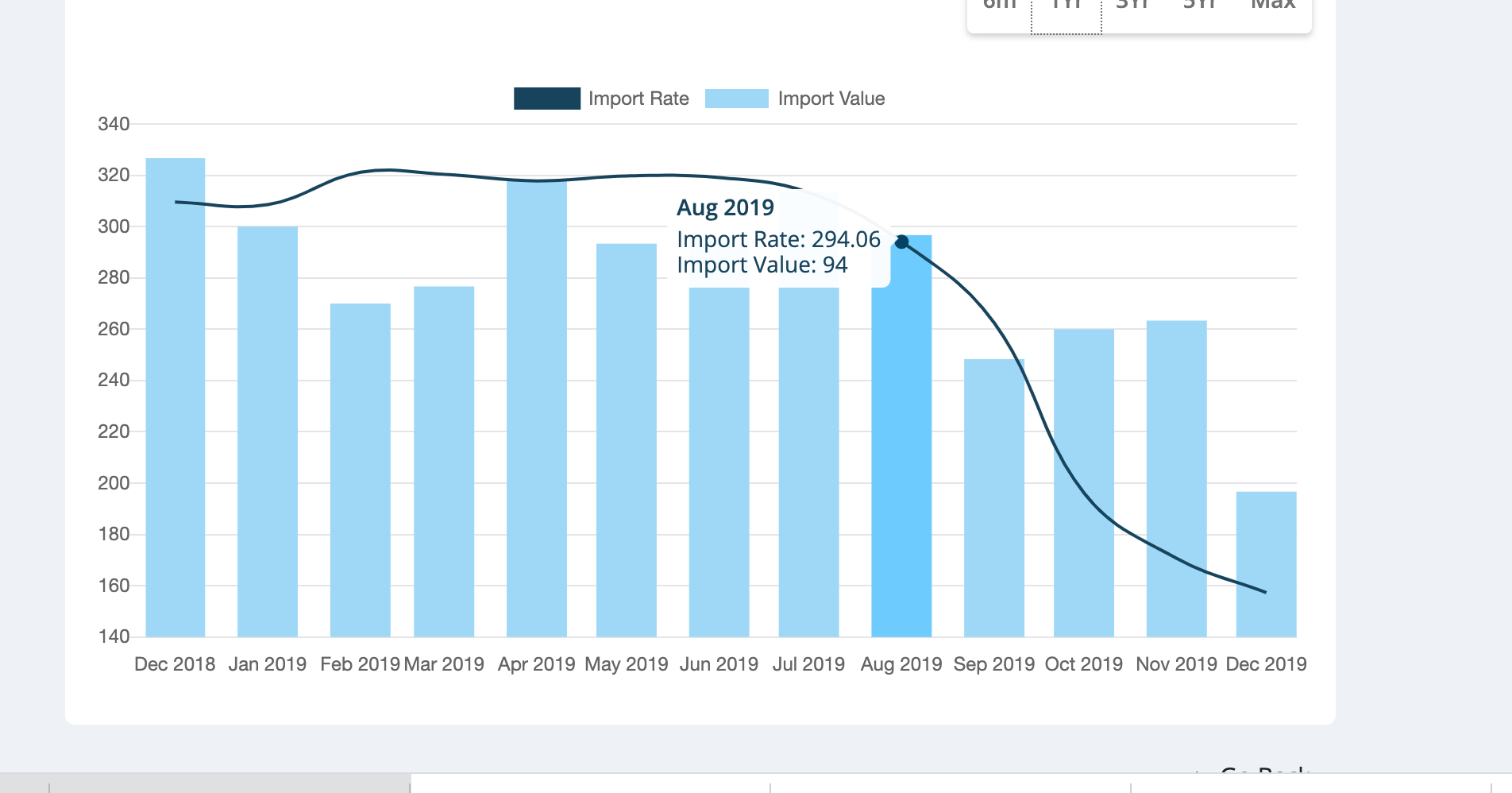

Gum Turpentine Oil prices declined from INR 300 per kg in Aug 2019 to INR 150 per kg in Dec 2019. Based on Indiamart quotes, prices have declined even further in the current quarter to INR 135 per kg. I believe this is the primary driver of lower camphor realizations - as a commodity manufacturer, Mangalam has been forced to pass on the benefit from reduction in input prices to its customers. On the positive side, Mangalam has been able to maintain gross margins at 40% even in Q3.

This drop in prices has been precipitated by:

- Gum tapping season which peaks in OND quarter

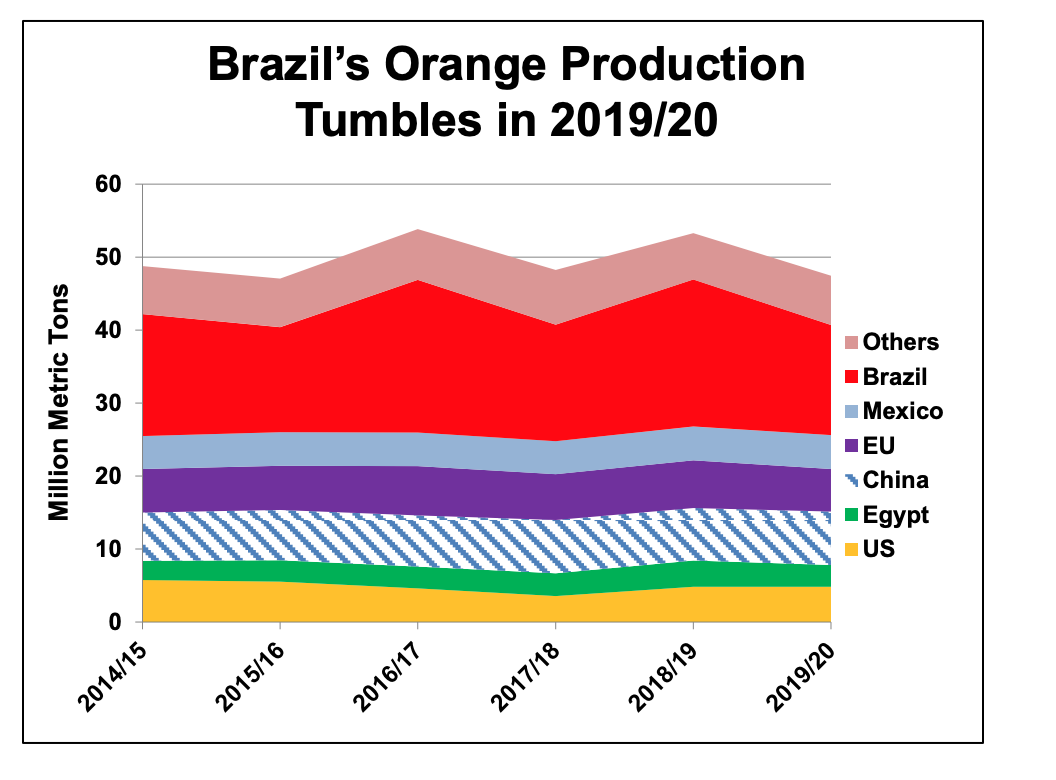

- After 2 terrible years, bumper orange crop in US and Brazil in CY2019, leading to plentiful availability of d-limonene, which was being substituted by dipentene in CY2017 and CY2018 - a GTO derivative

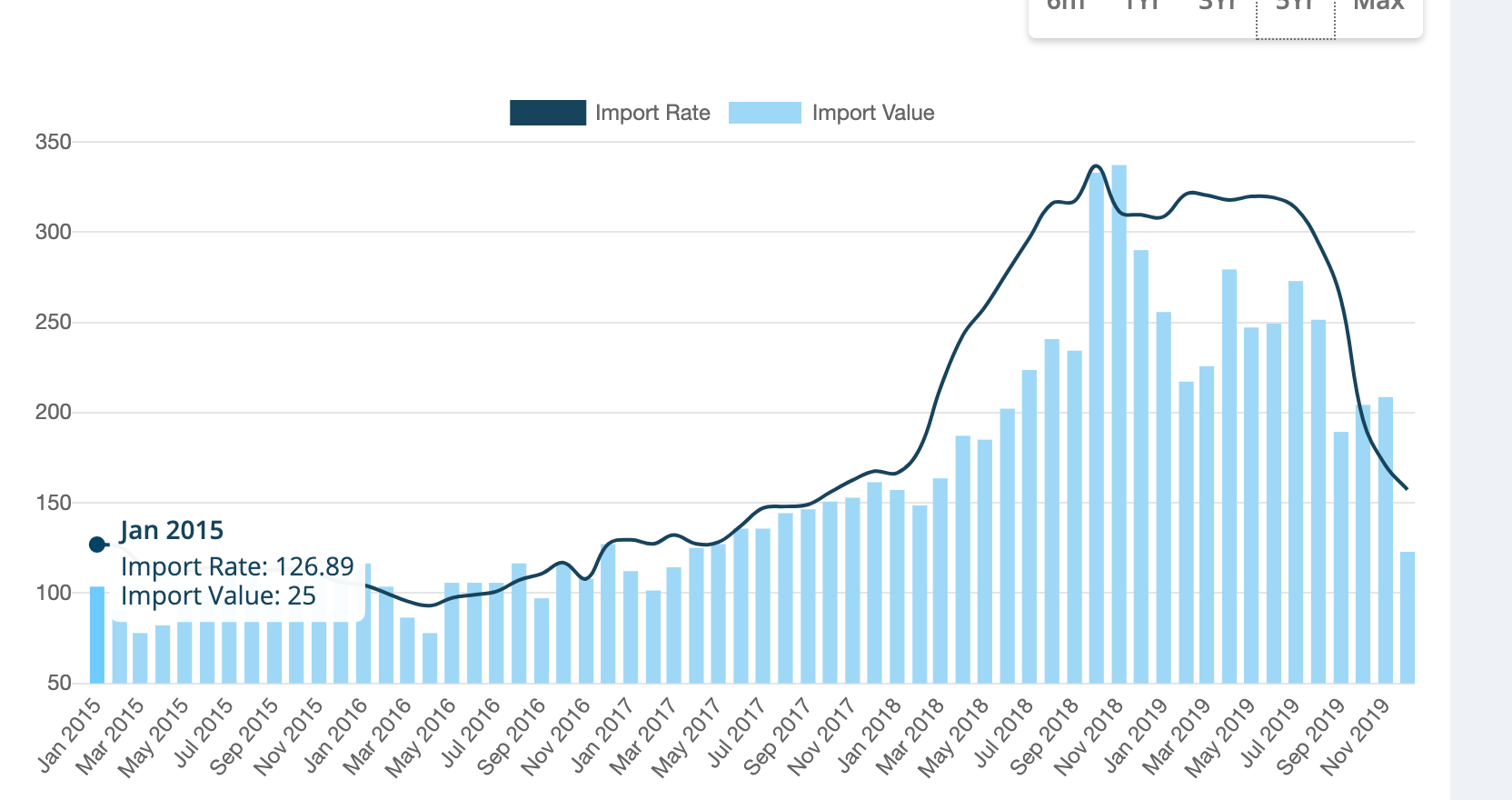

In the past, GTO prices have gone as low at 94 Rs/kg in May 2016. A decline to that level would mean a further 40% fall in realizations. But is that likely? I think not.

Since 2017, the sharp hike in GTO prices has compensated pine tree tappers for the low realisations of Gum Rosin. However, the fall in prices of GTO and Gum rosin make gum tapping and processing unviable at the moment. Refer the conference call transcript of Kraton Corp below:

"That turpentine fraction has obviously come off significantly in value. More in line with quite frankly the historical relationship between gum rosins and gum turpentine. And, yeah, we would presume that all else being equal, that that ought to bring some disciplined decision making and behavior back to that marketplace.

In fact, we try to track that on a – if you will a real-time basis, and our own internal analysis suggests that there’s just not a lot of incentive right now to be tapping trees. And one thing I want to mention too, I think it was from the prior question, but is probably important to this discussion. The question was asked about our business. But you need to understand that the majority of turpentine, whether gum or CST-derived, really ends up in the aroma space for fragrances and flavors. And that’s really important, because obviously that’s a very high-end application."

(Kraton Corp (KRA) Q3 2019 Earnings Call Transcript | The Motley Fool)

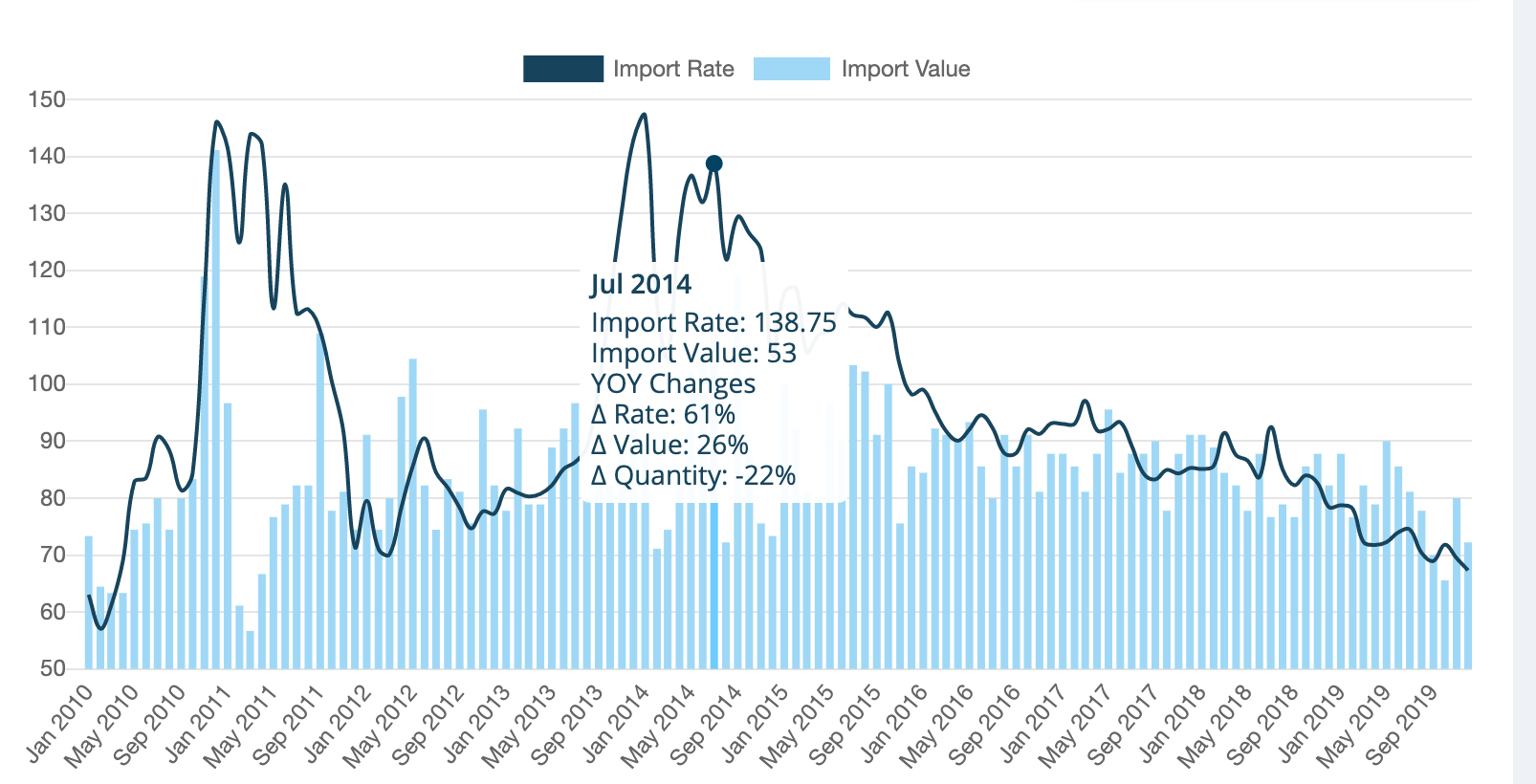

If prices of both GTO and GR stay at the current depressed levels, pine tapping will not be sustainable in CY2020. As can be seen below, GR demand and hence prices are in a secular decline since 2013 and unless crude spikes above 80 USD per barrel, it is unlikely to revive

Therefore, either GTO realizations will rise before next pine tapping season or gum harvesters will decrease their output.

Moreover, after the bumper crop in CY2019, Brazil’s orange crop is expected to decline by 25% in CY2020, while US is expected to increase by just 1%.

This will once again trigger limonene shortage and consequently demand for dipentene - thereby driving up GTO prices.

The above trends combined with DRT revenue + new capacity for pharma grade camphor and terpene derivatives + rapid scale up of retail foray + ability to maintain 40% gross margins at any price of GTO makes me feel that at the current price, the risk/reward ratio is favorable.

Disc: Invested