12 posts were split to a new topic: Macros 2.0: Economy-Markets-Cycles, and Actionables?

article discusses about the industries impacted…

Not sure where to post…

1 Like

12 posts were split to a new topic: Lockdown - Extension - Market Timing Agility

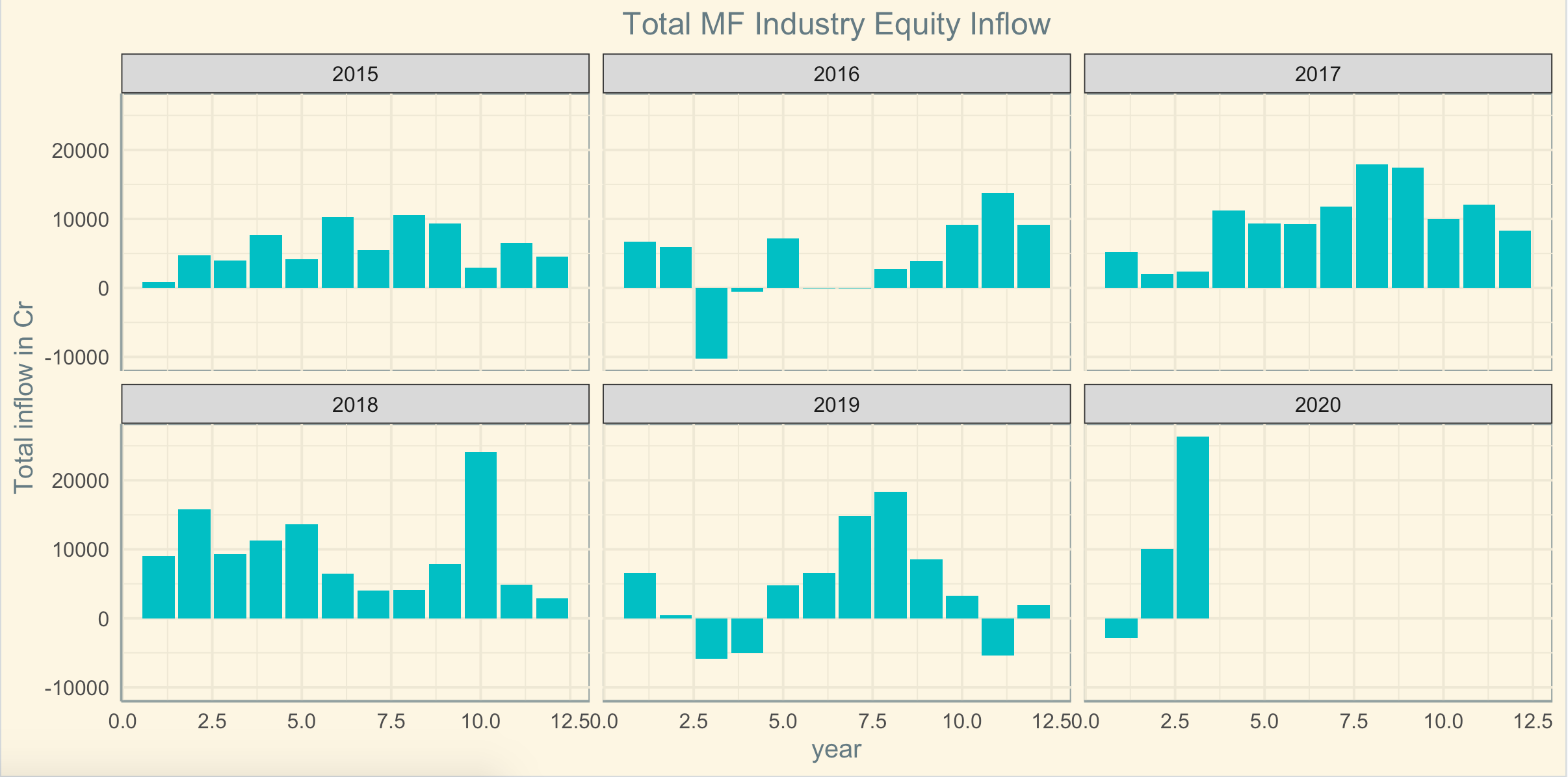

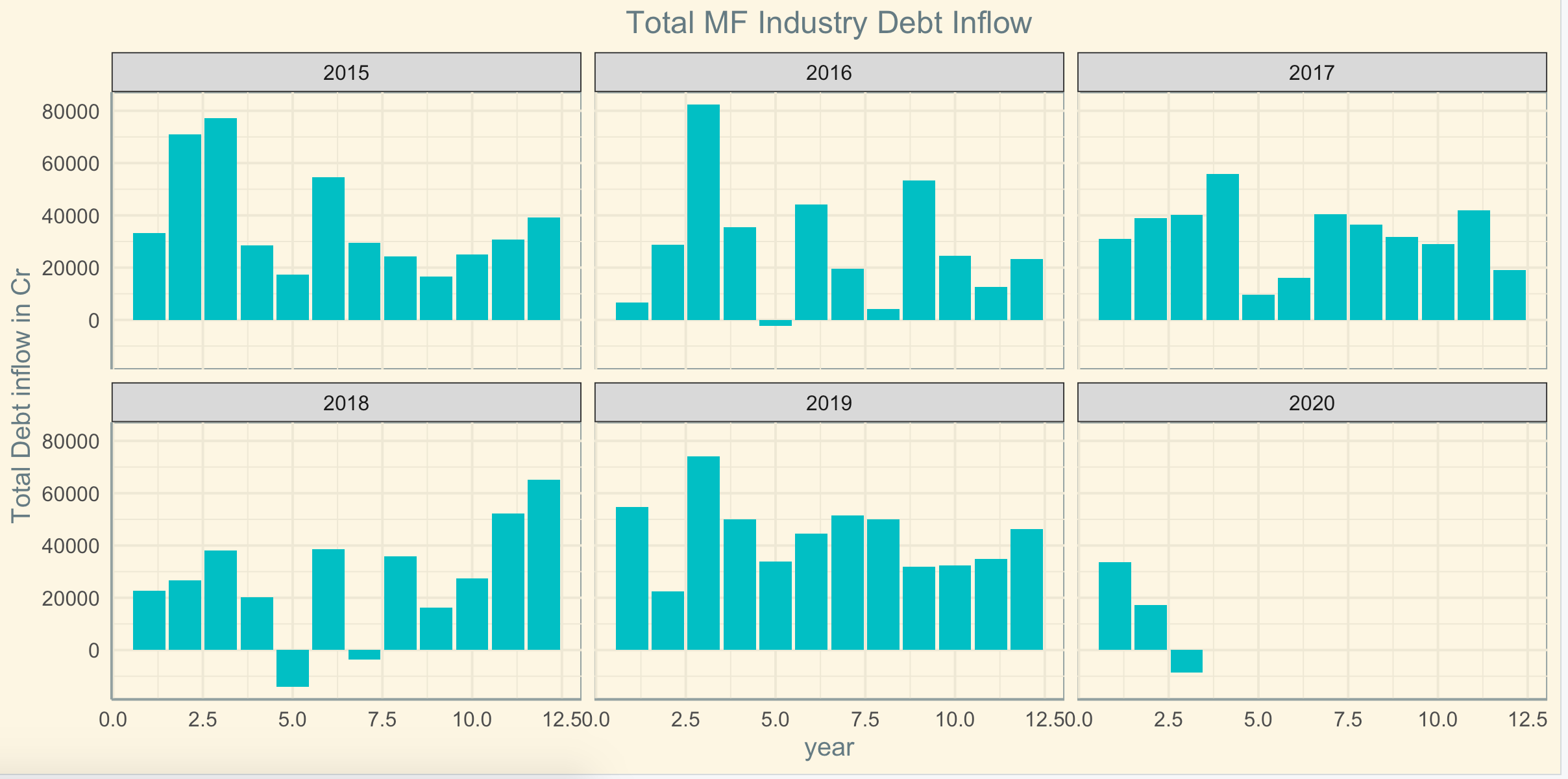

Data suggests something different. There is a spike in Equity inflows…

There is a dip in the debt fund inflows…

Smart people are moving money from debt funds to equity funds since the market is at reasonable valuations is what I believe.

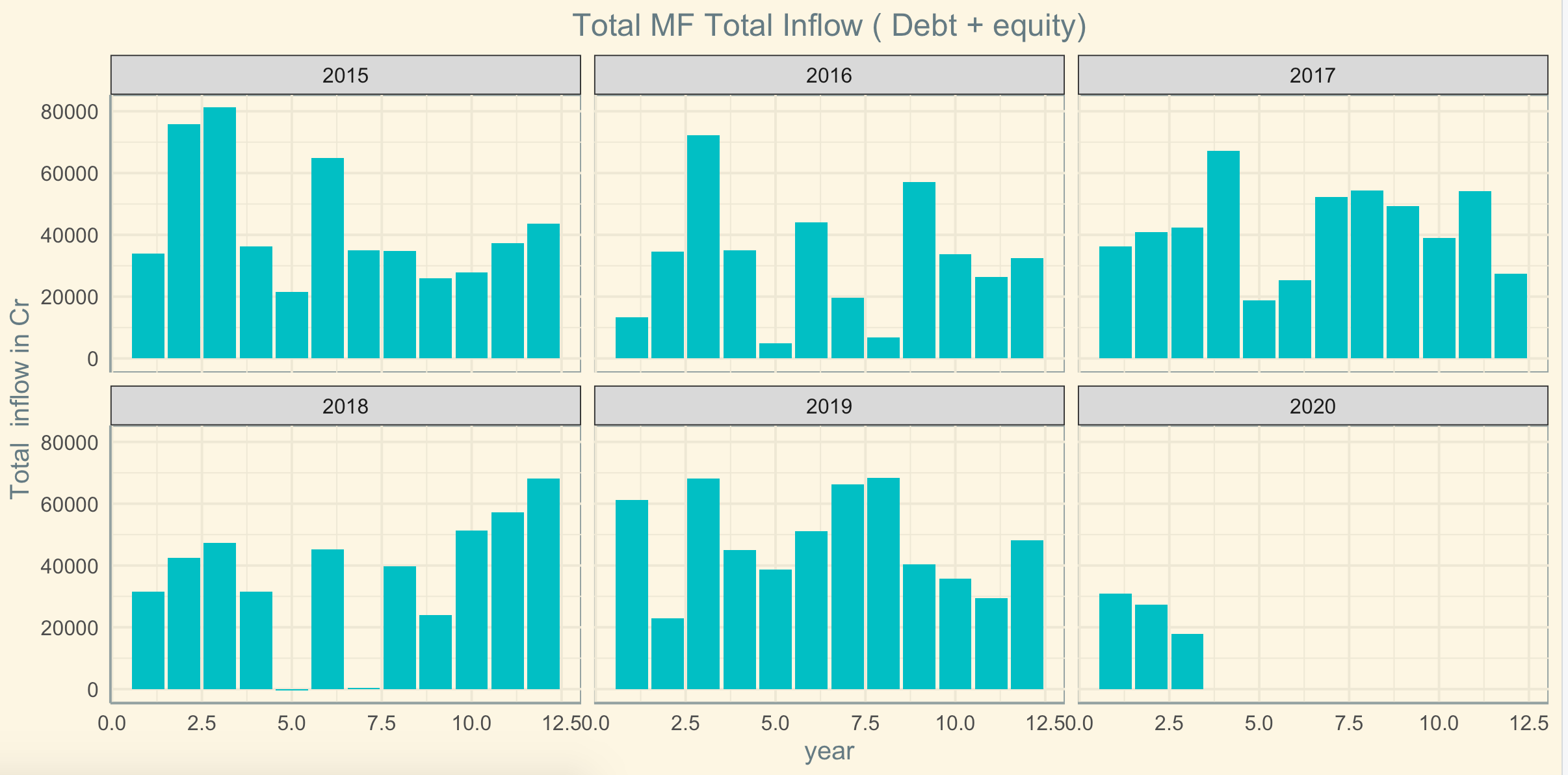

Following is the total info ( Debt + Equity ) statistics. As we can see there were occasions that it was low and then immediately shot up next month.

10 Likes

I have huge respect for your views many times on AMC business. I agree we always do Sector/Sub sector discussions irrespective of market conditions. However, it will be insightful to do that with respect to the medium/long term prospects of those same sectors/sub sectors with recent structural change that economy can see in near/medium term as well as knee jerk price changes to same.

Also, for example, if my target stocks to buy in meltdown is an HUL/3M or a M&M/L&T…same strategy and same timing will never work for me. So unless we discuss the timing and related aspects with context to the target stocks in mind…as a group there is no point in discussing on timing the market. That’s what I think and I maybe wrong.

Thanks

2 Likes

3 Likes

I think there is a lot of analysis being made with the same underlying assumption - markets currently represent a good discount to historically high values - I think this does not consider the possibility that for most companies, the reality on which the historical valuation was based does not hold anymore. One should consider steep cuts to forward earnings and growth and then see whether current valuation multiples seem reasonable or not. There will be very few companies that emerge relatively stable from this, and in all cases anybody buying now will need to be willing to sit put for a couple of years to breakeven on cost.

To add: There is also an application of mean reversion arguments - while valuations may certainly be mean reverting (at least on an index level), company mortality or prospects are certainly not - companies run the risk of ruin i.e. running into a permanent absorbing state of decline from which they never recover. There is nothing mean reverting about growth or earnings. I think its time to focus on whether individual companies run the risk of being permanently derailed from their former trajectories - even a partial derailment (impact / timeframe of impact) can compound into lost time and veer a company off course permanently. This is unfortunately not just a function of a clean balance sheet.

6 Likes

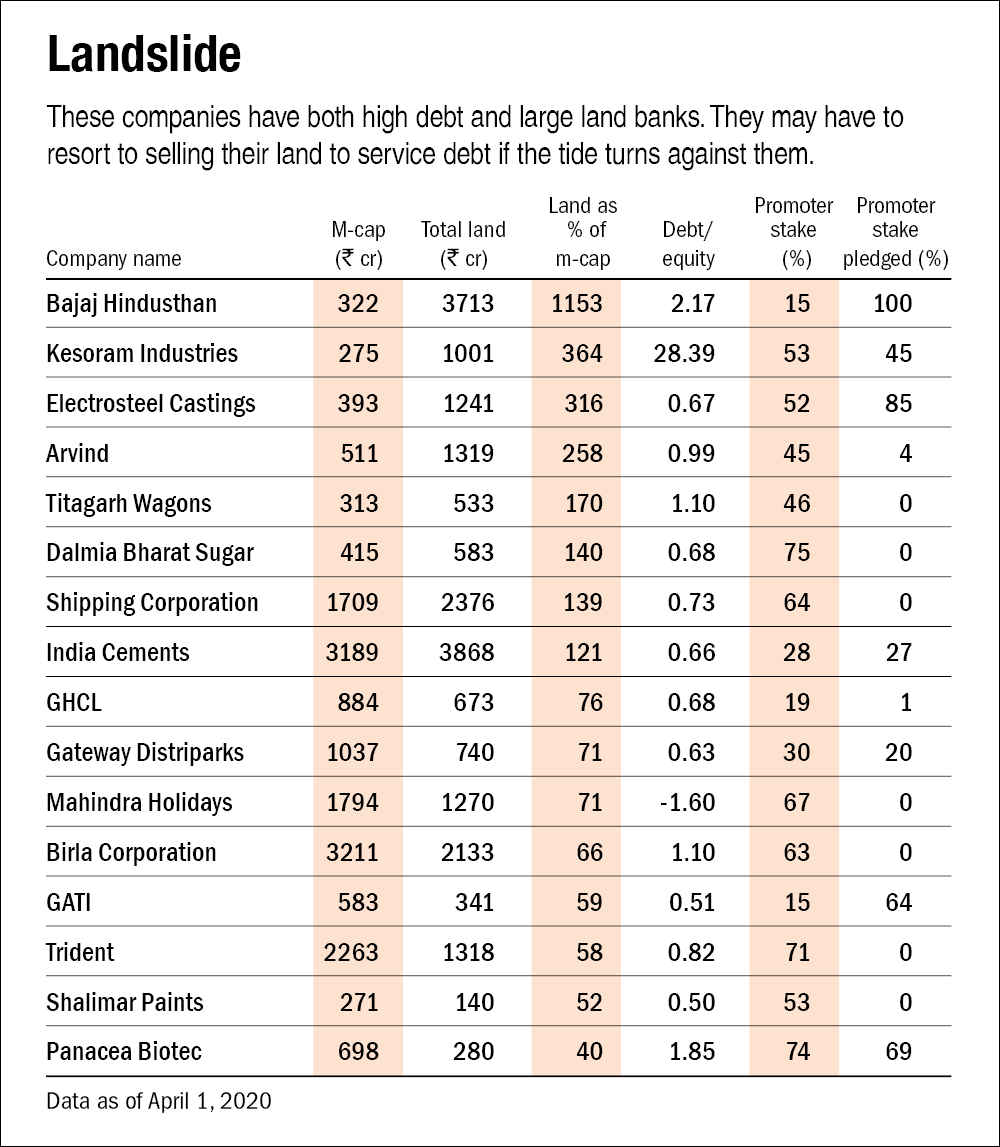

Selected excerpts from above.

We zeroed in on the companies with more than 10 per cent of their total assets invested in land, where the value of land on the books was 25 per cent or more of their market cap. This value of the land on the books is the cost of acquisition and hence is significantly lower than the market value, yet higher than the market cap in many cases.

We also found that many of these companies have high debt and a high promoter pledging. All these factors may force them to sell their land at a distressed price to clear their debt. Investors should be cautious while investing in any of these companies.

7 Likes

A post was merged into an existing topic: Lockdown - Extension - Market Timing Agility

2 posts were merged into an existing topic: Lockdown - Extension - Market Timing Agility

Guys,

Please maintain the sanctity of the main purpose of this thread.

There is a separate thread now for Scuttlebutt/Articles/Ability to Time on [Lockdown] and your opinion pieces (Lockdown - Extension - Market Timing Agility)

Please maintain the discipline to know where to post for lockdown related data points/articles/opinions

Lets get back to sectors/effect on sectors /2nd and 3rd order effects

3 Likes

After a long time posting on VP as I feel after 3 years or so, we have reached a stage where active discussion on economy, business, market, liquidity & valuation can really make us collectively wiser. We are at a “never seen before… never experienced before” type historic juncture where not human greed and fear which drive economic or market boom and bust in all earlier cycles is playing the spoilsport, but a health hazard created the crisis after almost 100+ years when globe is much more interconnected, when people, information and analysis travel must faster than anytime in human history.

I would like to split my thought process in different silos and then try to connect those:

Supply Side issues: When the Covid 19 started in China, almost all took it as a Supply Side issue as China is global supply source of most key raw material and electronic goods in the world. Most expected a 3 - 6 months supply disruption and then things may come to normalcy. Now China is limping back to normalcy BUT the global major “Consumption Centers” of those supplies are unable to absorb those supplies. We can safely assume, right now, 60% to 80% of GDP of most countries are not functioning in Developed World and major Economies. The rest of the functions which are working are Essential Commodities, Banking, Power, Water, Medical Services etc which may constitute 20% to 40% of the economy, roughly. In this scenario, China is forced to cut back labor, factory working temporarily.

Similarly there would be local supply shock at local level and it may vary depending on how complex are the supply chain of different countries, geographies and localities. Like in India, labor dislocation from business centers and ‘productive activity areas’ can create supply shock in almost any labor intensive sector from Harvesting to Transportation. I expect supply shock can be felt much longer after the lock-down is lifted because — a) Presently we are getting supplies from past inventory; b) Govt machinery is working in emergency mode; c) Effect of farm or warehouse or logistic migrant labor shortage would be felt once new set of supplies are expected in the market. This can possibly create an effect in “Farm to Fork” supply chain and distort agri commodity price and price of non perishable effecting fall in income in hands of farmers. Also, if finance, demand or liquidity become a “choke point” then revival of Supply from MSME / SME sector may become longer than desired.

However, the Supply Side issues would be significantly less or zero in sectors which work in “Start & Stop mode” like Cinema Halls, Consumer Durable, Airlines, Travel & Aviation, Online Retail of non-Essentials, Availability of credit etc.

Demand Side issues: It is function of earning power, predictability of cash flows. demographic profile, availability of quality jobs, skill level, wealth effect and “animal spirit” ---- Now these issues have varied effect on different countries. In India, these issues are constraining our growth for many years as we faced quite a few economic shocks which are known to everyone like Demonetization, Lack of Private Capital expenditure, Stretched Fiscal Position (combined and real Fiscal Deficit is almost 8%+), Poor growth in Tax collection and almost zero job growth.

This Lock Down has only exacerbated the issue significantly ---- Now we face situation when many people who are employed in SME / MSME may find problem in retaining their existing job, there may be salary cut or deferment in well paying jobs, poor increase in salary / wage across sectors. Add to that, as discussed above, if farm to fork supply chain get affected then income in hands of farmers can be affected too. This in turn, may affect “demand side” problem in rural economy too. Also, migrant labor remitting money to rural home and augmenting consumption there – This will also get impacted which can further depress rural demand. Demand side problem is hard to solve in short term, in my limited understanding especially in India.

Why I think demand side problem is tougher to solve in short term: Our Banking, NBFC, MFI sector which fueled the demand in Industry, Business and Individual sectors respectively have passed through different phases of crises in past 6 - 7 years. In spite of high liquidity and low borrowing cost, banks would be cagey to extend liquidity to disbursing intermediaries like NBFC or MFI in uncertain situation especially when they just passed through the worst NPA crises from which it is just about to recover. Unfortunately this Covid 19 crises have come at a very critical moment for Indian economy as we were about to come out of the decade long Banking NPA crises and presently staring at another NPA crises due to this massive lock-down and slowdown. Also, the bond market in India is not that well developed to supply entire credit demand at right cost.

In this situation, Fiscal measures like direct cash transfer and very liberal credit is essential for a major section to survive (at least 40% - 50% of the population) … It would be surely done by Govt irrespective of tight fiscal but it would only help “Sustenance” but not a “Stimulus” to consume. To me. this distinction is critical and important when we model rural demand related investment thesis in FMCG sector.

The rest 30% to 40% of population would be cagey to spend because of obvious consequences of lack of clear visibility of cash flow / job security / salary growth especially in areas of large value discretionary items (Foreign Travel to High Value Consumer Durable depending on sub segment of the middle class).

Now this demand reduction leading to supply reduction is a negative feedback loop — Large Govt spending can break the vicious cycle. I am unsure how much ability Indian govt has to spend and inflate away the crises given fiscal profligacy can reduce our global credit rating to non-investment category and can create a different set of problem in attracting global fund especially in our bond market.

Businesses: It is much easier to identify.

Business has 5 sources of expense – Vendors (for RM, Utilities, Rental etc), Salary, Interest, Taxes & Dividends. Out of these dividends are last and discretionary. Taxes and Vendors are function of sales and profit, Salary and Interest are almost fixed in nature. If we take only debt free, cash rich companies then they may be better placed to survive longer duration than others unless demand of their end product is drastically less needed by market. But here also I can visualize a scenario where this assumption may not work ---- For example, take NTPC — which produce power but if industrial demand (which pays) is low for long time then consumer & agri demand (which is subsidized) would force Discoms to delay payment or resort to load shedding to save money. So, without demand from remunerative customers, very few businesses except FMCG & Select Private Banks can remain unaffected in their business economics (nothing to do with valuation).

Some businesses are avoidable for me in present context for short to medium term — Travel, Tourism, Airline, High Value Capital Goods, High Value Consumer Durable, Theme Parks, Construction, Commodities like Metal and Minerals, Real Estate, Corporate Lenders, NBFC etc. Please note, it doesn’t take into account valuation (Imagine valuation has no meaning for this part of discussion)

Market: Now unprecedented fall has created a situation where everything may be looking attractive if one has cash. And conversely, may look very unjust, wrong, disgusting to anyone who is already invested and wounded. Present market give no consideration to past history of the business, terminal value of the business, incremental improvements in business or quality of earnings. Panic & fear has its own justification and evolutionary logic and I personally don’t feel anything negative about being panicked (mistaking rope as snake 10 times may be socially shameful and humiliating but mistaking snake as rope just once is recipe for death and destruction) ---- Most global investors are selling today simply out of fiduciary responsibility of risk mitigation which if one likes can call “fear” but I am more charitable to their reasoning. Since 'No Body Knows Anything" about when and how fast better days would come, taking some money out by investors can’t really be called “fear”. It may be noted that FII sell this time is much lower (at least till now in % of their total investment) than 2008 and even lower than 2012 taper tantrums. Investors were in risk mitigation mode so either raising or preserving cash.

Liquidity: Presently the biggest problem is faced by companies globally is liquidity. On global level there is huge shortage of US$ as global trade is stalled, which is predominantly denominated in US$ and hence velocity of US$ reduced substantially. The massive fiscal stimulus announced by US of US$ 2 trillion may reduce the crisis gradually. But effect of this would be felt by emerging market currencies and depreciation of INR may be highly likely. In India, the liquidity problem is high for similar reasons of trade stalling, certain fixed cost continuing and stringent regulations & credit concerns making funding institutions very selective. RBI actions are more than expected but how much effect it would have is something solely depend on risk appetite of banking channels.

In stock market also the present fall is primarily due to liquidity issues faced by ETF and global funds due to redemption pressures and flight to safety of global capital. Whether this issue would continue, exacerbate or slow down is a matter of pure conjecture at present moment as we have no clarity of when the virus spread and related fear would subside. At present it is very tough to guess.

Valuation: I feel, even if two years of earning get impacted, the terminal values of robust businesses are not substantially impacted. But since the present selling is not due to market excess, the valuation based investment has no meaning unless one has very long term view as price in the interim may fall to any absurd level if concerted sell and short sell continue. It can have definite reversal only when virus related concerns are abated by concrete data or some cure or vaccine is discovered, all of these are not going to happen in very short term as we know today.

Positives: For India there are few positives. Firstly we are younger country and possibly due to our better immunity (left handed compliment to our poor social hygiene) we may withstand it better than many countries where median age is much higher and immunity is compromised due to high social hygiene standards. Secondly, 60% of our population is dependent directly or indirectly to agriculture, essential services and govt jobs, which would be relatively immune to the vagaries of economic cycle to some extent (not fully) & high resilience of Indian common mass due to its adaptation to living with uncertain environment like flood, drought, cyclone, vagaries of monsoon, localized epidemic and some such negatives throughout history. Thirdly, we have huge food grain reserve which can withstand extreme existential issues without much stress even if the problem become acute and lingers for almost an year.

Other points: Since unlike war or calamity this particular emergency like situation doesn’t need rebuilding of infrastructure but needs huge investment in public health, creation of more medical, nursing and healthcare facilities apart from giving income support to poor and vulnerable, we may also expect major change in focus of Govt expenditure and private sector CSR initiatives. Also, the lock down may change certain priorities of human behavior and consumption in medium term … I am yet to fully build a scenario about those changes as yet. One thing can be said though — Fear of high inflation may be misplaced in low demand environment even if Govt resorts to fiscal expansion.

Will discuss in a separate note about how where and when I feel stock investment may be initiated slowly.

104 Likes

Impacts of this epidemic are massive and still we are just seeing initial views & first order effects, Just wanted to share my understanding:

Trump was recently forced to change tone from China-Virus to Thank you China, basically China control supply of all basic products, most likely china refused to supply Masks & PPE to US in order to force them tone down the narrative against china, most countries are in similar situation and dependent on China.

Supply Chains:

Basically in search for efficiency, resilience of countries/economies is compromised, so apparently localisation will be the theme going forward, as most countries will realise such vulnerabilities and will mandate local manufacturing as part of national security.

Since depression is deflationary in nature as massive jobs are lost --> lower total income–> lower total spending --> lower demand --> prices cuts

a perfect fit for such situation would be “local manufacturing” as it will help creating high paying jobs, its inflationary in nature and will help deleveraging, allow countries grow out of this likely depression, this could be permanent shift and would go on for years to come.

Portfolio Adjustment:

Avoid List: Exports, Travel, real estate, High value consumer discretionary, High debt businesses.

Buy List: India focused business, with low debt, for now essential products & services only:

ITC, IEX, Thyrocare, AIRTEL, CESC, Petronet LNG, Pharma basket coupled with some cheap bets like: CPSE ETF, Idea, KRBL

will add Index funds in case of another 20-30% cut from here in index.

rest planing to add some capital goods stocks as well, as India might get some share of global supply chain reshuffle, most likely lower end non critical products or pollution causing industries.

Timing part: I think panic in financial markets wont be lasting as long as historic panics/downturns lasting upto 1-2 years, as Social Media is amplifier of everything, thats why corrections are so sharp & sudden and quick, so i assume max damage will be discounted in next 2-3 months itself along with peaking of infection globally, would bet & prepare to deploy everything in next 2-3 months itself.

COVID19 India specific: i am hopeful India wont see social spread on large scale simply due to weather conditions, as in most cold country virus is most likely airborne, but in hot countries its not, i am saying this from my personal experience as i got infected with corona(Fully recovered now) while i was in turkey in first week of march, although i took all precautions, only time i use to take off mask was while eating, and most likely i got infected simply by breathing in infected air, but when i came back to Africa where temp is similar to India in 30-40 degree Celsius, before i knew i was infected i was with my friends and no one got it from me, also here in Africa, i see many cases where infected person went onto giving lecture in universities and then visited most of the hospital in the city but still there is no public spread, similar cases are in India, only specific sporadic concentrated cases are there, but no public spread on streets, although i understand its not proven scientifically simply because its not studied yet, as most countries are struggling to contain it.

This is Just my opinion, obviously can be dead wrong, rest individuals should assess according to their investment horizon, as economy will take time to recover, and depression may last minimum 2 years to max 4-5 years, any money needed before 5-6 years i guess should be kept safe in FD, i am working with 10 years investment assumption.

35 Likes

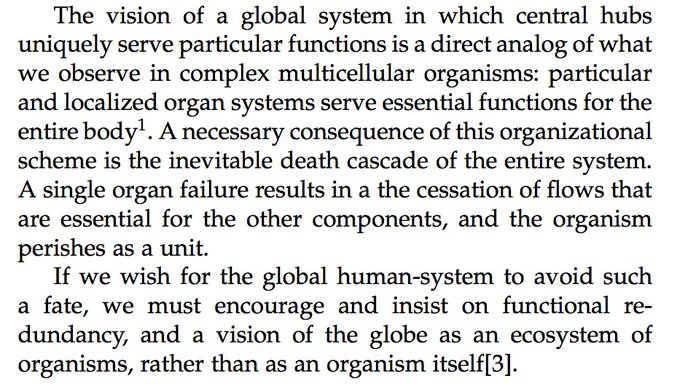

I am a firm believer of anti-fragility, redundancy over efficiency/optimization, localism over globalization as captured below.

Source: http://jwnorman.com/wp-content/uploads/2020/03/global_decentralization_security_JNorman.pdf

Just In Time (JIT) supply chains which were optimized for efficiency will need to be re-organized to incorporate redundancies (Hence, China + 2 in the short term. Local supply chains in the long run)

If we consider Hospital from the above perspective it is possible that we may see policy change which mandates all hospitals to reserve and maintain dedicated isolation units to handle pandemics or secondary/tertiary waves of COVID itself (as is being predicted)

Now coming to the 2nd and higher order effects of COVID, I am sharing the below links which I came across the internet

@Donald: Below is a neat live document where folks are collaborating and capturing the 2nd order effects.

Another Google docs capturing the 2nd order effects:

COVID-19-s-Ripple-Effect-Mapping-Out-The-Societal-Economic-Consequences

Other links:

https://www.etinosaa.com/2020/03/second-order-effects-covid-19.html

https://kscarrott.com/covid-19-second-order-effects/

https://pcon.blog/2020/03/14/covid-19-the-infectious-tech-revolution/

Must Read: Coronavirus Consequences - Unintended Consequences

5 Part blog series

I believe most would have come across this paper from Taleb and his NECSI colleagues.

Systemic Risk of Pandemic via Novel Pathogens – Coronavirus: A Note — New England Complex Systems Institute

Last but not the least came across the below site which tracks the consumer behaviour from multiple sources.

Apologies in case it is an information overload.

20 Likes

13 posts were split to a new topic: Long Cycles 2.0: Learnings from Market Cycles-Secular Crashes- and Actionables?

4 posts were split to a new topic: Elliot Wave Difficulty/Identifying Waves

KPMG covid.pdf (1.9 MB)

Detailed sector wise impact analysis by KMPG.

2 Likes

View Update:

Facts: The fall from Nifty 12430 to a low of 7511, happened due to the news of the virus. The fall was abruptly stopped (paused) and bottom was made on 24th March when US decalred the $2 Trillion package.

Current Asessment

On, 24th March, the registered cases for infection Internationally were around 4L, and 12 days later, they are now 12L.

I am noting for the past two days that close to 1L cases are being added every day! The number of everyday deaths is in thousands. This is alarming.

- The virus is far from receding, in fact now the situation is getting out of hand. If the fall is due to the virus, then the cause is more intense now, hence so should be the reaction.

This theory gets more credibility when one sees that the fall was of 4919 points, whereas the bounce was 1528 points, a 31% retracement, which is weak.

Ordinarily, $2 Trillion package is sizable, but given the severity of the situation, if the package was a meaningful remedy then the retracement would’ve been 50% or 61.80% at least. Then there would be hope that a fresh bottom won’t be made.

Furthermore, the market on 24th March may not have factored in such a rate of increase in infection, and the second order effects like mass unemployment across the world (notable the US), widespread reaction against the Chinese and several conspiracy theories, which may result in international backlash against them.

Conclusion:

There is no room for bulls, yet. I would want to see the negativity, at least, partially fade into a neutral sentiment, before expecting bulls to start making value purchases. In fact, this week good stocks that come out with positive results, like HDFC Bank, will be sold into. Even the top-tier, Asian, Pidilite, FMCGs have started cracking.

8 Likes