Hi, sharing my portfolio here for expert comments-

My portfolio size is at 40x my annual expenses. I have reached this level through concentrated investing mostly.

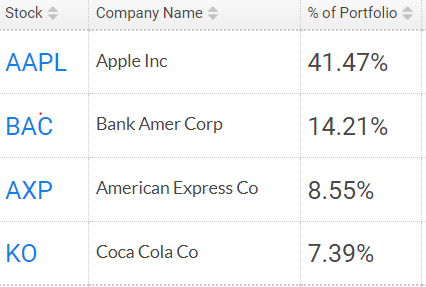

Currently, I have only 4 stocks in my portfolio-

GPIL- I have started posting on GPIL thread a few days ago. GPIL is 40% of my portfolio.

This is my latest post on it. Godawari Power - Any Trackers? - #267 by Kumar_manas

GPIL is my biggest allocation and I have bought stocks in last 1 week as well given how mouthwatering the valuations are. The stock was available at nearly 45% earnings yield just 10 days ago. Even now, it is at 30-35% earnings yield compared to 5% earnings yield of a fixed deposit or 10-12% earnings yield of other commodity stocks. Also, the new specialty steel plant will not just nearly double the earnings but re-rate the company as well to higher multiples than other steel companies as specialty steel plants have higher margins than regular steel. Please do your own diligence.

I don’t agree with many people that it deserves very low valuations. It is a very low depreciation, debt free, high free cash flow company which will be putting a big specialty steel plant in next 3 years (potentially doubling the revenue and profits, leading to 20-30% CAGR in growth for next few yrs). So, why should it not trade at higher valuations than other steel companies?

Also, the solar plant which will be operational in an year should add 170 cr EBITDA/year which is totally non-cyclical in nature. 170 cr non-cyclical EBITDA itself gets a 1200-1400 cr mkt cap in Indian companies if I am not wrong.

Market may have some other views right now, and Mr. Market may change its views when they get EC for the new plant and lay out the detailed capex and expected profits from that plant. Let us see how this happens.

There is no listed or unlisted company in Indian markets that is making annual EBITDA in range of 1400-2500 crores, is debt free and is in 4000-5000 cr mkt cap range or having debt and is in 4000-5000 cr Enterprise value range.

Meghmani organics and Meghmani Finechem- 20% allocation each.

Again both are doing very big capex in next 2-3 years. and currently have low valuations compared to their peers.

The theme of GPIL and Meghmani is common- low valuations, mega capex.

GPIL seems better than Meghmani - because it is debt free. They haven’t done corporate governance mis-deeds like Meghmani did. GPIL has been very transparent in their concalls and presentations every quarter for last many years.

That’s why GPIL gets double the allocation compared to each Meghmani.

Rest 20% allocation to Dynemic products

Again same theme- their new plant is ready now, and it can potentially triple profits. The stock is at lower valuations compared to its peers though not exactly cheap like GPIL or meghmani. Still, the mega capex theme is pretty similar to my investing style.

I see all are cyclical picks…are these 3-4 stocks responsible for your success so far or they have been churned?

Your strategy is not clear with above post. It is like discussing these 3-4 stocks which anyways we can do in their respective threads…

Would be good if you share about your evolution as investor, how you reached the 40x, what you learnt and unlearned and how portfolio evolved over time…that would be a more meaningful portfolio thread discussion and we can also learn from your tremendous achievement of 40x annual expenses! Thanks

So, all of my stocks have a common theme- Low valuations + big capex.

This is the easiest way I have found to make big money.

Earlier, I was more into automobile and banking stocks, but I found that they are also pretty cyclical stocks. Their profits and earnings are dependent on real economy growth and they are also make losses when economy is doing bad.

Also, they can’t increase profits multiple times in a span of 3-4 years.

I found this trend- that companies doing big capex are able to double/triple their profits in 2-3 years and they also get re-rated by the Mr. Market when they do so.

So, both earnings growth and re-rating happens and such stocks go 4-5x in 2-3 years.

Hence, I changed my investing style to align with such companies.

Not sure, why are you calling even dynemic and meghmani as cyclical themes?

Even GPIL with change in China’s steel strategy- where they have reduced steel output and rebates on steel exports- will make steel a very stable commodity from now on, going forward.

Steel was a very cyclical commodity for last 10 yrs- due to China dumping it on other countries. But, the future looks very different.

What is cyclical and what is not cyclical is dependent on your time-frame and your personal views.

Almost all sectors have some cyclicality - from banks to real estate to even FMCG (least cyclical though).

No sector’s earnings keep on going up continuously with no drawdowns. Banks also have had bad periods when their NPAs go up due to stress in the real economy.

Automobile is a very cyclical sector as well and so is chemicals.

Chemical prices keep on going up and down but they trade at 50 PE in Indian markets.

On the other hand, if you have a long time frame, you will find the commodity prices always go up in the long term. If you have short time frame, steel or iron ore prices will look very volatile to you.

However, if you check prices every 15-20 yrs, you will find them in a secular uptrend.

Shorter your time frame, more the volatility will look to you.

Like it happened recently- when iron ore fell from 200 USD to 100 USD.

But, look at iron ore price in 2004, in 1990 and 1970 and then today in 2021. and you will find only secular uptrend.

There are many companies who are under heavy capex or have just completed the capex. There are companies like Acrysil, Sudarshan Chemical, Alembic Pharma, Action construction, CCL, Rajratan, Shaily, Alufluoride and many more in this category… So is there any particular reason to select only 4 company and avoiding all other companies??

Deciding valuation of any company is very very specific for every one. The one who is selling in the market is having the view that company is not having any valuation and one who is buying is having the view that company is having a good valuation and both can not be right. So if possible, please disclose parameters upon which other companies were avoided.

Valuations are very objective. When I put money in Fixed deposit, I get 5% yield.

When I buy GPIL stock, I get 4% dividend (as they will share atleast 10% of profit as dividend), and 35% earnings yield. 35% yield is 7 times the yield on fixed deposit. There is no subjective criteria here.

Other things are- debt status, promoter history, competitive advantage, risks.

Alembic pharma- US generics are having price erosion leading to reduction in profits. Huge risk of US FDA audit every year. These risks are very objective and not subjective. The companies who are getting majority of profits from exports to US Mkts are constantly having erosion in their earnings because of huge competition in generics in USA.

Do they have a brand in US - No.

Can they for sure double revenues and profits in next 4 yrs- Not sure since their profits are always under threat due to price erosion.

Do they have innovation- No. they just manufacture generics like many other pharma cos.

Do they have risk of US FDA audit and sudden crash of profits- Yes.

Rajratan wires- I can’t see any NEW mega capex as you mention and earnings yield is very low. 120 cr EBITDA and 2000 cr mkt cap.

The capex I guess is last 3 yrs capex you are saying that has already happened. So, one should have bought Rajratan 3 yrs ago- when they started this capex in FY 19. It has already completed- and that’s why co has grown and re-rated and become a multi-bagger, and this is exactly what I am talking about. As per my style, Rajratan was a big buy in FY 19, when they started this capex- see the returns in last 3 yrs- both earnings growth+rerating has already happened here.

Ace - again, what’s the earning yield here? 3000 cr mkt cap for a 150 cr annual EBITDA? GPIL is doing 10-15 times this EBITDA and has only 4300 cr mkt cap. It is a very objective number based calculation.

And, again I can’t see any big capex happening here. Please elaborate which mega capex is happening in Ace?

Acrysil- yes, this looks decent. Agreed, it is continuously increasing capacity every few months. Valuations are on the higher side though.

Rajratan

Existing Capacity - Currently we have a capacity of 72,000 Tonnes per annum in Rajratan India and 40,000 Tonnes per annum in Rajratan Thailand;

Existing capacity utilization - We are currently operating at 80-90% capacity at both locations combined together;

Proposed capacity addition - 60,000 Tonnes per annum

This is the new plant proposed in South India

More ever we must also consider the nature of business in which company is operating. Rajratan having a business where entry barrier is very high… Business is ever-growing business not cyclic.

I guess this is not in the balance sheet yet, so thats why I can’t see it.

Barrier in iron ore mining is a lot higher. Iron ore mines are being auctioned at 118% premium. The buyer has to pay 118% of the price of iron ore it gets to the govt for every tonne of iron ore- Forever.

Basically, the buyer will never make a profit if it is paying 100%+ premium.

But they still bid at 100% because they get assured supply of high quality iron ore.

Even if you have Rs. 5000 crore cash today, you can’t buy a low cost profitable iron ore mine. Such are the times in India right now.

Action construction is operating at around 50 - 60 % capacity so they are able to increase the production without any expenditure. Business also looks very good. Huge manufacturing growth in India will lead to increase utilisation is product made my ACE + they also started supply for defence project also. We can’t go with profit what they are generating today. It is the future prediction which makes a company valuable. Increase capacity utilisation will definitely lead to margin expansion also.

Thanks for sharing your investment strategy and the detailed rationale behind selecting your stocks.

Your strategy brings to mind Buffet’s words, "Diversification may preserve wealth, but concentration builds wealth. ", as a matter of fact he himself has more than 70% of his portfolio in 4 stocks

I concur with you on your views about GPIL & Meghmani. When I had earlier analysed Dynemic products the concern for me was that they were not keen in entering into natural colors, the time for getting the Environment Clearance being unclear was another point. Could you give your views on this ?

In the process of identifying the 4 stocks did you get a chance to look into Anjani Portland, this pretty much satisfies your criteria, they have recently acquired a company of almost the same size as theirs(Bhavya cements).

Yes, low valuations + mega capex looks like a very good framework.

Infact, one can start a separate thread for companies which are doing big capex plus have low valuations.

Or is there an existing thread already there?

I was holding alembic pharma at one point of time because of this mega capex actually.

But, I sold it because the company guided for profit erosion in US generics.

I agree the point that Buffett is holding 70% in just four stocks but we may also need to consider the point that whether he started investing with 70% in four stocks? What we are seeing is the huge huge compounding of 20-30 years.

It is possible that one day a stock of my portfolio may become 30- 40 % of total portfolio but I would definitely not consider to invest 40% in one stock. Let us give a fair share to every stock and I let it grow to any % share in my portfolio. GPIL Acrysil and Rajratan were more than 50% of my portfolio in last month but I didn’t started with 50%. I alloted a fair value and I let them grow. If a stock is good it will definitely gain position in your portfolio.

I agree. My initial purchase price of GPIL is Rs. 400 per share, but I have been adding recently as well at even Rs. 1300 per share. It is not that I started with 40% allocation.

However, after the merger with Jagdamba was withdrawn I became confident of their corporate governance- they are unlikely to take small investors for a ride.

They could have gone ahead with the merger, but they did not.

This shows that they don’t want to put up a bad image of themselves in the market.

In India, once market is sure of corporate governance, the re-rating happens usually, sooner or later.

One company I would like to suggest for this theme is S.H. Kelkar. Fixed Assets are almost double and relatively very cheap give the the valuation of speciality chemical companies.

You have made good narrative and good approach. But, I advise you to invest in at least 10 such companies. If anything goes wrong in your assessment, it will not burn your finger heavily.

Thank you, however I have researched my portfolio companies in great depth.

I have even read the EC documents of GPIL mines.

My view is that wealth creation needs concentration.

Yesterday only, Tata steel placed a bid of 141% for a mine in Odisha. Tata steel would be making perpetual loss, but still wants to buy the mine.

Here, I am getting a mine at 3 PE. How ironical is that!

Promoters of Tata Steel are able to see something which Mr. Market is not able to see?