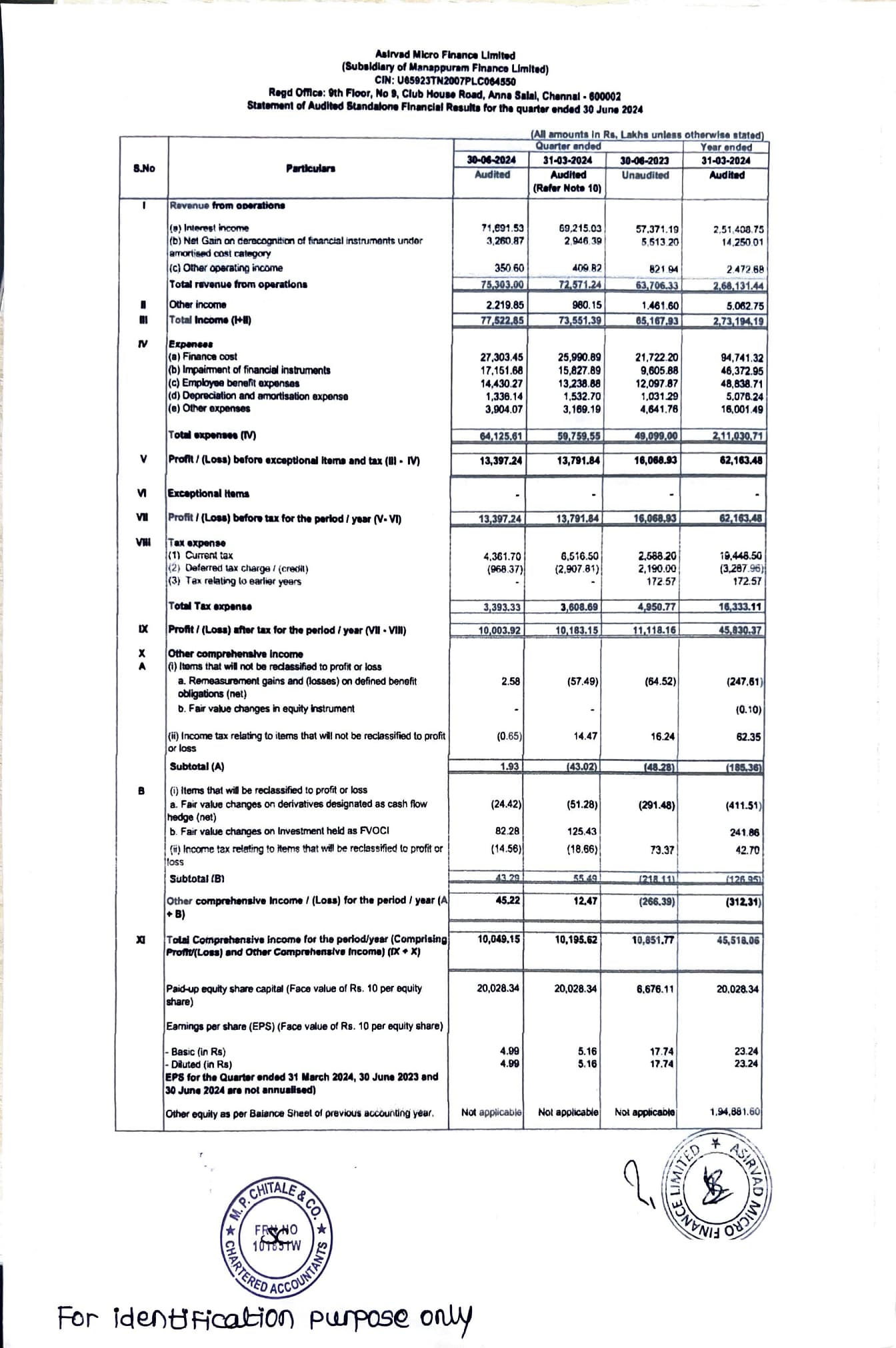

Asirvad Micro Finance results -

Results are standalone not consolidated

What is happpening in IPO front of Asirvad? Is it going to happen or still some issues left. Anybody who has clear cut understanding of matter, please help us in understanding the matter of their ipo route through holding corporation? Why they are not demerging Asirvad and seperately listing them on exchanges?

Can someone please share the net profit from the Ahirvad result? I’m unable to open the link.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/c61edc80-3592-4fce-bd13-885f894ce049.pdf

Growth Guidance At 30-35% For FY25: Manappuram Finance | CNBC TV18")

Good results.

Key highlights from the conference call:

- Management has now guided a 15% gold loan growth for this year, up from the previous estimate of 10-12%.

- The non-gold portfolio (excluding Ashirwad) is expected to grow by 30-35%.

- Discussion on Ashirwad Microfinance is currently on hold due to the upcoming IPO.

- Stress in the microfinance sector has likely peaked, with improvements expected going forward.

Growth drivers include:

- Rising gold prices

- Expansion efforts

- Stable borrowing costs

- Reactivation of old customers

- Increasing demand

- Shift from unorganized to organized gold loans

Risks include:

- A drop in gold prices

- Regulatory changes

- Geopolitical tensions

- A decrease in demand

—————-

Analyst target price post result

- ICICI securities : 260 Buy

- Jefferies: Rs 270 (maintained BUY )

- Nirmal Bang: Rs 248 (BUY ,raised from previous Target price of Rs 242)

- IDBI Capital: Rs 225 (maintained TP ,HOLD )

- Axis Securities: Rs 250 (BUY ,raised from Rs 220)

- Morgan Stanley : 245(BUY , overweight)

- Motilal oswal :250 (BUY )

Disc : Invested

Dear @maheshkumar … I too have manappuram finance and I have started buying it from 89 levels and kept on accumulating when all ED fiasco is happening. I have heard management commentary on ED raids and some how got the feeling that management is innocent in this case. It forms good portion of my portfolio. My exit criteria from manappuram will be value unlocking after Asirvad listing. What is your exit criteria for manappuram. As an investor , I feel lot of difficulty in getting the right exit criteria. This is where I am struggling a lot. I like to know your prespective?

I think as long as the Gold prices go up we can hold Manappuram. My view is that it is indirectly investing in gold.

The gold finance business carries significant geopolitical and regulatory risks, along with the potential for non-performing assets (NPA) in non gold

Therefore, regular careful assessment is necessary before making a decision to exit.

Personally, I would exit Manappuram under the following conditions:

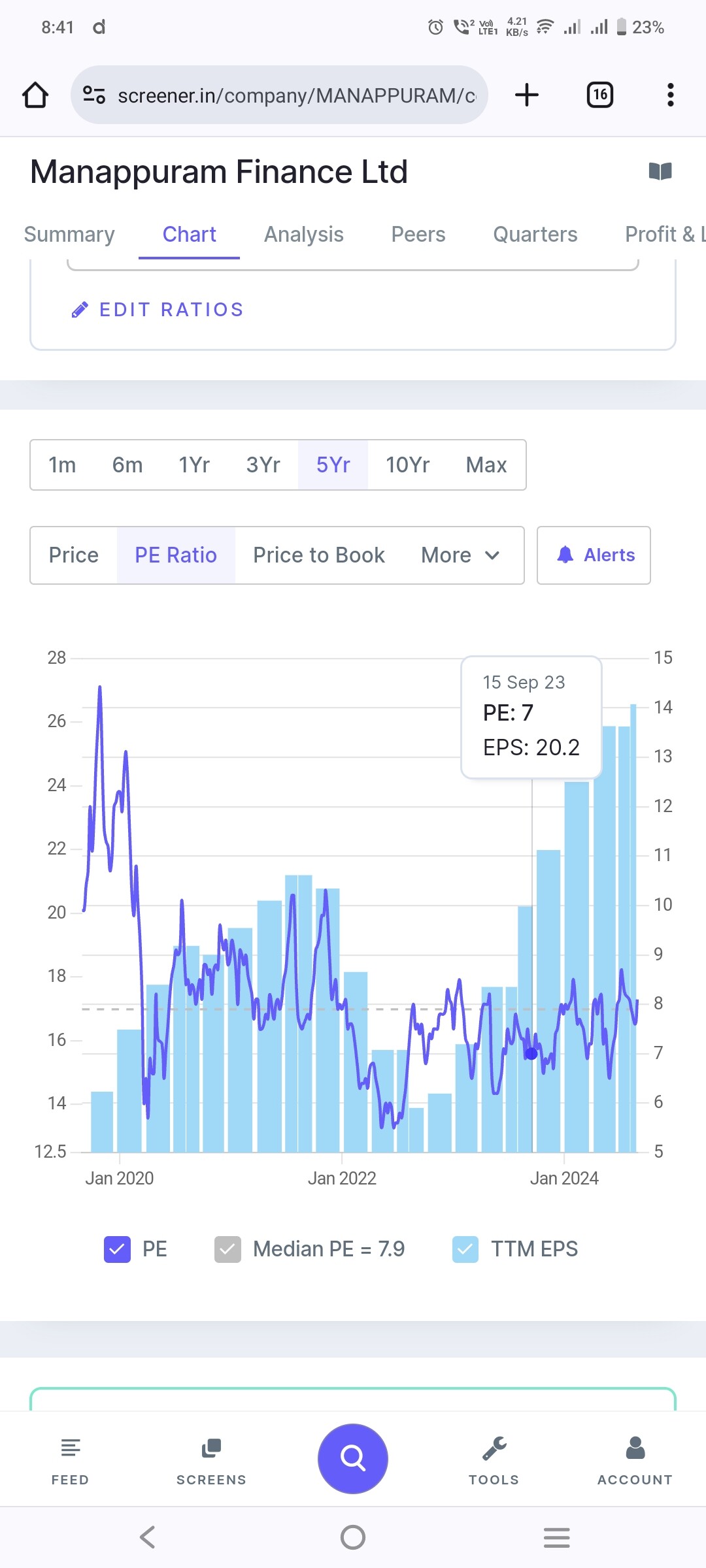

- Overvaluation:If the stock’s valuations become excessively high. Currently, the stock trades at a price-to-earnings (P/E) ratio of 7.5, with a dividend yield of 2%, effectively making the P/E around 5.5 for a company growing at 20%. I believe the fair value should reflect a P/E ratio of at least 15 or more.

I don’t value Manappuram on price to book as its PE if u compare with other NBFCs then there is a mismatch

- Increased Competition: If the company faces significant competition that negatively impacts the growth of its gold loan business.

- high NPA in non gold

4)There are also numerous unpredictable factors that could arise in the future. These challenges will become clear over time, but I believe the management has proven its ability to navigate through difficult situations effectively. For instance, they successfully handled the challenges posed by demonetization, the COVID-19 pandemic, and recent regulatory hurdles. The management has consistently demonstrated their competence, having been in this business for decades. I feel confident they have the capacity to overcome future challenges, and I remain optimistic about their continued growth.

5 ) business model failing due to regulatory risks

How will an IPO of subsidiary be value unlocking to shareholders? A demerger will be. IPO, I don’t think so. It will be a value destructor in fact. Manappuram will become a holding company of Aasirvad and will get discounted.

Then why promoter chooses such a route of asirvad ipo?@maheshkumar, @ sudhakar

Prof Sanjay Bakshi video old video from covid 19 era

Still many things are relevant

My takeaway

He Explains the relationship between the price-to-earnings ratio and the price-to-book value

He gives an example scenario where a business ( Manappuram ) appears cheap based on its P/E ratio but expensive based on its P/B ratio.

Prof explains that if the company’s book value were increased without changing its earnings, the P/B ratio would decrease, making the stock appear more attractive. However, this also results in a lower return on equity which ultimately makes the investment less efficient.

Explains the paradox of improving the P/B ratio at the expense of ROE, showing the complexity and potential contradictions in relying on these metrics alone for investment decisions.

One more optimistic report

Interesting to know that it was about Manappuram. When he posted this video on October 20 it had high P/B but low P/E. The price crashed to about half or two thirds from its highs after that, making it a low P/B and high P/E by November 22.

So with the benefit of hindsight what was market pricing in 2020? I think it was the fluctuating gold prices. The assets were not likely to become NPAs as he said ; but then the fluctuations forced their hands to auction the gold or recall the loans and bring down the loan book.

In addition the barriers were not as strong as it was supposed to be. It was not new entrants but the banks that focused on gold loans much during the period. In a low entry-barrier business low PE and high PB indicates arrival of competition as he said. When the business became high PE and low PB by 2022 the cycle has turned. Banks had better things to focus on and the intensity of the competition probably reduced?

But when I last checked a quarter ago the microfinance in which they have not yet proven themselves seemed to get riskier and I partially exited.

The gold finance business is highly operationally intensive. While entering the market is relatively easy due to the lack of significant barriers, maintaining and expanding the business on a large scale, as companies like Manappuram and Muthoot have done, is challenging. Bajaj Finance and many others attempted to venture into this sector but failed to keep focus

Similarly, many banks and non-banking financial companies (NBFCs) have tried their hand at gold finance, but often lose interest as it’s a single run business and most banks are intersted in 4s and sixes

The gold finance business is not easy to sustain.

Many triggers will help them

-benefit from an increase in gold prices, which boosts AUM

This advantage, combined with average growth potential, makes companies grow around 20% over long term

non-performing assets (NPAs) are not a major concern in the gold finance industry.

Before the COVID-19 pandemic, there was little competition in this space, but post-COVID, competition surged, which ironically increased the popularity of gold loans.

Despite the influx of competitors, demand remains high. It is estimated that two-thirds of the gold loan market is still in the unorganized sector. There is a gradual shift from unorganized to organized sectors, which is expected to drive further demand and growth.

Several factors act as triggers for the gold finance business: rising gold prices, the migration from unorganized to organized sectors, the perpetual need for loans, increased demand due to inflation, and the advantages NBFCs have over banks in terms of faster processing, better customer care, and longer working hours.

The gold finance industry is here to stay for the long term. Although competition may fluctuate, it is difficult for new entrants to sustain their operations over extended periods.

Only companies with a primary focus on gold loans will likely endure, while those whose main business lies outside of gold finance may struggle to maintain a foothold in this demanding industry.

In summary, while there are no significant barriers to entry, sustaining and growing a gold finance business is fraught with challenges. Over time, I strongly believe that Manappuram will see a significant re-rating from its current price, and this potential will become more apparent in hindsight.

How can a share price crash make the p/e high?

On the contrary p/e should also have crashed as p is the numerator and as a result directly proportional to p/e.

Also I don’t see Nov 2022 PE greater than Oct 2020 PE as per screener.

What we see is, share price crashed in line with EPS crash and PE remained same or actually reduced from oct 2020 to nov 2022.

True. I didn’t want to edit it after making the post. The earnings crashed by close to 30% from Oct 20 to Oct 22; stock price crashed by close to 40% during the same period. ( I am referring to the values 18.96 and 13.87 for EPS during the periods and 166 & 103 for stock price )

P/E came down but not substantially as I stated before. So you can basically call it as a stock trading below its own ten year median P/E during both the periods.

The change was in P/B. In Q2 and Q3 of 2022-23 it traded at a low P/B value and at times going below 1.

When the video was shared the assumption was that the high P/B was justified because there are entry barriers in this business. Even while agreeing that gold focused players are here for the long term and not everyone can scale this up , it is also true that many are opportunistically getting into this business affecting the margins and business growth at least for a short period.

So for such a business which goes through these cycles P/B alone could be a good reference. When it is trading at high P/B chances are that the market is reflecting the high ROEs and RoAs . But the high returns are attracting many opportunistic players into the business . When it is trading at low P/B those opportunistic players have already got in bringing down the returns . Now the returns are no longer attractive so that only focused long term players continue. The cycle repeats as non gold NBFCs/ banks etc get out of it.

So what about the low P/E? Where does it fit in? I think the easiest way to think about this is that the ratio of P/B and P/E , which is RoE , should go through a cycle if you believe that the business shows a cyclic nature - even if they are short cycles. If you believe that there are strong entry barriers then the returns or the ratio of P/B to P/E should improve or remain stable.

I am thinking this afresh so please don’t mind any contradictions with the previous post. Also I am thinking as I am writing this so the arguments may have holes. I am trying to think about what he was referring to a low P/E and high P/B scenarios. Let’s think about the truck business which had a book value of 2000 Rs and providing a return of 500 Rs. If it is trading at 2000 Rs then the return is 25% which is high. So for the sake of simplicity let’s assume that the market is pricing it at 4000 Rs and the earnings yield if you buy the stock now is only 12.5% . The P/E is 8 now. If the owner deploys another 2000 rs that gives zero returns then the P/E is still at 8 but price to book has become an attractive 1 now. So the essence of his message, I believe , was that you shouldn’t be looking at the high P/B negatively. You shouldn’t if you believe that entry barriers are strong. But if they are not strong then many players will enter this business bringing down the returns and the stock price would react to that.

Now something else.

Right now the projections on gold loan portfolio seems positive. But my question is how do you see the non gold loan portfolio. If I remember right only about 50% AUM is gold loan now. How good you think are their non gold loan portfolio? It is not the secured kind as referred in the video. In fact when we say that non gold NBFCs and banks may not do well since they are not focused , the same should also be true for gold focused players entering into other business. Will they lose the advantage they had on as a gold focused player or the present stock price take care all of that?

I think its all about perception. When banks were aggressive in gold loans then general perception is that manappuram is well placed then muthhoot due to diversification of business. And now when banks are not very much interested in gold loan then perception is becoming that Asirvad can make the business of manappuram quite risker.

There are things known and there are things unknown and in between are the doors of perception.

Holding and biased from 89 levels

MANAPPURAM FINANCE

Concall - Q1FY25

GOLD LOAN

But the demand has gone up. Our average ticket size remains around INR70,000 to INR75,000. From that class of customers, the demand started coming in. The ban on competition, I don’t think the effect is significant. Because even if it is there, it is getting distributed to so many players. And many of these are going to banks. Basically, the customer requirement has gone up. The demand for working capital, etcetera has gone up.

GUIDANCE - 15% this year. There will be growth in the number of customers also.

Gold Loan AUM has increased mainly because of demand increasing and their total live customers have increased…

During the quarter, we were able to add 4.21 lakh new customers and the number of outstanding customers has gone up to 24.5 lakhs from 23.76 lakhs

Online gold loan book stands at 70% of total AUM.

The gold loan AUM stands at INR23,647 crores, up by 9.11% Q-on-Q and 14.8% Y-o-Y.

MFI

For Asirvad, our Microfinance subsidiary, the AUM stands at INR12,310 crores, including gold loan AUM of INR1,016 crores;

The second thing, the gold loan also is coming to around 10% of the portfolio where you cannot expect, because that’s why the regulation also has facilitated the non-gold lending that has been enhanced from 15% to 25%. So, we have 520 branches as disclosed earlier.

Borrowing cost, at this stage, it is continuing at a similar level only. So, I think we are also expecting rate reduction, let us see, I think in September.

Other sectors

Most of them are secured .

House growing well. - Gnpas are a bit higher than other affordable housing companies….

Vehicle finance is also growing very well.

MSMe Gnpas have increased but the management is confident and a very small portion is unsecured.

My views on the Concall and the company

Management thinks that everything is related to heat waves, farmer loan waivers and elections and productivity loss.

Could be that the secured part of the portfolio may recover in the coming months.

I am more concerned about the MFI sector -

Many players in the MFI sector are talking about provisions and credit costs increasing and over leveraging in the industry.

On the other hand, the management did not say anything about this as there is an IPO which is on the way. They did not accept that there is over leveraging in the MFI industry only accepted that some states have problems.

Arman has been guiding for higher Credit costs for 2-3Q and even other MFI people(ujjivan,etc) are now accepting the same.

The management seemed optimistic about recovery in the MFI sector. .

| Q1 | Q2 | Q3 | Q4 | FY24 | Q1 | |

|---|---|---|---|---|---|---|

| MFI | ||||||

| AUM | 9310 | 10088 | 10685 | 10938 | 10938 | 11235 |

| Customers | 0.339 | 0.36 | 0.378 | 0.391 | 0.391 | 0.388 |

| AUM/Customer | 27463.12684 | 28022.22222 | 28267.19577 | 27974.42455 | 27974.42455 | 28956.18557 |

| GNPA | 2.9 | 3 | 2.8 | 3.7 | 3.7 | 3 |

| NNPA | 1.3 | 1.4 | 1.3 | 1.7 | 1.7 | 1.4 |

Could be that Manappuram is resorting to top up loans as their AUM has increased and MFI customers have gone down and their GNPA has also reduced.

On the other hand there are not many MFI lenders whose GNPAs Have reduced.

Pros

They have a 8-9% gold loan AUM in ashirwad which will help them.

No state has more than 10% and no district has more than 1%.

Gnpas have reduced but i am not sure how to read this as it could be cause of top up loans.

The Company is cheap on a P/E basis and has the Gold Loan Portfolio which is a very high yielding product with NO Credit Costs.

I am a bit confused on whether the MFI business will bite manappuram in the back.

Where as I am very interested in the Gold(as growth has just come back) and other Lending Products(Growing very fast)

Everyone please feel free add your views on the business.

@maheshkumar - you have been tracking this business very well for quite sometime.

Disc - Invested.

Sold Some shares Recently…