yes…shd there be a change?

No, I just thought that a while after you shared your portfolio, the stock grew quite a lot…

Is this good news for GPIL?

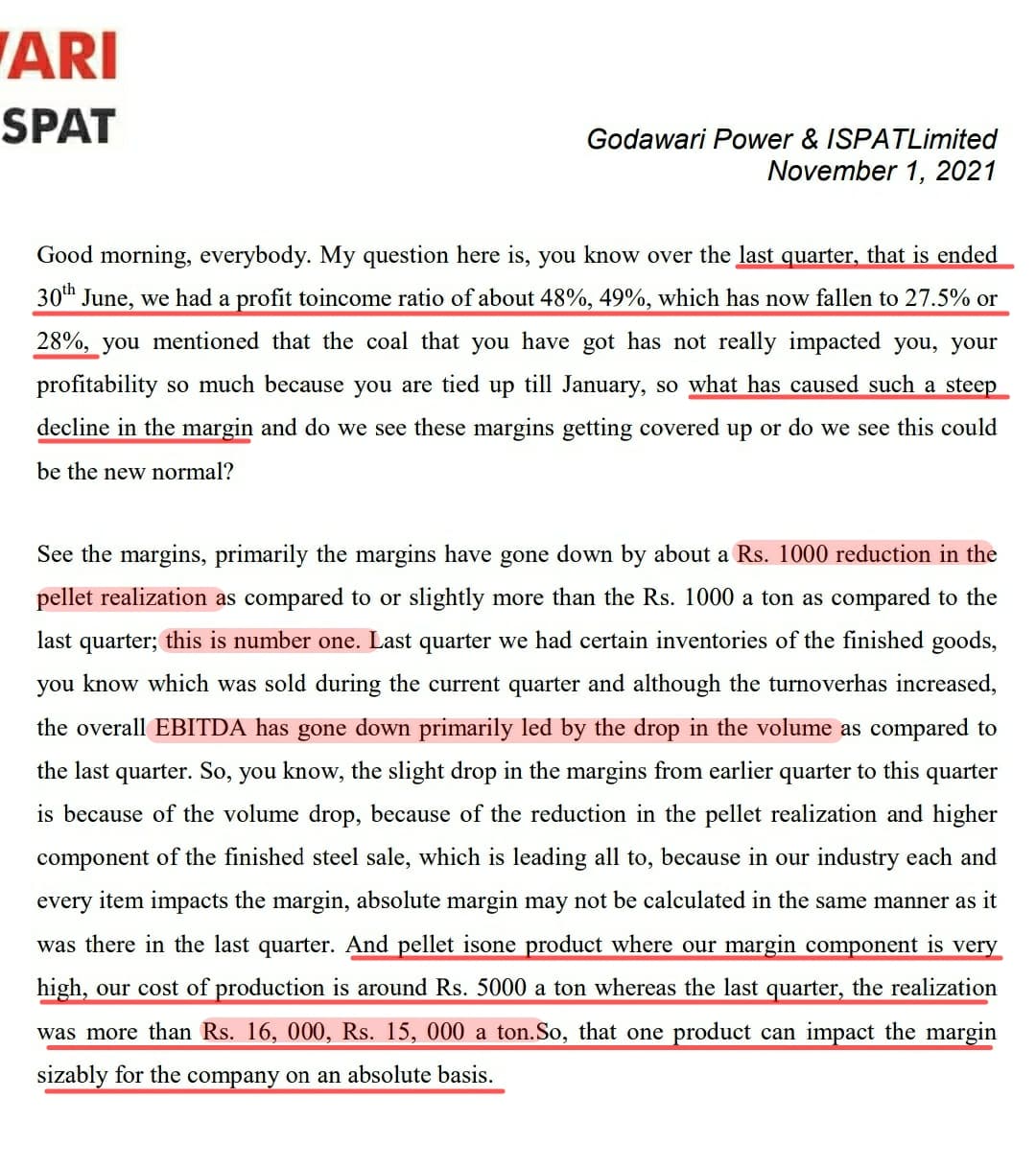

Currently GPIL derives significant revenue from pellets. Margins from pellet was very high for GPIL on Q1. Rs 1000 reduction in pellet realization and lower volumes has caused fall in margins on Q2 from 48% to 28%.

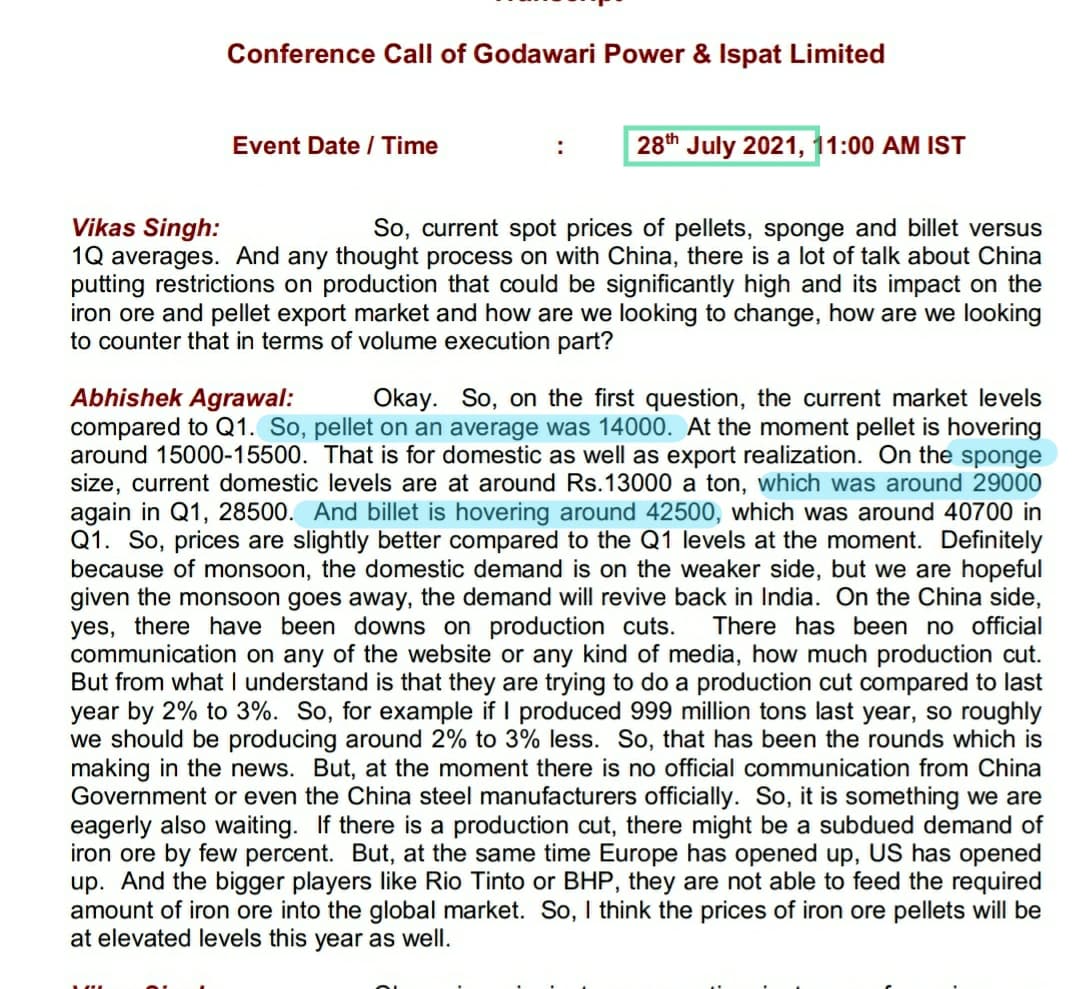

Q1 average pellet realization - 14,000

Q2 average pellet realization - 13,000

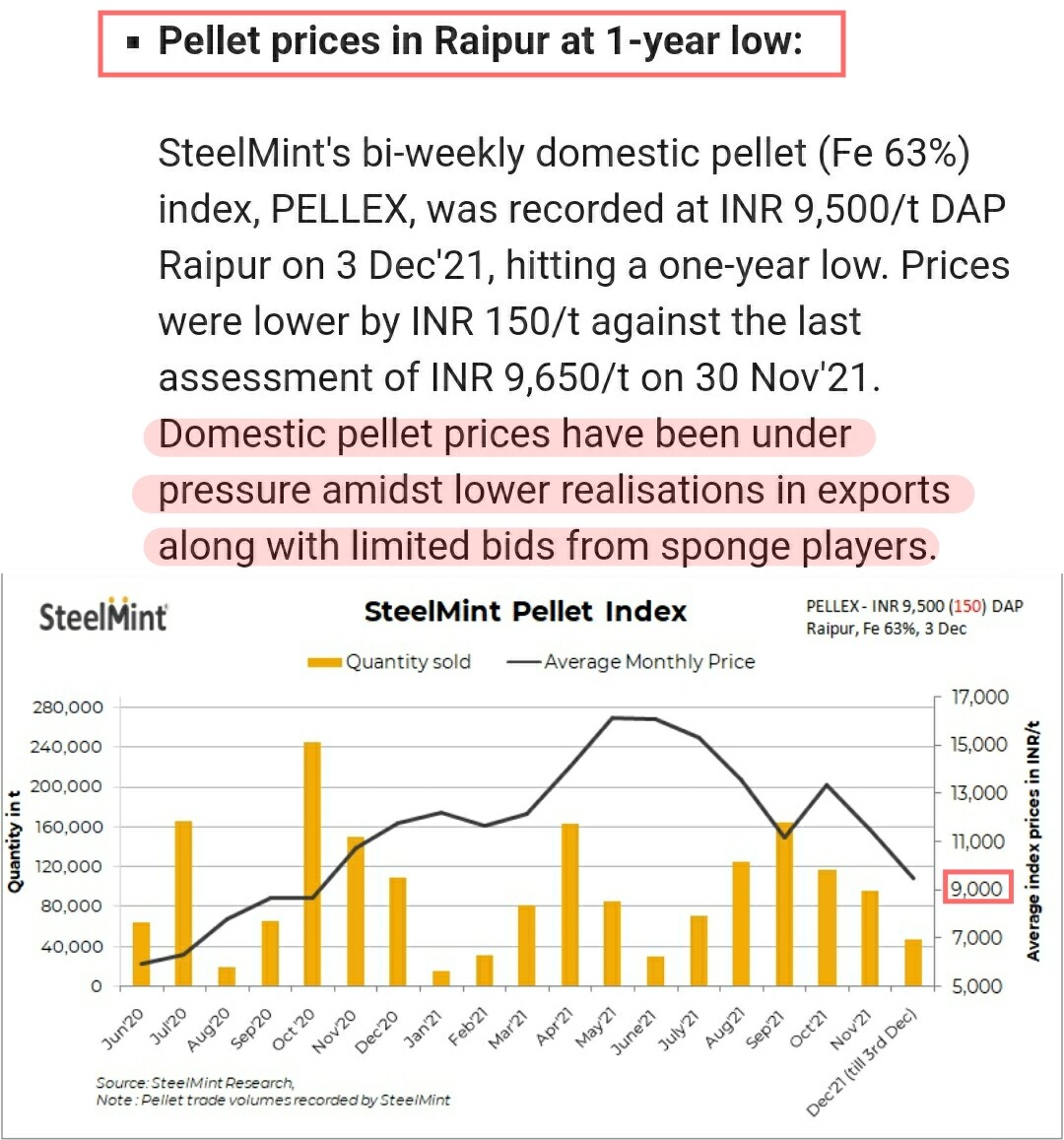

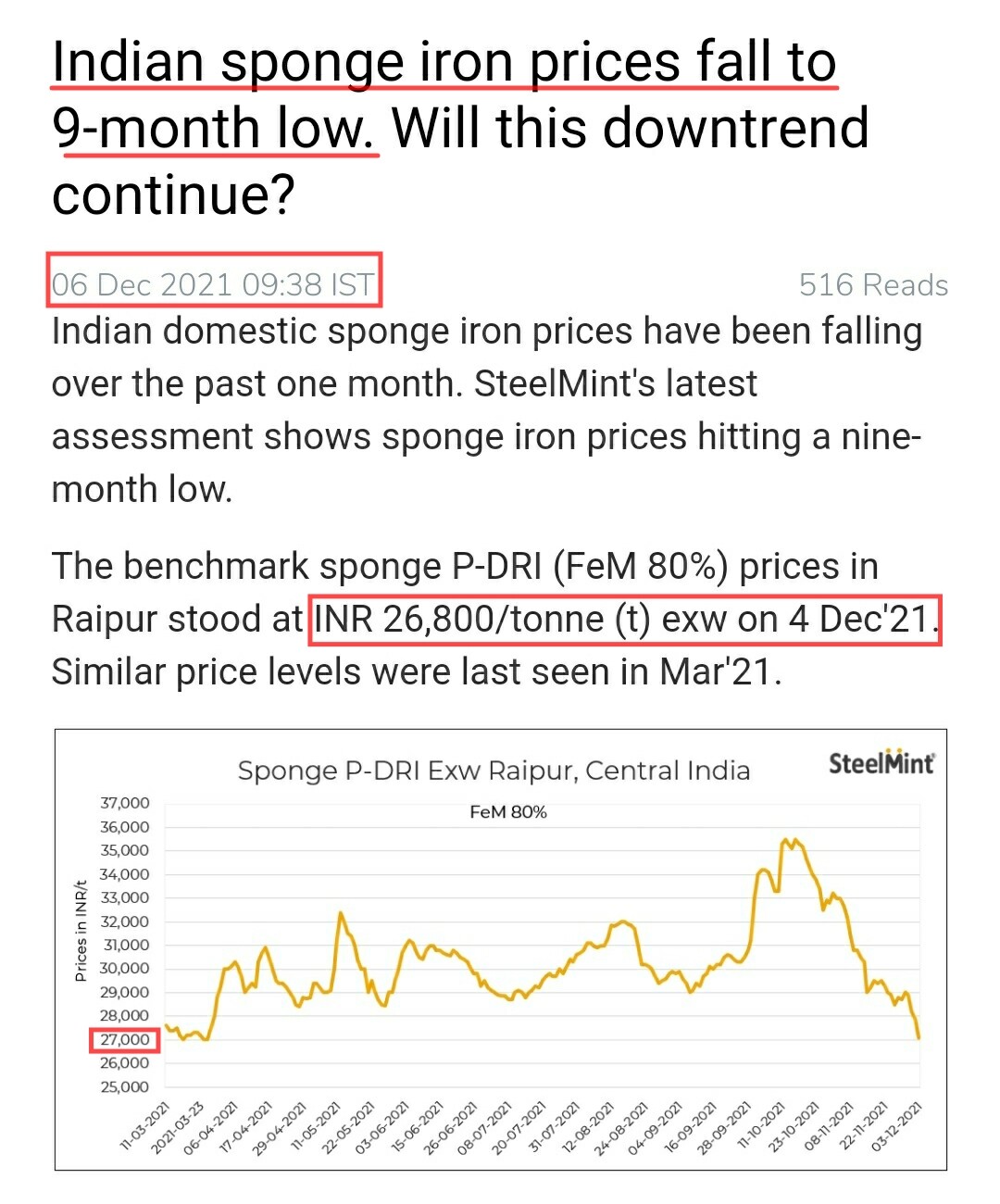

Pellet price on Dec3 - 9500. (Continuously falling and at one year low)

Pellet price is under pressure because of decreasing iron ore price and limited bids from sponge players. (Sponge iron price is also at 9 month low)

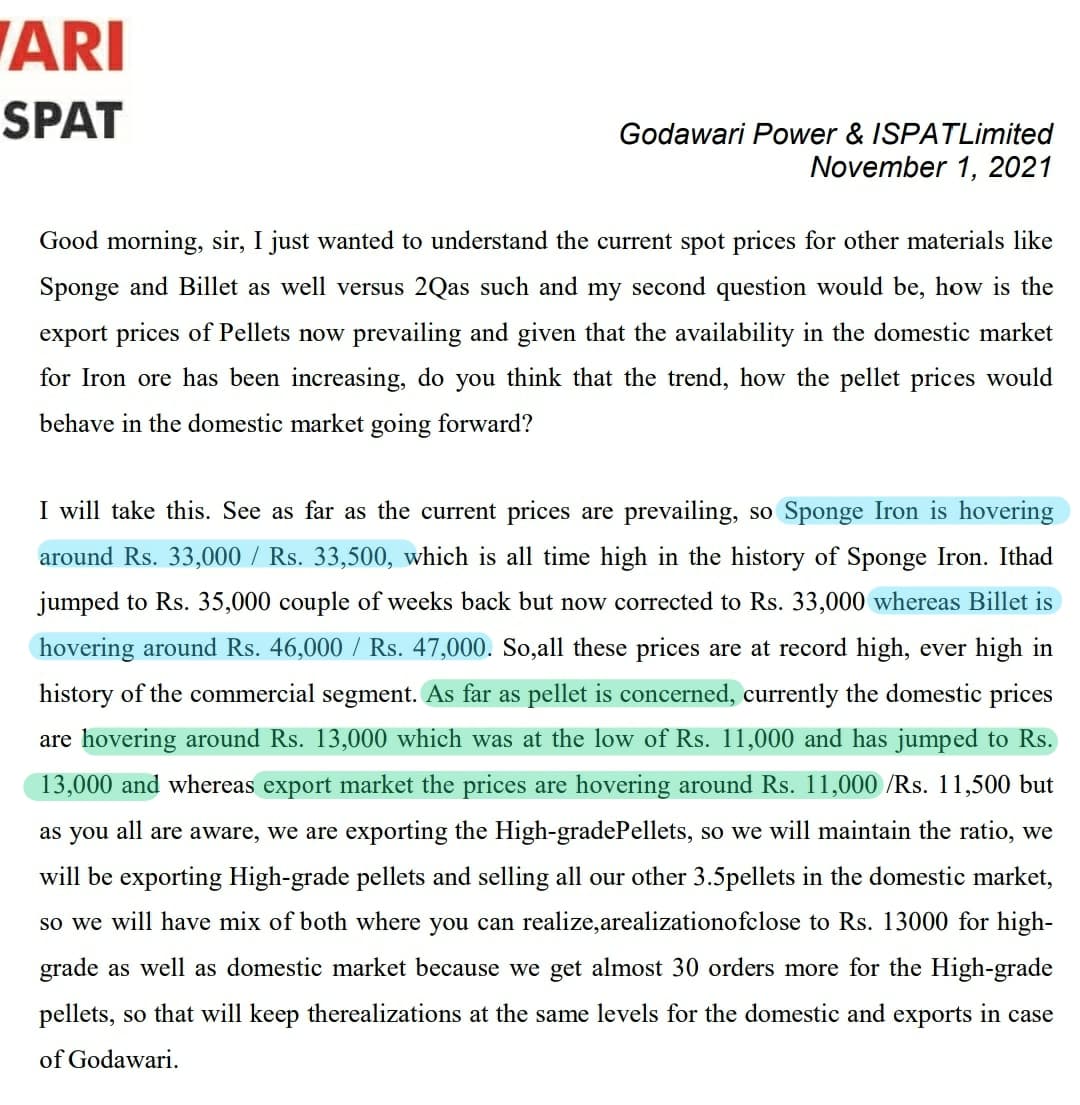

Sponge Iron price on Dec 3 - 26,800

Avg Sponge price on Q2 - 33,500

Avg Sponge price on Q1 - 29,000

I think the fall in realization of pellet will make a negative impact (as it contributes to the bulk of the margins). We have seen that 1000 Rs fall in realization reducing margins from 48%(Q1) to 28%(Q2).

By the end of the december we might get an idea about the average pellet price for this quarter.

5 Likes

What was the EBITDA in Q3, Sep-Dec 2020, when the average pellet price was 9700 only, and then in Q4 when the avg pellet price was 11700 only?

350 CR and 470 cr respectively I guess.

Last quarter was low also because of high inventory of finished goods at high price from the quarter before that + low volumes.

Pellet cost is 5000 per tonne. no? and selling price is 10k per tonne

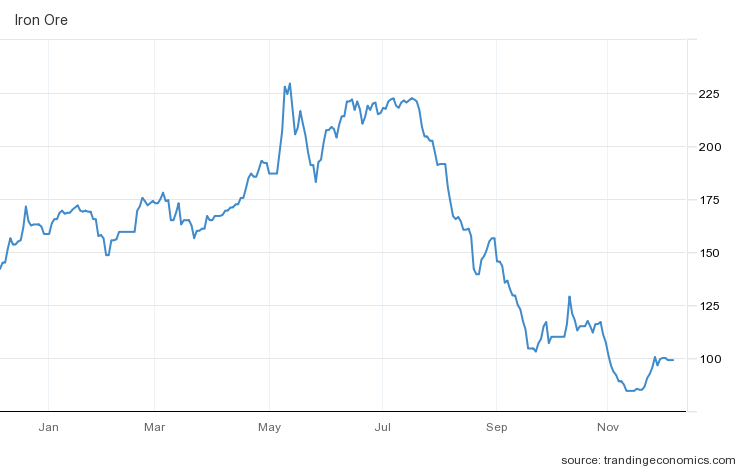

Anyway, today iron ore has surged 8% to 112 USD. Thats a big jump

1 Like

you are not looking at live data

Where can I see that?

Not real-time price (with 1 day delay)

1 Like

Here we go

Pellet prices have started rising.

Low prices below 10k remained for just 2-3 days. Not at all relevant.

October pellet price avg was 13400 or so. Nov was 11700.

Quarter avg likely to be 11800 or so.

2 Likes

China strategy seems like- crash the iron ore price by flashing news of winter curbs etc.- then import tons of cheap ore at low prices- sell steel at high price- repeat.

However, this doesn’t matter for GPIL. If earnings change by 20-30% it doesn’t matter much. PE ratio may change from 2.5 to 2.9 or vice versa with 20% increase or decrease in earnings. That’s a 0.4 change in PE ratio, which is immaterial.

2 Likes

I was already holding GPIL before coming across your thread but with your strong conviction I have decided to increase my holding to 17.5% of portfolio.

Will GPIL be affected by this?

1 Like

SteelMint estimates the weighted average price of pellet (Fe 63%) in Raipur at INR 11,500/t in Nov as against INR 13,350/t in Oct.

Average for the quarter may be around 11800/ton or so, and if volumes are normal and HIRA ferro alloy EBITDA is added, EBITDA for current quarter comes to around 430-480 cr range.- which would be 25 quarterly EPS, or 100 annualised EPS, implying a 2.7 PE for a debt free co, which should grow at 25% CAGR for next 4-5 yrs atleast (due to big capex).

Today iron ore is up another 5% to 115 USD, pellet prices should cross 11000 sooner or later.

2 Likes

Hi kumar,

I had a small question.

GPIL is giving an TTM net profit of 1200cr, it is trading at a PE of 3.1 and an EPS of 86.

The stock is doing heavy capex, moreover it is in the steel industry which might do good in the future due to infrastructure push in the future by the Indian government. Despite it being a good performing company and trading at cheap valuation why is it unable to attract FII and DII investment. What might be the reason for FII and DII to not invest in this company. Last quarter FII increased holding by 0.38% and DII decreased holding by 0.60%

1 Like

What qualities are FII and DII looking for which GPIL is lacking or what might be the trigger in the result which might generate investor interest .

1 Like

Not really.

FIIs are increasing stake every month and every quarter for last 3 quarters.

Please check October shareholding pattern released on BSE, then sep shareholding and June and March shareholding too.

on march 2021 fII had holding of 0.62% and their current holding is 1.87%.

DII holding on march 2021 was 0.54% and current holding is 0.29%.So there is a net increase of 1% in FII,DII holding.

Considering the opportunity GPIL is showcasing a 1% increase in last 10months is not very big. So my question is why is GPIL not

able to attract a Substantial amount of investment despite it being a big opportunity.