Lot of thoughts going in my mind with this latest development. From promoter’s perspective, It’s difficult to understand and find rational for Bain becoming majority and hence controlling shareholder in Manappuram. Why?

- Promoters are not selling their stake, they continue to hold skin in the game. But Promoters have left driving seat to Bain, while they plan to sit on sideline. Leaving control is not easy, why would promoter loose control. dilute his stake and continue to have skin in the game? There has to be some strong rational, that I am not able to understand.

- Do manappuram need funds to grow? A quick look at the balance sheet and P&L will tell you that company is having tons of cash to take care of future growth. In fact, they generate ample cash yearly , which they don’t know what to do with.

- Does Bain brings any expertise to run Gold loan business better? No, Promoters are running the business from generations and know in and out of it, so I find it difficult to accept it to be the cause.

- Does Mr Nandkumar was forced to bring in Bain? There are no apparent reason for this either, but this looks to be the most plausible explanation. Why?

There are many “maybe” explanations that may fit like:

a) Maybe it provides better perceived corporate governance.

b) Maybe regulator (RBI) perceive manappuram as better & professionally managed company with Bain as controlling shareholder.

c) Maybe…

d) Maybe…

e) May be…

I dont see a definitive response that I can accept on this front.

But one thing is clear, BAIN has come to make money and leave. It will squeeze everything it can to grow the company, produce higher profits, command better valuation and leave the party. How it plans to do it? Will it be successful? Answers of these questions will emerge with time.

So, lets wait and watch.

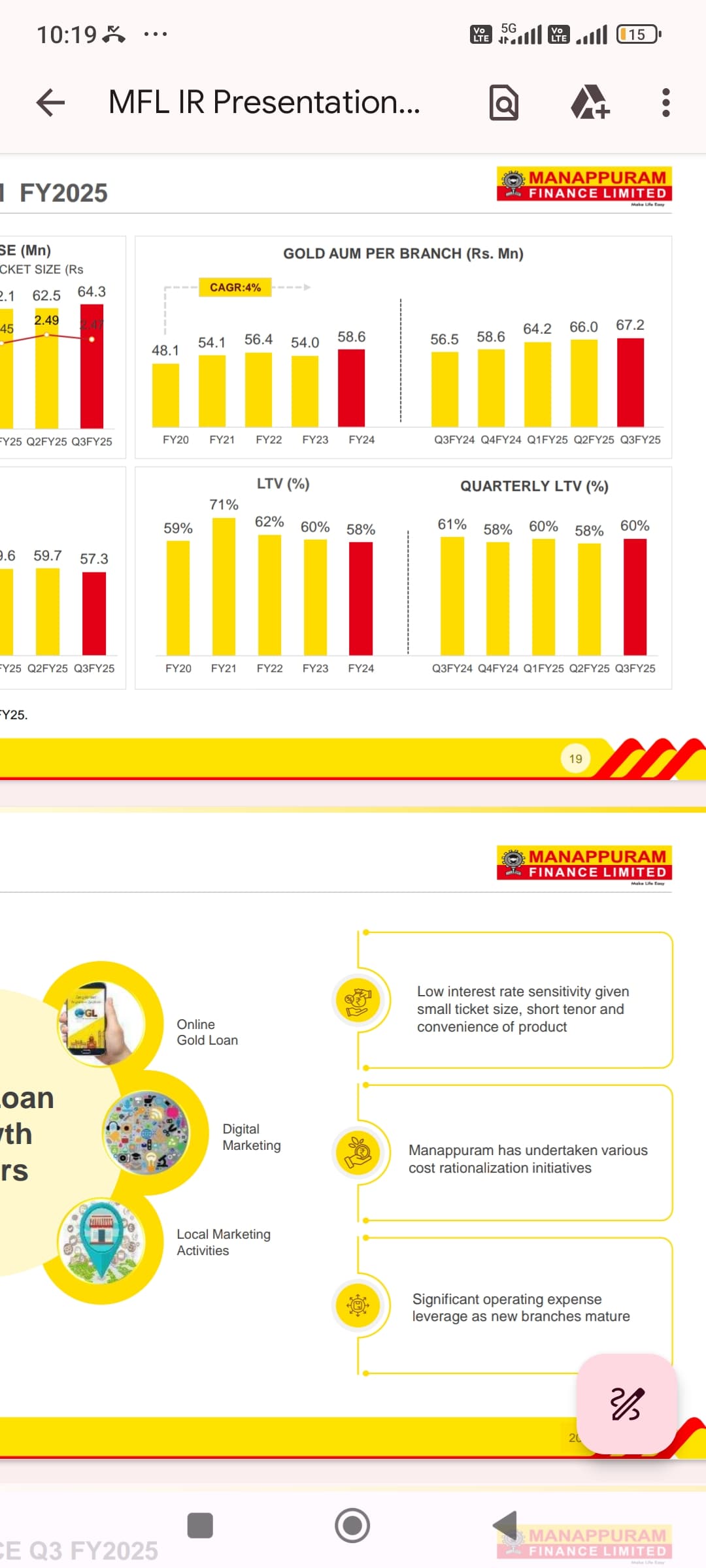

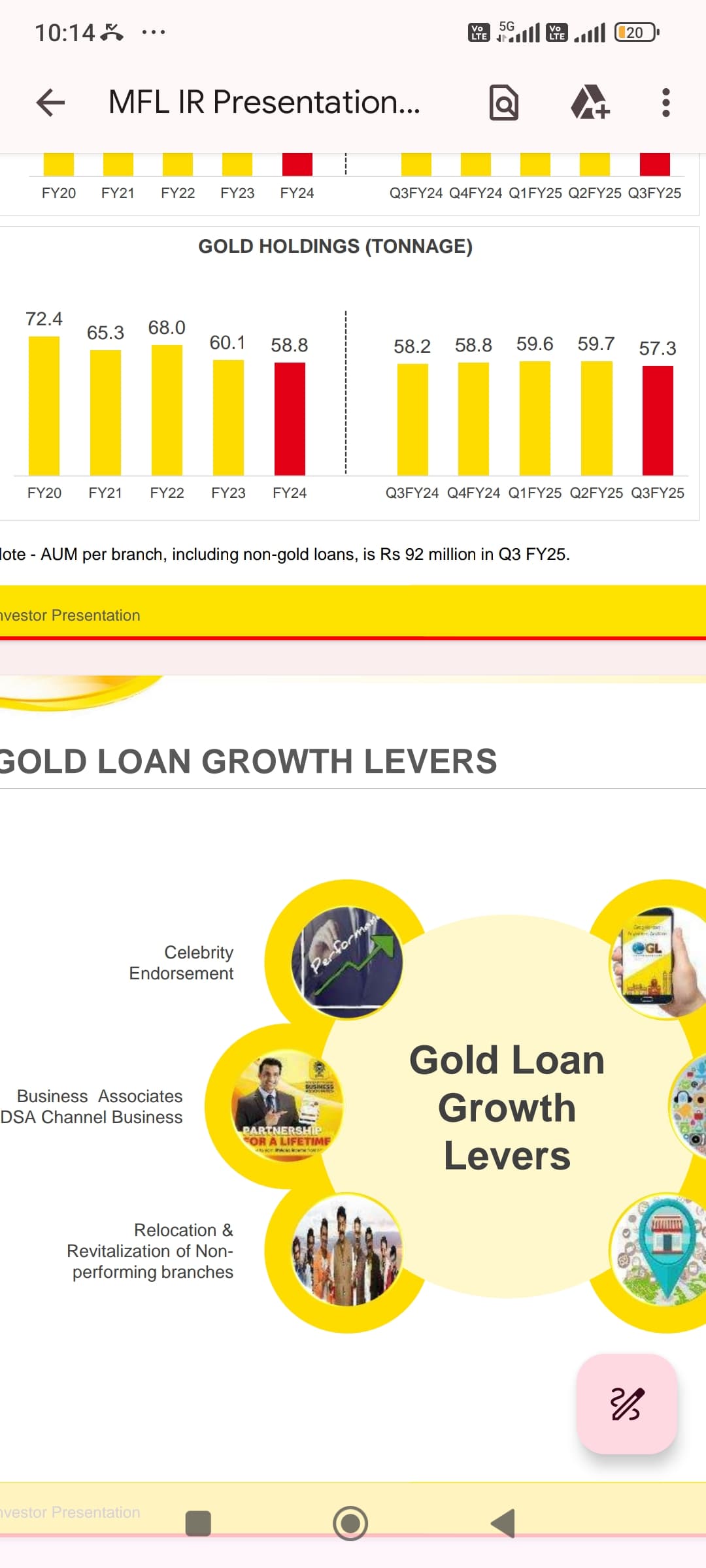

On other side, I see the competitor, Muthoot playing a different game. If you look at Muthoot data closely, you will observe that it’s Gold Loan AUM has doubled in last five years (2020 to 2024), but profitability has moved hardly 1.4X. The reason looks to be that Muthoot is willing to lend cheaply, and it can also afford to do so, as it is lowest cost operator (Gold loan per branch is much higher than manappuram, and his servicing those loans is much cheaper. And cost of operations is huge in gold loan business).

Manappuram has stayed away from this game, in fact manappuram cannot compete in this game as it is not the lowest cost operator, and hence has targeted customer segment that’s less sensitive to price and tried to remain highly profitable. However, data also tells that manappuram is not able to increase gold loan AUM during last 5 years when compared to Muthoot (2020 to 2024).

So, I believe Muthoot is giving tough competition to Manappuram to grow , and its hard to move ahead in the game for manappuram.

Aashirvaad Microfinance remains a joker in the pack that I dont understand.

These are my thoughts for now, and may be completely irrational from other investors perspective. I would be glad to hear counter arguments.

Disclosure - Invested, biased. Not a sebi registered analyst.