Mastek - performance expectations and no of upside triggers

-

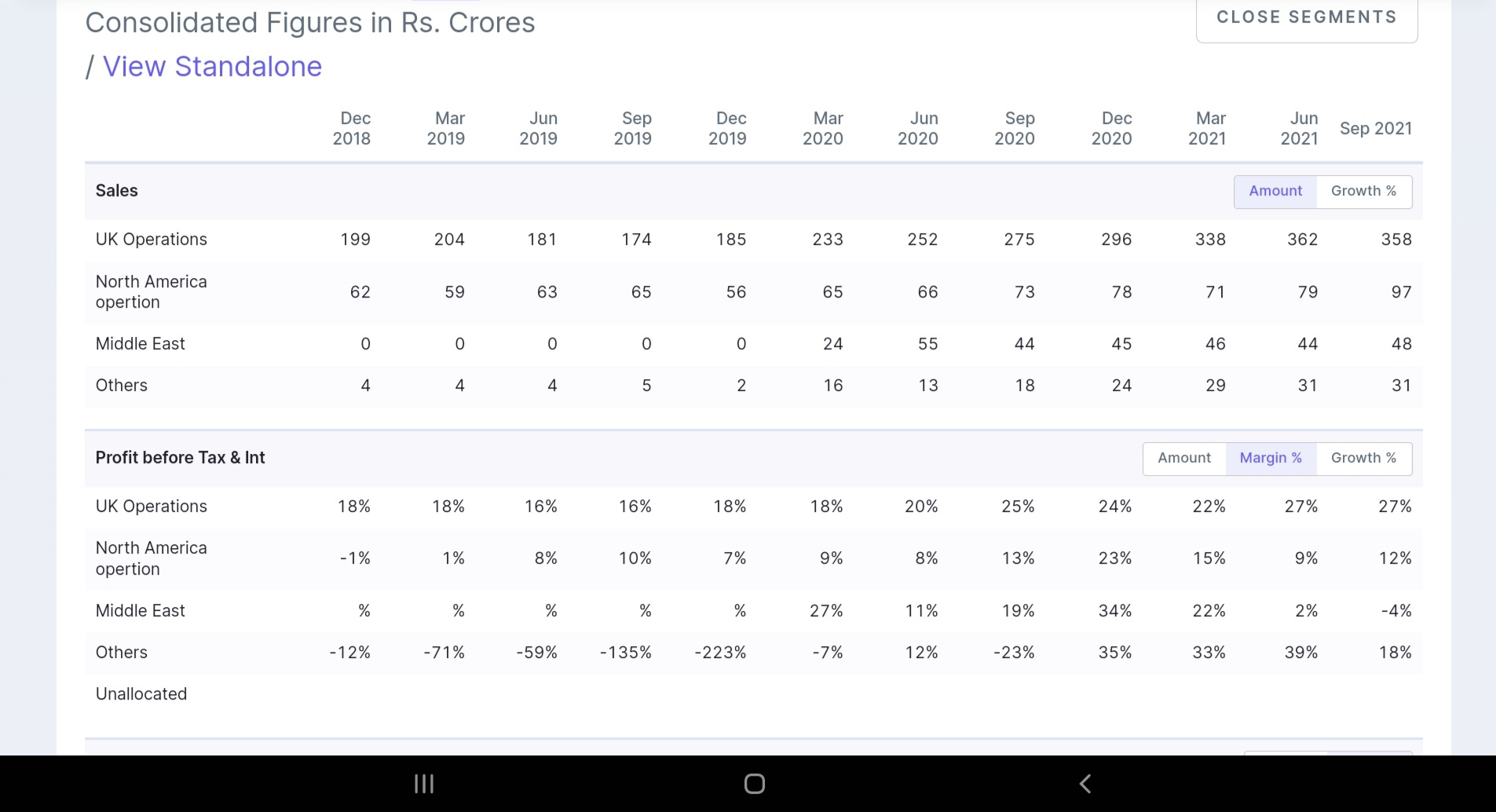

NHS new project win to help UK operations to continue on QoQ growth trajectory - 380-390 cr and Op margin at 26% ( factoring resources cost i

-

US to cross 105-110 cr and improved margins at 15 % ( being in investment phase margins were lower, gradually improving)

-

Middle East around 50 cr and margins normalizing midway to 10%( margins have been near zero for past two qtrs , mgmt commentary suggests improvements)

-

Others around 35cr at 20% margins

570 cr to 600 cr and 125to 135 cr Op margins, at annualized basis it would be 2800 cr+ rev and 600 cr+ Op margins for CY 22.( considered 20% growth on Q3 base annualized)

Assuming they deploy 1000 cr+ cash judiciously - can get a biz of 300 to 350 cr revenue and 60 to 80 cr margins ( lower margins typically for US based companies- scope to improve post acquisition) - ofcourse this is pure cash based buy out but usually it’s mix of cash+debt and equity and hence size could be much larger

Combined we are looking at 3200 cr+ sales 750 cr+EBDITA as base case performance with scope of margins improvement. Current mkt cap is 8600 cr, at 2.5X sales and 11X EBDITA,

At present median midcap IT are trading at 30-50x EBDITA given sector tailwinds.

even at conservative 20X EBDITA market cap could be in vicinity of 14K+ cr. As company delivers better Qtrs and US acquisition nears closure a rerating likely to follow.

These are back of envelope calculations and could be off, Promoters have recently bought around 2500 price and stock is Stable in recent correction, can see invetred head and shoulders formation on charts, suggesting good base building.

Risks - 25% Attrition reported in Q2 is big issue, need to see how it trends going forward and impact on margins. Getting a good deal for acquisition is a watch out , given valuations will be high for good assets in current mkt - mgmt past records are assuring here.

Invested and adding on dips