Overall quantity bought is 3,50,000 shares (worth approx. Rs. 6 Crores) which seems (for me as an individual) to be a peanuts considering the worth of Mr. Nandakumar.

Consider it from a point, a promoter earning handsome salary from listed company, earning approx. 75 Crores in dividend per year but reinvest just a fraction in his own company (where his family own 35%).

Reason → Either he don’t think, company is under-valued; or he is finding better opportunities to reinvest his earnings; or he is leveraged where most of the earnings are used to service personal debt.

Last time Mr. Nandakumar bought from Market in September 2022.

Note: I reinvest entire dividend back in Manappuram.

there wont be much difference as manappuram will be a holding company when the aasirvad grows may be it will be reflected in the manappuram stock but as of now this is a long term bet maybe more than 3-5 years

Muthoot is a much larger company almost double the AUM with more customer centric focus and more assets per branch so lesser compared to overall AUM % wise more aggressive marketing they are opening more gold branches 150 per year ,what works best for manappuramis microfinance as they have extended it to only some of the branches 20 % only right now i believe so execution is the key if not this they should grow gold loans

as the promoter buying i see it as positive i don’t have reasons why a promoter should invest fully back in the company

What is holding manappuram in recent rally post election results? I think holding corporation issue creates obstacles after Asirvad listing. I don’t know why prompter want to go for holding corporation route for Asirvad listing. Is it makes better control over newly formed company? Any experience person can share his/ her views on this.

My book on what’s happening to the US Dollar and hence Gold prices - https://bit.ly/3z4ITqR

Forewords to the book has been written by two renowned investors / economists - Dr.Marc Faber and Doug Casey. Snippets are included in the back cover of the book.

If the moderator feels appropriate, the book may kindly be shared in other stock groups as well.

Risks -

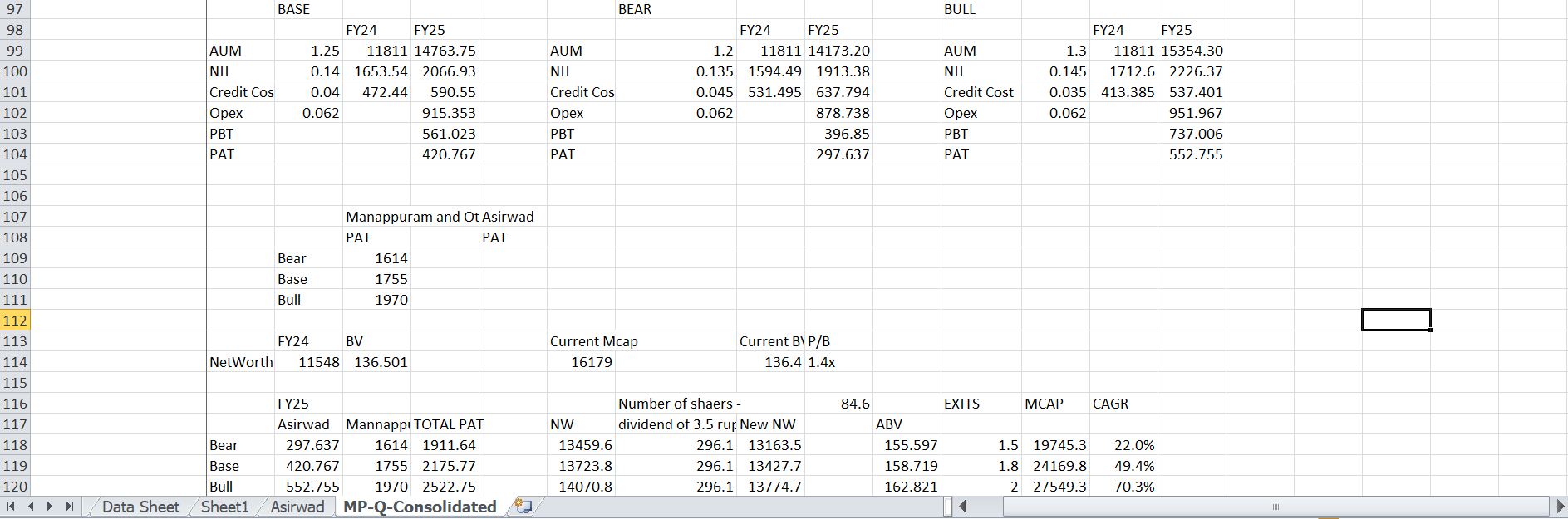

There was a steep rise in GNPA QoQ in asirwad and in Q4 they took about 150 crs and in FY24 460 crs of impairments and provisions , even after this their NNPA is at 1.7 % - compared to other MFI the number is on the higher side.

If the Credit costs increase then it can impact the profitability of the company and my calculations

Happy Investing To All

Views are Welcome

Disc - Invested

What about holding company discount for manappuram? My understanding is that asirvad ipo is not going to be full value unlocking for manappuram as holding company discount will always be there. Correct me if am wrong

.

We are targeting an AUM growth of 20 per cent in MAFIL (Manappuram Finance Ltd) book

—————

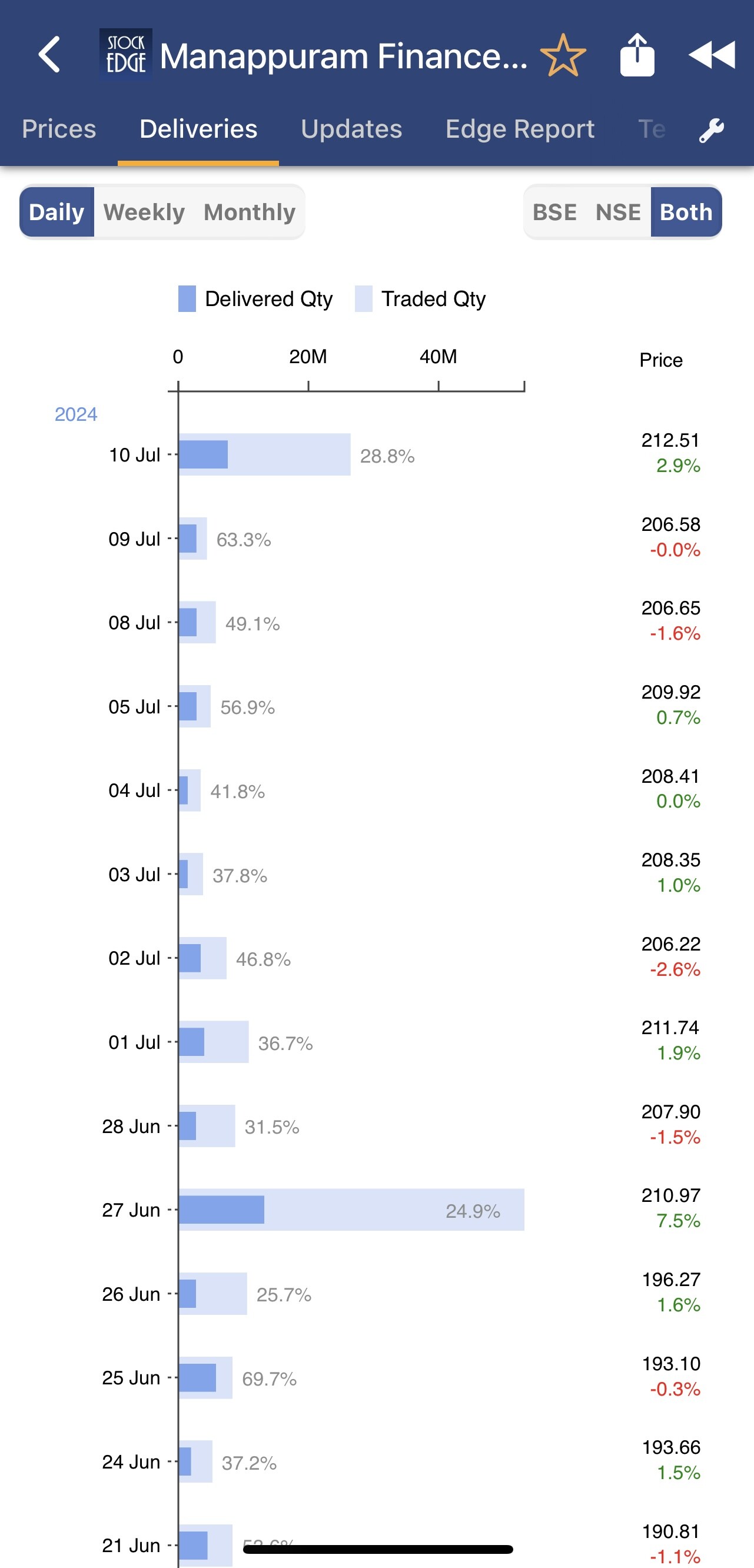

CLSA maintains “buy” rating, raises PT to 240 rupees from 220 rupees; says non-bank lender’s gold loan business has seen strong momentum since March, when India cenbank barred rival from disbursing such loans

——————-

Don’t know if it’s a coincidence, but both Muthoot & Manappuram are hiving off their microfinance subsidiaries at a time when there are signs of the cycle turning.

Irrespective of that, I think worth monitoring as MFI has done very well for them in the recent past.