Point No: 2 - promotors investing in personal capacity. This is just bad coporate governance. I couldn’t make out the management’s reply due to the bad audio quality of the concall.

1 Like

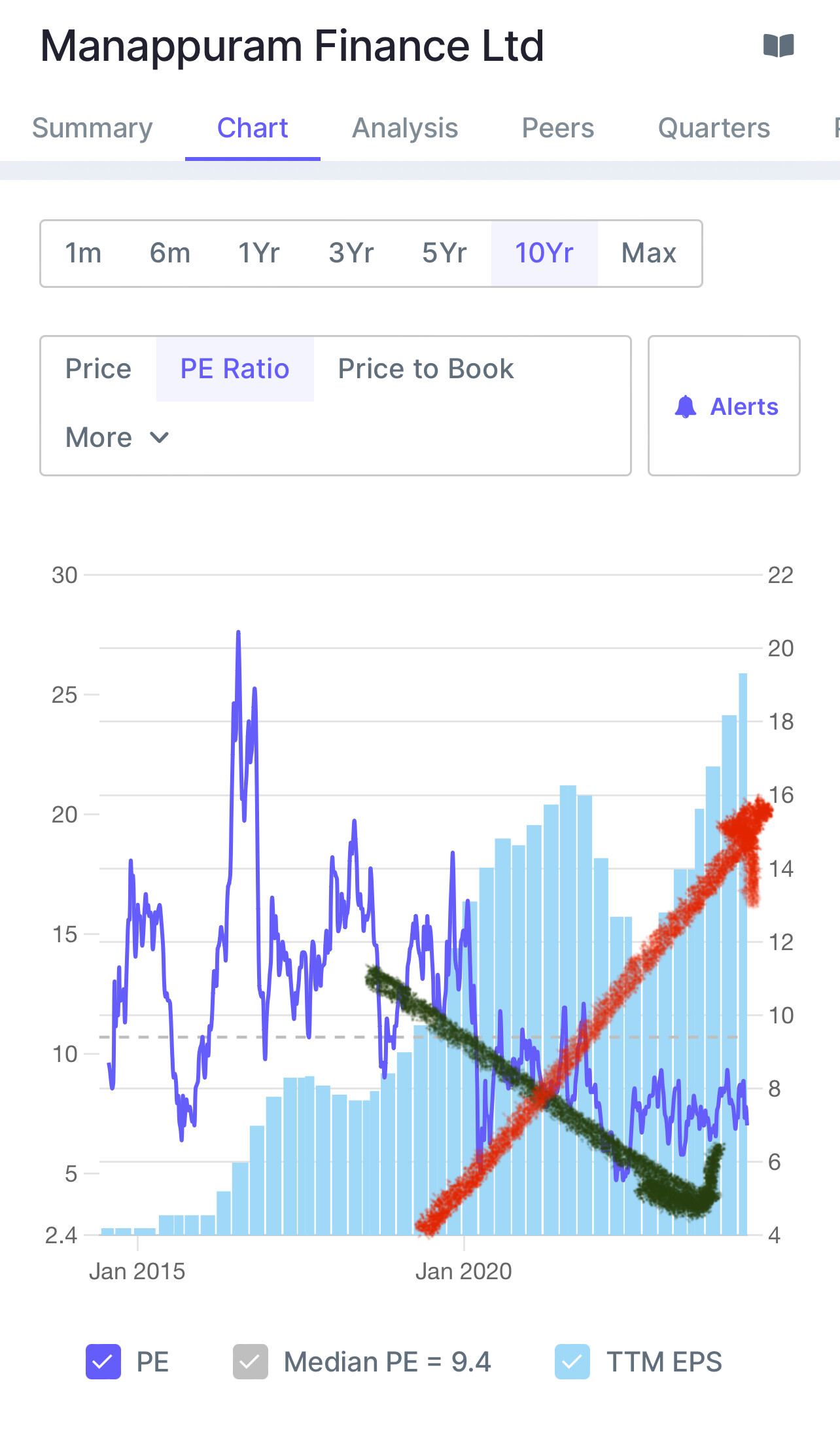

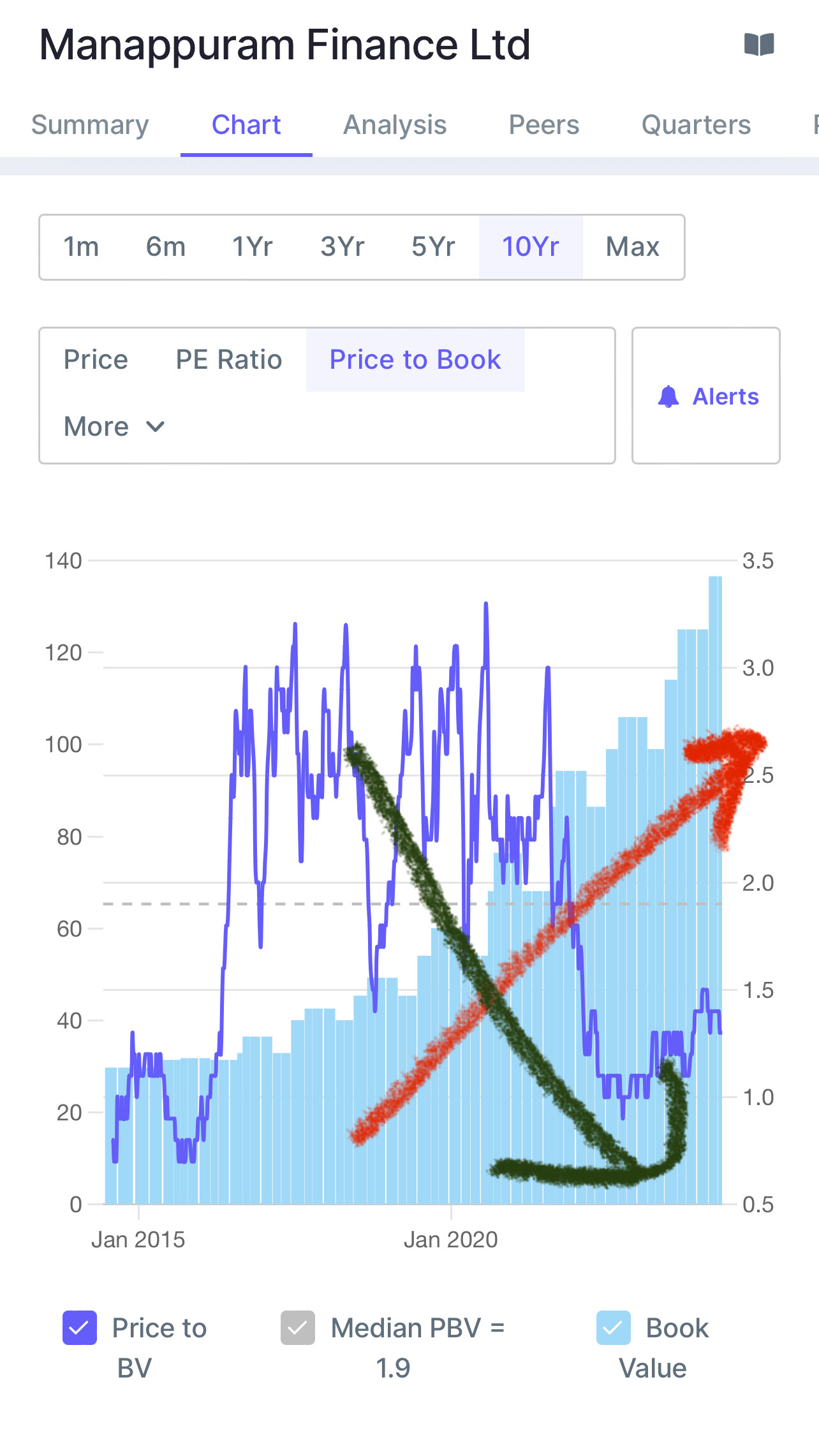

Intersting charts and data

Dividend ,EPS and BV going up

PE and P/book comimg down

Manappuram PE 6.98 x 2.5 = Muthoot PE 17.47

Manappuram P/book 1.32 x 2.2 = Muthoot PB 2.93

Gold price going up

4 Likes

with regards to Rights issue (calculations done only for 30/06/2023 issue, not for previous ones):

VP Nandakumar:

Shares subscribed: 16,012 Price:364; Total cost = (16012x364 = 58,28,368); Bonus Issue(26/08/2023): 2:1; Shares : 16012x3 = 48036. Total equity base: 200,283,372. Based on this Enterprise valuations at which Rights issue done: 2418 cr.

Shares subscribed by Manappuram in (4120879 no of shares) Rights issue: 4023144; Proportion: 97.62%. Current stake (pre-issue): 97.59%. Based on arithmetic, Manappuram subscribed to more shares it was entitled to, if minuscule in size.

Shares subscribed by VP Nandakumar in (4120879 no. of shares) Rights issue: 16012; Proportion: 0.388%. Current stake (pre-issue): 0.388%. Based on arithmetic, VP Nandakumar subscribed to similar shares it was entitled to (did not verify with higher decimal places).

Everybody is welcomed to form their judgements about valuations at which rights issue was done.

Promoters investing in personal capacity is also subjective, sometimes it is seen in positive light (skin in the game if not short changing others)

I was unable to find if VP Nandakumar took any remuneration or sitting fees. May be I missed it.

Disclosure: Invested.

PS: I would have liked if Asirvad got de-merged first and its shares were issued to minority shareholders. May be I would have sold my stake in Asirvad and practically brought overall cost of acquisition for Manappuram shares down. Similar to what happened in NMDC Steel de-merger and separate listing.

5 Likes

Management replied some other parties did not applied to rights issue (unclear whether he said they did not want to, but, he did say some due to cash constraints). So others over-subscribed.

2 Likes

if asirvad got listed separately then it will lose all the parental protection of manapuram including not able to expand operations through manapuram getting loans from parent and getting loans from third party at a discount and cross selling does not make sense to separate them except for short term gains in value as they say if you want to go faster go alone if you want to go further go together

other views are welcome

3 Likes

Sir , your answer seems quite philosophical…in terms common people understanding what is the best investor friendly way for Manappuram to list Asirvad? What are pros and cons of each way? Can you elaborate your views more clearly?

Tried to convert to text what I heard. It goes something like this.

“Promoters of Manappuram acquired the shares abdicated by the original shareholders during the rights issue- they don’t want to subscribe; they didn’t have the money. So whatever is the shortfall at the time of the rights issue, a portion has been acquired by Manappuram promoters.”

Given the fact that the promoters were acquiring the shares independently in Ashirvad starting from 2016, could there be any benign explanations for this which does not point out to bad intentions and conflicts of interest?

Invested.

3 Likes

Interesting data points.

Looking at parameters like:

NPA level (less than 2%),

Price to Book (less than 1.5),

Price to Earning ( around 7),

Sales Growth rate (5Y around 15% CAGR),

Profit Growth Rate (5Y around 18% CAGR),

Solid Capital adequacy (around 30%)

PEG ratio less that 1

Return on Equity (around 20%)

It seems like an experienced techie from Tier-1 IIT but employed at a salary of ITI fresher.

But looking at it under-performance over last 5 years (when rest of stocks in Indian Stock Market has moved to sky) - it seems perception among the masses (those who matters like large fund houses, well known Indian Investors etc.) is not yet good for Manappuram in recent times.

And without good perception, how long it will be on similar valuations - remains a guess.

Note: Got this investment note from Mr. Rajeev Agrawal, dated 24/05/2021 i.e. exactly 3 years back, when MCAP of Manappuram in USD terms was $1.863 billion. At today’s rate of USD/INR … It seems those FII’s who invested 3 years back gained nothing other than dividends.

Look forward to a catalyst, which will rerate Manappuram.

4 Likes

Please correct me if my understanding is incorrect.

In case original shareholders (Mr. Raja and others) were not having money to subscribe Right issue, rather than Mr. VP Nandkumar & Mr. Babu subscribing those available rights, Manappuram too was eligible to apply for these available additional rights. And if Manappuram would have subscribed these, promoters would have got indirect benefit.

But subscribing direct, they got preference over rest of shareholders of Manappuram like FIIs, DIIs, Retail shareholders.

Here quantum of direct holding by Promoters vs that of Manappuram must not be that material when it comes to doing right things in right spirit & intention.

3 Likes

Not sure how all analyst came to a single price target of 220 plus minus 5

No difference of opinion

Or is it just copy and paste ![]() by all national and international analysts

by all national and international analysts

3 Likes

MGFL-RR-26052024-27-May-2024-895157100.pdf (1.0 MB)

Manappuram Finance Ltd - Q4FY24 Result Update - 27052024_27-05-2024_11.pdf (848.6 KB)

Even Axis Securities giving a target of Rs. 220 as per attached report from them.

1 Like

With current situation looks like psu banks will suffer in next 5 years

And now private banks and NBFCs will go up

Also spending money on rural area will increase.

Again positive for Manappuram

1 Like

Many positives for mannapuram but still market is not giving valuations

I remember same happened with amara raja batteries

Could you explain why PSU banks will suffer and pvt banks will gain?

The related party transactions are a mess, both figuratively (education, rent waivers, rent paid/received, etc.) and literally (very difficult to read, the scanned pages are sometimes partially scanned and some section is not scanned properly).

2 Likes

On 24 May 2021

The Doordarshi advisors said “We expect that the company should grow PAT by 15% CAGR over the next few years (management has guided for faster growth).”

So now that we have benefit of hindsight, you can compare the actuals and the projections, In FY22, PAT went down by 22.xx%, in FY23, PAT went up by 12%, in FY24 it then went up by 46%, now you get a smoothened version, overall PAT grew by 8.39% CAGR in the last 3 financial years (((2,197/1,725)^(1/(2024-2021)))-1)*100

So now, we know what must we do with projections! Lest we still remain uninitiated, here’s Charlie Munger talking on projections:

2 Likes

Not much significant,not even 0.1 %

I am not sure these stream of news story updates are that useful. I understand you are invested and I hope it does well, but you seem to be looking at this only with a rose-tinted lens. It will be helpful if you can also highlight what are the things to watch out for.

I had invested earlier at lower levels and exited when it went up. I didn’t really find a good reason to hold on at 180-190 levels. Will the Aasirvad IPO (not sure when it’s finally happening) make a difference to the stock? What’s the rationale?

Munger at it’s best … no doubt projections are always at risk of going wrong.

I was going through the concall of Muthoot … where management guided 15% growth but delivered 20%, whereas Manappuram guided 20% and delivered approx. 19%.

No wonder, Muthoot command double the premium vs Manappuram.