———————————————————

Conference call :

Conference call transcript:

————————————————————

Vp nandkumar

Hopeful of 20% consolidated CAGR and ROE

———————————

Research reports bullish now

Motilal oswal

———————————————————

Conference call :

Conference call transcript:

————————————————————

Vp nandkumar

Hopeful of 20% consolidated CAGR and ROE

———————————

Research reports bullish now

Motilal oswal

This is the second block in the current week. Correct me if I am wrong please!!

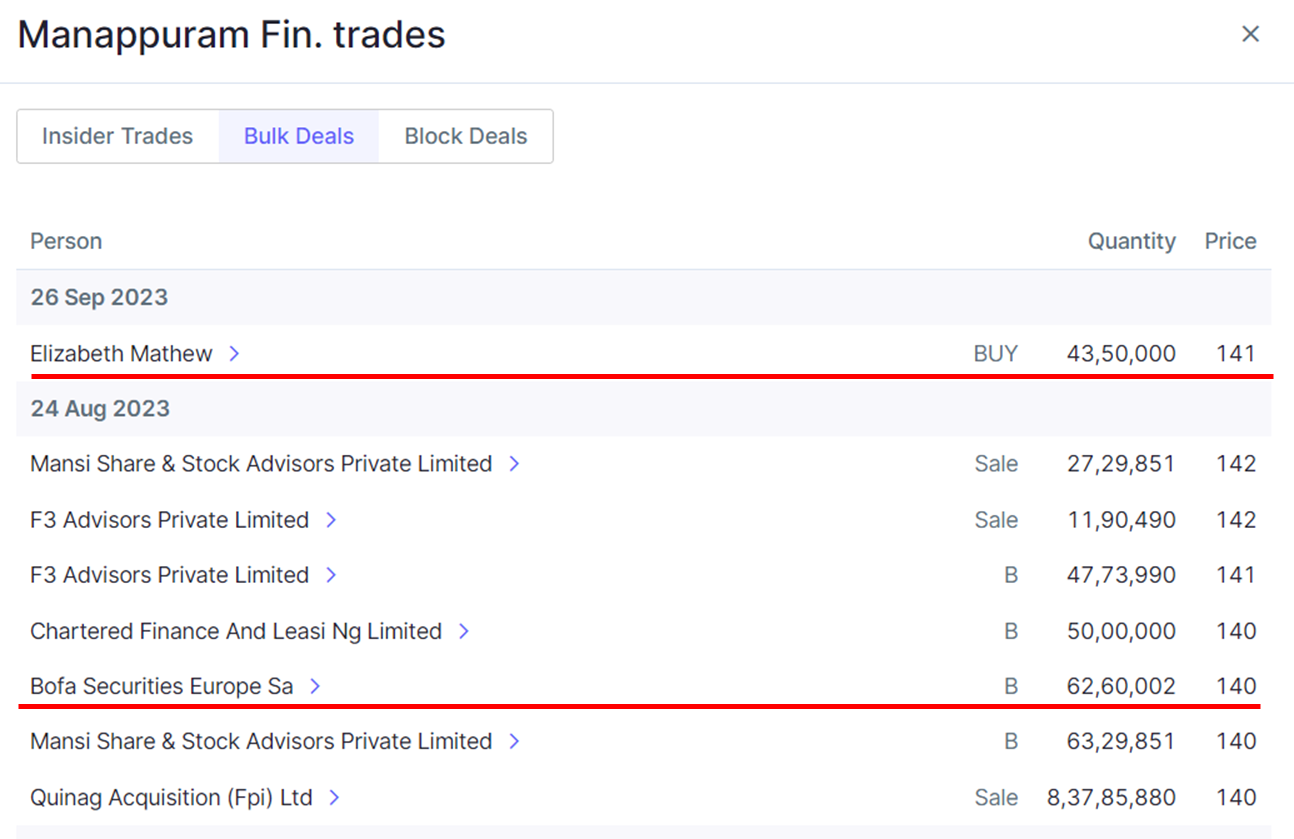

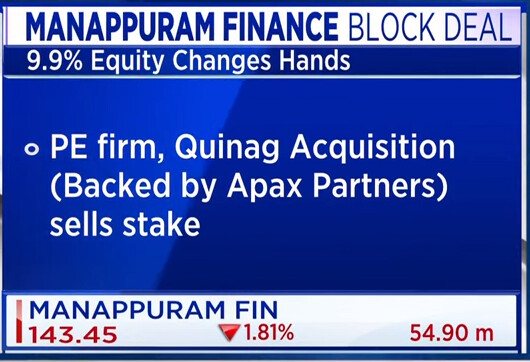

Mannapuram Finance-Bulk Deal

Buyers - Chartered Finance & Leasing & BoFa Securities

Seller-CDC Group (PE Player)

Buying and selling are common. BoFA can be considered as a serious investor. Market has absorbed the volume of sell.

Edit: information source is social media - veracity is always a suspect. Eg Godrej Aerospace was touted as a supplier when Chandrayaan 3 landed and Godrej Industries (GI) shot up. GI have since then denied involvement.

Seller Quaing

Buyer bofa ,chartered finance and few unknowns

Always intersting buyer always have a reason to buy and seller has a reason to sell

50:50 chance that one is right and one is wrong

Let’s see who wins the short mid and long term game

The other way to look at it is seller may have many reasons to sell not linked to business, like redemption, better opportunities elsewhere etc etc……buyer read investor has primarily one reason to buy value and opportunity in business.

[#ManappuramFinance] says Kerala High Court quashed Enforcement Case Information Report registered by Enforcement Directorate.

Crisil and other rating agencies as well as brokerages are now Turning positive with setting targets 175+

Hopefully should reach all time high in 6-12 months

FY 25 expected PE will be around 5

Standalone Profile Drives Ratings: MFIN’s ratings reflect its moderate franchise in semi-urban and rural consumer lending, particularly in gold-backed loans, which constitute 56% of the consolidated portfolio. The ratings also reflect steady asset quality from the liquid collateral and generally stable funding access. This is balanced by a shifting business mix that reflects a high risk appetite and a history of regulatory compliance findings.

Improved Sector Risk Operating Environment (SROE): Fitch has revised the SROE score for Indian finance and leasing companies (FLCs) to ‘bb+’, from ‘bb’, reflecting improved governance, risk and liquidity management frameworks, due partly to regulatory strengthening in the past few years, and the easing of Covid-19 and commodity shocks on medium-term growth prospects, despite lingering global growth and inflation risks. We expect resilient GDP expansion (financial year ending March 2024 (FY24): 6.3%, FY25: 6.5%) to provide adequate headroom for FLCs to expand profitably in the medium term.

VP Nandkumar MD CEO Manappuram:

-we expect to close the financial year with a 10-% y-o-y growth rate in gold loan AUM on a conservative basis

We have ventured into many new verticals such as hospital loans/loans for medical professionals, teachers’ loan, credit to retail trade, hotels, food processing industry, mahila micro credit and small business loans. Another focus area for us is the affordable home finance and vehicle segment.

isn’t the guidance for gold different from the latest concall? I believe they guided for a 10-12% rise due to customer addition while gold price variation to be in addition to that.

I guess 10-12 % range means 10% on conservative side,which is what he said in interview

many of the banks have slowly begun to cut back on their gold loan business.

third quarter should be good for them, due to festive demand as well, If all parameters falls in place with growth back in gold, it should cross 2000 in Rev and 520-550 in profit

Very good article…and very good understanding of the business. This is what manappuram had also written in its Annual report.

Buying from 89 levels and have Average price of 105 rupees for last 1.5 years.

positive development

Manappuram Finance arm Asirvad Micro Finance IPO DRHP with SEBI, to raise up to ₹1,500 cr via fresh issue of equity shares