenues come from Digital. Is it true? If yes why is this stock so cheap when at 22x FY22E when Happiest Minds is at 101x FY22E?

Personally I see digital less as a moat and more of future proofing of a business. Every IT service organization claims to be significantly digital these days, a bracket where one can (force) fit various transformational initiatives. One must take this segment with a pinch of salt, as digital becomes a commodity skill in coming years.

Counterintuitive, but there are situations where non-digital is a strength. The major BFSI organizations still heavily rely on mainframes (projected to grow further in this decade). The niche skills can brings more revenue to service companies.

In short, among other things one must see the spectrum of technologies, the size of engagements, industry verticals etc to assess the IT service companies

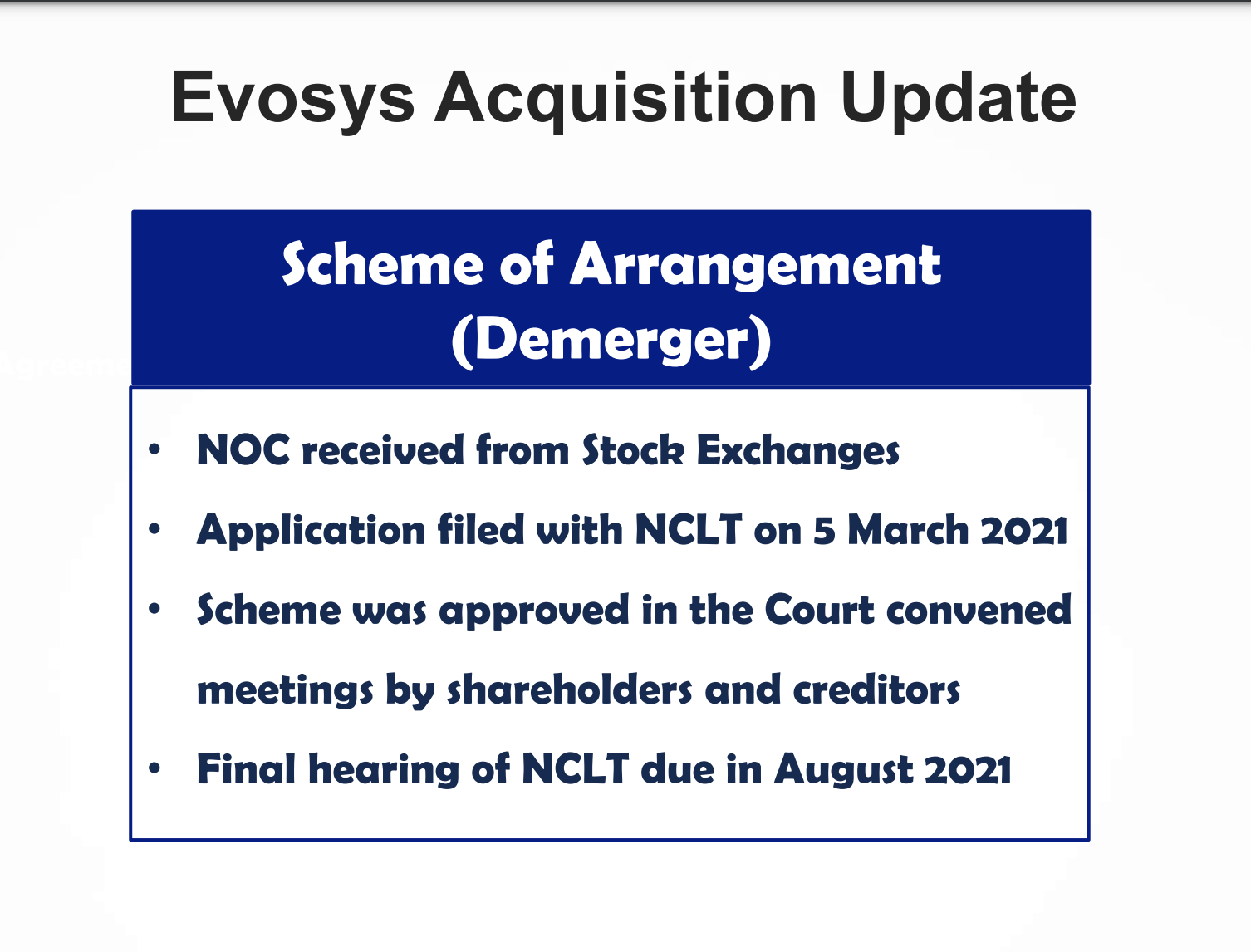

Mastek bought Evosys last year. It was a complex deal as Evosys has multiple subsidiaries in Middle East/Europe/US. I think Mastek is talking about these things.

As far as I remember above is procedural things but Mastek does records all the revenue from Evosys. Once the all formalities of Evosys are complete, there will be 12-15% dilution in Mastek equity as part of the original deal (signed in Feb 2020). Hope it helps.

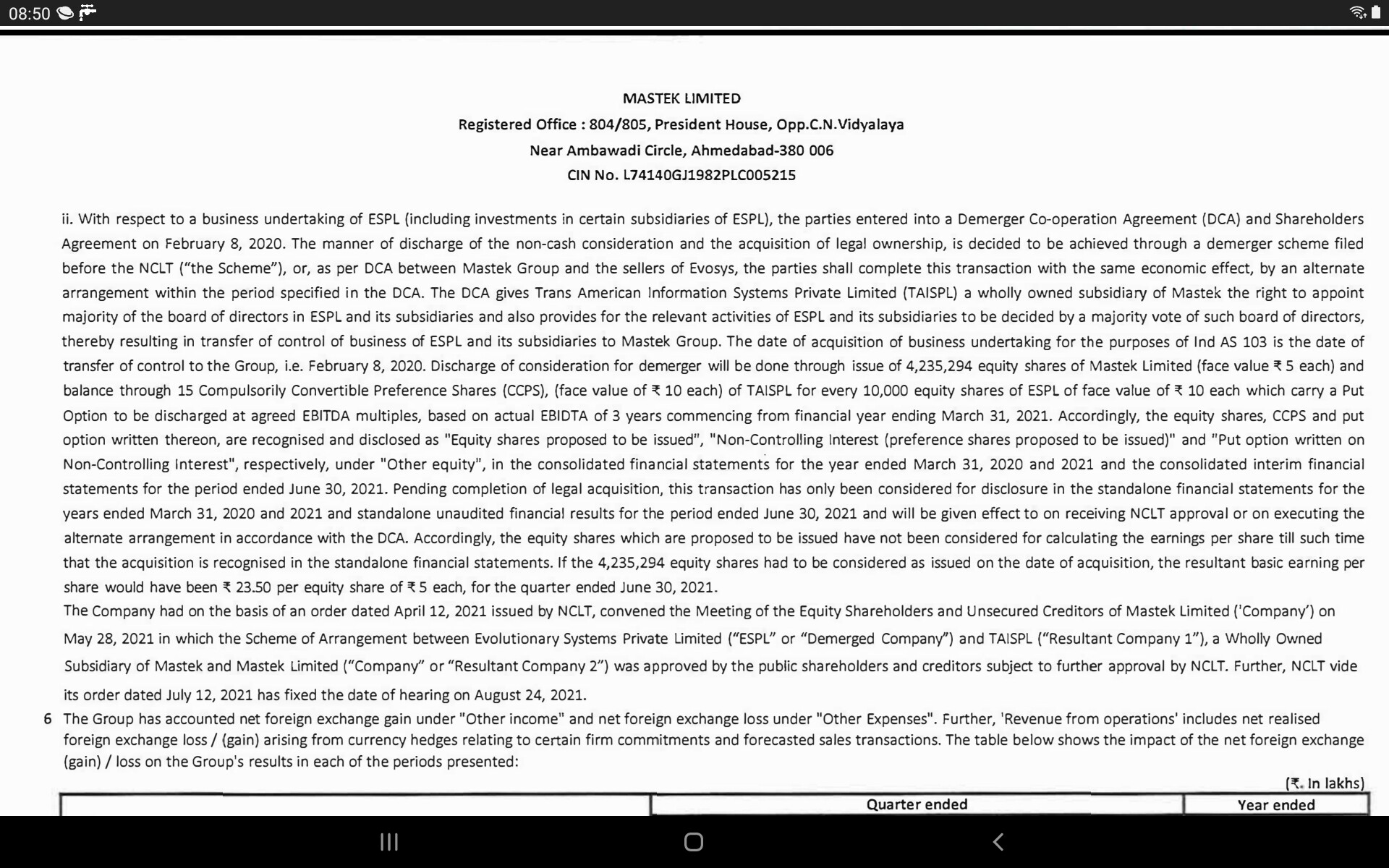

If the 4,235,294 equity shares had to be considered as issued on the date of acquisition, the resultant basic earning per

share would have been at: 23.50 per equity share of� 5 each, for the quarter ended June 30, 2021

YoY superb, however QoQ seems alright type considering peers, middle east profitability drag and onsite heavy aspects coming back in UK works, thus affecting margins bit downward - hope to normalize around 21% to be seen.

Mastek Limited acquired Evolutionary Systems Private Limited (Evosys) in a two-stage transaction:

The first leg of the transaction involved cash buyout of the Evosys middle-east business by Mastek Arabia FZ LLC for a cash consideration of US$ 64.9 million.

Under the second leg of the transaction, rest of the world business which includes India, US, UK and other markets of Evosys will be demerged and consequently merged into Trans American Information Systems Private Limited (TAISPL, 100% subsidiary of Mastek Ltd).

In consideration of the said demerger, shareholders of Evosys will get ~15% stake in Mastek Limited and Compulsory Convertible Preference Shares (CCPS) equivalent to 30% interest in Trans American Information Systems Private Limited, through the issuance of new shares.

Assigned preferred supplier status by one of the key clients – indicating further revenue potential

US - Cross sell & co sell continues to remain robust. 3 new deals in Evosys customer base in US

Middle east - Saw some impact on margins. Due to travel restrictions – restricted ability of employees to travel from India. Had to take sub-contractor model / local hires to take care of client’s onsite requirements. Which was slightly more expensive

Oracle side of business

Very good quarter with highest value in terms of order book. Added 9 new customers in million dollar deal range.

Verticalization approach (an approach where they develop vertical specific solution for prominent verticals – healthcare, retail, etc ) has worked well in UK. Will implement in North America as well.

North America & US - continue to remain key growth engines. 100% growth in last 12M - similar growth expected in next 12 M

UK public sector business continues to do well. Buzzing with digital transformation opportunities. Won 10 bn pound deals with HMRC . Similar trend expected in pvt enterprise space as well

While digital transformation business is growing at fast pace & will continue its momentum; planning to add more clients in application enhancement services, managed services business. Currently its around 30% - plan to increase further in next 2 years. (So when digital trans. business plateaus in the future – they will look to increase the contribution from this revenue stream)

Driving Cross-sell & Co-sell – focus is on reaching a stage where every opportunity is a co-sell opportunity

Scaling up the US business

Organic side –

Have all the elements in place to be successful. Healthcare & life sciences - seeing good momentum. Spend on healthcare is significant in US. Financial services another focus area.

Partnership ecosystem with Evosys - Critical part of the strategy. Customers are asking them to deliver integrated solutions.

Inorganic side – Actively evaluating acquisition opportunities. Would be a parallel strategy, along with organic. Acquisition has to add value to Mastek. So need to be careful while evaluating acquisition. Have the resources required. (Note - Company has cash equivalent of 960 Cr as of Jun 21; Healthy free cash flow of 115 Cr.)

New Group CEO Hiral Chandrana

Was with Wipro for 14 years; and 6 years with EDS

Has been in US for 26 years – 14 of which was with Wipro

Would be based in Chicago.

Views on his early days in Mastek. Wipro vs Mastek culture

Acknowledged Mastek’s continuous innovation over the last few years

Finds Mastek’s value system, governance & culture very similar to that of Wipro

One area that he intends to strengthen - is Marketing. Very interesting & complex work that company is doing. Important to articulate the same to the entire ecosystem.

Plans to highlight Go to Market strategy; account based marketing, content marketing; business case studies, etc

Hiring - 520 people added in this qtr. 12 to 13% of what their existing staff strength is. Will be focusing on training & capability building

Good coverage on notes above on concall. Concall was indeed interesting.

Being in same field and knowing that Mastek ( outside Majesco part) has been around for very very long with no remarkable success with scale (compared to peers), adding some qualitative aspect that hints at both sustainable sector tailwind and path forward.

Transformation from public sector and UK geo focused to truly global IT org is a remarkable journey - their org structure is totally in right shape and direction to scale

Evosys acquisition and piggyback of Oracle ERP ++ SAP compete delivering success in cloud enablement/Transformation theme( biggest beneficiary of digital transformation IMO ) -

*Although SAP compete program sounded key shortterm tailwind and current focus but their desire and steps taken to to get into ASM( spp service and maint) and make it 50% of revenue is where magic will unfold - implementation are short duration and non sticky and somewhat lower margins, ASM is sticky, has many operating leverage levers ( offshore, shared services cost benefits, value adds etc)

Hunger to win larger deals -$6M win this quarter is hopefully first of many to come

Successful integration and synergy from Evosys +Mastek and accelerated GTM with visible results - this alone is a biggest challenge in M&A and they have demonstrated success with outcomes - deserve credit

New Leadership in place - Hiral in just two weeks is clearly on top of game, meeting clients, matkeying focus, verticalizaion, US market scale focus, org structure for scale , offshore and freshers leverage eco system etc.

They are at right size to grow for mid term and don’t have a baggage with most of service line being aligned to Digital ( traditional govt projects may have some legacy but will become small as they grow)

One key risk is sizable fortune linked to only one of Oracle product and program - believe they are cognizant and will add capabilities to de risk

Cash in hand and desire for inorganic growth - while Evosys they got at extremely attractive Valuations- mkt has changed in last year on Valuations parameters

Given legacy Mastek identity they would need to work harder on branding/marketing/ identity refresh to attract and retain talent

Hope promoters take a back seat and give space and empower leadership team to run the show ( signs visible)

All in all reasonable valuations and exciting times ahead.