MAS Financial Services is a Gujarat-headquartered NBFC with more than 20 years of business operations. Operates in 6-7 states of India.

Focused on middle and low income customer segments, and include 5 categories: (i) micro-enterprise loans; (ii) SME loans; (iii) two-wheeler loans; (iv) Commercial Vehicle loans (which include new and used commercial vehicle loans, used car loans and tractor loans); and (v) housing loans.

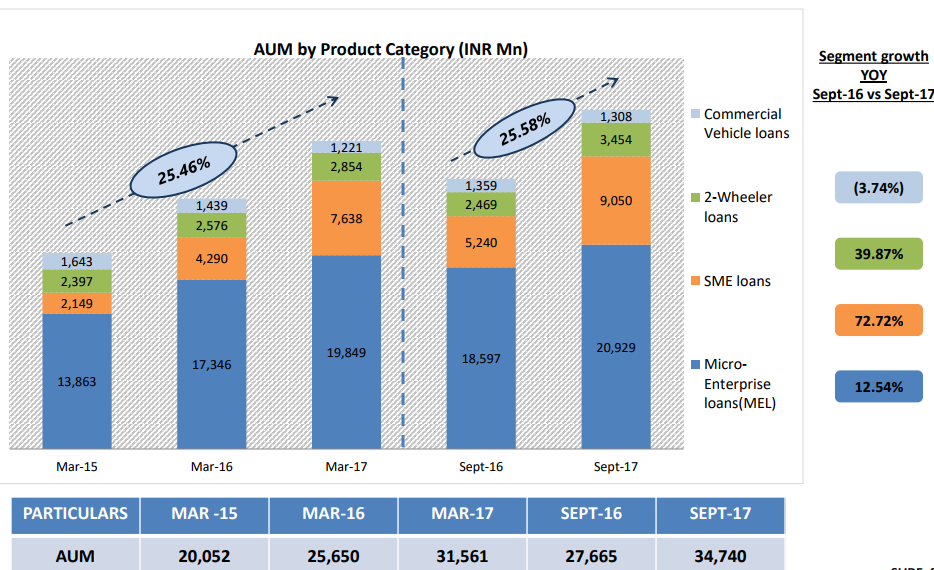

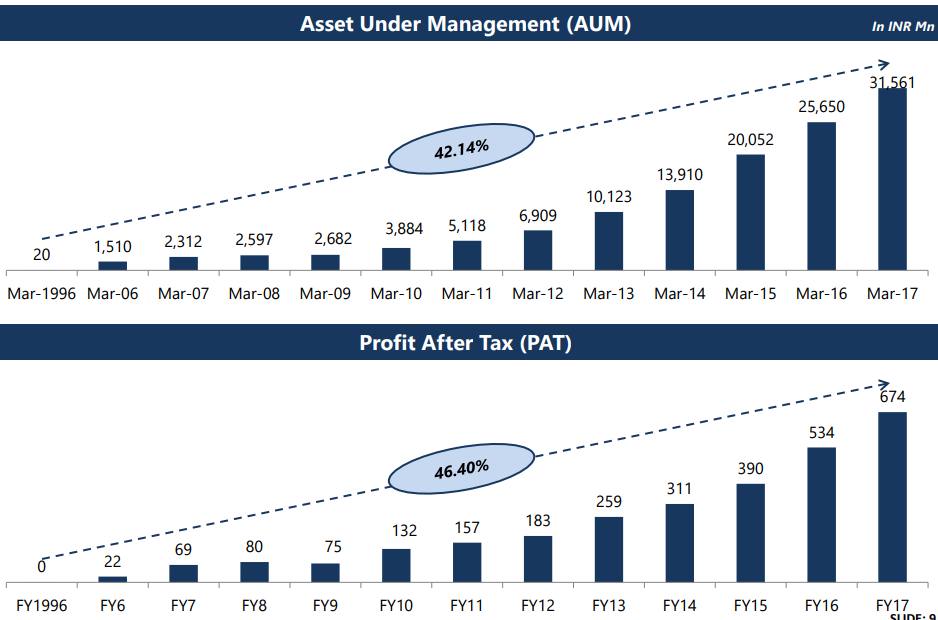

End Mar 31, 2017 AUM was Rs33bn. AUM increased at a CAGR of 34% since FY13.

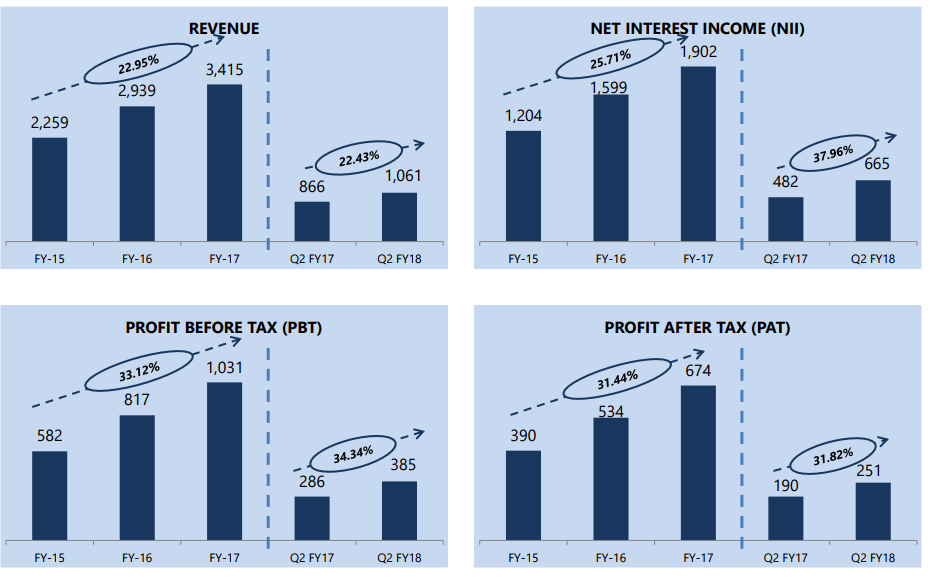

Excellent quarterly results. Quarterly net profit of Rs30cr almost doubled from last year. Small size, marque investment by Motilal Oswal, shareholder friendly management and an excellent history over the last 20 years of its operation. This stock has a lot going for it.

Low debt equity ratio and superlative past performance are positives. Has been a book value compounder in the past but related party transactions and heavy rise in receivables when compared with sales are red flags. Can invest only if promoter integrity is established. Any idea?

Mas Financials Services Ltd

Highlights of Q1 FY 19 results

Financials

As per IND-GAP Numbers

o AUM grew by 30.07 % to 4257.48 Cr compare to last year same quarter

o Profitability grew by 45.70 % to 33.75 Cr compare to last year same quarter

o GNPA stood at 1.19 % compare to 1.17 % last year same quarter on AUM

o NNPA stood at 0.95 % compare to 0.99 % last year same quarter on AUM

o Micro-enterprise loan book grew by 36.34 % from 1995 Cr to 2720 Cr last year same quarter

o SME loan book grew by 20.39 % to 1006 Cr from 836 Cr last year same quarter

o Two wheeler loan book grew to 380 Cr from 319 Cr last year same quarter

o Total 59.64 % of asset create through own distribution network

As per IND-AS Numbers

o AUM grew by 30.53 % compare to last year same quarter

o PBT grew by 60.7 % to 46 Cr compare to last year same quarter

o PAT grew by 86.14 % to 30.46 Cr compare to last year same quarter.

o GNPA at Stage-3 stood at 1.33 % and NNPA at stage-3 stood at 1.13 % of Balance sheet asset

o GNPA at stage-3 stood at 0.97-0.99 % of AUM and NNPA at stage-3 stood at 0.85 %-0.88 % of AUM.

Housing Finance Business

o As per IND-GAP numbers

AUM grew by 17.39 % to 179 Cr compare to 209 Cr last year same quarter

Gross profit grew by 19 % compare to last year same quarter

PAT grew by 25 % compare to last year same quarter

GNPA stood at 0.33 % compare to 0.44 % same quarter last year

NNPA stood at 0.24 % compare to 0.36 % same quarter last year

o As per IND-AS numbers

AUM grew by 17.94 % compare to same quarter last year.

Gross Profit grew by 10.09 % compare to same quarter last year.

PAT grew by 14.28 % compare to same quarter last year.

GNPA at Stage-3 stood at 0.36 % before provisioning and 0.26 % after provisioning .

GNPA at Stage-3 stood at 0.39 % before provisioning and 0.28 % after provisioning on AUM

Key Highlights

Company will remain on trend of increase 25-30 % growth in AUM and profitability.

AUM target is 5000-5250 Cr including Housing and it will result into 190-200 Cr of PBT as per IND-AS.

Company is focused on main products that are MFI and MFIL as 85 % of revenue comes from these two category .

Company has adopted a philosophy to first understand the liability then procide service and improving scalability.

Company has 3500 plus distribution network.

Impact of IND-AS on Borrowing side

o Total portfolio assign is 37 % amount to 1597 Cr remaining in Cash Credit (CC) facility. In CC limit company block the limit of CC and avail the WCL and it help in reducing the company cost of borrowing . Current cost of borrowing stood at 8.67 % compare to 8.74 % in march 2018. Borrowing cost on YOY basis stood at 8.72 % from 8.98 % last year.

Impact of IND-AS on profitability

o PBT stood at 33.5 Cr and PAT stood at 30.4 Cr for the quarter

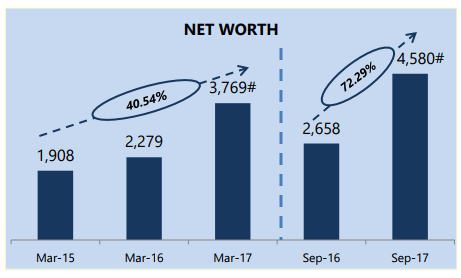

o Net worth on 31st march 2018 stood at 713 Cr compare to 752 Cr in April 2018 . 326 Cr of net worth looks at 161 Cr as per IND-AS. This is mainly because of re-recognized of CCPS and CCM from equity and recognized as liability. Same has been reversed in Sep-2017 because of same thing converted into equity.

Credit quality as per IND-AS

o Out of total 4316 Cr of portfolio category , 2759 Cr on Balance sheet and 2607 Cr in Stage1 and 110 Cr in stage-2 and 36.64 Cr in stage-3 and provisioning for the same was done at 8 Cr for stage-1 , 11 Cr at stage-2 and 5.3 Cr at stage-3 totaling to 24.85 Cr .

o 0.72 % of provisioning is now in stage-1 and stage-2 and14.47 % of provisioning is now in stage-3 and it is based on the probability of default base on past track record.

o Provision on AUM at stage-3 stood at 0.83 %.

MHFSL

Impact of IND-AS

o PAT grew to 9.08 Mn compare to 8.97 Mn last year same quarter

o Net worth stood at 30.6 Cr compare to 32 Cr as there was a option of Intended convertible shares and company intend to convert it into equity very soon. In April-2017 net worth as per IND-GAP was 21.91 Cr which according to IND-AS is 20.95 Cr.

Credit quality in Housing Portfolio

o Company have assign 206 Cr out of 210 Cr and out of which 197 Cr in Stage-1 , 9 Cr in stage-2 and 70 lakh in stage-3 and provisioning done was 0.4 % for Stage-1 & 2 and 27.43 % for Stage-3 under 90 DPD and 27.91 % on AU< basis.

Q&A

Kindly give outlook on the loan book mix ?

o Company continue to focus on MFE and SME so that will be around 75-85 % of total assets in future.

What is the yield on loan book ?

o 15.42 % is rate of deployment in MFI

o 15.46 % is rate of deployment in SME

o 18.18 % is rate of deployment in Two-wheeler

o 17.54 % is rate of deployment in commercial vehicles

What is the spread on the off balance sheet part on the cost part of the AUM ?

o Cost of fund for off balance sheet item is 8.52 % based on 1 year MCLR .

What would be the gain on assignment projects booked in current quarter ?

o In this quarter company has done 360 Cr of assignment in which company have booked 53 Cr as income . In march-17 company has booked 38 Cr

What will be the cost of fund going forward ?

o Currently it is 8.6 % and it may increase by 10 to 15 basis points over a period of time.

How much of company portfolio is through company channel partner and how much from direct ?

o Around 59 % of business is coming from Channel partner rest id direct distribution .

What are the risk available with 59 % of business coming with partner ?

o Biggest risk is not identifying the partner correctly and engaging and evaluating with them.

What kind of revenue sharing is there with the channel partner ?

o At the end the revenue from both direct and channel partner is same for the company . Average rate for lending channel partner is close to 13.53 % in June 18 and average cost of fund which is at around 7.2 %. Margin is close to average 6.62 %.

What was the fresh disbursement during the quarter ?

o It was 995.67 Cr.

How much new NBFC engagement done by the company in the quarter ?

o Around 3-4 new addition of NBFC are added this quarter and company work with 100 NBFC within the country.

What is the number of retention customers and cross selling strategy ?

o Around 30-40 % customers are repeat customers of company.

o For cross selling company have a call center so company do Data Mining and approach them time to time and that gives company an opportunity to cross sell other products also but limiting factor for the company is in-depth capability that existing customer capability is to first finish a loan and then take another loan.

What is the rejection rate of the company for the loan ?

o It depend on products for the company flagship product that is SME loan there the rejection will be anywhere between 25-35 %.

What is the ROE target ?

o 17-18 %.

Why company don’t want to leverage high as company has given good performance ?

o Company have 20.5-2.75 % kind of ROA including company assignment and on book if company leverage them to seven times and that will give ROE of 17-18 % so this is how company look on it .

In channel partner business does company have a maximum limit for each channel partner ?

o That depend upon the size and quality of the partner . Top 20 borrowers hold 20 % of company total AUM.

Where can be the lending to channel partner can be seen ?

o It is given on product wise . For each different product different lending is provided underline.

Where will be the Housing business in next 2-3 years ?

o Company first target is to achieve 1000 Cr by 2-3 years and on a 1000 Cr base company intend to grow anywhere around 30-40 % which will double company AUM every 2-3 year and the markets are large to cater . AUM in FY18 is 209 which is a growth of around 18 %.

Around how much cases company do on quarterly ?

o Around 100-150 Cases on quarterly basis.

@Julian, You got anything negative about the promoters? Any examples where they have short charged minority investors?

In my view they have a demonstrated track record of more than 20 years of consistent growth. I have seen their presence in some retail shops as well many years back. Since then they have moved a long way and if u see the presentation and annual report etc, u will find that the AUM has grown at close to 42% cagr since 1996. There are very few companies that have demonstrated these kind of track record.

The litmus test for this company was in 2008 and 2016 time periods and there too it has not suffered much.

A presentation on MAS Financial I presented as a stock idea at VP annual conference at Goa 2018.

Please find attached the short presentation prepared from data available from company’s presentations and annual report etc. MAS FINANCIALS.pptx (60.4 KB)

Their Debt Equity Ratio is 2, which is very low for a finance company. I do not think they needed to raise capital during the IPO.

This can be taken as a positive or a negative. Unnecessary dilution hurting ROEs is a bit negative.

Also, 58% AUM is microfinance. After demonetisation, many companies like Equitas, Ujjivan etc are focussing on shifting business from microfinance to other avenues… What is making these companies exit from the sector that made them… I believe this sector has a huge opportunity but political interference is the main issue.

The company has made a few crore rupees loans to related parties Paras capfin pvt. ltd. and M power micro finance ltd. Also there is a heavy rise in receivables for 2018 when compared with sales indicating that the net profit may not be real to some extent.

ROE is a multiplication of ROA with leverage. Considering average ROA of 2.5% a leverage of 2 times will give on 5% ROE which is not sustainable. The company will go back to 7 times leverage (so as to get 17.5% ROE but only 12% ROE in effect after 20% dividend payout) .

Hope the promoter comes out with clarifications on the above issues and inform his comfortable leverage position. The stock is overvalued in the present leverage condition.

MAS corrected 15% today (CMP: 382), thats 40% down from past 2 trading sessions is there any reason for the fall or is this a spillover effect of IBHF and ILFS episode?

Mas Financial Concall 1/11/2018

These are my personal Notes from my understanding. Views may have errors.

Management order of Focus : Quality > Profitability > AUM

To grow Top Line is easy but to strike a Balance between Quality , Profitability and AUM is most important.

AUM grown from 3400 Cr to 4625 Cr which is 39% increase YoY. Target set at the start of the Year was at 5200 Cr AUM which they are confident of achieving by the end of this Year.

Loan Book grown at 35% CAGR in last 5 Years due to Increase in Ticket Size as well as increase in number of Partners.

Caters to mainly 4 segments which are MEL , SME , 2W and CV.

MEL and SME loans Comprises 85% of AUM . MEL loan book Grown at 40% , SME loan book grown at 24% , 2W Loans growth at 25% and CV growth at 15%.

78 Branches in the Parent Business and 47 for Housing Business ! Total 3500 Centers across different states in MP , Rajasthan , GJ , TN , Karnataka , Maharashtra.

Working with 100 NBFCs right now , started with 1 NBFC in 2010. Average ticket size of NBFCs they lend is around 250 Cr. For these NBFCs to grow by 25% , they need little fund of 60-70 Cr. NBFCs they work are in good Position. They check the underlying asset before assigning the Loans to these NBFCs. They continuously monitor all the Partners.

Subsidiary : Mas Rural Housing and Mortgage : Growing it cautiously. AUM growth at 25% Year on Year. NNPA at 0.26 % vs 0.32% .

Management View of Current Scenario : In the events of Crisis , everyone becomes Irrational and start painting everyone with Same Brush. Approach towards individual Companies should be discreet. In Good Times , Not every Company is Good and in Bad Times , Not every Company is Bad. MAS has experienced 1995 Crisis , 2002 Earthquakes , 2008 and 2013 Liquidity Crisis. Companies with Sound Fundamentals will navigate through these times and will grow and create good assets. For India to Grow at 7% of GDP , NBFCs are the backbone. NBFCs remains the most important last mile delivery of credit . There is no slowdown from the end user demand and these are temporary times which will pass soon.

Company Borrowing Resource Mix : 52% Assignment , 32 % Cash Credit and around 13% Term Loans. There is no CP outstanding as of now. The company is in comfortable Position with regard to liquidity. There is no slowdown in assignment. They have enough Sanction Limit till June 2019.

Cost of Funds : 8.95% (H1 FY 19) Vs 8.65% (H1 FY 18). This Quarter , they raised around 225 Cr from Assignment and around 200 Cr from Cash Credit at a cost of 9.25%.

Rates at which they lend to NBFCs is around 13.75% and 17.65% to direct Customers.

AUM grew by 34.36 % to 4914 Cr from 3657 Cr last year same quarter.

PBT grew by 46.72 % to 56.86 Cr from Cr 38.75 Cr last year same quarter.

PAT grew by 47.75 % to 37.29 Cr from 25.34 Cr last year same quarter.

GNPA stood at 1.8 % and Net NPA stood at 0.88 %.

IND-AS Number

AUM grew by 34 % to 4956 Cr compare to last year same quarter.

PBT grew by 50.31 % to 69.36 Cr from 46.14 Cr last year same quarter.

PAT grew by 50.94 % to 45.45 Cr compare to last year same quarter.

Nine Month FY19

PBT grew by 47.24 % compare to last year same period.

PAT grew by 55.20 % compare to last year same period.

GNPA at stage-3 before provisioning stand at 1.38 % compare to 1.37 % last year

Net NPA at stage-3 post provisioning stood at 1.3 % compare to 1.26% last year

Disbursement grew by 29.26 % to 3400 Cr from 2631 Cr last year nine month.

Key Highlights

In company liability is at place and company have not done any mismatch of funds ever and that help company to grow.

MSME Funding

As on 31st Dec MSME loans stand at 3062 Cr which is a 35 % rise over last year compare to 2266 Cr

As on 31st Dec SME loans grew by 32.99 % to 1192 Cr from 896 Cr last year

Two Wheelers

Grew by 41.39 % to 5020.51 Cr compare to 3055.42 Cr because of the advantage that many of the players working in this segment has slowdown their disbursement because of their internal liability issues

Commercial Vehicle

Grew by 13 % where AUM stands at 150.19 Cr compare to 139.03 Cr as on 31st Dec 2017.

Company have more than 3500 distribution center across six states of operations add to that company have partnership with various NBFC which stood to close to 120 which is growing from strength to strength.

HFC

I-GAP

AUM grew by 31 % to 251.37 Cr compare to last year.

Total income grew by 28 % on QOQ basis

PBT grew by 61 % on QOQ basis

PAT grew by 78.63 % on QOQ basis

GNPA at conventional 90 DPD stood at 0.32 %

NNPA at conventional 90 DPD stood at 0.25 %.

IND-AS

Q3FY19

AUM stood at 251.93 Cr on QOQ basis.

PBT stood at 85 lakhs compare to 86 lakhs QOQ

PAT grew by 25.01 % to 72 lakhs compare to 57 lakhs QOQ

GNPA stood at 0.34 % compare to 0.36 %

NNPA stood at 0.24 % compare to 0.26%.

Nine Month Basis

PBT grew by 34.98 % to 3.26 Cr from 2.42 Cr

PAT grew by 57.19 % to 2.64 Cr compare to 1.68 Cr

Liability

Company finance 50 % from direct assignment , 35 % from WC facility and 15 % from term loan. Company never had any mismatch. In direct assignment company get door to door maturity and term loan is for long term purpose.

During the quarter company raise 780 Cr by assigning the portfolios

For the quarter company average cost of borrowing was 9.1 % but incremental cost has gone up to 9.75 % and out of that half will be pass on to customers,

Going forward company will touch the capital market because now company siz is bigger one and also working on raising ECB also. In borrowing mix company will have some portion of capital borrowing from the capital market and borrowing through the ECB route.

Company use Commercial paper for reduction of the cost rather than enhancement of the resources.

company have raise its lending rate between 0.50 to 0.75 % that covers 65 % of portfolio. In MEL lending rate is 15.5 % ,SME at 15 % ,Two wheeler is around 17 % ,HFC is 17.5 %. From September overall it increase from 15.27 % to 15.55 % so it increase by 0.35 %.

Outlook

Concentrate on MSME segment where company see tremendous scope

Continue to focus on two wheeler and commercial vehicle also with deep penetration under long vintage and relationship with the two wheeler dealer across the country. Continue to see robust growth in two wheeler business also and in commercial vehicle there will be decent growth.

On Distribution from current 72 branches company plan is to expand to 150 branches in next 2 years.

Company will continue to focus on technology side on transaction purpose.

Company have two month of sanctions on hand for various type of liability that company need in Q4 and Q1.

is there any reason for the fall or is this a spillover effect of IBHF and ILFS episode?

is there any reason for the fall or is this a spillover effect of IBHF and ILFS episode?