Competitive Edge

Camphor being an commodity and like any other commodity, Pricing will be key factor.

Mangalam has an Competitive edge as they entered into Resin Segment in which they have capacity of approx 2850 MT/month which is 68% of total capacity. Approximately in value terms it should be 40% from Resins and rest from Turpentine (i.e.Camphor) . Diversification into new products which are co related to its existing product lines will add value to Mangalam in terms of profitability and scalability.

Kanchi expansion plan is purely into Turpentine Products i.e Camphor ,Camphene,Sodium, etc. Camphene is an intermediate product of Camphor and infact many companies use Camphene as raw material for manufacturing Camphor.

Pharma Industry

Synethic Grade Camphor acts as Active Pharma integredient (API) for Topical Pain Relief pharma segment. Usage of Camphor in Tiger Balm https://www.verywellhealth.com/what-is-tiger-balm-2552293 .

Topical Pain Relief Segment https://www.alliedmarketresearch.com/topical-pain-relief-market

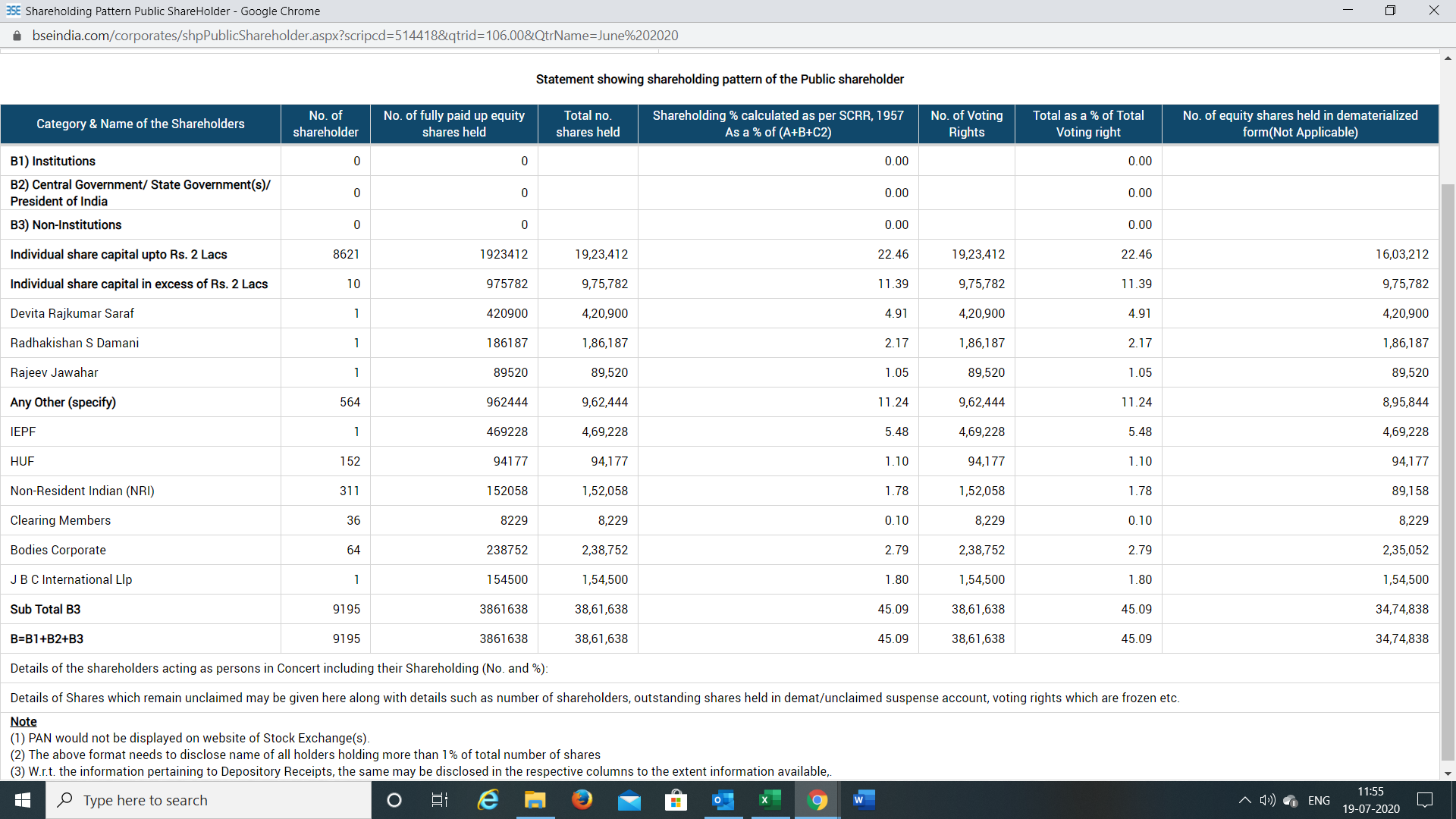

Mangalam has come with Investor Presentation for March 2020 first time ever which clearly states that they has Turpentine client (Camphor) such as Amrutanjan, Dabur,Emami and Himalaya.

Product Portfolio of Mangalam Clients:

Emami - Zandu Balm,Menthol Oil Balm and many more where karpoor (Camphor) is used as raw material (API) http://www.emamiltd.in/brands/75/170/mentho-plus-balm.php

Amrutanjan - Camphor has been used by Amrutanjan in large quanity as they are speacialied in Pain and Congestion Mangament since 1893 https://www.amrutanjan.com/headache-aromatic-balm-massage.html

Himalaya - Have a very good presence in Wellness Industry https://himalayawellness.in/products/pain-balmstrong#:~:text=How%20Himalaya%20Pain%20Balm%20Works,reliever%20that%20remedies%20pain%20naturally.

Dabur - FMCG Company which has lots of products in his basket where mangalam is serving.

Having such Giant Players in your Pharma bucket is surely an indication that Mangalam has already established his footprint in Synethetic Camphor Market .

Mangalam has Retail Clients – D Mart, Reliance Retail, Spencers and Amazon and Synthetic resin Operations client such as – Pidilite, Henkel, Bostik and H.B. Fuller.

Retail presence, Resin expansion, Big Investor Presence and leader in Camphor industry will surely have an competitive edge to Managalam as compared to other players.

I firmly believe that any stock to become compounder , Stories with Numbers are equally important.

Eagerly watching that Stories/Thesis are converting into Numbers…