Introduction:

Marshall Machines Limited is a micro cap stock [Market Capitalization- 18 Crores], listed in NSE Emerge platform. Lot size is 3000 shares.

Marshall Machines Limited is in the business of developing, manufacturing and marketing of machine Tool Equipment including wide range of single spindle, patented double and four spindle CNC machines, automated robotic solutions and patent pending IoTQ [internet of things and quality] suite of intelligent equipment. Computerised numerically controlled (CNC) machines are electrical cum mechanical devices which are capable of controlling tools, with high-precision via a computer programming. As technology further leads, intelligent machines are now becoming a reality. They are providing product offering and solutions to wide range of industries including manufacturers of Axles, Crankshafts, Auto Parts, Fans, Pumps, Bearings, Gear Blanks, Bushes, etc. They claim that their machines are known for reliability and quality, innovative technology, quality manufacturing and complete service and support are part & parcel of the Marshall experience.

Financials:

FY

Revenue

Ebitda

Net Profit

Cash Flow from Operating activity

2013-14

39.3

5.2 (12.26%)

0.6

1.4

2014-15

42.6

6.2 (13.39%)

0.2

(-)0.8

2015-16

43.9

5.6 (12.48%)

0.4

7.1

2016-17

50.5

6.5 (12.25%)

1.2

11.5

2017-18

59.4

12.9 (21.55%)

5

5.2

2018-19

65.5

15.4 (23.24%)

5.8

13.6

2019-20

60.5

16.4 (25.68%)

3

11.5

For the last 3-4 years, the company is investing capital in the intelligent technology. The figures are reflected in cash flow from investing activities and higher depreciation. The company has reasonable amount of debt, debt equity ratio of 0.8.

New Initiatives:

Marshall is Dealer of M/s SPINNER (Germany) one of Europe’s top builders of Turning & Machining Centres. Marshall has Technical Partnership with M/s CARON Eng. (USA) for machine performance enhancement technologies. Marshall had a tie-up with M/s DOOSAN (S. Korea) from 2012-2014 to produce LYNX 220 series in India.

In 2019 end, Marshall tied up with the world’s leading IIoT Platform (Machine Metrics) who has its systems installed on thousands of CNC machines in hundreds of customers AND with THE TOOL & GAGE HOUSE, one of the largest dealers of measurement equipment who has almost all top OEMS & TIER 1 & 2 companies in its customer base. Marshall will integrate Machine Metrics solution for machine monitoring, called Machine Metrics Production on existing machines for OEM, Tier 1 & Top Tier 2 companies. Apart from direct revenue, it will build relationships and help reach out to Vendors of OEM & TIER 1 companies. Further, it will Pre-Load MM in its top end machines & automated lines to deliver high value to customers & enhance the saleability of its products. The company feels that it is a HUGE Competitive advantage for Marshall.

Lately the company engaged top world dealers- The Tool and Gage House (TGH), and Morris South to sell its products.

Marshall Automation America, Inc. successfully started operations from Atlanta, US launching & inaugurating their Technology Center.

The company has been awarded 5 patents and 16 patent applications are pending.

Recently the company was awarded order worth INR 29 crores for ROBOT OPERATED MACHINING CELLS from M/s ROCKMAN.

From 10% share in FY 19, sales of Smart Automated Machines rise to over 40% in FY 20.

The thesis of Investment:

Automation is being accepted. The company has potential to grab the opportunity in affordable automation space. Further government push on Make in India and Atmanirbhar Bharat can also help the company.

There are large organized players in automation, serving large industry. The company emphasis on affordable automation can find acceptance in MSME sector.

Attractive valuation- the company is available at 0.5 times book value, 0.3 times sales and 6 PE.

Automation businesses operate on a better profit margin. OPM is increasing sequentially for the last 3 years and may increase in the future. Decent margin improvement is expected. With topline growth and margin improvement, net profit can grow at a quicker pace.

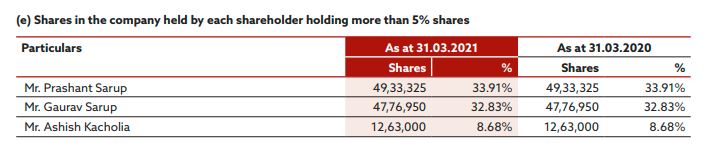

Shareholding pattern is attractive. The promoters own almost 74% of the equity. Further, 8.5% equity is held by Ace Investor Ashish Kacholia.

Risk Factors:

Investing in micro-cap companies are extremely risky and it can result in loss of 100% invested capital.

The products of the company do not have high customer loyalty. Further, any change in technology can make their products obsolete.

With covid lockdown, the company is not likely to put good results in the current scenario.

Hey , few days back I was also going through its financials and company’s website. I have few observation , if you reply it would be helpul for further discussion -

Even a very low small revenue base, company was unable to show any growth in last 4-5 years.

What’s the reason behind sudden jump in the depreciation from 3.73 cr in 2019 to 8.1 cr in the year 2020. Whereas no such changes in the fixed assets comparetively.

In the Fixed assets sechdule, there is leasehold plant and machinery of over 2.5 cr. Any information about nature of such P&M.

Inventory turnover is very low, as they are in research based machine manufacturing.And inventory level is very high and increasing comare to turnover. It may be the case, lying inventory is now out of demand.

It is very true to say that even on a very small revenue base, not much revenue growth is evident. Still, the topline has grown by 50% from 40 crores [2014] to 60 crores [2020]. Actually in my view that change has started coming since 2017. Have a look at following figures:

FY

Fixed Assets

Cash flow from Investing activity

Depreciation

Trade Receivable

Current Asset

2013-14

14.4

(-) 2.4

1.4

3.9

36.1

2014-15

12.6

(-) 0.3

2.3

5

46.1

2015-16

12.5

(-) 1

1.2

5.7

46

2016-17

16

(-) 5.1

1.6

8.2

48.8

2017-18

22.8

(-) 8.9

2.2

11.4

56.6

2018-19

46.4

(-) 27.3

3.7

12.4

61.2

2019-20

52.9

(-) 14.5

8.1

14

68

My observations are as follows;

The fixed asset of the company has started growing since 2016-17, it has grown from 16 crores to 53 crores.

When we look at the cash flow statement, it is evident that since 2016-17 the company is investing good amount of money.

Depreciation has grown proportionately.

The investment has been made largely through internal accruals, though some financing has been done.

From 2017-18 onwards the operating profit margin has jumped from 10-12% earlier to 23-25%.

Trade receivable appears to be reasonable, approximately 3 months revenue.

Inventory appears to be on the higher side, 46 crores in 2020 and 39 crores in 2019; almost 75% of the annual sale. It is also possible that some of the inventories may have become obsolete. Inventory turnover is low.

Still, we have to give certain benefits of doubt to micro-cap companies, had everything been okay and hunky-dory, it may not be trading at 18 crores valuation, almost 1/3rd of sales. Honeywell Automation is trading at almost 13 times sales and 80 times earnings.

It appears that Q4 of 2020 was impacted due to covid. Further, the financial year 2020-21 had also been affected, and thus we may not expect a good result for 2020-21. However, in my view the company is promising and may post good result in the current financial year, if covid impact do not affect much. The management appears to be pro-active in finding new opportunity. Recent 29 crore order from Rockwell shows that the company has the potential to enter into a higher league.

I bought and sold its shares a couple of years back. The company has more than Rs 33cr of borrowings compared to the market cap of Rs 20cr. I won’t call this a reasonable amount of debt. Indeed, there are not many SME-listed companies with such high debt to market cap ratio. The company still seems to be in the need of further expenditure towards marketing and sales, and further expansion. Will they be able to raise funds at favorable terms? This is the key reason for me to avoid investing into this company.

The high depreciation of Rs 8cr (operating profit was Rs 15cr) in FY20 seems like a write-off and more such things may happen in the coming quarters.

The path they have taken has not been inspiring. An investment at this time will be based on faith on the promoters that they recognize the debt burden, are willing to improve the financials in the new few quarters and are able to do it.

This sector is lucrative with a huge runway and typically low debtor days. One may consider Macpower CNC, which is a peer with great financials and attractive valuation. I have a substantial position in Macpower.

Macpower CNC is a machine maker, what Marshall was 4-5 years ago. We are analyzing Marshall for automation capability, which it is trying to develop. Early signs of success are evident in the operating profit margin going up substantially, the product mix is being shifted in favour of automated products and 29 crores order from Rockwell for robot operated machining cells.

Depreciation figures are not write-offs, they have fixed asset of 52 crores and depreciation of 8 crores is reasonable on such asset. Further, as their asset will shift towards computers and software, a higher rate of depreciation is available.

Of course, the debt of 33 crores is at a higher level, still, an interest coverage ratio of 4 is available. Cash flow from operating activity has been healthy and I don’t see any problem in debt servicing.

Faith, Yes. Every investment is an act of faith, and it is a hundred times more true when you are investing in nano caps.

Marshall Automation America (MAAI) is not a subsidiary of Marshall Machines but a company held by promoters. The company said in its IPO DHRP that MAAI will become subsidiary by FY19 but this has not happened yet.

There are general issues of delayed annual reports and delayed results.

The company has short-term loans with high interest rates.

One can check multiple auditor comments in the latest results (page 9). It shows the less than perfect corporate governance in the company.

“the product mix is being shifted in favour of automated products” Any links to substantiate this?

" 29 crores order from Rockwell" Can you please share the details and any link/references in this regard? I could not find anything in the corporate announcements in the last year.

“Early signs of success are evident in the operating profit margin going up substantially”. A large part of the margin improvement in FY20 seems to have come from lower raw material cost. Is it sustainable?

Your observations are perfect and need to be kept in consideration.

Regarding the latest tie-ups, orders, product mix, etc., the company has discussed it in the following investor presentation [August 2020]. Marshall-Machines-Presentation-20082020.pdf (5.0 MB)

Their website, marshallcnc.com is also well made and gives a whole lot of information on technology they are working and developing.

Thanks a lot. I could not find this presentation on NSE/BSE. There is no corporate announcement dated 20 Aug 2020 by the company. No wonder I could not find the information about product mix.

FY 2020-21 results in not out yet.

Nevetheless, the stock is in the upper circuit for the last many days. Any idea, why?

Lately Marshall Machines Ltd has announced that Mr. A.N. Chandramouli, a highly qualified, experienced, and distinguished person has joined the Company as a Strategic Advisor to the Board. Mr. A.N. Chandramouli headed Makino India for 6 years as President & CEO. Makino is a Japanese machine tool company considered among the best in the world. Mr. Chandramouli later joined Switzerland based Starrag Group as MD of Starrag India for 7 years till his retirement. Starrag is the world leader in high performance CNC machines used in Aerospace, Medical and Automotive

industries.

Marshall Machine has come out with excellent H2-2021 results. Topline has gone up to 52 crores, more than a 100% jump from H2-2020. Net profit has gone up to 2.3 crores, a 5 fold increase from H2-2020. The annual result looks a bit muted on the profit front due to washing out of H1-2021 owing to corona lockdown. Marshall_Machines_2021.pdf (3.7 MB)

The company has come out with investor presentation. Following are the key points:

Completed a significant CAPEX between 2018-21, taking manufacturing capacity to ₹250 crores in Sales from erstwhile ₹75 crores in 2017.

Potential to do 25% EBITDA Margins on the sale.

Order book has increased 19% to 51 crores. Order bids has gone up by more than 100%. Order Book and Bids as on 31st March, 2021 are at higher prices compared to 31st March, 2020.

AFAIK this is the first time they have said they were doing capex that will take their manufacturing capacity to Rs 250 crores in sales. Please correct me if wrong. Isn’t this company intriguing?

They are talking about debt reduction. I would have liked if they also talked about Marshall Automation America and the Rockwell order. They had many more things in their “Vision 2021” presentation but there is no follow up, as usual. Each presentation is so different from the previous; each seems to have come from a different management team / power source!

Although they have not kept their words in the past (check my posts above) I hope they do well this time. I am tempted to buy as this stock is still cheap but I am undecided. I will either buy or will wait until the company shows further positive signs, in particular shows friendliness towards minority investors.

In the annual report 2020-21, there is no mention of Marshall Automation America as subsidiary. Though it was stated by management that Marshall Automation America Inc will be converted into a subsidiary in the year 2018-19, it has not been done till date.

Marshall Machines is more than 60-year old company, with long-standing relationship with customers. Run largely by second and third-generation promoters.

NSE SME-listed with lot size of 3000. Thus, investment should be in multiples of around Rs 100K. Company has started the process to transition to the main board soon.

The company has expanded capacity for Rs 250cr revenue and 25% EBITDA margin (source: company presentation). The current market cap is only Rs 45cr, which leaves potential for huge multibagger returns.

Marshall Automation America (MAA) was set up a few years back to work on robotic automation, and have a number of technologically advanced offerings such as Industry 4.0 technologies of SmartFac (Productivity) and SmartPredict (Predictive Maintenance). They have deals with TGH and Morris South for distribution in the US.

Primarily a product-based revenue stream. Prominence of AMC and Service & Maintenance to rise in future, as the company moves towards complex and automated offering.

Promoters hold more than 70%, which gives confidence.

Risks

Leverage play on GDP/export growth. Continued low demand can delay stock performance.

Corporate Governance can be better. Failed to keep their words in the past. MAA was to become a subsidiary as per IPO prospectus but this has not happened. It is owned by the promoters. In the future, need to look out for related-party transactions to ascertain whether Marshall Machines shareholders will be allowed to benefit.

There have been general issues of delayed annual reports and delayed results.

There have been multiple auditor comments in the last few financial results, though not of high level of concern. It shows the less than perfect corporate governance in the company.

High debt of Rs 39cr (March 2021), with short term loans at high interest rates.

High working capital, the company says, due to high inventory in a 6-month long production process, and due to high debtors given seasonal burstiness in demand.

The company had a “Vision 2021” presentation at the end of last calendar year that included many things such as Rockwell deal and details about MAA. Many of these details are lacking in the latest presentation.

Scenarios

Best case: The company is able to leverage its work in the US in a big way. Debt is paid-off quickly after windfall profits. Minority shareholders are allowed to benefit, for example, from dividend. In this case, huge re-rating of share price is likely over the next few years.

Worst case: The company continues in its present form largely oblivious of the concerns of the small shareholders, for example, not sharing details, not keeping their words. However, the current market cap of around Rs 45cr is quite low (8x PAT of FY19), so there is limited downside.

As of now, based on experience, the two scenarios seem equally likely to me.

Price and Technicals

The well-known investor Ashish Kacholia owned more than 8% but sold in 2020. High churn among the non-promoter public shareholders is visible in the shareholding pattern history of the recent quarters. Promoters holding of more than 70% is stable, which is comforting.

There is strong base around the current price.

Although future price movement is unpredictable for a mispriced stock, the current optically high PE ratio (~80) may keep the upside limited in the near term.

As per their FY 21 AR Ashish kacholia still holds 8.68% shares as on March 21. Not able to get any latest shareholding data. Can you pls share the source of his stake sale.

You can check the latest shareholding pattern at NSE company page > Corporate Information > Shareholding Patterns > View All > Click on any row.

Please confirm what you find. Under the “public shareholder” tab, there is only one name “RAJESH KUMAR” with 1.55% shares.

One can check the shareholding pattern of the previous quarters also. Ashish Kacholia’s name occurs in March 2020 shareholding pattern but does not occur in the March 2021 shareholding pattern. That’s why it is strange that his name appears in the FY21 Annual Report. Given the company history, anything is possible. This needs to be investigated further.

In any case, my investing decisions are independent of whether Ashish Kacholia holds or not. However, a glaring error in the annual report would be a big issue.

Also, I corrected the lot size in my writeup above.