I believe past valuation of book value at 3+ times is long gone in today’s environment where the business has structurally changed as the margins have compressed.

I agree with @tushar24’s view that this might be a good opportunity for Demerge of Asirvad to unlock value but then the gold business’s valuation will fall further as growth and margins both have structurally declined.

How much book value to give depends on time and circumstances which is different for everyone

I firmly believe in 3 plus book valuations in short to medium term

Let’s see what market decides

Now the ED issue is in their favour base will be formed in this month

Let’s see first the base valuations

It’s a roller coaster ride

Stock moving 50% plus and minus is not uncommon in this script

I concur with @maheshkumar MFL is highly volatile and once it starts its uptrend usually it flies in a short timeframe. This time is no different. As far as my understanding goes, the management will not demerge the microfinance unit atleast in the next 2 years.

Nanda is in talks with multiple PE players and they should bring one strategic investor to establish a baseline / benchmark the valuation for Asirvad Microfinance (before they demerge). @arjunbadola

There’s still a lot of overhead supply hanging on this stock and we need very strong hands to move it up against gravity. Let’s see how the events unfold.

Manappuram Finance Ltd to infuse Rs 146.40 cr equity in its subsidiary Asirvad Micro Finance Ltd through a rights issue

Manappuram Finance grants approval to apply for right issue of unit Asirvad Micro Finance. Co entitled to apply for shares worth up to Rs 146 crore at Rs 364/share

Does this mean company wants to sell non listed subsidiary Asirvad share to shareholders to raise the cash at 364 rupees per share of Asirvad microfinance?

Research conducted by domestic brokerage house, Yes Securities Ltd, suggests a promising trend in incremental market share for these companies. “Ground checks suggest some reverse migration of customers - many customers who had left for lower rates coming back, and notably both high-value and low-value customers," said the domestic brokerage house in a report dated 26 June. Reasons behind customers coming back include convenience, flexibility/ease of foreclosure, part prepayment/release and higher processing fees and documentation/other charges at bank

More good news flowing for Manappuram

Morgan Stanley - Manappuram can give outsized return

There is no official confirmation from the management on the above money control article. However, in a recent filing Mr. Shyju K (Head HR) was moved from MFL to AMF to take up new responsibilities. There is some kind of reorg happening for sure but can’t say with confidence if it is for the de-merger. Only time will tell if the news is true.

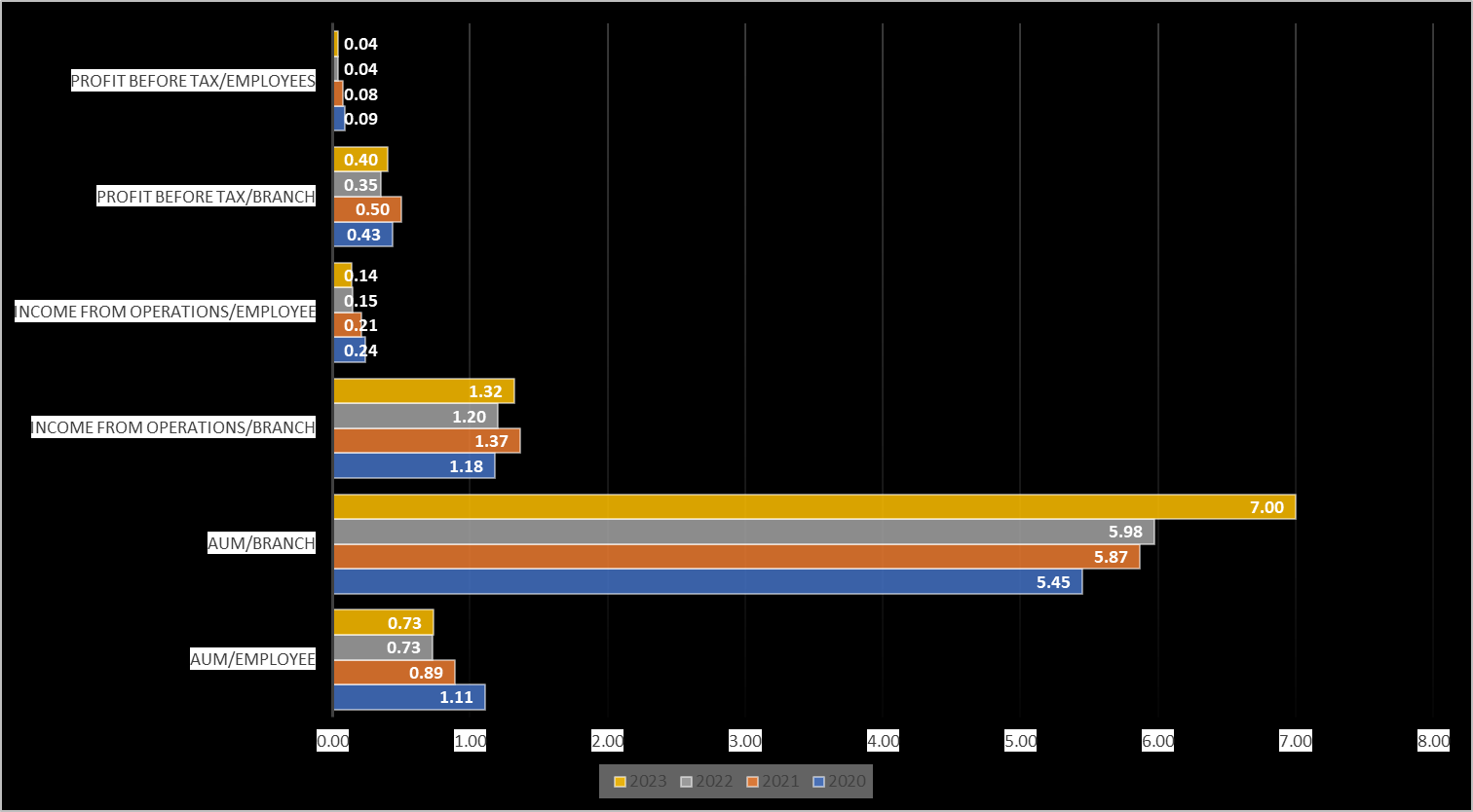

the company seems to have aggressively hired new employees and hence there is a fall in AUM and income per employee

income per employee fell from 24 lacks in 2020 to 14 lacks at 2023

PBT per employee fell from 9 lacks to 4 lacks

AUM per employee from 1.1 crore to 73 lacks

on the branches front

AUM per branch increased from 5.45 crores to 7 crores per branch

income per branch at 1.1 crore to 1.32 crores

PBT per branch from 43 lacks to 40 lacks

this tells us the new employees might generating more revenue soon or later the relative expansion of branches from 4622 to 5057 must also be factored in

and also, the employees from 22726 to 48396 from 2020 to 2023

Hi, Can someone please throw some light on the Asirvad Microfinance IPO and how it can unlock the value of existing shareholders ? Any valuation insights will be very helpful.

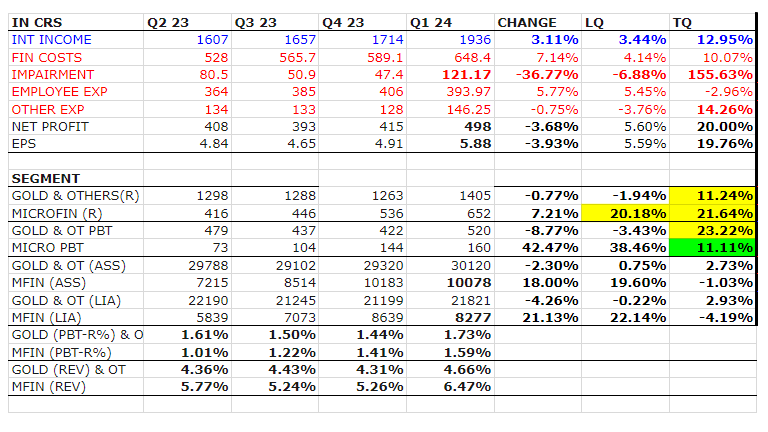

Good to see QoQ PAT growth in a seasonally weak quarter. This is in line with many top of the line MFI cos this cycle. But the PAT growth could have been much better if not for high credit costs. Credit costs this Q are quite high, my estimate is around 3.5% annualized whereas most other MFI cos are reporting sub 1% credit costs. If not for this they would have been on track for a standout Q this time.

This time Gold & others segment gave a turn around vs neutral performance in microfinance (apx 80crs increment as impairment cost which in turn could not give similar growth in profit as of revenues). Overall good performance after a long struggling time.

1.Yield improved sequentially and guided for 21-22%.

2.Guided for 10-12% AUM growth.

3.Cost of funds went up by 18 basis points and they expect another 20 basis point in this quarter as well.

MFI

1.AUM growth muted sequentially due to liquidity issues, they slowed disbursement for a month,expect 30% growth annually.

2.Yield is around 25% in MFI.

3.Cost of funds went up by 50 basis points in Ashirvad,expect cost to stay around similar level in subsidiary.

4.Credit cost will come down and they expect it around 2%.

5.They are looking for capital in Ashirvad,nothing concrete as now(PE/IPO),don’t want to sell it completely.

Other business(VF/HF/MSME)

1.Want to grow AUM by 35-40%.

2.Asset quality is stable.

My thoughts

ED issue is now behind us and MFI profitability is going to go up sequentially.Book value after Q1 is 119 and 135 for FY24 is looking doable now.PAT for whole year will be in excess of 2000cr.Analysts are still behind the curve and upgrades will follow.If they can grow gold loan AUM in coming quarters then we may see some valuation rerating as well.