Since last Q solid numbers the company share price really has been moving, which is good a lot of shareholder value lies to be made in Marksans that being said it’s important to keep an eye on valuation metrics since markets tend to get euphoric at times.

Given the future growth scenario as discussed by management in the recent concall seems to be largely discounted given the current CMP.

The 3000cr mngmt guidance by FY26 seems to be a less optimistic take and might get revised in a couple of quarters. The trailing pe as of writing this stands at 34, bv/cmp at 5.7. Unless we see continued growth in the US OTC market and the promised revival of UK and integration of Europe in the revenue mix the valuation seems reaching a far stretched land.

As usual good set of results. waiting for tomorrows press conference for more info regarding backward integration and M&A news. share price may not react much because of rich valuations already.

As usual great set of results. but because of tariff war we may have a bumpy ride for next few months. all-in-all great. My assesment of tariffs on india is musk wants tesla entry in india so they will negotiate automobile tariff with pharma. sensible option for both countries.

Does anyone have any take on current tariff situation and how it can affect Marksans Pharma in coming Qtr as there major chunk of revenue comes from US only.

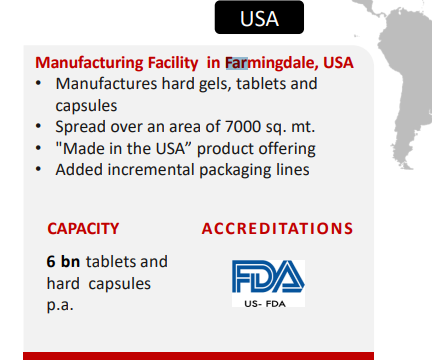

We don’t know exactly how these tariffs are going to be. But I believe, Marksans may be one of the Indian companies who may not have a significant impact as they have a manufacturing plant in Farmingdale.

But there are products imported as well. It will be tough to estimate the effect of tariffs now.

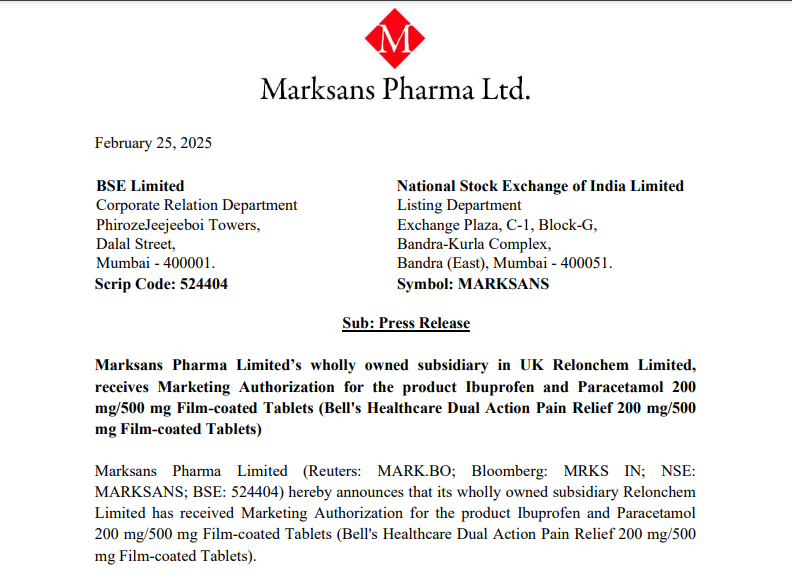

Company announces that its wholly owned subsidiary Relonchem Limited has received Marketing Authorization for the product Ibuprofen and Paracetamol 200 mg/500 mg Film-coated Tablets (Bell’s Healthcare Dual Action Pain Relief 200 mg/500 mg Film-coated Tablets).

As the heading of this topic suggests - does Marksans still remain on course to be the next Pharma Biggie ? Especially, given that it has manufacturing facilities in US, UK, ANZ etc, and therefore probably having competitive advantage in terms of tariffs impact ? Would love to hear perspectives from group members who have passionately followed this company over past few years.

Even if Marksans has manufacturing capacities across the region, the tariffs might be on the APIs which probably get imported, so we don’t know the full extent of what may happen which is why the stock is tumbling

During the Q4FY25 earnings call, Marksans Pharma’s management clarified that any tariffs introduced would likely be treated as a force majeure under existing contracts, giving scope for renegotiation of terms. While nominal tariffs (e.g., below 5%) may be absorbed by the company, any significant increase (e.g., above 10%) would be passed through to customers and ultimately consumers.

The company remains competitively positioned even if tariffs are implemented, as US-based manufacturers also rely heavily on imported raw materials, primarily from China, which are themselves subject to tariffs. Thus, the relative cost advantage of Indian manufacturers like Marksans is expected to persist.