Good results from Manappuram subsidiary - asirvad microfinance https://amlcdn.b-cdn.net/img/Financial-Result-FY-23.pdf

9 Likes

Yes, Results are good. slightly higher than my expectations in both revenue and profit terms. On a whole year base from next year onwards should cross 2500 Revenue with a profit around 450. Lets see how does it pans out

Hopefully Malappuram also gives in similar lines

3 Likes

Results

https://www.bseindia.com/xml-data/corpfiling/AttachLive/a37290b5-8cb8-4b87-bbe4-b331b1e0dcd3.pdf

Investor presentation

3 Likes

Manappuram Q4 Concall highlights

Gold Loan

1.Product tenor has changed to 6 month now completely.

2.Expecting 10% increase in AUM.

3.Yield will be around 22.5% … Current yield is 21%… will increase slowly and till Q3 they will reach here.

4.Banks are not that aggressive now as they are getting less liability growth and asset growth is high.

MFI

1.They

1.Next year expected AUM growth of 35-40%.

2.They will infuse 500Cr equity and also Tier 2 capital.

3.They are also in talk with bankers about how to raise funds.

4.Do not want to expand branches.

In other business they expect growth north of 50%.

ED Case

They got a stay order from Kerala highcourt on Friday … Expecting further favourable outcome in coming days on defreezing assets.

My interpretation

As business was expected to show good performance,this ED issue came out of nowhere. I think risk here is on funding side. How lenders react after ED issue?(though management says they were aware of same since long).

Otherwise they are on a path to 20% ROE by end of this year.

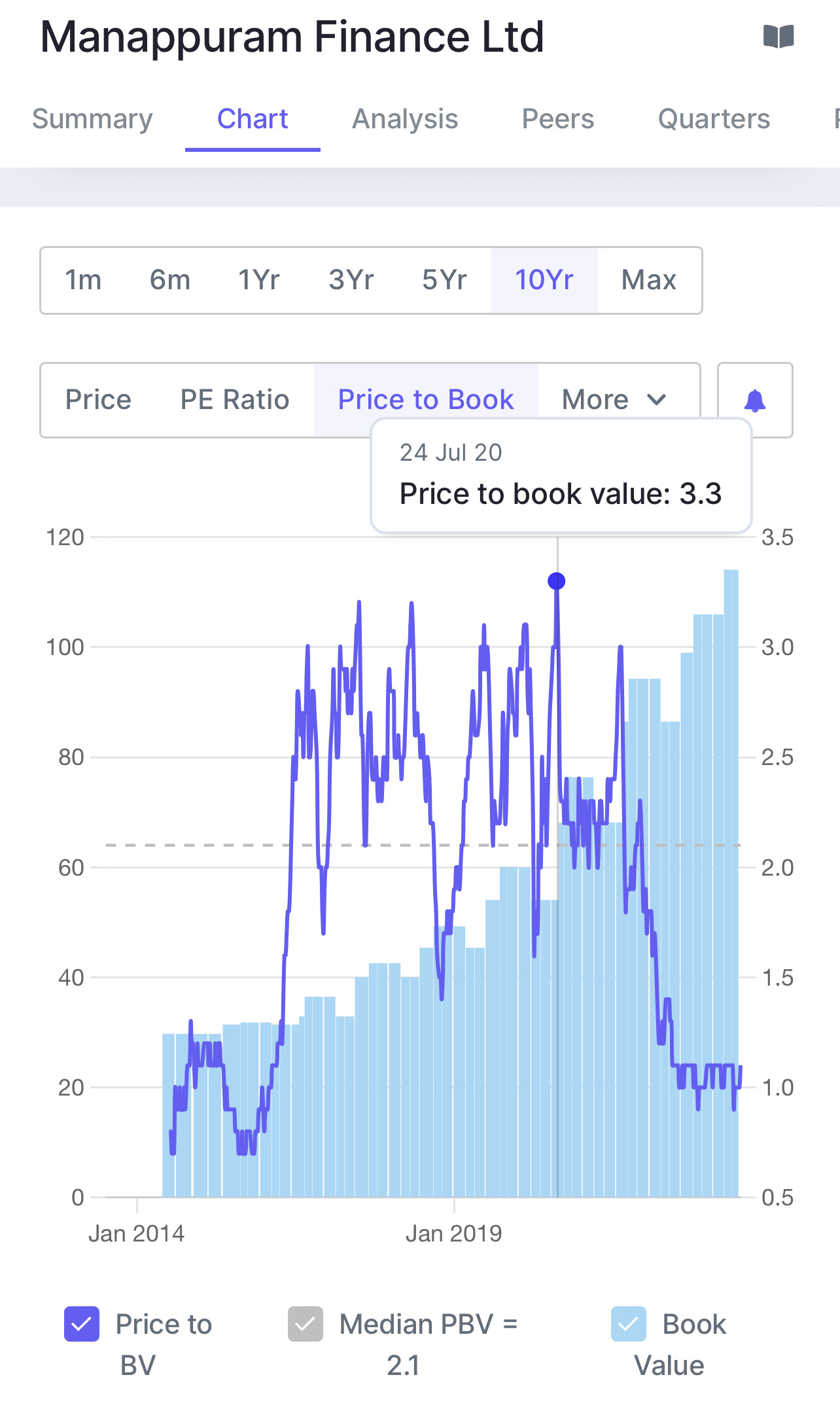

Valuation

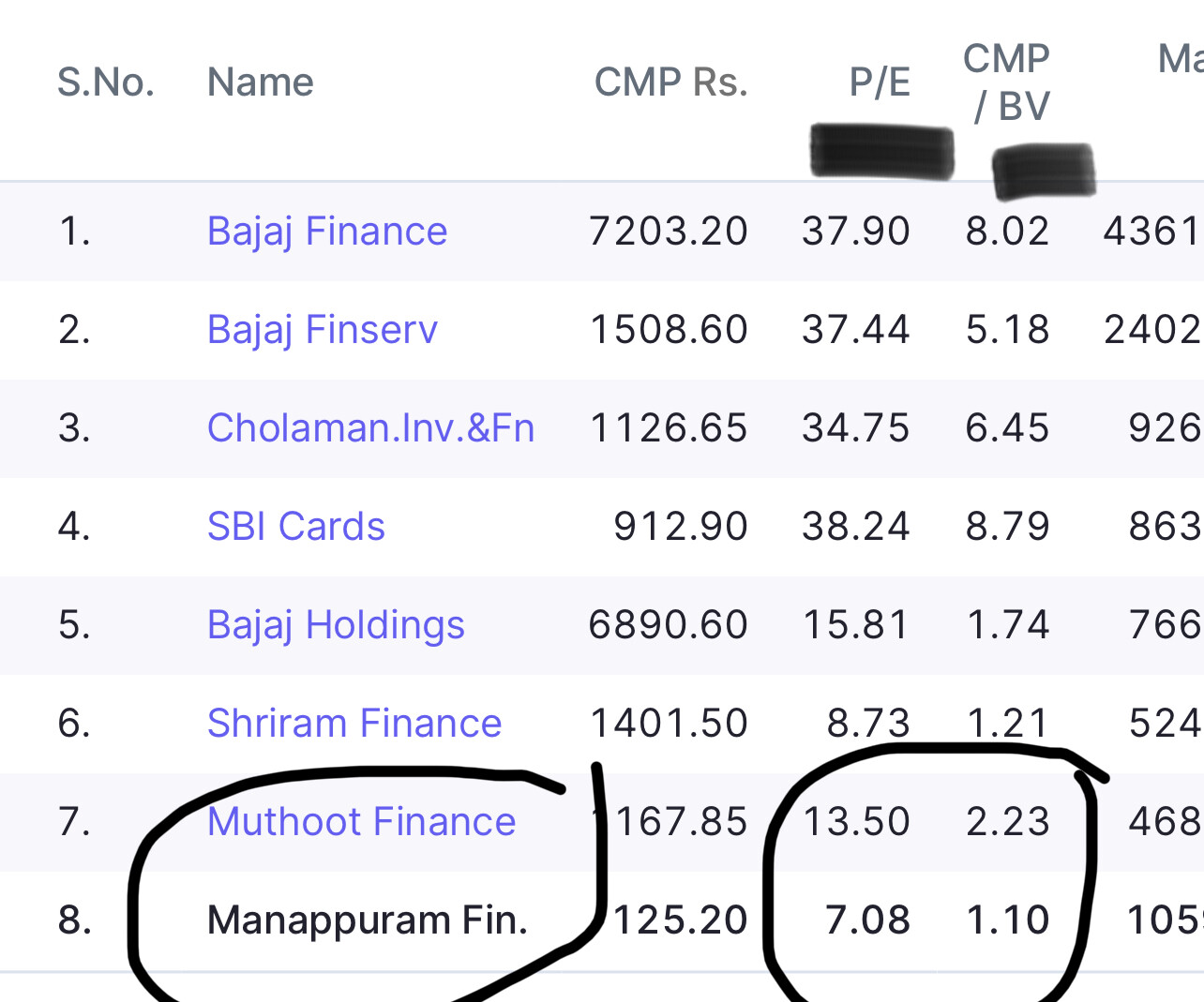

1.If we look at gold lender Muthoot is valued at 2 times book.

2.All pure MFI(Credit acces,Arman,Fusion) are valued at 2-4times book.

Manappuram current book Value is 114.

FY 24 will be near 135.

13 Likes

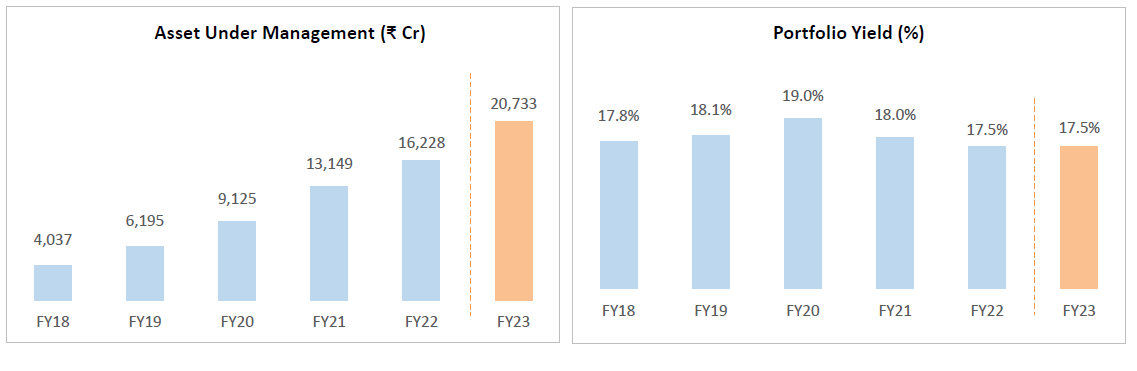

Good results from Manappuram Finance. Went through the results and PPT, yet to listen to the concall.

FY23 ROE 16.6%, Q4 ROE 17.5%

YoY AUM growth 17.2% (In spite of Gold AUM de-growth by 2% YoY)

Non gold to gold AUM ratio: 44% vs 56%

YoY PAT growth 59%

Consol CRAR 32%

Cost of borrowings steady at 8.2%

Asirvad:

YoY AUM growth 43%

Credit costs for FY23 down to 2.7% from 5.6% last year

NIMs steady YoY

Collection efficiencies remain strong at 104%

GNPAs down to 2.7% from 6.7% a quarter ago; NNPA 1.2%

Capital adequacy ratio 20%

Q4 ROE annualised 26%, FY23 ROE 17%

Cost of borrowing steady at 10%

27% YoY increase in no of borrowers (All MFIs are reporting strong growth nos)

Housing Finance GNPA nos have come down significantly. HFC, VF, MSME/personal finance are all showing decent growth with improving credit quality in line with most financial instruments.

Manappuram is trading at 0.96x PB now. With some uptick in GLs and a strong MFI cycle, consol quarterly annualized ROEs can start hitting 20% very soon. The ED overhang, while related to a very old case, can be a near term overhang for sentiments around the stock. But at 0.96x PB, most of the bad news seems already in the price.

Disc: Invested and biased.

14 Likes

The concern now though is that their Gold Loans business is still not growing. All this growth is based on segments which are riskier than the easy cash-making Gold Loan segments. I understand that that was the strategy but then the risks involved have completely changed now, haven’t they?

MFI is heavily linked to the economic cycle. HF and VF have collateral liquidity risk. A question did arise to me, has the company become more fragile from diversification rather than stronger?

Would love to hear y’all’s opinions on this

Disc: Invested

5 Likes

Kerala high court order for stay on ED investigation for 2 weeks.

215700156512023_1.pdf (88.8 KB)

Promoter has said that he is trying for quashing of the investigation but will take multiple hearings as courts need to hear the other side’s argument too.

Management has also clarified that there are no changes to their funding terms with their stakeholders and has gotten funding even after the raid on similar terms as before.

6 Likes

2 Likes

why is there a difference in interest income -6440 crores and finance cost -2187 crores in profit and loss statement in 2023 march

Were as in cash flow statement for the year 2023

There is interest income-(4674) why is it is not equal to the profit and loss statement

There is interest received on loans -4579 what is the difference between interest income and this

and also there is finance cost-1546 why finance cost does not match with profit and loss statement

can some one explain the rationale behind this ?

Muthoot cash flow statement is easy to understand

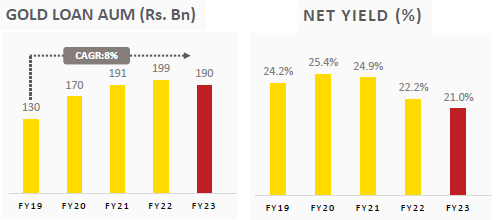

FY2023 end IIFL Finance Ltd (IIFL) has overtaken Manappuram in Gold AUM base though on yield basis Manappuram still is much better compared to IIFL. So, now Manappuram is 3rd largest lender against gold in NBFC space; 1st being Muthoot Finance followed by IIFL.

From FY2019 to FY2023, IIFL gold loan AUM grew 3x while for Manappuram it grew by 1.5x.

Muthoot Gold loan though on a larger base (FY2019) has grown at a faster rate 1.8x than Manappuram (1.5x).

Conclusion- Though industry pie for gold loan is increasing, Manappuram is losing out to incremental growth to competitors it seems.

IIFL (Gold loan AUM)

Manappuram (Gold loan AUM)

Muthoot (Gold loan AUM)

4 Likes

I think the writing is on the wall.

Gold loan biz is fully matured and is likely to stagnate.

MFI is the growth engine with VF, HF, MSME trailing it.

All listed MFIs trade between 1.5x PB - 4x PB (Spandana, Fusion, CAG)

Asirvad MFI has AUM of 10,000 crs with ROA of 4%, ROE 20%+ and decent NPA ratios

Yet as a whole available at 1x PB due to gold loan biz drag and recent ED issue.

Management has a very good opportunity to IPO/Demerge Asirvad given Asirvad is sitting at 5x Leverage and has to raise equity capital anyhow.

All MFI stocks have been on a roll the past 1 year and paper will be absorbed quite easily (contingent on ED matter being quashed)

Beneficial to all stakeholders involved due to value unlocking and every entity being judged on its own merit.

8 Likes

Loan never saturates dosen’t matter if it’s gold or personal loan

We all need loan

Even in developed countries people take personal loan at higher interest rate than gold loan

Everyone need working capital

Only difference is in sentiments which changes with price , at lower prices every positive becomes negative and at higher prices , negative news is also digested very easily

1 Like

Kerala High Court case update order on 25-05-2023

“Treat as admitted. …Interim Order … extended by 2 months. … Both sides agree… Post for hg as per Roster next week.”

2 Likes

Can u share the link of kerla court order

1 Like

Number of loans requests initiated and/or processed through this lending app would be another important metric to track going forward. Moving to digital platforms eventually is inevitable so you might as well start early and iron out all issues sooner rather than later.

8 Likes

Here is my analysis report on Manappuram Finance which I did in February 2023. Figures have been taken mostly uptil FY 2022. Need suggestions and feedback from what you guys think of it specially from the admin team.

Link -

MANAPPURAM ANALYSIS.pdf (253.5 KB)

Disclosure : Invested at the time of posting this.

18 Likes

MANAPPURAM FINANCE: CO RECEIVED UPDATE FROM PROMOTER V P NANDAKUMAR OVER A CASE AGAINST HIM || PROMOTER INFORMED THAT HIGH COURT OF KERALA HAS QUASHED AN FIR FILED BY VALAPAD POLICE STATION

Kerala high court squashed the case

12 Likes

Penalty Manappuram vs HDFC

Even HDFC has some minor irregularities

Trading at half valuations than muthoot

In past they at times Manappuram valuations were up to 3.5 booo

5 Likes

I think quashing of FIR is big positive for Manappuram. The way the management has responded during ED raid is appreciable. Hearing the management in concall, gives the feeling that management is telling the truth and complainant had some very old , past grudge against the promoter family. I along with my wife accumulated a lot of manappuram shares based on our capacity.

Let see how much correct is our decision. Fingers crossed and thanks a lot @maheshkumar and @Malkd

Disclosure: Holding and buying from 89 levels and last buying at recent fall.

3 Likes