After capital infuse by Bain, open offer at price of 236 will trigger to further increase the share holding of Bain capital. It can vary from 18% to 41% till open offer ends. It indicates that lower prices of share will cap at 236 rupees. How much upside happens from 236 will have to see? Disclaimer: holding from 89 levels and biased.

1 Like

There is a bit of a contradiction in your statements. Even Muthoot is impacted by the change in the market dynamics. If you look at it for a 2x increase in AUM the profits has increased only 1.4x . With increased competition Muthoot has reduced the pricing and hence its profitability has also decreased. The only point is Muthoot may not be bothered about the valuation. Muthoot is playing a long game, sustainably growing and being there, waiting for its time.

Manappuram may be in for a valuation game as at some point the promoters may want to cash in. This could be the reason for allowing Bain to enter ..scale up.. increase the valuation … sell off

4 Likes

Nandakumar and his family have a lot of experience running Manappuram, but Bain Capital has more specialized skills and resources to grow businesses. Bain has a strong history of making companies more successful using smart strategies, technology, and good management. They also have a global network and more access to funding, which helps with expansion and innovation. The Nandakumar family doesn’t have the same resources or outside help, so they may not be able to grow the company as quickly or efficiently as Bain can.Bain is a completely different league with different skill set while nandkumar on sideline will put his expertise .Old age plus new age combination may be good

4 Likes

Nandakumar age is above 70 years and his only daughter is Gynecologist. Further, she is not interested to run or overlook this business. This is the only thing which forced Nandakumar to sell his stake.

4 Likes

Nandakumar is not selling his stake for now and Bain has been provided equity through dilution of the entire outstanding shares. We can only conclude if he tenders any share during the open offer.

2 Likes

There is a 4-year lock-in period for Nandkumar; he cannot sell his shares during this period as per the deal.

I believe Bain’s plan is to fast-track growth over the next 5 years, build strong valuations for Manappuram, and then exit with a 20% CAGR return. The most likely exit route would be through an IPO of the subsidiary

5 Likes

4 Likes

Nothing major I feel

In boom period need strict controls

2 Likes

Open offer price by Bain capital is holding Manappuram at current level, otherwise considering past track record of volatility in Manappuram - it could have been below 200 at this news.

2 Likes

Joker has declared Q4 FY2025 results - wondering with the kind of provisions taken (Rs. 849 Cr just in Q4, in addition to Rs. 472 Cr already done in Q3) - will Listed Manappuram Finance declare net loss in Q4 FY2025.

Since my first investment in Manappuram - I haven’t seen it reporting loss on consolidated basis.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/766f7bd6-5928-42aa-94f9-1e430d156093.pdf

1 Like

(63,871) lacks lost for the whole year (62.6,00)lacks lost for the quatre yearly will show profit

i expect in the range of 1500 crores to 1800 crores quarterly a break even or a loss of 1 to 200 crores .

I think this is reason IPO was delayed and Brain capital did not value the assets of its subsidy much any how the quoted price of 231 per share is the correct price

On the positive side the company will again become a gold loan lead company

1 Like

Reason for yesterday rise. Do not know how long price hovers around 229-231 levels. But one thing is sure it is the ofs that is maintaining price at these levels after such disastrous results. In future MFI will become 10% of overall AUM.This is as per latest concall.

DISCLAIMER: HOLDING FROM 89 LEVELS and bought till 150 levels for past 2-3 years.

4 Likes

Personal loans are getting difficult to have due to its unsecured nature these days and hence people are force to pledge their gold for meeting their needs.

Disclaimer: holding Manappuram and biased.

1 Like

Bain

High LTV

better sentiment

Getting into more secured loans

High loan value

Still undervalued

3 Likes

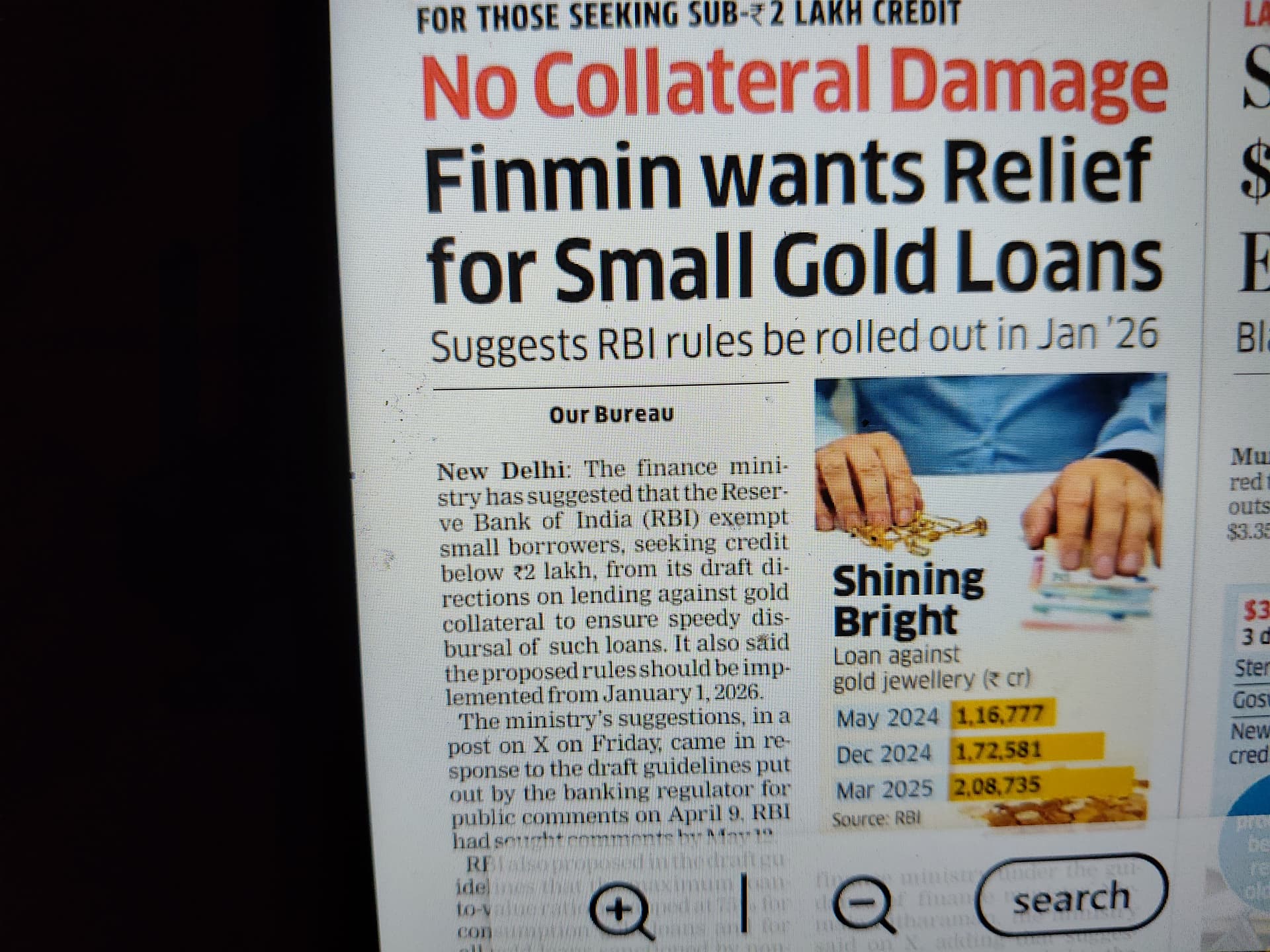

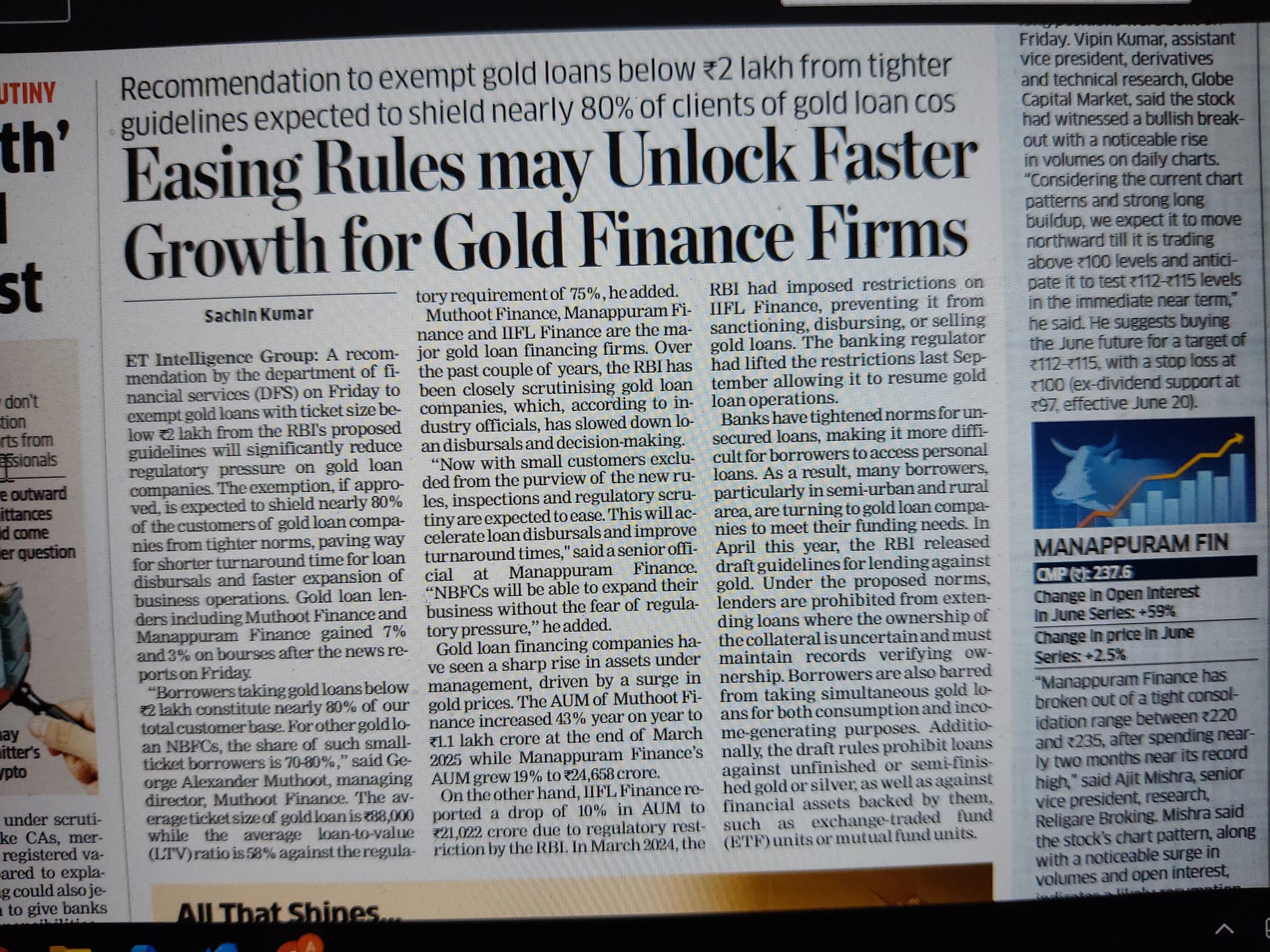

Think another guidelines on same day by RBI i.e. on “Review of Qualifying Assets Criteria” Reserve Bank of India - Notifications is also important. Now with just 60% of unsecured MFI lending book an NBFC can get a tag of MFI-NBFC, remaining 40% can be in secured book.

For Asirvad, they can increase Gold loan book - which seems a positive development.

On the flip side, other MFI-NBFC can also start Gold loans aggressively (as a minor segment).

Additionally, there is change in guard at Asirvad too - Mr. Nandkumar’s buddy Mr. Raveendra Babu tenure as MD ended on June 01 .. and new CEO (from an ex-manappuram kid Mr. Chinta Prasad to a professional banker Roy Varghese) has been appointed.

All in all, it will be a key event - once open offer by Bain Capital ends - how biggies in market perceive Manappuram - a next wealth creator - or - still a value trap.

Disc: Invested

4 Likes

Gold loan business is operationally challenging business

It takes ages to settle and set up this business

current book value of 150

20% growth in book will make it Rs 300 book in 3-4 years

With easy 2-3 x price to book Bain will exit in 4 years that’s my guess

Its a golden period for gold loan with sky High gold price , increase in LTV, plus Bain effect will increase efficiency in the system and hopefully make the business more robust and add will add excellent technology

2 Likes

You are bang on.

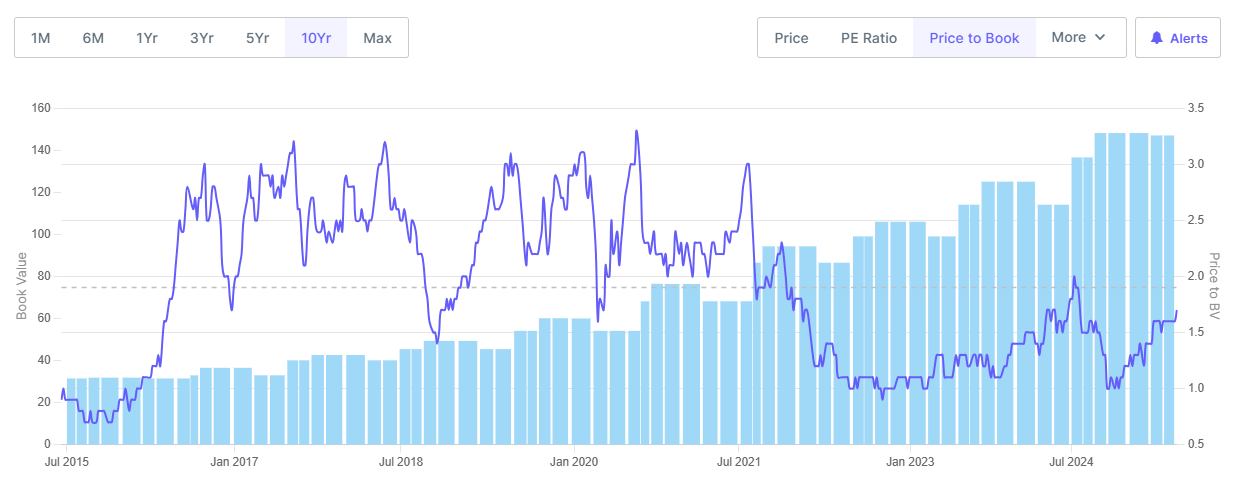

As per screener data, PB has been between 1 (on lower side) and 3 (on higher side) in last 10 years out of which last 5 years were like a bad dream - prima facie on account of poor corporate governance.

An investor’s dream would be to see the underlying (invested) company to trade at best possible valuation ratios.

Now with Bain capital as coach, and its appointed KMPs as players - we look forward to a rewarding investment.

FII’s already own a quarter of Manappuram.

Let’s see if DII’s bet their dry powder on Bain & team - if it happens - we are riding the next bull.

As a side note: Muthoot is consistently above PB of 2 and specifically in last 1 year available at PB of 3.

4 Likes

Now market see some medium term stability due to few factors

-Bain

-high good price

- RBI ‘s positive actions for good loan less than 2.5 lacs

Overall can see safe secured 20% growth in the medium-term

So can see price to book 2-3

1 Like