NBFC who did excellent in FY18-19 due to their CV and Two Vehicles loan portfolio will come with bad news in this year. Market is very bad for automobile sector!

what are other growth drivers to compensate for auto slowdown for the company?

This is an interesting story. The company has steadily compounded AUM and Profits for 20+ years. There is a long runway for the company in the space of MSME financing and in affordable low ticket housing finance.

While there is geographical concentration risk as the company is concentrated on a few key states where it does direct lending like Gujarat and Maharashtra, these are also some of the most industrialized states with a large enough market for their products.

The company uses the word “indulgence” when talking about their clients to understand their profiles, which seems essential considering that in the absence of strong financial data to project cash flows and profitability for SME clients, it is upon the company to understand the business and the local factors thoroughly before lending to their clients. This shows in the NPAs too, the company has had it under control over long periods and the low ticket size and aggressive collection methods could have helped too, aside from solid disbursal criteria.

Hence, the company prefers to make their network dense in their existing markets before branching out to new markets. While, also lending to other NBFCs in non-core markets and with control over the asset quality those NBFCs further lend to. This again ties to the company’s belief that the last mile delivery is better done by those who are closer to the customer and understand the local factors and business better. The subsidiary MRHMFL though insignificant to their revenues now, looks to be one of the major growth drivers for the company going forward given the long runway and the company’s focus on lower middle class segment and ability to cross sell.

Few possible issues with the company.

- The cost of borrowing I assume came down to 8% due to the influx of IPO money and the company’s cost of borrowing earlier hovered around 9%, which I think it should revert to dampening the PAT growth in future. Please correct me if I’m wrong here.

- The scalability of the company. The company is still strong in maybe just 2 states after 20 years’ presence due to the nature of the SME lending requiring strong local presence and understanding barring the company from scaling up quickly.

- Any regulation barring the company to sell its loan assets to banks as priority sector lending.

- Strong possibility that the likes of Google (with a future product that is an amalgamation of GPay-GPay Jobs-Maps for Business) or Amazon can provide a better scalable solution for availing credit facilities for MSMEs. I believe it most likely is easier for a company like Google to innovate in this space than for a company like MAS to innovate an ecosystem like that.

- The company is not really cheap at 23 PE levels. I doubt there is significant room for PE expansion from here.

Looks interesting overall, though. Would love to have some more analysis on this company in this thread from other folks tracking this company for a while.

Disc: Tracking.

8 Likes

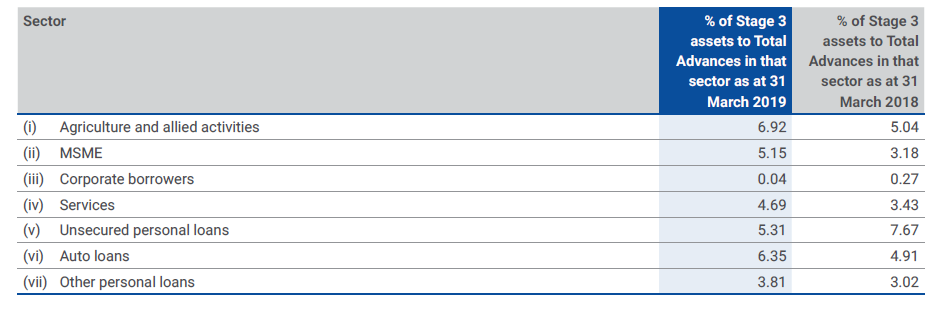

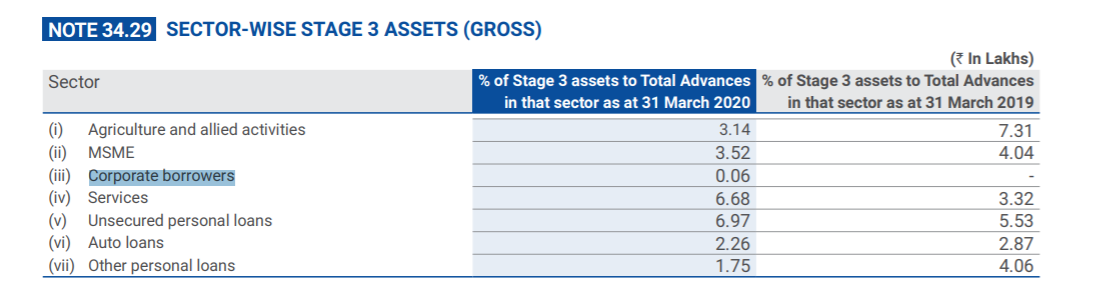

Was going through their Annual Report; one thing puzzles me that the segment wise NPA is ~3-5% for each segment, then how is the overall npa <2%. This indicated the direct lending part is not as efficient as it has been shown.

5 Likes

Strange this is one of the lesser discussed companies here given the stupendous track record of management, business performance and excellent stock returns.

Trying to decode the recent months sharp up move - December shareholding actually shows all big institutional players Axis MF, IDFC MF, Foreign Portfolio Investors lightening their positions.

The company is now trading around 5.6x book and 30 P/E - one notch below the league of the best NBFCs in the country. Any views on the recent stock outperformance?

PS: Coverage for Moneycontrol Pro subscribers - bullish on the company

https://www.moneycontrol.com/news/business/moneycontrol-research/why-we-continue-to-repose-faith-in-this-high-quality-nbfc-4676941.html

Disc: Invested at 530 levels

5 Likes

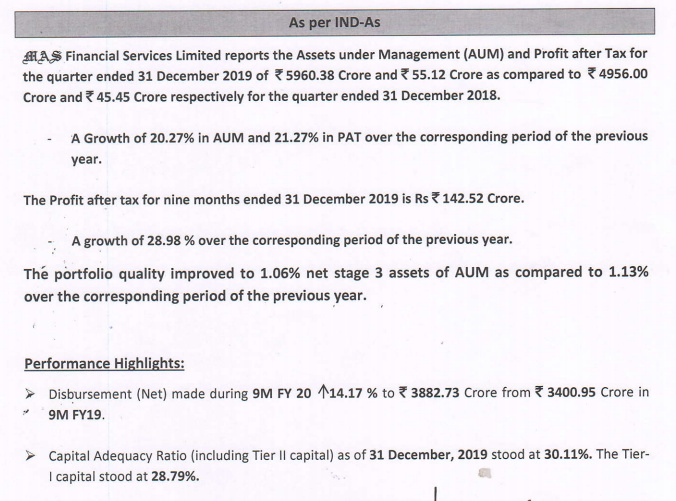

Steady Q3 performance given the turbulent environment for NBFCs. Bottomline growth mainly aided by corporate tax cut

Interest Income up ~15% YoY

PAT up ~20% YoY

Solid AUM Growth >20%

Improvement in Net NPA to 1.06%

Interestingly the stock hit a new life-high today. Company reminds me of Gruh Finance - which would keep on reporting steady performance quarter after quarter, and the markets kept lapping it up quarter after quarter. (although most results reaction was always immediately negative due to steady growth path and not like a rocket

4 Likes

Any one has any idea why MAS has fallen by 20% in two sessions?

I do not see any corporate announcements by the company to the exchanges.

Seems the valuations are correcting. Valuations of 5-6 times were not sustainable for a wholesale lender, no matter how good it is. But I believe stock will go a long way.

4 Likes

@hitesh2710

Does your perception about mas financial has changed or it is intact?

They have announced to reach rupees hundred crore debentures of 10 lakh rupees each.

Q1-FY2020 Investor Presentation Notes

- [Geographical diversification] 105 total branches. 59 Branches in Gujarat, 21 in Maharashtra, 10 in Madhya Pradesh, 10 in Rajasthan.

- [Size of business] 5657 cr of AUM, 7 lakh loan accounts.

- [Business Growth] In last 25 years, AUM has CAGR of 40%; Growing from 2 cr 5966cr. PAT has had a growth of 45% growing to 178 cr.

- [Capitalization position]: Adequately capitalized for growth. CAR of 35% (Tier 1 capital of 32%).

- [Provisions and NPA]: Gross NPA of 1.41%. Net NPA of 1.14% (30 june). Covid-provisions of 1.62% of book assets. The covid provisions have not been netted against the gross assets.

- [Liquidity Position]: Cash equivalents of 1300cr (July, 20). Sufficient liquidity to cover opex and debt liabilities for 12 months.

- [Moratorium] 26% of book under moratorium in June and 13% of book under moratorium in July. Company has not opted for moratorium benefits on the loan o/s from any of its lenders

- [Product Offerings] Micro-enterprise loans (Ticket Size: Rs 44k): 3424 cr. SME loans (Ticket size: Rs 20L): 1674 cr. Two Wheeler Loans (Ticket size: 48k): 400 cr. Commercial vehicle loans (Ticket Size: Rs 2.9L): 158 cr.

- [Cost of borrowing]: 9.3% in Q1-FY21 versus 9.23% for Q1-FY20.

- [Future Growth] Company guides for 20-30% growth in AUM in next 5 years. Company believes that growth along with quality is the key to enhance the shareholders’ value. The company will also explore the potentiality of entering into new geographies

- [Profitability] NII of 90cr in Q1-21. NII and PAT are down due to covid-special provisioning which is 1.6% of on-book assets.

- [Operating expenses] Operating expenses are down 37% YoY from 19.6 cr to 12.2 cr. Operating expenses as a percent of NII came from 20.6% in Q1-FY20 to 13.6% in Q1-FY21.

- [Breakup of Provisions] Company has provided a very granular break-up of the provisions. For example, they have created 26% provisions for Stage 3 Assets

- [Liabilities vision] Self Propelling Business Model – Capital requirement met predominantly from internal accruals

- [Credit assessment and Risk management] Robust and Comprehensive Credit Assessment & Risk Management Framework. For Micro-enterprises: Analysis of business potential and end use, cash flows and model (business to have cash profit for the previous 3 years). For SME Loans: Business operating history is required from minimum 1 year to 5 years depending on loan size. 50-70% of turnover to be reflected in current account. Eligibility criteria is based on turnover, debt/equity ratio and net worth on a case-to-case basis. Two-wheeler Loans: At least one property (residential or business) should be owned by the applicant or jointly residing family members. Commercial Vehicle Loans: Analysis of income, experience, and business stability requirements depending on whether the applicant is a first time user, first time owner, fleet operator or a captive user

Notes on MRHMFL

- [Business] MRHMFL provides loans for purchase of new and old houses, construction of houses on owned plots, home improvement loans and loans for purchase and construction of commercial property. It also extend loans to developers for construction of affordable housing projects

- [Business] With its continued focus on the rural and semi-urban segments, the company has 69 branches and have sourcing arrangements with 55 intermediaries – typically project developers and property agents

- [Business] Loans of up to INR 5 Mn. for residential and INR 10 Mn. for commercial. Provides housing loans to customers, who are primarily salaried and self-employed individuals and loans to developers for construction of affordable housing project. Tenure up to 300 months for residential and 144 months for commercial. Average Ticket size in Q1 FY21– INR 8,21,622. AUM as of June 30, 2020– INR 2,842Mn.

- [NPA] The Gross Stage 3 Assets is 0.36% and Net Stage 3 Assets is 0.26% of AUM as on 30th June 2020

- [Moratorium] 17% of book under moratorium in July, down from 20% in June.

- [Covid Provisions] The Company total special COVID provision as on 30th June 2020 stands at INR 21.05 Mn. which is 0.81% of the on book assets of Rs 258 cr

- [Capitalization] Company’s Capital adequacy remained strong at 42.07% with Tier I Capital of 33.26% and Tier II Capital of 8.81%. The Company has adequate capital and financial resources to run its business operations

- [Breakup of Provisions] Company has provided a very granular break-up of the provisions. For example, they have created 28% provisions for Stage 3 Assets.

Overall takeaway: Company is provisioning for Covid very conservatively. The company has successfully survived the 2008 great depression and looks prepared for next leg of growth coming out of covid.

Disc: Not invested yet but intending to invest in coming few days/weeks.

8 Likes

*It has not been mentioned in this thread, for the uninitiated, this business lends money without any security.

As a result, Covid related NPA will be high.

*Is an NBFC, so will have high interest Expense.

*It doesn’t have a technological platform, advancement, cutting edge, which Bajajfinance and a few others have.

Hi Amit,

thanks for adding your thoughts. They are a real risk wrt any cashflow based lender. However, I would not over-index too much on any such predictions or projections. The downward risks exist. But there is no way for anyone to make statements like NPA will be high with any amount of confidence or backed by data. Just my 2c. Based on similar thoughts as yours, I have reduced my position by half and now only have ~2% of PF in MAS financial.

1 Like

MAS Financial Services Q3FY21 Concall Update

> Prioritization of asset quality over loan growth has translated in best in class collection efficiency

> Credit cost normalizes to pre-covid levels of ~1%

> A gradual pickup in AUM growth should lead the co back to ~18% ROE levels by H2FY22E

Outlook: Positive

• The collection efficiency for the December quarter was at 96% which is very close to pre COVID levels and above 92% witnessed in the September month. 100% of collections happen online. This helped the co to manage its asset quality well even during demon period.

• CE is better compared to Bandhan (90%), CreditAccess (91%), RBL MFI segment (92%). MFI industry at large has witnessed CE of around 90% in Q3.

• As far as possible MAS will avoid doing restructuring and will prefer those accounts to slip. Restructuring is expected to be at 1% of AUM by March 2021.

• Excluding SC order on standstill, NNPA would have been at Rs. 67 Cr (1.98% of on-book AUM & 1.33% of total AUM). Cumulative management overlay provisions stood at Rs. 56 Cr. Apart from this, additional provisions of Rs. 36 Cr are also held. Thus total contingent provisions are at Rs. 92 Cr (2.7% of on book AUM & 1.8% of total AUM). This should be sufficient to deal with the stress in book.

• Credit cost runrate normalized to 1.1% during the qtr in line with pre covid level (was at 2.0% in Q1 & Q2).

• The on book exposure to Sambandh had been fully provided for in Q2 (~Rs. 18 Cr) and co has recovered back Rs. 14 Cr.

• Disbursements during Q3 were at Rs. 1031 Cr against a runrate of Rs. 1300 Cr pre-covid. Disbursement in Q4 will be around Rs. 1200 Cr.

• AUM declined by -15% YoY to Rs. 5055 Cr as the co had stopped growing its disbursements since Q3FY20 while collections continued to be strong. Co expects to resume its AUM growth from FY22 at 20-25% CAGR.

• Co holds Rs. 1,000 Cr liquidity and also has Rs. 500 Cr cash credit facility.

• Co has not been able to grow at a fast pace in 2W & CV despite having a low base as these segments do not offer a favorable risk-reward metric which the co finds in Micro Enterprise & SME segments.

• Tier 1 stands at a healthy 30.35% denoting that the co’s growth will be self funded with ROE heading back to normalized levels of 18% from H2FY22 onwards. Median Tier 1 of all partner NBFCs is at 20-22%.

7 Likes

@hitesh2710 and interested members

Just in case you have missed below or overlooked it …

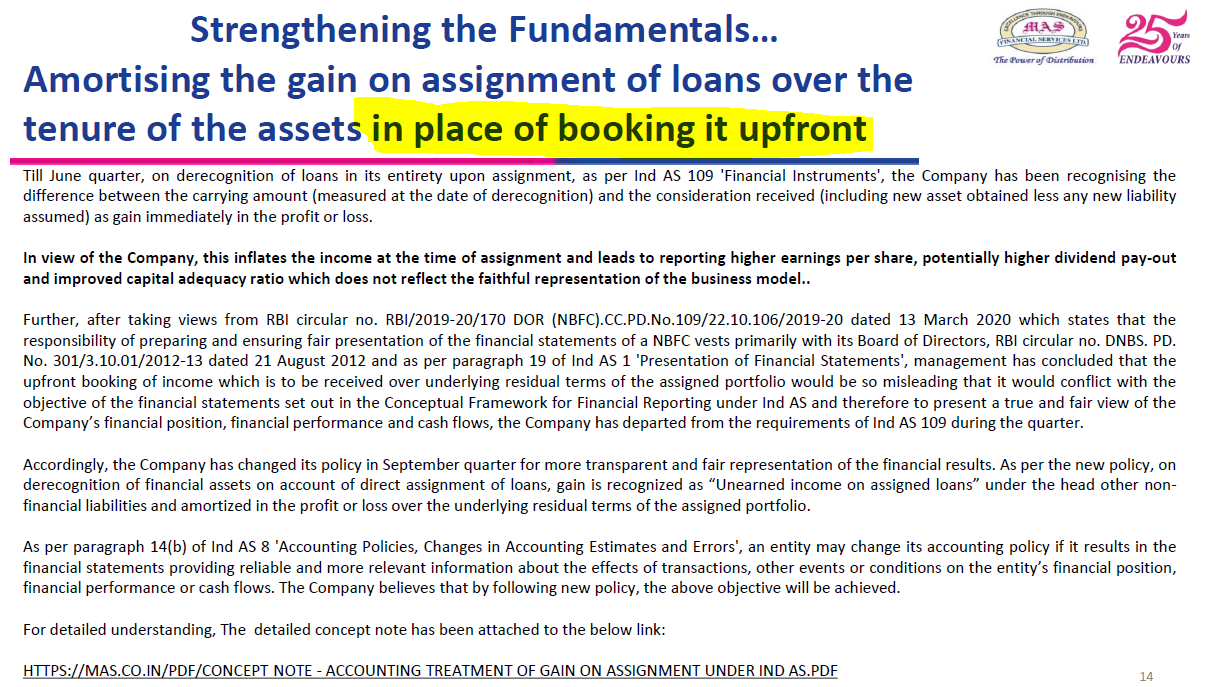

Company would have easily gone with IND AS rules to show better short term profit …

I feel this is very bold and apt step by the company to forgo the short gains for better accounting practice ![]()

![]()

Please correct my view incase of error …

6 Likes

Was going through their Annual Report; one thing puzzles me that the segment wise NPA is ~3-5% for each segment, then how is the overall npa <2%. This indicated the direct lending part is not as efficient as it has been shown.

NAP Data AS per FY 20…

the logical reasoning I could get out of the my limited understanding is as below …

Bit of MAS Asset structure

- In house (thorough 106 own branches ) – 40% of Assets are created

- Corporate borrowers (Onward Leading via NBFC’s )

– Around 60% of the leading is via this channel as you see

– this segment has least NPA i.e .06 due to none recourse agreement or MAS would get only current accounts

though you can see that other NPA or higher side in the range of 1.75 to 6.97 all this combined constitutes of only 40% (Around)

so when you combine both in house and Onward Leading via NBFC’s NPA’s tend to drop significantly… which could lead to NPA < 2

Note :: I am still trying to understand the company , please go through above and correct me if my view is wrong…

2 Likes

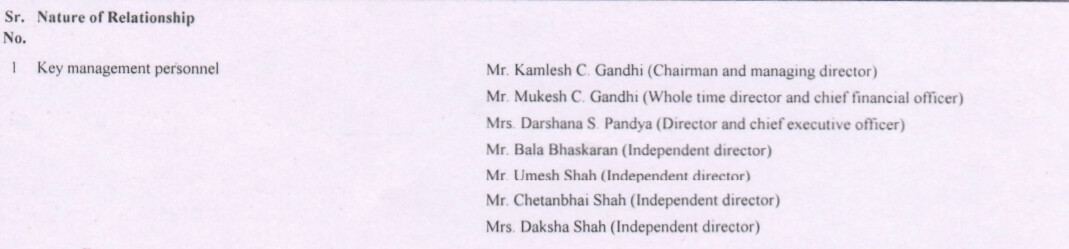

Mrs Daksha Ma’am is an independent director on MAS’s board as well as the managing director of another NBFC Altura Financial Services. In October 2019, Altura had sold its microfinance portfolio to Centrum Microcredit. So it seems like Daksha Ma’am may be an interested party in Centrum Microcredit. And as at June 2020, MAS had given a term loan of 94.96 Crore rupees to Centrum Microcredit. (https://www.nsdl.co.in/downloadables/commercial-papers/2019/LOF/INE865Z1404222092020LETTEROFOFFER.pdf#page=3)

Should this be viewed as a red flag?

I did not see any related party related to Centrum Microcredit in the

Better mail to invertor relation of Mas to check about the same…

Regards,

Rama

Hi - has anybody read this note from the auditors who’ve resigned today, and what should one make out of this -

Thanks

Earlier this year, RBI came up with this regulation:

According to the central bank, auditors must be rotated every three years with a cooling off period of six years before the next appointment, while joint audits by more than one auditor have been mandated for NBFCs with assets of Rs. 5,000 crore or more. That apart, auditors will also not be allowed to work for more than eight NBFC clients concurrently.

The notice which you have mentioned clearly states the same:

The Audit Committee considered the above prior to the Board meeting and noted that the resignation is on account of regulatory requirement.

5 Likes

Q1FY22 notes:

Net interest income stood at 78.6 cr down 13.7% from 91 cr in Q1FY21 and PAT at 36.8 cr flat yoy.

The AUM stood at INR 51,616 Mn. a contraction of 8.77% over the corresponding period. Gross Stage 3 Assets is 2.21% and Net Stage 3 Assets is 1.74% of AUM as on 30th June 2021. Collections exceeded disburements and hence the decline in AUM. Practically no business in April and May but still the disbursement was INR 1041 Cr during the quarter.

Break up of asset Rs. 2762 Crores is from micro enterprises loan which was last year Rs. 3424 Crores, SME loans is Rs. 1813 Crores as compared to Rs. 1674 Crores last year.Two-wheeler loan is Rs. 375 Crores as compared to Rs. 400 Crores last year and commercial vehicle loan is Rs. 211 Crores as compared to Rs. 158 Crores last year. Segmenet wise Stage 3 assests, 2%-3% for wheels, 2.13% in MEL loan and 1.95% in SME loans.

The collection efficiency for the June quarter was around 93%. Now the collection efficiency is at 96.5%, very close to the normal 97%-98%.

Company’s Capital adequacy remained strong at 28.42% with Tier I Capital of 26.55% and Tier II Capital of 1.87%.

As on 30th June 2021, the company had liquidity buffer of around INR 810 Cr and unutilized Cash Credit facility of around INR 485 Cr In addition the company has sanction on hand to the tune of INR 1300 Cr in the form of Term loan, NCD and Direct assignment.

During the quarter, the company has not restructured fresh loan. Assessing the financial position of

various borrowers and we will be in a position to complete assessment in Q2FY22. Expecting around Rs. 15 Crores to Rs. 20 Crores as restructuring demand.

The cost of borrowing for the quarter works out to be 8.72% vis-à-vis the last year which was around 9.24%.

On the Housing finance frount: In medium term housing finance to play an important role in the overall scheme of things of the group.AUM as on Q1 FY22 is Rs. 295 Crores as compared to Rs. 284 Crores last year, up 3.71%. Total income is Rs. 8.89 Crores as compared to Rs. 8.77 Crores which is 1.41% rise in income. Profit before tax is Rs. 1.06 Crores as compared to Rs. 1.41 Crores and profit after tax is Rs. 0.82 Crores as compared to Rs. 1.05 Crores last year. The reduction in PBT and PAT is mainly because of higher provisioning during Q1 FY22. net stage III assets at .56%.

Total recovery from the Sambandh Finserv is around 32-33 cr, MAS’s share is around 7-8% of that.

57-60% of AUM sourced by partner NBFC. As per management “On product to product in annual around 60% must be done through partner, in SME around 65% because majority of the business done though partners is in MFI and SME and in twowheeler and commercial vehicle the range is around 40% to 45% through partners and the rest will be through us.”

As per management, expecting disbursements to be strong in Q2FY22 and we should see AUM growing by end of current fiscal. Aiming to reach 10000 Cr AUM in next 4 years, given further covid waves don’t derail this. Plan to increase reach from current 3500 centres to not less than 5000 centres by penetrating other states deeply (apart from Gujarat). Expect the retail assets will increase and what looks like 57%:43% in favour of NBFC might look reverse in favour of direct retail that it might be 55%:45%. With normalization of economy expect wheels contributing 25% and 75% coming from MEL and SME. Not interested in being a SFB, focus is on the asset side of the balance sheet creating an efficient last mile delivery of credit across the segments.

Another thing which I noticed while parsing through the FY21 annual report, quoting from FY21 annual report:

“looking at the scenario due to the pandemic and the financial implications on the business of the Company and on the overall economy, Mr.Kamlesh Gandhi, Chairman & Managing Director and late Shri Mukesh Gandhi, Whole-time Director & CFO of the Company, have voluntarilyrelinquished their salaries for the Financial Year. Further, Mrs. Darshana Pandya, Director & CEO of the Company, had voluntarily relinquished her 20% of salary starting from the month of August, 2020 till February, 2021. The said waiver of salary was taken as a precautionary step for safeguarding company’s interest and as a proactive measure for monitory relief from the continuous adverse implications of Covid-19 until the market conditions were stabilized.”

I think this reflects well on the management and shows their cautious approach in stressed MFI/MSME sector.

Disc:- Initiated a tracking position, still trying to study and understand the company better. Not an investment advice.

7 Likes